Global Encryption Software Market

Размер рынка в млрд долларов США

CAGR :

%

USD

15.05 Billion

USD

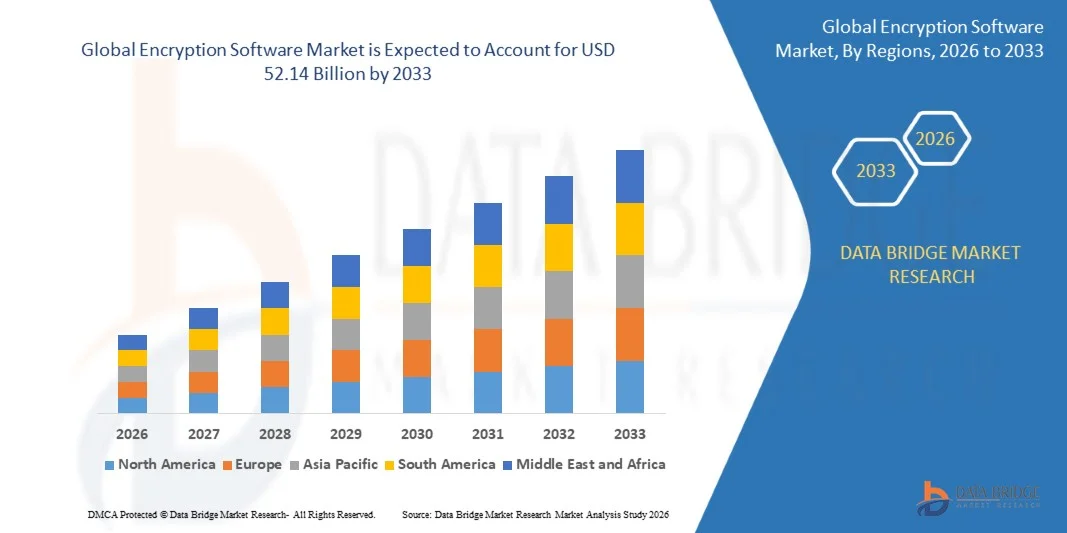

52.14 Billion

2025

2033

USD

15.05 Billion

USD

52.14 Billion

2025

2033

| 2026 –2033 | |

| USD 15.05 Billion | |

| USD 52.14 Billion | |

| % | |

|

Global Encryption Software Market Segmentation, By Component (Software and Services), Application (Disk Encryption, File/Folder Encryption, Database Encryption, Communication Encryption, and Cloud Encryption), Deployment Mode (On-Premises and Cloud), Enterprise Size (Small and Medium-Sized Enterprises and Large Enterprises), Vertical (Banking, Financial Services and Insurance, Aerospace and Defense, Government and Public Utilities, IT and Telecommunication, Healthcare, Retail, and Others) - Industry Trends and Forecast to 2033

What is the Global Encryption Software Market Size and Growth Rate?

- The global encryption software market size was valued at USD 15.05 billion in 2025 and is expected to reach USD 52.14 billion by 2033, at a CAGR of 16.8% during the forecast period

- The rise in concerns pertaining to loss of critical data across the globe acts as one of the major factors driving the growth of encryption software market. The rise with growing trend of Internet of Things (IoT) and Bring Your Own Device (BYOD), among enterprises, and increase in cyber-attacks, data breaches, commercial espionage, and theft and losses in companies accelerate the market growth

- The continuous advancements in mobile technology in terms of hardware and software, their dissemination among businesses, and rise in stringent regulatory standards and data privacy compliances further influence the market

What are the Major Takeaways of Encryption Software Market?

- Increase in the number of data centres, quick adoption of database encryption solutions, rapid digitization, and increase in the adoption of cloud and virtualization technologies positively affect the encryption software market

- Furthermore, adoption of encryption software across verticals and rise in demand for integrated data protection solutions and EAAS among SMES extend profitable opportunities to the market players

- North America dominated the encryption software market with a 39.2% revenue share in 2024, driven by the strong presence of leading cybersecurity vendors, high adoption of cloud technologies, and stringent data protection regulations across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 7.98% from 2025 to 2033, driven by rapid digital transformation, rising cloud adoption, expanding fintech ecosystems, and increasing investments in cybersecurity infrastructure across China, Japan, India, South Korea, and Southeast Asia

- The Software segment dominated the market with a 68.4% share in 2025, as organizations increasingly invest in standalone and integrated encryption platforms to protect sensitive enterprise, customer, and transactional data

Report Scope and Encryption Software Market Segmentation

|

Attributes |

Encryption Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Encryption Software Market?

