Global Hematologic Malignancies Market

Размер рынка в млрд долларов США

CAGR :

%

USD

90.89 Billion

USD

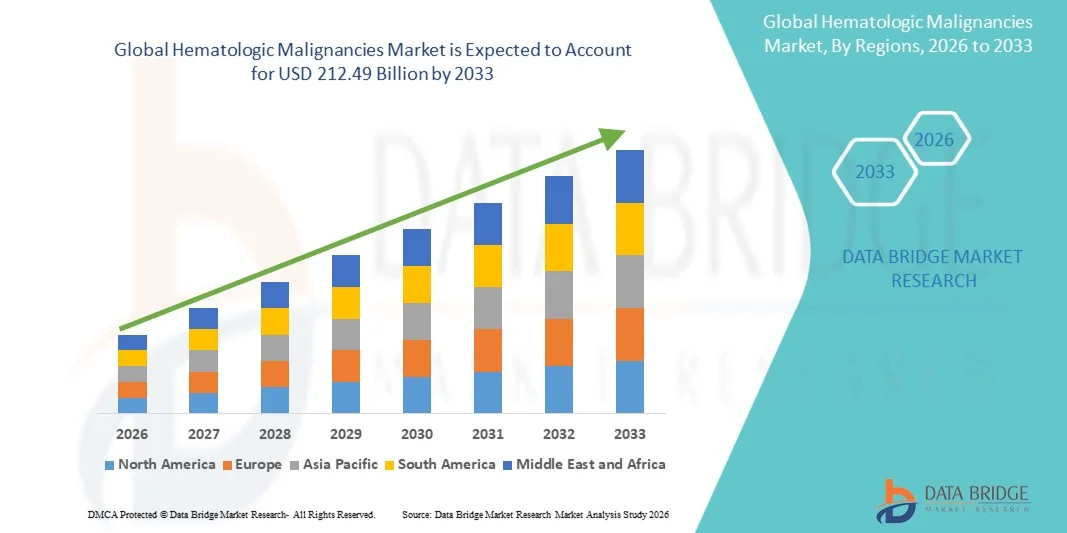

212.49 Billion

2025

2033

USD

90.89 Billion

USD

212.49 Billion

2025

2033

| 2026 –2033 | |

| USD 90.89 Billion | |

| USD 212.49 Billion | |

| % | |

|

Global Hematologic Malignancies Market Segmentation, By Type (Leukaemia, Lymphoma and Myeloma), Therapy Type (Chemotherapy, Immunotherapy, and Targeted Therapy), Diagnosis (Blood Tests, Biopsy, Imaging Tests and Others), Route of Administration (Oral, Parenteral and Others), Dosage Form (Tablets, Capsules, Injections and Others), End-Users (Hospitals, Specialty Clinics, Homecare and Others), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacy and Others)- Industry Trends and Forecast to 2033

Каковы размеры рынка гематологических злокачественных новообразований и темпы роста

- По данным Data Bridge Market Research Analysis Объем мирового рынка гематологических злокачественных новообразований оценивается в90,89 млрд долларов США в 2025 годуОжидается, что он достигнет212,49 млрд долларов к 2033 году, вCAGR 11,20%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен увеличением распространенности рака крови, такого как лейкемия, лимфома имножественная миеломаНаряду со значительными достижениями втаргетная терапияиммунотерапии и подходов точной медицины, что приводит к улучшению результатов лечения

- Кроме того, растущие инвестиции в онкологические исследования, расширение доступа к передовой диагностике и повышение осведомленности о раннем выявлении заболеваний создают инновационные методы лечения в качестве предпочтительного подхода к лечению. Эти сходящиеся факторы ускоряют принятие гематологических методов лечения злокачественных новообразований, тем самым значительно повышая рост отрасли.

Размер рынка и прогноз

- Глобальная рыночная стоимость (2025):$90,89 млрд.

- Ожидаемая рыночная стоимость (2033):$212,49 млрд.

