Global Healthcare Integration Solutions Market

Размер рынка в млрд долларов США

CAGR :

%

USD

3.20 Billion

USD

7.48 Billion

2025

2033

USD

3.20 Billion

USD

7.48 Billion

2025

2033

| 2026 –2033 | |

| USD 3.20 Billion | |

| USD 7.48 Billion | |

| % | |

|

Global Healthcare Integration Solutions Market Segmentation, By Product (Interface Engine, Medical Device Integration, and Media Integration), Services (Support and Maintenance Services, Implementation Services, and Training Services), Application (Hospital Integration, Medical Device Integration, Lab Integration, Clinics Integration, Radiology Integration, and Other Applications) - Industry Trends and Forecast to 2033

Healthcare Integration Solutions Market Size

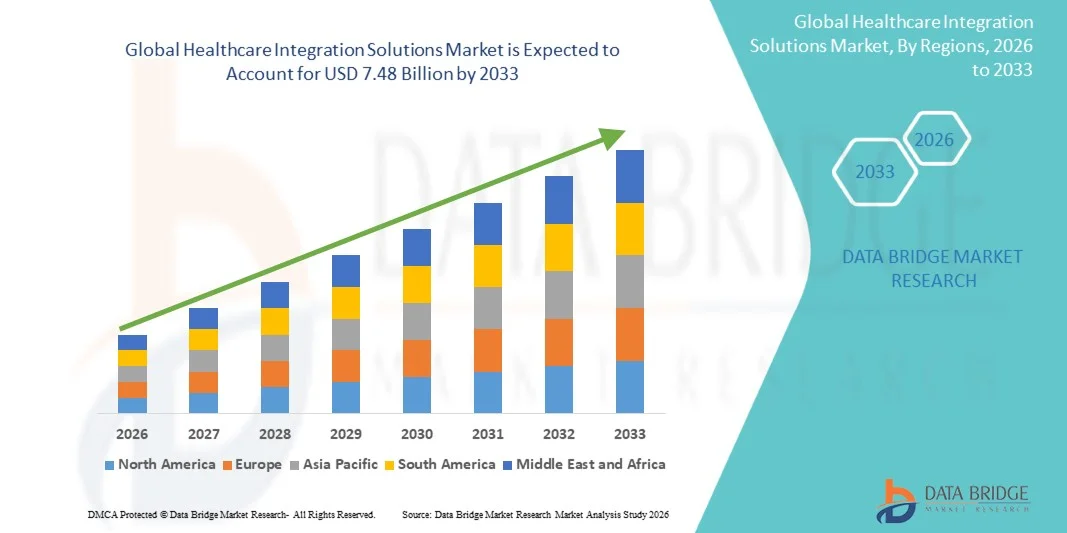

- The global Healthcare Integration Solutions market size was valued at USD 3.20 billion in 2025 and is expected to reach USD 7.48 billion by 2033, at a CAGR of 11.20% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital healthcare systems and advancements in interoperable health IT infrastructure, leading to improved connectivity between hospitals, laboratories, pharmacies, and other healthcare providers, resulting in enhanced data exchange and workflow efficiency

- Furthermore, rising demand for seamless data integration, improved patient care coordination, and reduced healthcare operational inefficiencies is establishing Healthcare Integration Solutions as a critical component of modern healthcare ecosystems. These converging factors are accelerating the uptake of Healthcare Integration Solutions, thereby significantly boosting the industry's growth

Healthcare Integration Solutions Market Analysis

- Healthcare Integration Solutions, enabling seamless connectivity and interoperability across healthcare IT systems such as EHR, laboratory systems, imaging platforms, and pharmacy systems, are increasingly vital components of modern healthcare ecosystems due to the growing need for efficient data exchange, improved patient outcomes, and streamlined clinical workflows

- The escalating demand for Healthcare Integration Solutions is primarily fueled by the rapid digitalization of healthcare systems, increasing adoption of electronic health records (EHR), rising focus on value-based care, and the need for improved coordination among healthcare providers

- North America dominated the healthcare integration solutions market with the largest revenue share of 43.0% in 2025, characterized by advanced healthcare IT infrastructure, high adoption of interoperability solutions, strong regulatory support for digital health systems, and significant presence of key industry players, with the U.S. experiencing substantial growth driven by large-scale hospital digitization and cloud-based integration adoption

- Asia-Pacific is expected to be the fastest growing region in the healthcare integration solutions market during the forecast period due to increasing healthcare digitization, rising investments in healthcare IT infrastructure, expanding hospital networks, and government initiatives promoting digital health adoption

