Global Edema Treatment Market

Размер рынка в млрд долларов США

CAGR :

%

USD

3.14 Billion

USD

5.60 Billion

2025

2033

USD

3.14 Billion

USD

5.60 Billion

2025

2033

| 2026 –2033 | |

| USD 3.14 Billion | |

| USD 5.60 Billion | |

| % | |

|

Global Edema Treatment Market Segmentation, By Type (Peripheral Edema, Pedal Edema, Lymphedema, Pulmonary Edema, Cerebral Edema, Macular Edema, and Others), Treatment (Diuretic, Anti-allergic, Blood Thinners, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy)- Industry Trends and Forecast to 2033

Edema Treatment Market Size

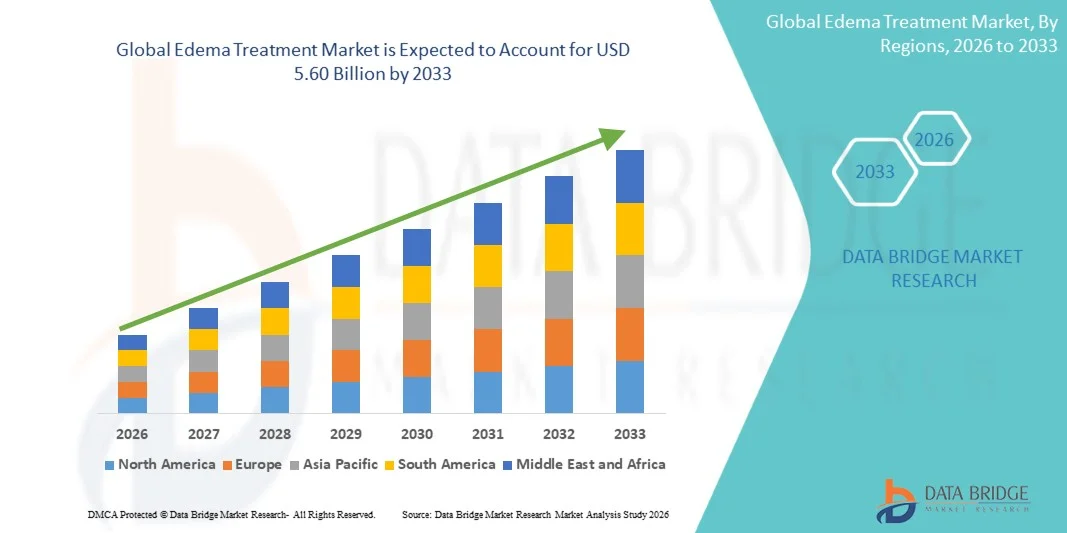

- The global edema treatment market size was valued at USD 3.14 billion in 2025 and is expected to reach USD 5.60 billion by 2033, at a CAGR of 7.50% during the forecast period

- The market growth is largely fueled by increasing incidence of chronic illnesses linked to fluid retention, innovations in treatment modalities (including diuretics, blood thinners, and compression therapies), and heightened awareness among healthcare providers and patients, leading to broader adoption of effective edema management solutions across clinical settings

- Furthermore, government and private investments in clinical research for novel edema therapies, expanding geriatric population vulnerable to edema, and enhancement of healthcare facilities in emerging regions are supporting market expansion establishing comprehensive treatment options for both localized and systemic edema

Edema Treatment Market Analysis

- Edema treatments, encompassing pharmacological therapies such as diuretics, anti-allergic drugs, blood thinners, and other therapeutic interventions, are increasingly essential in managing fluid retention disorders across both acute and chronic clinical settings, improving patient outcomes and overall quality of life

- The growing demand for edema treatments is primarily driven by the rising prevalence of chronic diseases such as heart failure, kidney disease, liver cirrhosis, and lymphedema, coupled with increasing awareness among healthcare providers and patients about early intervention and effective management strategies

- North America dominated the edema treatment market with the largest revenue share of 39.5% in 2025, attributed to advanced healthcare infrastructure, high healthcare spending, strong reimbursement policies, and a well-established pharmaceutical industry. The U.S. saw substantial adoption of innovative therapies targeting edema, particularly in the management of peripheral and pulmonary edema

- Asia-Pacific is expected to be the fastest-growing region in the edema treatment market during the forecast period, fueled by increasing incidence of chronic diseases, expanding healthcare infrastructure, rising awareness about edema treatment options, and improving access to healthcare in emerging economies

