Global Fuel Additive Market

Размер рынка в млрд долларов США

CAGR :

%

USD

10.79 Billion

USD

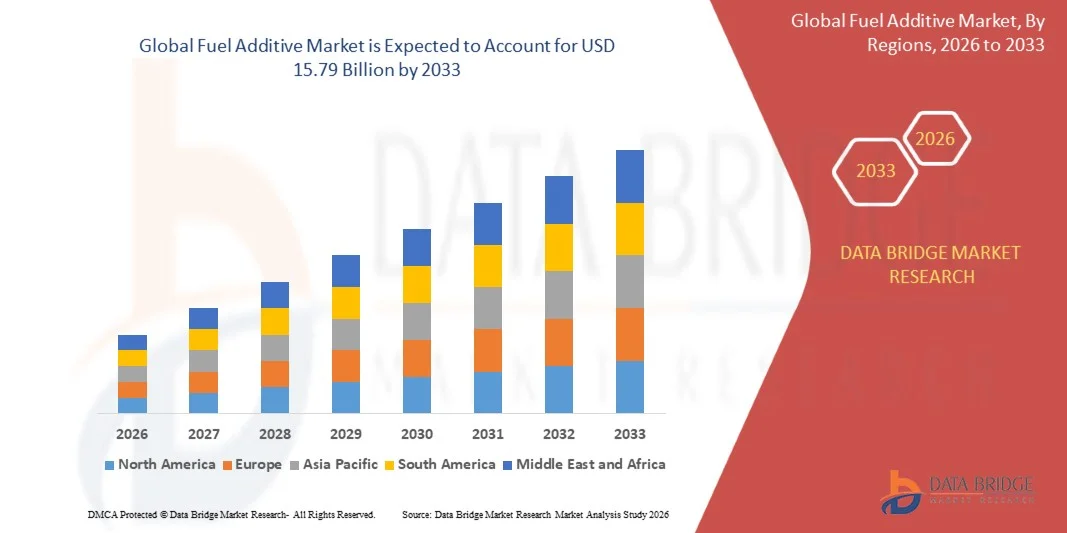

15.79 Billion

2025

2033

USD

10.79 Billion

USD

15.79 Billion

2025

2033

| 2026 –2033 | |

| USD 10.79 Billion | |

| USD 15.79 Billion | |

| % | |

|

Global Fuel Additive Market Segmentation, By Type (Deposit Control, Cetane Improvers, Lubricity Improvers, Cold Flow Improvers, Stability Improvers, Octane Improvers, and Corrosion Inhibitors), Application (Diesel Fuel Additives, Gasoline Fuel Additives, Aviation Fuel Additives, and Others) - Industry Trends and Forecast to 2033

Fuel Additive Market Size

- The global fuel additive market size was valued at USD 10.79 billion in 2025 and is expected to reach USD 15.79 billion by 2033, at a CAGR of 4.88% during the forecast period

- The market growth is largely fueled by the increasing demand for cleaner fuels and stringent emission regulations, driving the adoption of fuel additives that enhance engine performance, improve fuel efficiency, and reduce harmful exhaust emissions

- Furthermore, rising industrialization, growing vehicle ownership, and technological advancements in engine and fuel formulations are establishing fuel additives as essential solutions for both automotive and industrial applications. These converging factors are accelerating the uptake of high-performance fuel additives, thereby significantly boosting the industry's growth

Fuel Additive Market Analysis

- Fuel additives are chemical compounds added to fuels to improve their performance, enhance combustion efficiency, prevent engine deposits, and reduce emissions. These additives include detergents, antioxidants, corrosion inhibitors, lubricity enhancers, and cetane or octane improvers, and are widely used across gasoline, diesel, and biofuel applications

- The escalating demand for fuel additives is primarily fueled by the need to meet environmental standards, improve engine longevity, and optimize fuel consumption. Growing awareness among consumers and industries regarding sustainability and operational efficiency further drives the adoption of fuel additive solutions globally

- North America dominated the fuel additive market with a share of 34.3% in 2025, due to the extensive use of diesel and gasoline engines across transportation, industrial, and commercial sectors

- Asia-Pacific is expected to be the fastest growing region in the fuel additive market during the forecast period due to rapid urbanization, rising vehicle ownership, and expanding industrial and transport sectors in countries such as China, India, and Japan

- Deposit control segment dominated the market with a market share of around 40% in 2025, due to its critical role in preventing engine deposits and maintaining optimal fuel injector performance. Engine manufacturers and fleet operators prioritize deposit control additives for their ability to enhance combustion efficiency, reduce maintenance costs, and prolong engine life. Strong adoption is also fueled by regulatory emphasis on emissions reduction and fuel efficiency, making deposit control additives essential in both diesel and gasoline engines