- The implementation services segment dominated the largest market revenue share of 47.3% in 2025, driven by the growing deployment of healthcare IT systems across hospitals and clinics

Report Scope and Healthcare Integration Solutions Market Segmentation

|

Attributes |

Healthcare Integration Solutions Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Healthcare Integration Solutions Market Trends

“Advancements in Interoperability and AI-Driven Healthcare Data Integration Platforms”

- A significant and accelerating trend in the global healthcare integration solutions market is the increasing adoption of interoperable, AI-enabled platforms that enable seamless data exchange across hospitals, laboratories, imaging centers, and electronic health record (EHR) systems

- These solutions are improving clinical coordination and enabling more efficient, data-driven decision-making across healthcare ecosystems

- For instance, modern healthcare integration platforms are increasingly incorporating HL7 FHIR standards to enable real-time sharing of patient records between different healthcare providers, reducing duplication of tests and improving continuity of care

- AI-powered integration solutions are being used to automate data mapping, normalize heterogeneous medical data formats, and detect anomalies in clinical datasets, thereby improving data accuracy and reducing manual workload for healthcare IT teams

- Furthermore, cloud-based integration platforms are enabling healthcare organizations to connect legacy systems with modern digital applications, ensuring smooth interoperability without requiring complete system overhauls

- The growing use of predictive analytics within integration platforms is also helping healthcare providers identify patient risk patterns, optimize resource allocation, and improve operational efficiency

- This shift toward intelligent, connected, and interoperable healthcare ecosystems is significantly transforming how patient data is managed and utilized across global healthcare systems

Healthcare Integration Solutions Market Dynamics

Driver

“Rising Digital Transformation in Healthcare and Need for Seamless Data Exchange”

- The increasing digitalization of healthcare systems and the growing need for seamless data exchange across multiple care settings are major drivers of the Healthcare Integration Solutions market

- Healthcare providers are focusing on improving care coordination and reducing inefficiencies caused by fragmented data systems

- For instance, hospitals and healthcare networks are increasingly adopting integrated platforms that connect laboratory information systems, radiology systems, and electronic health records to ensure real-time access to patient data across departments

- The rising prevalence of chronic diseases and the growing demand for coordinated care delivery are further accelerating the need for integrated healthcare IT systems

- In addition, government initiatives promoting healthcare digitization and standardized health data exchange are supporting the widespread adoption of integration solutions

- The need to reduce administrative burden, improve clinical workflow efficiency, and enhance patient outcomes is also driving healthcare organizations toward advanced integration platforms

Restraint/Challenge

“Data Privacy Concerns and High Implementation Complexity”

- Concerns regarding data privacy, security, and compliance remain a significant challenge in the Healthcare Integration Solutions market, as these platforms involve the exchange of sensitive patient health information across multiple systems

- For instance, healthcare organizations must comply with strict regulatory frameworks such as HIPAA and GDPR, which increase the complexity of deploying and managing integrated systems

- The integration of legacy healthcare IT infrastructure with modern digital platforms often requires substantial customization, leading to high implementation costs and longer deployment timelines

- In addition, interoperability challenges between different software vendors and healthcare systems can hinder seamless data exchange

- Limited IT expertise and budget constraints in smaller healthcare facilities further restrict the adoption of advanced integration solutions

- Addressing these challenges through standardized data protocols, enhanced cybersecurity frameworks, and cost-effective deployment models will be essential for sustained market growth

Healthcare Integration Solutions Market Scope

The market is segmented on the basis of product, services, and application.

• By Product

On the basis of product, the Healthcare Integration Solutions market is segmented into interface engine, medical device integration, and media integration. The interface engine segment dominated the largest market revenue share of 44.6% in 2025, driven by its critical role in enabling seamless data exchange between different healthcare information systems. Interface engines facilitate interoperability between EHR, HIS, LIS, and other clinical systems, ensuring efficient data flow across healthcare networks. The increasing adoption of digital healthcare infrastructure and hospital information systems significantly boosts demand. Growing emphasis on interoperability standards such as HL7 and FHIR further strengthens adoption. Rising need for real-time data exchange in clinical decision-making supports segment growth. Expanding hospital digitization projects globally contribute to widespread deployment. In addition, increasing healthcare IT investments accelerate adoption of integration platforms. The need for reducing data silos and improving workflow efficiency further drives usage. Technological advancements in cloud-based integration engines enhance scalability and performance. Increasing focus on value-based care supports data-driven healthcare systems. These factors collectively ensure the dominance of the interface engine segment.