- Прогноз CAGR (2026–2033):11.20%

Гематологические злокачественные образования Анализ рынка

- Гематологические злокачественные опухоли, охватывающие рак крови, костного мозга и лимфатической системы, такие как лейкемия, лимфома и множественная миелома, являются критическими областями фокусировки в онкологии из-за их сложной патофизиологии и необходимости передовых, целевых подходов к лечению как в больницах, так и в специализированных учреждениях по уходу.

- Растущий спрос на лечение гематологических злокачественных новообразований в первую очередь подпитывается ростом глобальной заболеваемости раком крови, растущим внедрением иммунотерапии и целевых препаратов и растущим акцентом на персонализированную медицину для улучшения результатов лечения пациентов.

- Северная Америка доминировала на рынке гематологических злокачественных новообразований с самой большой долей дохода в 42,15% в 2025 году, характеризующейся развитой инфраструктурой здравоохранения, высокими расходами на здравоохранение и сильным присутствием ведущих компаний.биофармацевтическийВ США наблюдается значительный рост новых разрешений на терапию и клинических испытаний, обусловленных непрерывными инновациями в исследованиях онкологии.

- Ожидается, что Азиатско-Тихоокеанский регион станет самым быстрорастущим регионом на рынке гематологических злокачественных новообразований в течение прогнозируемого периода из-за улучшения инфраструктуры здравоохранения, повышения осведомленности и расширения доступа к передовым методам лечения рака.

- Сегмент целевой терапии доминировал на рынке гематологических злокачественных новообразований с долей рынка 47,6% в 2025 году, что обусловлено его более высокой эффективностью, снижением побочных эффектов по сравнению с обычной химиотерапией и увеличением принятия подходов к точному лечению.

Сфера охвата и гематологические злокачественные образования сегментация рынка

|

Атрибуты |

Гематологические злокачественные образования Ключевые рыночные идеи |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

|

Каковы основные тенденции на рынке гематологических злокачественных новообразований

«Достижения в области целевой терапии и интеграции иммунотерапии»

- Значительной и ускоряющейся тенденцией на мировом рынке гематологических злокачественных новообразований является растущая интеграция целевых методов лечения и иммунотерапии, таких как моноклональные антитела, CAR-T клеточная терапия и ингибиторы контрольных точек. Это сближение передовых методов лечения значительно улучшает результаты лечения пациентов и показатели выживаемости.

- Например, клеточная терапия CAR-T, такая как кимрия и ескарта, продемонстрировала замечательную эффективность в лечении определенных типов лейкемии и лимфомы, предлагая новую надежду для пациентов с рецидивирующим или рефрактерным заболеванием. Аналогичным образом, моноклональные антитела все чаще включаются в схемы комбинированного лечения.

- Интеграция точной медицины в гематологические злокачественные опухоли позволяет идентифицировать конкретные генетические мутации и биомаркеры, позволяя клиницистам адаптировать методы лечения для отдельных пациентов. Например, целевые препараты, такие как ингибиторы BTK, предназначены для блокирования путей роста рака, в то время как передовая диагностика направляет оптимальные стратегии лечения. Кроме того, подходы иммунотерапии усиливают иммунный ответ организма на эффективное распознавание и устранение раковых клеток.

- Бесшовная интеграция передовых терапевтических средств с диагностическими технологиями способствует более персонализированной и эффективной экосистеме лечения. Благодаря скоординированному использованию геномного тестирования, целевых препаратов и иммунотерапии медицинские работники могут оптимизировать планы лечения и улучшить управление заболеваниями среди пациентов.

- Эта тенденция к более точным, эффективным и ориентированным на пациента подходам к лечению коренным образом меняет стандарты лечения в гематологической онкологии. Следовательно, такие компании, как Novartis и Gilead Sciences, разрабатывают инновационные методы лечения с повышенной эффективностью, снижением токсичности и более широким применением при множественных гематологических злокачественных новообразованиях.