- Peripheral edema segment dominated the edema treatment market with a market share of 31.2% in 2025, driven by its high prevalence among patients with cardiovascular and renal conditions

Report Scope and Edema Treatment Market Segmentation

|

Attributes |

Edema Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Edema Treatment Market Trends

“Advancements in Targeted and Personalized Therapies”

- A significant and accelerating trend in the global edema treatment market is the development of targeted therapies for specific edema types, such as lymphedema, pulmonary edema, and macular edema, enhancing treatment efficacy and patient outcomes

- For instance, recent innovations in lymphedema therapy include wearable compression devices that deliver personalized pressure levels, improving lymphatic drainage and reducing discomfort for chronic patients

- The integration of digital monitoring with edema treatments enables remote tracking of fluid retention, adherence, and therapy effectiveness, allowing clinicians to adjust regimens based on real-time patient data

- For instance, mobile applications paired with smart wearable sensors can alert patients and healthcare providers to abnormal swelling, supporting early intervention and reducing hospitalization rates

- Growing research in novel drug formulations, such as sustained-release diuretics and anti-inflammatory agents, is improving therapeutic outcomes while minimizing adverse effects

- This trend toward personalized, data-driven, and patient-centric edema management is reshaping treatment standards, prompting pharmaceutical and medical device companies to focus on precision therapies

- The demand for edema treatments incorporating advanced monitoring, tailored drug dosing, and integrated therapy solutions is rising rapidly across both hospital and outpatient care settings, as patients and providers increasingly prioritize efficacy and quality of life

Edema Treatment Market Dynamics

Driver

“Rising Prevalence of Chronic Diseases and Aging Population””

- The increasing incidence of cardiovascular, renal, and hepatic disorders, combined with a growing geriatric population, is a significant driver of heightened demand for edema treatments

- For instance, in 2025, pharmaceutical firms introduced new combination diuretics aimed at patients with heart failure and chronic kidney disease, targeting both fluid retention and electrolyte balance

- As healthcare providers focus on early diagnosis and intervention, edema treatments offer enhanced management of fluid retention, reducing complications and improving patient outcomes

- For instance, outpatient clinics are increasingly prescribing integrated therapy plans combining pharmacological and compression treatments to manage peripheral and pedal edema effectively

- Furthermore, expanding healthcare access in emerging regions and increasing awareness of edema management options are making effective therapies more widely adopted

- Increasing investments in clinical trials and R&D by pharmaceutical companies are accelerating the launch of next-generation edema treatments

- For instance, companies are evaluating novel anti-fibrotic and lymphatic-targeting agents to address lymphedema and pulmonary edema, creating new market opportunities

- Technological integration, such as wearable edema monitoring devices, is enhancing patient adherence and therapy personalization. For instance, hospitals are implementing sensor-based compression systems that track swelling and automatically adjust therapy pressure, improving patient compliance

Restraint/Challenge

“Side Effects and Access Limitations”

- Concerns regarding potential side effects of pharmacological therapies, including electrolyte imbalances and allergic reactions, pose a significant challenge to broader market penetration

- For instance, diuretics, while effective, can lead to dehydration or electrolyte disturbances if not properly monitored, making some patients hesitant to continue treatment

- Limited access to specialized therapies in rural or underdeveloped regions restricts the adoption of advanced edema management solutions

- For instance, patients in low-income areas may have limited availability of compression devices or targeted therapies, relying mainly on general diuretics with less personalized efficacy

- Ensuring patient adherence, monitoring adverse reactions, and expanding equitable access to therapies are crucial for sustaining market growth. For instance, hospital outreach programs and telemedicine initiatives are being developed to improve treatment adherence and overcome geographic and socioeconomic barriers

- High cost of advanced therapies, particularly in private healthcare systems, can limit patient uptake and slow market penetration in price-sensitive regions. For instance, wearable compression devices and novel combination drugs often come with premium pricing, making them less accessible in developing countries

- Regulatory challenges and delayed approvals for new edema therapies in certain regions may impede market expansion

- For instance, delays in clinical trial approvals or reimbursement approvals can slow the launch of innovative treatments, limiting timely access for patients

Edema Treatment Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-user, and distribution channel.