Report Scope and Fuel Additive Market Segmentation

|

Attributes |

Fuel Additive Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Fuel Additive Market Trends

“Rising Adoption of High-Performance and Eco-Friendly Fuel Additives”

- A prominent trend in the fuel additive market is the increasing shift toward high-performance and environmentally friendly fuel additives, driven by the growing emphasis on reducing vehicular emissions and improving engine efficiency. This shift is promoting the development of formulations that enhance fuel combustion, lower carbon footprints, and extend engine life across automotive and industrial applications

- For instance, companies such as BASF and Afton Chemical are introducing advanced detergents and combustion improvers that optimize engine performance while complying with environmental standards. These innovations are enabling automotive manufacturers and fleet operators to meet stricter emission norms without sacrificing power output

- The demand for bio-based and synthetic fuel additives is accelerating as governments and regulatory bodies encourage sustainable energy solutions. These additives enhance fuel stability, reduce deposit formation, and improve overall energy efficiency, supporting long-term sustainability goals in transportation and logistics

- The market is witnessing growth in multi-functional additives that combine cleaning, anti-knock, and lubricating properties to provide comprehensive fuel performance solutions. This is reinforcing the adoption of additive packages that reduce engine wear, lower maintenance costs, and enhance vehicle reliability

- Industries such as aviation and marine transport are increasingly deploying specialized fuel additives to maintain engine integrity under extreme operating conditions. Additives that improve cold-flow properties, corrosion protection, and fuel combustion efficiency are becoming standard requirements for high-performance operations

- The rising consumer awareness regarding fuel economy and environmental impact is influencing purchasing decisions, prompting manufacturers to innovate with greener and more effective additive solutions. This trend continues to drive investment in research and development for next-generation fuel additives

Fuel Additive Market Dynamics

Driver

“Increasing Demand for Cleaner Fuels and Engine Efficiency”

- The growing emphasis on reducing vehicular emissions and improving engine longevity is driving demand for fuel additives that enhance combustion efficiency and lower pollutant output. These additives enable engines to perform optimally while meeting stricter fuel standards imposed by governments and environmental agencies

- For instance, Chevron Oronite provides fuel detergent additives that improve fuel burn efficiency and reduce carbon deposits, supporting cleaner operations across automotive and industrial engines. Such solutions are critical for fleet operators aiming to balance performance and regulatory compliance

- Rising adoption of high-performance vehicles and heavy-duty machinery is increasing reliance on fuel additives that prevent engine knock, improve lubrication, and maintain thermal stability. This is enhancing engine life and operational reliability across transportation and industrial sectors

- The global push for sustainable fuels and reduction in greenhouse gas emissions is expanding the market for eco-friendly additive solutions. Additives that enable biofuel compatibility and lower sulfur content are becoming key tools for manufacturers and fuel suppliers

- Increasing regulatory enforcement on fuel quality and emissions standards continues to reinforce this demand. The requirement for higher fuel efficiency and cleaner combustion is positioning fuel additives as essential enablers of modern engine performance

Restraint/Challenge

“Stringent Regulatory Compliance and High Production Costs”

- The fuel additive market faces challenges due to rigorous regulatory standards that govern formulation, performance, and environmental impact. Compliance with emission limits, chemical safety regulations, and fuel quality requirements increases complexity and operational costs for manufacturers

- For instance, Infineum must adhere to global emission standards such as Euro 6 and Tier 3 regulations while producing high-performance additives, leading to substantial investment in R&D and testing. These compliance obligations contribute to longer development cycles and elevated production expenses

- Developing high-performance and eco-friendly additives often requires costly raw materials and sophisticated chemical processing techniques. This combination increases overall manufacturing costs and affects pricing strategies across the market

- Quality assurance and testing protocols for fuel additives are extensive, as performance under variable engine conditions must be validated. These procedures further extend production timelines and elevate operational overheads for suppliers

- Scaling production while ensuring consistent additive performance and regulatory compliance remains a major challenge. Manufacturers must balance cost-efficiency with stringent quality standards, which limits flexibility and impacts market growth potential

Fuel Additive Market Scope

The market is segmented on the basis of type and application.