- Спрос на передовые и персонализированные варианты лечения быстро растет как на развитых, так и на развивающихся рынках здравоохранения, поскольку пациенты и поставщики все чаще отдают приоритет улучшенным клиническим результатам и долгосрочному лечению заболеваний.

- Растущее внедрение цифровых технологий здравоохранения и реальных доказательных платформ способствует лучшему мониторингу и оптимизации лечения пациентов, что позволяет использовать более ориентированные на данные и адаптивные подходы к лечению в гематологической онкологии.

Динамика рынка гематологических злокачественных опухолей

водитель

«Растущее бремя болезней и растущее принятие передовых методов лечения»

- Растущая глобальная заболеваемость гематологическим раком в сочетании с растущим внедрением передовых методов лечения является значительным фактором повышенного спроса на терапию гематологической злокачественности.

- Например, в последние годы несколько нормативных утверждений для новых методов лечения, таких как CAR-T и целевые препараты, расширили варианты лечения и улучшили доступ пациентов. Ожидается, что такие стратегические разработки ключевых компаний будут стимулировать рост рынка гематологических злокачественных новообразований в прогнозируемый период.

- По мере того, как осведомленность о ранней диагностике и лечении продолжает расти, пациенты все чаще ищут эффективные методы лечения, которые предлагают улучшенные показатели выживаемости и качества жизни, создавая переход от традиционной химиотерапии к целенаправленному и иммунному лечению.

- Кроме того, расширение инфраструктуры здравоохранения и увеличение инвестиций в онкологические исследования делают передовые методы лечения более доступными, поддерживая более широкое внедрение в различных группах пациентов.

- Доступность инновационных вариантов лечения, улучшенные диагностические возможности и поддерживающие механизмы возмещения являются ключевыми факторами, способствующими внедрению гематологических методов лечения злокачественных новообразований как в развитых, так и в развивающихся регионах. Растущее участие в клинических испытаниях и постоянное развитие трубопроводов способствуют росту рынка.

- Растущее внимание к программам раннего скрининга и информационно-пропагандистским кампаниям способствует дальнейшему повышению показателей диагностики, своевременному вмешательству и повышению спроса на эффективные решения для лечения.

- Растущее сотрудничество между фармацевтическими компаниями, научно-исследовательскими институтами и поставщиками медицинских услуг ускоряет разработку и коммерциализацию лекарств, тем самым усиливая расширение рынка.

Сдержанность/вызов

«Высокие затраты на лечение и сложные пути регулирования»

- Опасения, связанные с высокой стоимостью передовых методов лечения, включая CAR-T и биологические препараты, представляют собой серьезную проблему для более широкого внедрения на рынке. Поскольку эти методы лечения включают в себя сложные процессы производства и администрирования, они часто приводят к значительному финансовому бремени для пациентов и систем здравоохранения.

- Например, высокая стоимость, связанная с терапией CAR-T и целевыми препаратами, имеет ограниченную доступность в нескольких регионах с низким и средним уровнем дохода, что создает неравенство в доступности лечения.

- Решение проблем, связанных с затратами, с помощью стратегий ценообразования, поддержки возмещения и моделей ухода, основанных на стоимости, имеет решающее значение для расширения доступа пациентов. Такие компании, как Bristol Myers Squibb и Roche, уделяют особое внимание программам помощи пациентам и партнерским отношениям для повышения доступности. Кроме того, строгие нормативные требования и длительные сроки одобрения могут задержать внедрение новых методов лечения, что повлияет на потенциал роста рынка.

- Хотя нормативно-правовая база обеспечивает безопасность и эффективность, сложность клинических испытаний и процессов утверждения может препятствовать быстрой коммерциализации инновационных методов лечения, особенно для небольших биотехнологических фирм.

- Преодоление этих проблем путем оптимизации затрат, рационализации механизмов регулирования и расширения сотрудничества между заинтересованными сторонами будет иметь жизненно важное значение для устойчивого роста рынка.