- By Type

On the basis of type, the edema treatment market is segmented into peripheral edema, pedal edema, lymphedema, pulmonary edema, cerebral edema, macular edema, and others. The Peripheral Edema segment dominated the market with the largest revenue share of 31.2% in 2025, driven by its high prevalence among patients with cardiovascular and renal disorders. Peripheral edema often requires continuous monitoring and pharmacological management, creating steady demand for diuretics and combination therapies. Clinicians prefer established treatment protocols for peripheral edema due to predictable outcomes and effectiveness in reducing fluid retention. The segment benefits from widespread awareness among healthcare providers and patients, ensuring strong adoption in hospitals, specialty clinics, and homecare settings. In addition, ongoing R&D and new drug approvals for peripheral edema management further support its dominance. The segment also sees stable growth due to integration with digital patient monitoring tools that enhance therapy adherence and treatment efficacy.

The Lymphedema segment is anticipated to witness the fastest growth rate of 9.1% from 2026 to 2029, fueled by increasing awareness of lymphatic disorders and rising demand for personalized therapies. Lymphedema treatments include compression devices, physiotherapy, and novel pharmacological options, which are gaining traction in both hospital and homecare settings. The growing geriatric population, post-cancer treatment patients, and expanding healthcare infrastructure in emerging economies are key growth drivers. Moreover, technological integration, such as wearable monitoring devices, supports real-time tracking of limb swelling, enhancing patient compliance. Increasing investments in R&D for targeted lymphedema therapies are attracting new players into the market. The segment’s growth is also supported by awareness campaigns and insurance coverage expansion in several regions.

- By Treatment

On the basis of treatment, the edema treatment market is segmented into diuretics, anti-allergic, blood thinners, and others. The Diuretics segment dominated the market with the largest share of 42.7% in 2025, driven by their established clinical efficacy in managing fluid retention and reducing swelling. Diuretics are widely prescribed for conditions such as heart failure, kidney disease, and hepatic disorders, making them a cornerstone of edema management. The segment benefits from well-defined dosing protocols, ease of administration, and broad adoption across hospitals, homecare, and specialty clinics. Pharmaceutical companies continue to innovate with combination therapies and sustained-release formulations, enhancing the therapeutic impact of diuretics. In addition, diuretics are cost-effective compared to newer or specialized treatments, increasing their accessibility in emerging regions. Their proven safety and predictable outcomes ensure that diuretics remain the preferred choice for clinicians managing both acute and chronic edema.

The Blood Thinners segment is expected to witness the fastest CAGR from 2026 to 2029, fueled by the rising prevalence of edema associated with thromboembolic disorders. Blood thinners, such as anticoagulants, are increasingly used in patients with pulmonary or cerebral edema to prevent complications from vascular blockages. Growing awareness among healthcare professionals about the dual benefits of edema reduction and cardiovascular risk mitigation drives adoption. Technological advances in monitoring and dosing protocols reduce the risk of adverse effects, encouraging wider usage. In addition, expanding patient populations in aging societies and post-surgical care settings support the growth of this segment. Blood thinners are also gaining traction in specialty clinics and outpatient care, contributing to rapid market growth.

- By Route of Administration

On the basis of route of administration, the edema treatment market is segmented into oral, parenteral, and others. The Oral segment dominated the market with a share of 61.3% in 2025, due to the convenience, ease of self-administration, and established efficacy of oral pharmacological therapies. Oral drugs such as diuretics and anti-allergic medications are widely used across hospitals, homecare, and outpatient settings. Patients prefer oral administration for chronic edema management because it reduces hospital visits and improves adherence. The segment is supported by continuous product innovations, including combination tablets and sustained-release formulations. Oral administration also benefits from global regulatory approval pathways that facilitate market entry and distribution. High physician preference for oral medications and patient familiarity ensure the dominance of this route.

The Parenteral segment is expected to witness the fastest CAGR from 2026 to 2029, driven by increasing use in hospital-based acute edema management and severe cases. Parenteral administration allows rapid fluid reduction and precise control over therapeutic effects, making it suitable for pulmonary, cerebral, and macular edema. Technological advancements in infusion systems and improved formulation safety have further accelerated adoption. Parenteral treatments are especially favored in intensive care units, emergency rooms, and specialty clinics. Rising hospital infrastructure in emerging markets is also contributing to the segment’s rapid growth. The segment benefits from integration with clinical monitoring tools that optimize dosing and enhance patient outcomes.

- By End-User

On the basis of end-user, the edema treatment market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the market with the largest share of 55.6% in 2025, owing to the high incidence of acute and chronic edema cases requiring intensive monitoring and treatment. Hospitals provide comprehensive care with access to pharmacological, parenteral, and specialized therapies. The segment benefits from the presence of trained healthcare professionals, advanced diagnostic tools, and structured treatment protocols. Hospitals also facilitate clinical trials and the introduction of novel therapies, further strengthening their market position. Patients with severe edema often rely on hospital-based care for rapid symptom relief and therapy optimization. Moreover, the segment’s dominance is supported by government and private healthcare investments improving hospital infrastructure.