“Increasing Shift Toward Cloud-Based, AI-Driven, and Zero-Trust Encryption Solutions”

- The encryption software market is witnessing strong adoption of cloud-native, AI-enabled, and zero-trust security solutions designed to protect sensitive enterprise, consumer, and government data across endpoints, networks, databases, and cloud environments

- Vendors are increasingly introducing advanced encryption platforms with automated key management, real-time threat detection, and multi-cloud compatibility to strengthen data security and regulatory compliance

- Growing demand for cost-efficient, scalable, and remotely deployable cybersecurity solutions is driving adoption across BFSI, healthcare, government, IT, and manufacturing sectors

- For instance, companies such as Microsoft, IBM, Palo Alto Networks, Cisco, and Fortinet are continuously enhancing their encryption software portfolios with AI-powered threat intelligence, ransomware protection, and cloud workload security

- Rising need for data privacy, secure digital transactions, and protection against cyberattacks is accelerating the shift toward enterprise-grade encryption platforms

- As digital transformation and cloud migration continue to expand, Encryption Softwares will remain essential for safeguarding critical business information and ensuring regulatory compliance

What are the Key Drivers of Encryption Software Market?

- Rising concerns regarding data breaches, cyberattacks, ransomware, and unauthorized access are significantly driving demand for advanced encryption software solutions

- For instance, in 2025, leading companies such as Microsoft, IBM, and Check Point Software Technologies strengthened their security suites with enhanced endpoint encryption, file-level protection, and cloud security tools

- Growing adoption of cloud computing, IoT devices, remote working models, and digital banking services is boosting demand for robust data encryption tools across the U.S., Europe, and Asia-Pacific

- Advancements in AI-based threat analytics, automated key lifecycle management, and quantum-resistant encryption algorithms have strengthened security capabilities and software performance

- Rising use of digital payment systems, online identity management, and confidential enterprise communications is creating strong demand for scalable encryption platforms

- Supported by rising investments in cybersecurity infrastructure, compliance frameworks, and enterprise risk management, the Encryption Software market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Encryption Software Market?

- High costs associated with advanced enterprise encryption suites, continuous updates, and managed security services restrict adoption among SMEs and budget-sensitive organizations

- For instance, during 2024–2025, the increasing sophistication of cyber threats and frequent software upgrades raised implementation and maintenance costs for several vendors

- Complexity in encryption key management, integration with legacy systems, and compliance with global data protection regulations increases operational challenges

- Limited cybersecurity awareness and lack of skilled professionals in emerging markets continue to slow adoption

- Competition from integrated security platforms, endpoint detection tools, and cloud-native cybersecurity suites creates pricing pressure and reduces differentiation

- To address these challenges, companies are focusing on cost-optimized SaaS models, automated key management, AI-driven analytics, and simplified deployment frameworks to increase global adoption of encryption softwares

How is the Encryption Software Market Segmented?

The market is segmented on the basis of component, application, deployment mode, enterprise size, and vertical.

• By Component

On the basis of component, the Encryption Software market is segmented into Software and Services. The Software segment dominated the market with a 68.4% share in 2025, as organizations increasingly invest in standalone and integrated encryption platforms to protect sensitive enterprise, customer, and transactional data. Software solutions such as endpoint encryption, database encryption, and cloud workload protection are widely adopted due to their scalability, automation capabilities, and compliance support across industries. The growing use of AI-enabled cybersecurity tools and centralized key management systems continues to strengthen segment growth.

The Services segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for consulting, deployment, managed security, and maintenance services. Increasing complexity in regulatory compliance, cloud migration, and cyber risk management is pushing enterprises to outsource encryption implementation and monitoring services.