- Ограниченный доступ к передовой инфраструктуре здравоохранения и специализированным лечебным центрам в развивающихся регионах еще больше ограничивает внедрение передовых методов лечения, влияя на общее проникновение на рынок.

- Потенциальные побочные эффекты и проблемы безопасности, связанные с новыми методами лечения, включая нежелательные явления, связанные с иммунитетом, могут повлиять на принятие пациента и требуют тщательного мониторинга, что создает дополнительную проблему для широкого распространения.

Сфера рынка гематологических злокачественных опухолей

Рынок сегментирован на основе типа, типа терапии, диагностики, пути введения, лекарственной формы, конечных пользователей и канала распределения.

- По типу

Исходя из типа, рынок гематологических злокачественных новообразований сегментирован на лейкемию, лимфому и миелому. Сегмент лейкемии доминировал на рынке с самой большой долей рынка в 2025 году, что обусловлено его высокой глобальной распространенностью и растущей доступностью передовых вариантов лечения, таких как таргетная терапия и клеточная терапия CAR-T. Рост заболеваемости как острыми, так и хроническими формами лейкемии в значительной степени способствовал спросу на эффективные решения для лечения. Кроме того, сильные клинические исследования и постоянное одобрение лекарств улучшают результаты лечения. Наличие хорошо зарекомендовавших себя методов диагностики и растущая осведомленность в отношении раннего выявления способствуют дальнейшему росту сегмента. Более того, увеличение расходов на здравоохранение и доступ к специализированной онкологической помощи усиливают доминирование этого сегмента.

Ожидается, что в сегменте лимфомы будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует увеличение показателей диагностики и прогресс в лечении иммунотерапией. Растущее применение моноклональных антител и ингибиторов контрольных точек улучшает выживаемость пациентов с лимфомой. Кроме того, активизация информационно-просветительских кампаний и инициатив по скринингу приводят к более раннему выявлению и началу лечения. Расширение клинических испытаний с акцентом на инновационные методы лечения еще больше ускоряет рост сегмента. Увеличение инвестиций фармацевтических компаний и внедрение новых комбинированных методов лечения также способствуют его быстрому расширению.

- Тип терапии

На основе типа терапии рынок сегментирован на химиотерапию, иммунотерапию и таргетную терапию. Сегмент целевой терапии доминировал на рынке с самой большой долей дохода в 47,6% в 2025 году, что обусловлено его способностью точно нацеливаться на раковые клетки, минимизируя повреждение здоровых тканей. Растущее внедрение методов прецизионной медицины и лечения на основе биомаркеров значительно расширило использование целевых методов лечения. Кроме того, наличие широкого спектра одобренных целевых препаратов и постоянные инновации в этой области поддерживают рост сегмента. Улучшение результатов лечения пациентов и снижение побочных эффектов по сравнению с традиционной химиотерапией еще больше усиливают ее предпочтения среди медицинских работников. Растущие одобрения регулирующих органов и сильные клинические трубопроводы усиливают доминирование этого сегмента.

Ожидается, что сегмент иммунотерапии станет свидетелем самого быстрого CAGR с 2026 по 2033 год, что обусловлено быстрым развитием клеточной терапии CAR-T и ингибиторов иммунных контрольных точек. Эти методы лечения продемонстрировали высокую эффективность в лечении рефрактерных и рецидивирующих гематологических злокачественных новообразований. Расширение научно-исследовательской деятельности и увеличение инвестиций в биопрепараты ускоряют инновации в этом сегменте. Кроме того, растущее предпочтение пациентов перед передовыми вариантами лечения и расширение показаний к иммунотерапии способствуют его принятию. Стратегическое сотрудничество и партнерские отношения между ключевыми игроками способствуют дальнейшему росту сегмента.