The medical device integration segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by the increasing use of connected medical devices and IoT-enabled healthcare systems. Growing demand for real-time patient monitoring in ICUs and critical care units supports adoption. Integration of devices such as ventilators, monitors, and infusion pumps improves clinical efficiency. Rising prevalence of chronic diseases requiring continuous monitoring further fuels growth. Increasing adoption of smart hospital infrastructure accelerates deployment. Advancements in wireless connectivity and IoT technologies enhance device interoperability. In addition, growing focus on reducing manual data entry errors supports automation. Expanding telehealth and remote patient monitoring services further boost demand. Increasing healthcare investments in emerging economies support market expansion. These factors position medical device integration as the fastest-growing product segment.

• By Services

On the basis of services, the Healthcare Integration Solutions market is segmented into support and maintenance services, implementation services, and training services. The implementation services segment dominated the largest market revenue share of 47.3% in 2025, driven by the growing deployment of healthcare IT systems across hospitals and clinics. Implementation services ensure proper installation, configuration, and integration of complex healthcare software solutions. Increasing adoption of electronic health records and interoperability platforms supports demand. Rising hospital digitization initiatives globally further strengthen segment growth. In addition, the need for customized integration solutions across healthcare systems boosts usage. Expanding healthcare infrastructure in emerging markets accelerates implementation activities. Growing complexity of IT ecosystems increases reliance on expert deployment services. Furthermore, integration of legacy systems with modern platforms drives demand. Strong involvement of vendors in end-to-end deployment enhances market penetration. These factors collectively ensure dominance of implementation services.

The support and maintenance services segment is expected to witness the fastest CAGR of 9.9% from 2026 to 2033, driven by the need for continuous system upgrades and technical support in healthcare IT environments. Increasing reliance on integrated systems requires ongoing monitoring and maintenance. Rising cybersecurity concerns in healthcare systems further boost demand for support services. Growing adoption of cloud-based healthcare solutions increases maintenance requirements. In addition, frequent software updates and system enhancements support segment growth. Expanding digital healthcare infrastructure in hospitals drives long-term service contracts. Increasing complexity of healthcare IT systems necessitates specialized technical support. Demand for minimizing system downtime further accelerates adoption. Rising focus on operational efficiency in healthcare facilities strengthens growth. These factors position support and maintenance services as the fastest-growing segment.

• By Application

On the basis of application, the Healthcare Integration Solutions market is segmented into hospital integration, medical device integration, lab integration, clinic integration, radiology integration, and other applications. The hospital integration segment dominated the largest market revenue share of 39.8% in 2025, driven by the high adoption of integrated healthcare systems in large hospital networks. Hospitals require seamless connectivity between multiple departments, including radiology, laboratory, and pharmacy systems. Increasing patient inflow and complex clinical workflows support adoption. Growing demand for centralized data management enhances operational efficiency. Rising implementation of EHR and HIS systems further strengthens integration needs. In addition, government initiatives promoting digital hospitals boost market growth. Expanding hospital infrastructure globally contributes to segment dominance. The need for real-time clinical decision-making supports integrated systems. Increasing focus on patient-centric care models accelerates adoption. These factors collectively ensure the dominance of the hospital integration segment.

The radiology integration segment is expected to witness the fastest CAGR of 10.6% from 2026 to 2033, driven by the increasing demand for advanced imaging data management and seamless PACS integration. Rising adoption of teleradiology and remote diagnostics supports growth. Growing volume of imaging procedures across healthcare facilities further boosts demand. Technological advancements in imaging software enhance integration efficiency. Increasing use of AI-based imaging analytics accelerates adoption. Expanding diagnostic centers and imaging networks contribute to segment expansion. In addition, rising need for faster diagnostic reporting supports workflow integration. Growing investments in radiology IT infrastructure further strengthen growth. Increasing focus on interoperability between imaging systems and hospital networks enhances efficiency. These factors position radiology integration as the fastest-growing application segment.

Healthcare Integration Solutions Market Regional Analysis

- North America dominated the healthcare integration solutions market with the largest revenue share of approximately 43.0% in 2025, characterized by advanced healthcare IT infrastructure, high adoption of interoperability solutions, and strong regulatory support for digital health systems

- The region benefits from the strong presence of key industry players and a mature ecosystem for healthcare digitization, enabling seamless data exchange across hospitals, laboratories, and care networks

- The increasing focus on large-scale hospital digitization, cloud-based integration platforms, and real-time clinical data sharing is further strengthening market growth, as healthcare providers prioritize efficiency, improved patient outcomes, and reduced operational fragmentation across systems

U.S. Healthcare Integration Solutions Market Insight

The U.S. healthcare integration solutions market captured the largest revenue share within North America in 2025, driven by rapid adoption of cloud-based healthcare IT systems, increasing hospital digitization initiatives, and strong demand for interoperable platforms. The growing need to integrate electronic health records (EHR), imaging systems, and laboratory data across healthcare networks is significantly boosting market expansion. Additionally, continuous investments in healthcare IT modernization and the presence of leading technology providers are further accelerating growth in the country.