• By Application

On the basis of application, the market is segmented into Disk Encryption, File/Folder Encryption, Database Encryption, Communication Encryption, and Cloud Encryption. The Disk Encryption segment dominated the market with a 31.7% share in 2025, supported by strong demand for endpoint protection across laptops, desktops, and enterprise devices. Organizations across BFSI, healthcare, and government sectors extensively use disk encryption to prevent unauthorized access, ransomware risks, and data theft from lost or stolen devices.

The Cloud Encryption segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising adoption of cloud computing, SaaS applications, hybrid work environments, and multi-cloud data storage. Growing concerns over cloud data breaches, cross-border data transfers, and privacy regulations are accelerating demand for advanced cloud-native encryption solutions with automated key lifecycle management and zero-trust security frameworks

• By Deployment Mode

On the basis of deployment mode, the Encryption Software market is segmented into On-Premises and Cloud. The On-Premises segment dominated the market with a 57.2% share in 2025, primarily due to its strong adoption among government agencies, defense organizations, financial institutions, and highly regulated enterprises requiring complete control over sensitive data and encryption keys. On-premises deployment offers enhanced data sovereignty, stronger internal access controls, and easier compliance with strict industry-specific regulations.

The Cloud segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rapid digital transformation, increasing remote workforce adoption, and the rising use of cloud-native business applications. Enterprises are increasingly preferring cloud-based encryption solutions for their flexibility, scalability, lower infrastructure costs, and ease of deployment across distributed teams and global business environments.

• By Enterprise Size

On the basis of enterprise size, the market is segmented into Small and Medium-Sized Enterprises and Large Enterprises. The Large Enterprises segment dominated the market with a 63.5% share in 2025, driven by higher cybersecurity budgets, large-scale data volumes, and greater exposure to sophisticated cyber threats. These organizations extensively deploy enterprise-grade encryption platforms across networks, endpoints, databases, and communication channels to ensure compliance and business continuity

The Small and Medium-Sized Enterprises segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising cybersecurity awareness, increasing digital adoption, and the availability of cost-effective SaaS-based encryption tools. The growing frequency of cyberattacks targeting SMEs is further boosting adoption of affordable and scalable encryption software solutions.

• By Vertical

On the basis of vertical, the Encryption Software market is segmented into Banking, Financial Services and Insurance, Aerospace and Defense, Government and Public Utilities, IT and Telecommunication, Healthcare, Retail, and Others. The Banking, Financial Services and Insurance (BFSI) segment dominated the market with a 29.8% share in 2025, owing to the need for secure financial transactions, fraud prevention, customer data protection, and strict compliance with data privacy regulations.

The Healthcare segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by rising digitization of patient records, connected medical devices, telehealth platforms, and growing concerns around patient data privacy and ransomware threats. Increasing regulatory requirements and healthcare cybersecurity investments are further supporting segment growth.

Which Region Holds the Largest Share of the Encryption Software Market?

- North America dominated the encryption software market with a 39.2% revenue share in 2024, driven by the strong presence of leading cybersecurity vendors, high adoption of cloud technologies, and stringent data protection regulations across the U.S. and Canada. Rising incidents of ransomware attacks, data breaches, and increasing demand for endpoint, cloud, and communication encryption solutions continue to accelerate market growth across BFSI, healthcare, government, and IT sectors. Strong investments in cybersecurity infrastructure and enterprise risk management further support regional dominance

- Leading companies in North America are continuously introducing advanced encryption platforms integrated with AI-driven threat detection, automated key management, and cloud-native security frameworks, strengthening the region’s technological leadership

- High concentration of digital enterprises, mature cloud ecosystems, and strong regulatory compliance requirements such as HIPAA, PCI-DSS, and government cybersecurity mandates further reinforce regional market leadership

U.S. Encryption Software Market Insight

The U.S. is the largest contributor in North America, supported by strong demand for data protection solutions across financial institutions, federal agencies, healthcare providers, and cloud service enterprises. Increasing adoption of remote work, BYOD policies, digital banking, and SaaS platforms is significantly driving demand for disk, database, and cloud encryption software. The presence of major cybersecurity vendors such as Microsoft, IBM, Cisco Systems, and Palo Alto Networks further strengthens market growth.