- По диагнозу

На основе диагностики рынок сегментирован на анализы крови, биопсию, визуализационные тесты и другие. Сегмент анализов крови доминировал на рынке с самой большой долей доходов в 2025 году, что обусловлено его широким использованием в качестве основного и рутинного диагностического инструмента для выявления гематологических аномалий. Анализы крови являются экономически эффективными, минимально инвазивными и обеспечивают быстрые результаты, что делает их предпочтительными в клинических условиях. Растущее внедрение передовых диагностических технологий, таких как проточная цитометрия и молекулярное тестирование, еще больше повышает точность диагностики. Кроме того, регулярные медицинские осмотры и ранние программы скрининга повышают спрос в сегменте. Растущее бремя рака крови также увеличивает частоту диагностических тестов.

Ожидается, что в сегменте биопсии будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует его критическая роль в подтверждении диагностики рака и определении подтипа заболевания. Достижения в области методов биопсии и молекулярного профилирования улучшают диагностическую точность и позволяют персонализировать планирование лечения. Увеличение внедрения минимально инвазивных процедур биопсии повышает комфорт и соответствие пациентов. Кроме того, растущий спрос на точную постановку и прогноз приводит к необходимости диагностики на основе биопсии. Интеграция геномного тестирования с образцами биопсии еще больше ускоряет рост сегмента.

- По маршруту администрации

На основе пути администрирования рынок сегментирован на устный, парентеральный и другие. Парентеральный сегмент доминировал на рынке с самой большой долей дохода в 2025 году, чему способствовало широкое использование инъекционных методов лечения, таких как химиотерапия и биологические препараты в больницах. Парентеральное введение обеспечивает быструю доставку лекарств и более высокую биодоступность, что делает его пригодным для тяжелых и запущенных стадий заболевания. Растущее использование внутривенной иммунотерапии и таргетной терапии еще больше укрепляет этот сегмент. Кроме того, предпочтение контролируемого дозирования под медицинским наблюдением способствует его доминированию. Расширение инфраструктуры больниц и онкологических центров также способствует росту сегмента.

Ожидается, что пероральный сегмент станет свидетелем самых быстрых темпов роста с 2026 по 2033 год, чему способствует растущая доступность пероральной таргетной терапии и увеличение предпочтений пациентов в отношении удобных вариантов лечения. Пероральные препараты уменьшают потребность в частых посещениях больницы, улучшая соответствие пациентов и качество жизни. Достижения в области разработки лекарств и технологий доставки повышают эффективность пероральной терапии. Кроме того, переход к амбулаторному лечению и домашнему лечению поддерживает расширение сегмента. Увеличение одобрения пероральных онкологических препаратов способствует дальнейшему росту.

- По форме дозировки

На основе лекарственной формы рынок сегментирован на таблетки, капсулы, инъекции и другие. Сегмент инъекций доминировал на рынке с самой большой долей дохода в 2025 году, чему способствовало широкое использование инъекционных биопрепаратов, химиотерапевтических препаратов и иммунотерапии. Инъекции обеспечивают точное дозирование и быстрые терапевтические эффекты, что делает их необходимыми для условий критической помощи. Растущее внедрение передовых биологических методов лечения еще больше усиливает этот сегмент. Кроме того, сильная зависимость больницы от инъекционных препаратов поддерживает ее постоянное доминирование. Развитие новых систем доставки инъекционных наркотиков также способствует росту.

Ожидается, что в сегменте таблеток будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует растущий спрос на пероральную терапию и варианты лечения для пациентов. Таблетки обеспечивают простоту введения и улучшение приверженности пациента, особенно в долгосрочных схемах лечения. Растущий поток пероральных целевых терапий стимулирует расширение сегмента. Кроме того, достижения в области технологий рецептуры повышают стабильность и эффективность лекарств. Сдвиг в сторону амбулаторных и домашних условий лечения также поддерживает рост.