• By Type

On the basis of type, the fuel additive market is segmented into deposit control, cetane improvers, lubricity improvers, cold flow improvers, stability improvers, octane improvers, and corrosion inhibitors. The deposit control segment dominated the largest market revenue share of around 40% in 2025, driven by its critical role in preventing engine deposits and maintaining optimal fuel injector performance. Engine manufacturers and fleet operators prioritize deposit control additives for their ability to enhance combustion efficiency, reduce maintenance costs, and prolong engine life. Strong adoption is also fueled by regulatory emphasis on emissions reduction and fuel efficiency, making deposit control additives essential in both diesel and gasoline engines. Their compatibility with a wide range of engine types and fuel formulations further strengthens their market position.

The cetane improvers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for diesel engines in commercial and transportation sectors. Cetane improvers enhance ignition quality, resulting in smoother engine operation, lower emissions, and improved fuel economy. For instance, companies such as BASF are innovating high-performance cetane boosters tailored for modern diesel engines. The increasing focus on meeting stringent emission norms and improving engine efficiency across emerging economies is expected to accelerate adoption. Moreover, their ease of integration into existing diesel formulations makes them a preferred choice among fuel blenders.

• By Application

On the basis of application, the fuel additive market is segmented into diesel fuel additives, gasoline fuel additives, aviation fuel additives, and others. Diesel fuel additives dominated the market revenue share in 2025, driven by the widespread use of diesel engines in transportation, logistics, and industrial sectors. Diesel additives help improve combustion efficiency, reduce particulate emissions, and enhance engine longevity, making them critical for both commercial fleets and individual vehicle owners. Regulatory requirements for lower emissions in diesel engines also support the continuous adoption of diesel fuel additives across mature and emerging markets. Their effectiveness in cold weather performance and fuel stability further reinforces market dominance.

Gasoline fuel additives are expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for high-performance passenger vehicles and cleaner fuels. These additives improve octane levels, prevent engine knocking, and reduce deposit formation, enhancing overall engine efficiency and longevity. For instance, companies such as Chevron Oronite have developed advanced gasoline additive formulations that optimize engine performance while meeting environmental standards. The growing adoption of premium fuels and increasing consumer awareness about engine maintenance contribute to their accelerating growth. In addition, their role in reducing emissions and supporting fuel economy makes them increasingly relevant in both developed and developing markets.

Fuel Additive Market Regional Analysis

- North America dominated the fuel additive market with the largest revenue share of 34.3% in 2025, driven by the extensive use of diesel and gasoline engines across transportation, industrial, and commercial sectors

- Consumers and fleet operators in the region prioritize additives that enhance fuel efficiency, reduce engine deposits, and ensure compliance with stringent emission regulations

- The market is further supported by high awareness of advanced fuel formulations, technologically sophisticated vehicles, and robust regulatory frameworks promoting cleaner fuels

U.S. Fuel Additive Market Insight

The U.S. fuel additive market captured the largest revenue share in 2025 within North America, fueled by the increasing use of high-performance fuels and rising demand for emission reduction solutions. The shift towards cleaner fuels and regulatory compliance is encouraging the adoption of fuel additives in both gasoline and diesel engines. For instance, Chevron Phillips Chemical Company offers advanced detergents and combustion improvers that enhance fuel efficiency while reducing harmful emissions. In addition, growing consumer preference for vehicles with longer engine life and better performance further propels market growth. The expanding presence of refining and petrochemical industries also supports the widespread availability and development of fuel additive formulations.

Europe Fuel Additive Market Insight

The Europe fuel additive market is projected to expand at a significant CAGR throughout the forecast period, driven by stringent emission standards and the growing need for fuel efficiency in commercial and passenger vehicles. The increase in urbanization, vehicle electrification trends, and adoption of biofuels are fostering demand for specialized additives. European consumers and industries increasingly favor additives that improve engine performance while reducing environmental impact. The market is witnessing growth across diesel and gasoline fuel applications, with advanced deposit control and octane improvers being widely adopted.

U.K. Fuel Additive Market Insight

The U.K. fuel additive market is expected to grow at a notable CAGR during the forecast period, driven by stringent regulatory requirements for cleaner fuels and increased focus on engine longevity and performance. Growing awareness among vehicle owners regarding fuel economy and emission reduction is encouraging the adoption of high-performance fuel additives. The market is further supported by the country’s well-established automotive sector and growing preference for premium fuel formulations that integrate advanced additive solutions.

Germany Fuel Additive Market Insight

The Germany fuel additive market is poised to expand at a considerable CAGR, fueled by high automotive production, technological advancements in engine efficiency, and strict European emission norms. German consumers and fleet operators show increasing preference for additives that enhance fuel stability, lubricity, and cetane quality. The integration of additives in both commercial and passenger vehicle fuels, along with support for sustainable fuel formulations, is contributing to strong market growth.