The Homecare segment is expected to witness the fastest CAGR from 2026 to 2029, driven by increasing demand for convenient, at-home edema management solutions. Homecare services include oral medication adherence, compression therapy, wearable monitoring devices, and telemedicine support. Rising awareness among patients and caregivers about early intervention and continuous monitoring contributes to the segment’s growth. Technological advancements in wearable and smart devices allow remote tracking of swelling, fluid retention, and therapy effectiveness. Expanding insurance coverage for homecare services in several regions further supports adoption. The segment is also driven by patient preference for comfort, reduced hospital visits, and personalized care plans.

- By Distribution Channel

On the basis of distribution channel, the edema treatment market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Hospital Pharmacy segment dominated the market with the largest revenue share of 48.9% in 2025, driven by the convenience of direct access to prescribed therapies and integration with hospital treatment protocols. Hospital pharmacies ensure the availability of both pharmacological and specialized edema treatments. The segment benefits from trained pharmacists who provide patient guidance and monitor therapy adherence. Hospitals also facilitate supply chain efficiency for high-demand medications, ensuring uninterrupted access. The segment’s dominance is strengthened by the integration of hospital pharmacies with clinical monitoring and prescription systems. Patients with severe or chronic edema often rely on hospital pharmacies for timely medication refills and counseling.

The Online Pharmacy segment is expected to witness the fastest CAGR from 2026 to 2029, fueled by increasing digital adoption, e-commerce penetration, and patient preference for home delivery of medications. Online pharmacies provide access to oral, anti-allergic, and specialty edema drugs with convenience and discretion. The growth is supported by telemedicine services, subscription-based medication deliveries, and remote patient monitoring programs. Rising smartphone usage and internet penetration, particularly in emerging economies, are accelerating adoption. Patients and caregivers appreciate the ease of ordering, doorstep delivery, and real-time updates on medication availability. Online pharmacies are also expanding partnerships with healthcare providers to enhance therapy adherence and patient support.

Edema Treatment Market Regional Analysis

- North America dominated the edema treatment market with the largest revenue share of 39.5% in 2025, attributed to advanced healthcare infrastructure, high healthcare spending, strong reimbursement policies, and a well-established pharmaceutical industry

- Patients and healthcare providers in the region highly value established treatment protocols, advanced pharmacological therapies, and integrated monitoring solutions, which improve clinical outcomes and support effective management of both acute and chronic edema cases

- This widespread adoption is further supported by strong healthcare spending, well-developed hospital networks, and growing awareness of edema management among patients and caregivers, establishing effective edema treatment as a standard of care across hospitals, specialty clinics, and homecare settings

U.S. Edema Treatment Market Insight

The U.S. edema treatment market captured the largest revenue share of 82% in 2025 within North America, fueled by the high prevalence of cardiovascular, renal, and hepatic disorders requiring advanced management of fluid retention. Patients and healthcare providers are increasingly prioritizing effective, evidence-based therapies, including diuretics, blood thinners, and anti-allergic medications. The growing trend of homecare and outpatient edema management, coupled with widespread adoption of remote monitoring devices, further propels market growth. Moreover, the increasing integration of digital health tools for tracking patient adherence and therapy outcomes is significantly contributing to the market's expansion.

Europe Edema Treatment Market Insight

The Europe edema treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by advanced healthcare infrastructure, favorable reimbursement policies, and increasing adoption of personalized therapies. Rising awareness of chronic edema management and the prevalence of aging populations are fostering greater use of pharmacological and non-pharmacological interventions. European patients and providers are drawn to treatments that improve quality of life and reduce hospitalizations. The region is experiencing significant growth across hospitals, specialty clinics, and homecare services, with edema therapies being incorporated into both new treatment protocols and ongoing patient care programs.

U.K. Edema Treatment Market Insight

The U.K. edema treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing incidence of heart failure, kidney disease, and lymphedema, as well as a growing focus on preventive care. In addition, concerns regarding complications from untreated edema are encouraging both hospitals and homecare providers to adopt comprehensive therapy solutions. The U.K.’s well-established healthcare infrastructure, combined with robust insurance coverage and clinical guidelines, is expected to continue stimulating market growth. Digital patient monitoring tools and telehealth programs further support adoption by enabling remote management and improved adherence.