- конечными пользователями

На базе конечных пользователей рынок сегментирован на больницы, специализированные клиники, домашнюю помощь и другие. Сегмент больниц доминировал на рынке с наибольшей долей доходов в 2025 году, что обусловлено наличием передовых диагностических и лечебных учреждений. Больницы служат основными центрами для администрирования сложных методов лечения, таких как химиотерапия и лечение CAR-T. Наличие квалифицированных медицинских работников и комплексных услуг по уходу за пациентами еще больше укрепляет этот сегмент. Кроме того, увеличение притока пациентов для лечения рака поддерживает его доминирование. Государственное финансирование и развитие инфраструктуры также способствуют росту.

Ожидается, что в сегменте услуг по уходу на дому будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, что обусловлено растущим предпочтением лечения на дому и мониторинга. Достижения в области портативных медицинских устройств и пероральной терапии позволяют обеспечить эффективный уход на дому. Пациенты все чаще предпочитают уход на дому, чтобы сократить посещение больницы и связанные с этим расходы. Кроме того, расширение решений телемедицины и дистанционного мониторинга поддерживает этот сегмент. Растущее внимание к моделям ухода, ориентированным на пациента, еще больше стимулирует рост.

- Дистрибьюторский канал

На базе канала дистрибуции рынок сегментирован в больничную аптеку, розничную аптеку, онлайн-аптеку и другие. Сегмент больничных аптек доминировал на рынке с самой большой долей выручки в 2025 году, чему способствовал большой объем онкологических препаратов, отпускаемых в больницах. Больничные аптеки обеспечивают надлежащее хранение, обработку и введение специализированных лекарств. Растущее число стационарных процедур и процедур также поддерживает этот сегмент. Кроме того, сильная координация между поставщиками медицинских услуг и аптеками повышает эффективность лечения. Наличие в больничных аптеках широкого спектра онкологических препаратов усиливает их доминирование.

Ожидается, что в сегменте онлайн-аптек будут наблюдаться самые высокие темпы роста с 2026 по 2033 год, чему способствует растущее внедрение цифровых платформ здравоохранения и услуг электронной коммерции. Онлайн-аптеки предлагают удобство, доставку на дом и конкурентоспособные цены, привлекая все большее число пациентов. Растущее проникновение интернет-услуг и использование смартфонов еще больше поддерживают эту тенденцию. Кроме того, доступность лекарств для лечения хронических заболеваний через онлайн-каналы стимулирует рост. Регулятивная поддержка и улучшение логистической инфраструктуры также способствуют расширению сегмента.

Гематологические злокачественные образования рынок региональный анализ

- Северная Америка доминировала на рынке гематологических злокачественных новообразований с самой большой долей дохода в 42,15% в 2025 году, характеризующейся развитой инфраструктурой здравоохранения, высокими расходами на здравоохранение и сильным присутствием ведущих биофармацевтических компаний.

- Пациенты в регионе получают большую пользу от наличия передовых методов лечения, возможностей ранней диагностики и интегрированных систем здравоохранения, которые поддерживают комплексное лечение рака в больницах и специализированных центрах.

- Это широкое распространение также поддерживается высокими расходами на здравоохранение, сильным присутствием ведущих биофармацевтических компаний и хорошо налаженной экосистемой клинических исследований, устанавливая передовые гематологические методы лечения в качестве предпочтительного решения для эффективного управления заболеваниями среди различных групп пациентов.

Гематологические злокачественные опухоли США Market Insight

Рынок гематологических злокачественных новообразований в США занял самую большую долю доходов в Северной Америке в 2025 году, чему способствовала высокая распространенность рака крови и быстрое принятие передовых вариантов лечения, таких как иммунотерапия и таргетная терапия. Пациенты все чаще отдают приоритет доступу к инновационным и эффективным методам лечения рака, поддерживаемым сильной инфраструктурой здравоохранения. Растущее предпочтение подходов к точной медицине в сочетании с надежной деятельностью клинических испытаний и передовыми диагностическими возможностями еще больше продвигает рынок. Более того, растущая интеграция геномного тестирования и персонализированных стратегий лечения вносит значительный вклад в расширение рынка.