Asia-Pacific Fuel Additive Market Insight

The Asia-Pacific fuel additive market is expected to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, rising vehicle ownership, and expanding industrial and transport sectors in countries such as China, India, and Japan. Increasing adoption of diesel and gasoline fuel additives, supported by government initiatives for cleaner fuels and emission control, is boosting demand. Moreover, APAC’s emergence as a major manufacturing hub for fuel additive components and formulations is improving affordability and accessibility, facilitating market penetration across both urban and semi-urban regions.

Japan Fuel Additive Market Insight

The Japan fuel additive market is gaining momentum due to the country’s high focus on engine efficiency, emission control, and technological advancements in automotive fuel systems. Japanese consumers and commercial operators increasingly prefer fuel additives that improve cetane quality, lubricity, and deposit control for both diesel and gasoline engines. The adoption is further supported by a large number of advanced vehicles, strict emission regulations, and the integration of additives in industrial and aviation fuel applications.

China Fuel Additive Market Insight

The China fuel additive market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid industrialization, rising vehicle fleet, and high technological adoption in automotive and transport sectors. Strong government initiatives promoting cleaner fuels, expansion of fuel distribution networks, and the presence of domestic manufacturers producing cost-effective additive solutions are major growth drivers. China’s emphasis on fuel efficiency and emission reduction, combined with the growing adoption of diesel and gasoline fuel additives in residential, commercial, and industrial applications, continues to propel the market forward.

Fuel Additive Market Share

The fuel additive industry is primarily led by well-established companies, including:

- INEOS (U.K.)

- China Petrochemical Corporation (China)

- Kothari Petrochemicals Limited (India)

- The Lubrizol Corporation (U.S.)

- BASF SE (Germany)

- Infineum International Limited (U.K.)

- Chevron Corporation (U.S.)

- Cummins Inc. (U.S.)

- Cerion, LLC (U.S.)

- Royal Dutch Shell Plc (Netherlands)

- Eni S.p.A. (Italy)

- Evonik Industries AG (Germany)

- LANXESS (Germany)

- LG Chem (South Korea)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Nizhnekamskneftekhim (Russia)

- Repsol (Spain)

- Exxon Mobil Corporation (U.S.)

- TPC Group (U.S.)

- Formosa Plastics Corporation, U.S.A. (U.S.)

- Borealis AG (Austria)

- Versalis S.p.A. (Italy)

Latest Developments in Global Fuel Additive Market

- In October 2023, The Lubrizol Corporation announced a new distribution contract with IMCD Group, a leading global distributor and formulator of specialty chemicals. This strategic partnership enhances Lubrizol’s ability to serve the growing fuel additive and lubricant market in Bangladesh, ensuring improved product availability and stronger market penetration. The agreement positions Lubrizol to meet increasing regional demand, expand its customer base, and strengthen its presence in South Asia’s emerging fuel additive sector

- In August 2022, BASF commenced production of fuel performance additives at its newly established Pudong site in Shanghai, China. This facility was developed in response to rising regional demand for high-performance fuel additives and aims to offer better supply flexibility and security to clients across Asia. By localizing production, BASF can reduce lead times, improve cost efficiency, and support the expanding automotive and industrial sectors, thereby reinforcing its competitive edge in the Asia-Pacific fuel additive market

- In December 2021, BASF launched KEROPUR-D, a high-performance multipurpose diesel additive, in South Korea. The product is designed to remove existing engine deposits while preventing new deposit formation, enhancing engine efficiency and fuel performance. This launch strengthens BASF’s product portfolio in the Asia-Pacific region, addresses growing concerns about engine maintenance and emissions, and supports the adoption of high-quality diesel fuels among commercial and industrial vehicle operators

- In November 2021, Evonik inaugurated a new oil additive performance testing laboratory in the Asia-Pacific region. The state-of-the-art facility provides comprehensive testing and evaluation services for fuel and lubricant additives, enabling customers to optimize product performance. By offering advanced testing capabilities, Evonik enhances its value proposition to regional clients, supports the development of tailored additive solutions, and promotes the adoption of high-performance additives in emerging Asian markets

- In January 2021, BASF Enzymes LLC and Innospec Fuel Specialties LLC entered into a distribution agreement to supply DCI-11 Plus ClearTrak, a concentrated corrosion inhibitor, to ethanol producers in the U.S. This collaboration aims to boost overall value for consumers in the ethanol fuel segment while demonstrating both companies’ commitment to the growing biofuel industry. The agreement ensures wider availability of specialized additives, strengthens market reach, and supports operational efficiency for ethanol producers, thereby promoting growth in the North American fuel additive market

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.