Canada Encryption Software Market Insight

Canada contributes significantly to regional growth, driven by rising investments in enterprise cybersecurity, cloud migration strategies, and data privacy frameworks across banking, telecom, and public sector organizations. Growing awareness regarding ransomware threats and regulatory compliance is accelerating adoption of enterprise-grade encryption solutions across the country.

Asia-Pacific Encryption Software Market

Asia-Pacific is projected to register the fastest CAGR of 7.98% from 2025 to 2033, driven by rapid digital transformation, rising cloud adoption, expanding fintech ecosystems, and increasing investments in cybersecurity infrastructure across China, Japan, India, South Korea, and Southeast Asia. Growing use of mobile payments, IoT devices, e-commerce platforms, and enterprise cloud workloads continues to accelerate demand for advanced encryption software solutions.

China Encryption Software Market Insight

China is the largest contributor to Asia-Pacific due to strong digital infrastructure expansion, rising enterprise cloud adoption, and significant investments in data privacy and national cybersecurity initiatives. Rapid growth in e-commerce, smart manufacturing, and fintech platforms continues to drive strong demand for encryption software.

Japan Encryption Software Market Insight

Japan shows steady growth supported by advanced IT infrastructure, strong enterprise cybersecurity spending, and rising adoption of encrypted communication and cloud security platforms across manufacturing, telecom, and financial institutions.

India Encryption Software Market Insight

India is emerging as a major growth hub, driven by rapid digital payments adoption, expanding cloud ecosystems, startup growth, and government-led digital transformation initiatives. Increasing demand for data privacy and enterprise cybersecurity solutions is further accelerating market penetration.

South Korea Encryption Software Market Insight

South Korea contributes significantly due to strong demand from telecom, consumer electronics, and digital banking sectors. Rapid 5G deployment, AI ecosystem growth, and cloud expansion continue to support sustained demand for advanced encryption software solutions.

Which are the Top Companies in Encryption Software Market?

The encryption software industry is primarily led by well-established companies, including:

- Microsoft Corporation (U.S.)

- Bloombase (Taiwan)

- Symantec (U.S.)

- Intel Security / McAfee (U.S.)

- EMC Corporation (U.S.)

- Amazon Web Services Inc. (U.S.)

- Check Point Software Technologies (Israel)

- Cisco Systems Inc. (U.S.)

- F-Secure (Finland)

- Fortinet Inc. (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Palo Alto Networks Inc. (U.S.)

- WinMagic Inc. (Canada)

- Trend Micro Incorporated (Japan)

What are the Recent Developments in Global Encryption Software Market?

- In June 2023, Amazon Web Services introduced Amazon S3 dual-layer server-side encryption with keys stored in AWS Key Management Service (DSSE-KMS), a new security feature that applies two layers of encryption to data stored in Amazon S3 buckets. This advanced encryption capability helps enterprises strengthen data protection frameworks and meet stringent regulatory compliance requirements, thereby reinforcing growth opportunities in the Encryption Software market

- In May 2023, Vaultree enhanced healthcare data security by launching its advanced Data-in-Use encryption solution, supported by a software development kit and an encrypted chat tool. The solution is designed to secure sensitive patient information even during active processing and potential breach scenarios while maintaining operational performance, thereby accelerating adoption of advanced encryption technologies in the healthcare sector

- In February 2023, Irdeto launched an upgraded version of its ActiveCloak for Media (ACM) software development kit, integrating multiple security layers to prevent unauthorized extraction of content encryption keys from devices. This advancement significantly improves digital content protection and platform security, thereby strengthening innovation within the Encryption Software market

- In January 2023, Amazon Web Services enabled default encryption for all newly uploaded Amazon S3 objects, automatically applying server-side encryption unless an alternative method is selected. By generating unique encryption keys for each uploaded object, the service improves seamless data security for users, thereby supporting widespread enterprise adoption of built-in encryption solutions

- In November 2022, IronCore Labs introduced the latest version of Cloaked Search, an encrypted search proxy designed for Elasticsearch and OpenSearch environments. The enhanced solution expands application-layer encryption capabilities and protects sensitive data across search services, thereby strengthening data privacy and secure cloud application deployments

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.