Европейское исследование рынка гематологических злокачественных опухолей

Согласно прогнозам, рынок гематологических злокачественных новообразований в Европе будет расширяться при существенном CAGR в течение прогнозируемого периода, главным образом за счет увеличения заболеваемости раком и сильной государственной поддержки онкологической помощи. Рост стареющего населения в сочетании с достижениями в области диагностических технологий способствует принятию инновационных вариантов лечения. Европейские пациенты также получают выгоду от улучшения доступа к медицинским услугам и системам возмещения. Регион переживает значительный рост в больницах и специализированных учреждениях, где передовые методы лечения включены как в стандартные протоколы лечения, так и в инициативы по клиническим исследованиям.

Британские гематологические злокачественные опухоли Market Insight

Ожидается, что в течение прогнозируемого периода рынок гематологических злокачественных новообразований в Великобритании будет расти при заметном CAGR, что обусловлено повышением осведомленности о ранней диагностике рака и достижениях в технологиях лечения. Кроме того, растущие инвестиции в здравоохранение и поддерживающие правительственные инициативы побуждают пациентов искать своевременные и эффективные методы лечения. Ожидается, что сильная клиническая исследовательская среда Великобритании, наряду с хорошо зарекомендовавшей себя системой здравоохранения, продолжит стимулировать рост рынка.

Немецкий рынок гематологических злокачественных опухолей

Ожидается, что в течение прогнозируемого периода рынок гематологических злокачественных новообразований в Германии будет расширяться на значительном CAGR, чему будет способствовать растущее внедрение передовых методов лечения онкологии и сильный акцент на исследованиях и инновациях. Хорошо развитая инфраструктура здравоохранения Германии в сочетании с акцентом на прецизионную медицину способствует принятию целевых и иммунотерапевтических методов лечения. Интеграция передовой диагностики с планированием лечения также становится все более распространенной, при этом предпочтение высококачественной и эффективной терапии рака соответствует ожиданиям пациентов.

Азиатско-Тихоокеанский рынок гематологических злокачественных опухолей

Рынок гематологических злокачественных новообразований в Азиатско-Тихоокеанском регионе будет расти самыми быстрыми темпами в течение прогнозируемого периода с 2026 по 2033 год, что обусловлено увеличением расходов на здравоохранение, ростом распространенности рака и улучшением доступа к передовым вариантам лечения в таких странах, как Китай, Япония и Индия. Растущее внимание региона к развитию инфраструктуры здравоохранения, поддерживаемое правительственными инициативами, стимулирует внедрение гематологических методов лечения рака. Кроме того, по мере того, как Азиатско-Тихоокеанский регион становится ключевым регионом для клинических испытаний и фармацевтического производства, доступность и доступность лечения расширяется.

Японский рынок гематологических злокачественных опухолей

Рынок гематологических злокачественных новообразований в Японии набирает обороты благодаря передовой системе здравоохранения страны, старению населения и сильному акценту на инновации в лечении рака. Японский рынок уделяет большое внимание ранней диагностике и эффективному лечению заболеваний, а внедрение передовых методов лечения обусловлено увеличением клинической исследовательской деятельности. Интеграция новых подходов к лечению с передовой диагностикой способствует росту. Кроме того, стареющее население Японии, вероятно, будет стимулировать спрос на эффективные и доступные решения по лечению рака как в больницах, так и в специализированных учреждениях.

Рынок гематологических злокачественных новообразований Индии

Рынок гематологических злокачественных новообразований в Индии составил значительную долю рынка в Азиатско-Тихоокеанском регионе в 2025 году, что связано с ростом бремени рака в стране, расширением инфраструктуры здравоохранения и повышением осведомленности о ранней диагностике и лечении. Индия является одним из самых быстрорастущих рынков для онкологической помощи, и лечение гематологических злокачественных новообразований становится все более доступным в городских и полугородских районах. Стремление к улучшению доступа к здравоохранению и доступности экономически эффективных вариантов лечения наряду с сильным отечественным фармацевтическим производством являются ключевыми факторами, стимулирующими рынок в Индии.