Europe Healthcare Integration Solutions Market Insight

The Europe healthcare integration solutions market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare digitalization, rising demand for interoperable systems, and strong regulatory frameworks supporting standardized health data exchange. The region is witnessing growing adoption of integrated healthcare platforms across hospitals and diagnostic centers to improve care coordination and operational efficiency.

U.K. Healthcare Integration Solutions Market Insight

The U.K. healthcare integration solutions market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing investments in digital healthcare infrastructure, rising demand for connected care systems, and government-led initiatives to improve healthcare interoperability. The expansion of cloud-based healthcare platforms and data-driven care models is further contributing to market growth.

Germany Healthcare Integration Solutions Market Insight

The Germany healthcare integration solutions market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, increasing adoption of advanced IT systems, and rising focus on secure and efficient data exchange. The country’s emphasis on data privacy, system reliability, and healthcare innovation is driving the implementation of interoperable integration solutions across clinical environments.

Asia-Pacific Healthcare Integration Solutions Market Insight

The Asia-Pacific healthcare integration solutions market is expected to be the fastest growing region during the forecast period, driven by increasing healthcare digitization, rising investments in healthcare IT infrastructure, expanding hospital networks, and government initiatives promoting digital health adoption. Rapid modernization of healthcare systems and growing demand for efficient data management solutions are further accelerating market growth across the region.

Japan Healthcare Integration Solutions Market Insight

The Japan healthcare integration solutions market is gaining momentum due to the country’s advanced healthcare system, strong focus on technological innovation, and increasing adoption of digital health platforms. The rising aging population and growing need for efficient healthcare data management are driving the demand for integrated healthcare systems across hospitals and care facilities.

China Healthcare Integration Solutions Market Insight

The China healthcare integration solutions market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid healthcare infrastructure expansion, increasing government support for digital health initiatives, and strong adoption of advanced healthcare IT systems. The country’s large patient base, growing hospital networks, and emphasis on smart healthcare development are key factors driving market growth.

Healthcare Integration Solutions Market Share

The Healthcare Integration Solutions industry is primarily led by well-established companies, including:

- Oracle (U.S.)

- Epic Systems Corporation (U.S.)

- McKesson Corporation (U.S.)

- Allscripts Healthcare Solutions (U.S.)

- InterSystems Corporation (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- Philips Healthcare (Netherlands)

- GE HealthCare (U.S.)

- Infor (U.S.)

- NextGen Healthcare (U.S.)

- Athenahealth (U.S.)

- eClinicalWorks (U.S.)

- Orion Health (New Zealand)

- Interfaceware Inc. (Canada)

- Lyniate (U.S.)

- Fujitsu Limited (Japan)

- KLAS Research (U.S.)

- Veradigm Inc. (U.S.)

Latest Developments in Global Healthcare Integration Solutions Market

- In April 2021, Lyniate (then Rhapsody Health) acquired the Datica integration business and launched Lyniate Envoy to simplify interoperability and make seamless data exchange between healthcare systems more achievable. This move strengthened integration capabilities for healthcare providers by enabling easier connectivity and data flow between disparate clinical systems

- In January 2025, Innovaccer raised $275 million in a Series F funding round to expand its AI and cloud-based healthcare data integration and interoperability capabilities, advancing its unified data infrastructure across providers and payers. This funding boost supported deeper integration of clinical, claims, and operational data at scale

- In June 2025, 1upHealth launched its 1up Prior Authorization solution designed to streamline and automate prior authorization workflows through interoperable health data exchange, helping healthcare organizations meet modern interoperability demands. This launch reflects ongoing innovation in healthcare integration platforms focused on improving administrative efficiency

- In July 2025, Onyx Health released the OnyxOS Spring’25 Edition with expanded support for the latest CMS interoperability and patient access implementation guides, enabling healthcare organizations to better comply with regulatory data-sharing requirements. This update strengthened integration and API support in healthcare systems

- In December 2025, Trivitron Healthcare launched Trivitron Digital.AI, a next-generation digital health venture aimed at accelerating hospital digitization and clinical interoperability through cloud-based integration of LIS, Web-PACS, PHR, and AI-driven workflows. This launch marks a significant step toward interoperable and patient-centric digital healthcare ecosystems, particularly in emerging markets

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.