Germany Edema Treatment Market Insight

The Germany edema treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of chronic edema management and growing demand for innovative therapies. Germany’s strong healthcare system, high physician expertise, and emphasis on preventive and personalized medicine promote adoption across hospitals and specialty clinics. Integration of digital therapy monitoring and patient-centric care is increasingly prevalent, with patients and providers favoring treatments that combine efficacy, safety, and convenience. Moreover, ongoing clinical research and availability of advanced pharmacological and compression therapies are supporting market growth.

Asia-Pacific Edema Treatment Market Insight

The Asia-Pacific edema treatment market is poised to grow at the fastest CAGR of 8.3% during the forecast period of 2026 to 2029, driven by increasing prevalence of chronic diseases, rising geriatric population, and expansion of healthcare infrastructure in countries such as China, Japan, and India. The region’s growing awareness of early intervention and preventive healthcare is driving adoption of edema treatments in hospitals, specialty clinics, and homecare. Furthermore, government initiatives supporting digital health monitoring and telemedicine are enabling better patient management. Emerging economies’ expanding middle class and increased healthcare spending are also accelerating market penetration and accessibility of effective therapies.

Japan Edema Treatment Market Insight

The Japan edema treatment market is gaining momentum due to the country’s high prevalence of cardiovascular and renal disorders, aging population, and strong emphasis on preventive healthcare. Patients and providers are increasingly adopting advanced therapies combined with remote monitoring to manage chronic edema effectively. The integration of edema management with telemedicine and homecare programs is further driving growth. Moreover, Japan’s focus on innovation in pharmaceuticals and medical devices is supporting the development of patient-friendly treatment solutions suitable for both residential and hospital settings.

India Edema Treatment Market Insight

The India edema treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising prevalence of lifestyle-related diseases, and expanding healthcare access. India is witnessing growing adoption of oral medications, compression therapy, and telemedicine solutions for home-based edema management. The push towards digital health initiatives, combined with affordable treatment options and a large patient population, is propelling the market. Strong domestic pharmaceutical manufacturing capabilities and increasing awareness among patients and providers are key factors driving the adoption of edema therapies across hospitals, specialty clinics, and homecare settings.

Edema Treatment Market Share

The Edema Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- F. Hoffmann‑La Roche Ltd (Switzerland)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Hikma Pharmaceuticals PLC (U.K.)

- Sun Pharmaceutical Industries Ltd (India)

- Novartis AG (Switzerland)

- Teva Pharmaceutical Industries Ltd (Israel)

- Aurobindo Pharma Ltd (India)

- Dr. Reddy’s Laboratories Ltd (India)

- Cipla Ltd (India)

- Lupin Ltd (India)

- Zydus Lifesciences Ltd (India)

- Glenmark Pharmaceuticals Ltd (India)

- Torrent Pharmaceuticals Ltd (India)

- Wockhardt Ltd (India)

- Natco Pharma Ltd (India)

- Biocon Ltd (India)

- Viatris Inc (U.S.)

- Sandoz International GmbH (Germany)

What are the Recent Developments in Global Edema Treatment Market?

- In October 2025, the U.S. Food and Drug Administration (FDA) approved Lasix® ONYU, a novel drug‑device combination for the treatment of edema due to fluid overload in adult patients with chronic heart failure, enabling selected patients to receive treatment subcutaneously at home rather than only in hospital settings significantly expanding at‑home care options for edema management

- In July 2024, new research on chronic lower extremity edema highlighted emerging alternative therapies such as exogenous calf muscle stimulation, high‑dose albumin injections, and device‑based negative pressure lymph drainage (NPLD), illustrating expanding clinical exploration beyond traditional diuretics and compression signaling broader therapeutic interest in edema subtypes

- In March 2024, targeted delivery innovations in macular edema associated with uveitis continued to gain clinical traction, with Xipere® (triamcinolone acetonide) recognized as an advanced suprachoroidal treatment providing more precise therapy for macular edema and improving outcomes for affected patients, reinforcing the importance of novel administration routes in edema care

- In March 2023, clinical insights and reviews into edema management reported contemporary data on treatment challenges such as diuretic resistance and mechanistic understanding of fluid accumulation, offering new therapeutic targets and guiding clinicians toward more tailored management approaches for edema patients

- In October 2021, the FDA approved XIPERE™ (triamcinolone acetonide injectable suspension) for the treatment of macular edema associated with uveitis, marking a breakthrough as the first therapy targeting the suprachoroidal space for this condition, representing a significant advancement in edema‑related ophthalmic care

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.