Каковы основные компании на рынке гематологических злокачественных новообразований

Отрасль гематологических злокачественных новообразований в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- Pfizer Inc. (США)

- F. Hoffmann-La Roche Ltd (Швейцария)

- Санофи (Франция)

- Бристол Майерс Сквибб (США)

- AbbVie Inc. (США)

- Novartis AG (Швейцария)

- GSK plc (Великобритания)

- Amgen Inc. (США)

- Takeda Pharmaceutical Company Limited (Япония)

- AstraZeneca PLC (Великобритания)

- Merck & Co., Inc. (США)

- Eli Lilly & Company (США)

- Gilead Sciences, Inc. (США)

- Regeneron Pharmaceuticals, Inc. (США)

- Incyte Corporation (США)

- BeiGene, Ltd. (Китай)

- Bluebird Bio, Inc. (США)

- Atara Biotherapeutics, Inc. (США)

- Celldex Therapeutics, Inc. (США)

Каковы последние события на мировом рынке гематологических злокачественных новообразований

- В декабре 2025 года Бристол Майерс Сквибб объявил, что FDA США одобрило Breyanzi (lisocabtagene maraleucel) для лечения взрослых пациентов с рецидивирующей или рефрактерной лимфомой маргинальной зоны, отметив первую терапию CAR-T, одобренную для этого показания. Одобрение было основано на сильных клинических результатах, демонстрирующих высокие показатели ответа у пациентов, подвергшихся интенсивной предварительной обработке. Эта разработка подчеркивает продолжающееся расширение терапии CAR-T при множественных гематологических злокачественных новообразованиях и усиливает их роль в качестве преобразующих вариантов лечения.

- В декабре 2025 года исследователи представили результаты на ежегодном собрании Американского общества гематологии, показывающие, что сочетание терапии CAR-T-клетками с биспецифическими антителами и конъюгатами антител-лекарств значительно улучшает выживаемость без прогрессирования у пациентов с лимфомой. Этот новый комбинированный подход направлен на повышение долговечности лечения и преодоление проблем с рецидивами. Исследование отражает растущую тенденцию к мультимодальной терапии для улучшения долгосрочных результатов при гематологическом раке.

- В июне 2025 года Управление по санитарному надзору за качеством пищевых продуктов и медикаментов США отменило требование по оценке рисков и стратегиям смягчения (REMS) для одобренной терапии CAR-T-клетками, уменьшив нормативную нагрузку на поставщиков медицинских услуг и улучшив доступ пациентов. Это решение влияет на несколько методов лечения, используемых при лейкемии, лимфоме и множественной миеломе. Ожидается, что этот шаг упростит доставку лечения и ускорит принятие передовых методов иммунотерапии в клинической практике.

- В ноябре 2024 года Roche объявила о приобретении Poseida Therapeutics на сумму до 1,5 млрд долларов США для укрепления своего трубопровода аллогенных методов лечения CAR-T, направленных на гематологические злокачественные опухоли. Сделка отражает увеличение стратегических инвестиций в клеточную терапию следующего поколения и подчеркивает конкурентный ландшафт инноваций в лечении рака крови. Ожидается, что это приобретение повысит возможности Roche в разработке масштабируемой и готовой иммунотерапии.

- В мае 2024 года Управление по контролю за продуктами и лекарствами США расширило использование терапии Breyanzi CAR-T для пациентов с рецидивирующей или рефрактерной лимфомой мантийных клеток, основываясь на клинических данных, показывающих значительные показатели ответа на рак. Это стало одним из многочисленных расширений для CAR-T терапии рака крови, демонстрируя их растущую клиническую применимость. Расширение также отражает растущую уверенность в клеточной терапии в качестве стандартных вариантов лечения трудно поддающихся лечению гематологических злокачественных новообразований.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.