Global Human Papillomavirus Infection Drugs Market

Размер рынка в млрд долларов США

CAGR :

%

USD

8.00 Billion

USD

13.74 Billion

2025

2033

USD

8.00 Billion

USD

13.74 Billion

2025

2033

| 2026 –2033 | |

| USD 8.00 Billion | |

| USD 13.74 Billion | |

| % | |

|

Global Human Papillomavirus Infection Drugs Market Segmentation, By Diseases (Cervical Cancer, Anal Cancer, Genital Warts, and Others), Drugs (Immunomodulators, Keratolytics, Antineoplastics, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy) - Industry Trends and Forecast to 2033

Human Papillomavirus Infection Drugs Market Size

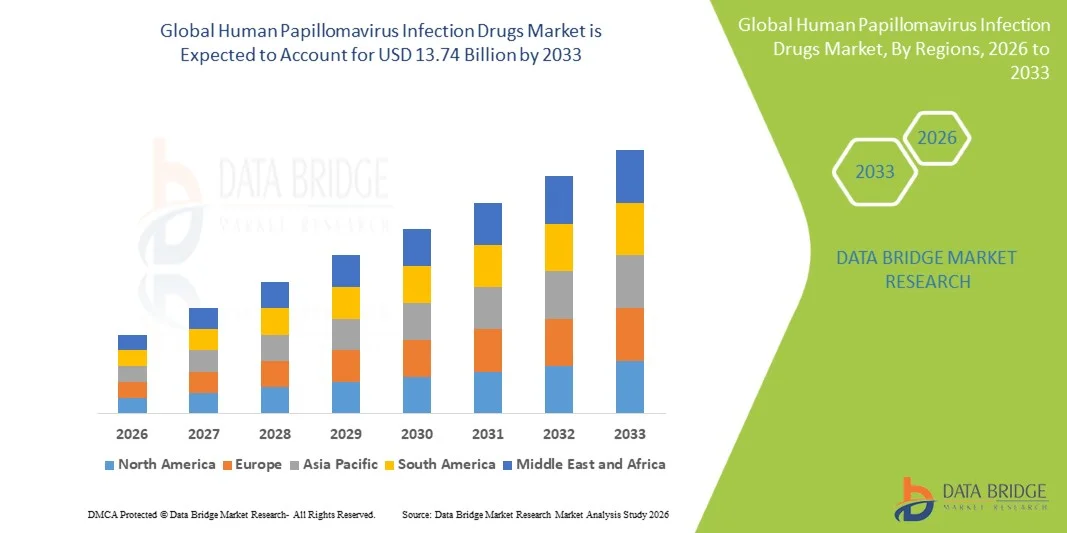

- The global human papillomavirus infection drugs market size was valued at USD 8.00 billion in 2025 and is expected to reach USD 13.74 billion by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of human papillomavirus (HPV) infections worldwide, along with rising awareness regarding early diagnosis and treatment options, leading to greater adoption of antiviral and immunotherapy-based treatments across healthcare settings

- Furthermore, growing demand for effective, safe, and targeted treatment solutions, coupled with advancements in therapeutic approaches and increasing vaccination awareness, is establishing Human Papillomavirus Infection Drugs as a critical component in infection management. These converging factors are accelerating the uptake of Human Papillomavirus Infection Drugs solutions, thereby

Human Papillomavirus Infection Drugs Market Analysis

- Human Papillomavirus (HPV) Infection Drugs, including antiviral agents, immune response modifiers, and therapeutic vaccines, are increasingly important in managing HPV-related conditions such as genital warts and HPV-associated cancers. These treatments are gaining prominence across healthcare settings due to their role in reducing disease progression and improving patient outcomes

- The escalating demand for HPV infection drugs is primarily fueled by the rising global prevalence of HPV infections, increasing awareness regarding sexually transmitted infections, and growing screening and diagnosis rates. In addition, advancements in targeted therapies and immunotherapies are further supporting the adoption of more effective treatment options

- North America dominated the human papillomavirus infection drugs market with the largest revenue share of 37.6% in 2025, characterized by strong healthcare infrastructure, high awareness levels, and widespread screening programs. The U.S. is witnessing significant growth driven by increased diagnosis rates, availability of advanced therapeutics, and strong presence of key pharmaceutical players

- Asia-Pacific is expected to be the fastest growing region in the human papillomavirus infection drugs market during the forecast period due to increasing population, rising awareness of HPV-related diseases, improving healthcare access, and expanding vaccination and screening initiatives across countries such as China and India

- The Oral segment dominated the market with a revenue share of 49.5% in 2025, driven by ease of administration and high patient compliance

Report Scope and Human Papillomavirus Infection Drugs Market Segmentation

|

Attributes |

Human Papillomavirus Infection Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Human Papillomavirus Infection Drugs Market Trends

“Growing Focus on Targeted Therapies and Immunomodulatory Treatments”

- A significant and accelerating trend in the global Human Papillomavirus (HPV) Infection Drugs market is the increasing focus on targeted therapies and immunomodulatory treatments aimed at improving the management of HPV-related conditions, including genital warts and HPV-associated cancers

- For instance, topical treatments such as imiquimod and podophyllotoxin are widely used for the treatment of external genital warts, while therapeutic vaccines and immune-based therapies are being explored to enhance the body’s ability to clear persistent HPV infections

- The development of therapeutic HPV vaccines, unlike preventive vaccines, is gaining traction as they aim to treat existing infections and associated lesions by stimulating a targeted immune response

- Increasing research into antiviral agents that directly inhibit HPV replication is further contributing to the evolution of treatment options, although this area is still in developmental stages

- In addition, combination therapies integrating immunotherapy with conventional treatment approaches are being explored to improve treatment efficacy and reduce recurrence rates

- Growing awareness regarding HPV-related cancers, particularly cervical cancer, is encouraging early treatment and boosting demand for effective drug therapies

- Pharmaceutical companies are investing heavily in clinical trials and pipeline development focused on novel mechanisms of action for HPV treatment

- This shift toward advanced, targeted, and immune-based therapies is reshaping the treatment landscape and driving innovation in the HPV infection drugs market

Human Papillomavirus Infection Drugs Market Dynamics

Driver

“Rising Prevalence of HPV Infections and Increasing Awareness Programs”

- The increasing prevalence of Human Papillomavirus infections globally is a major driver of the HPV Infection Drugs market, as HPV remains one of the most common sexually transmitted infections worldwide

- For instance, the high global burden of cervical cancer, largely caused by persistent HPV infection, has led to increased demand for treatment options, particularly in developing regions where screening and vaccination coverage remain limited

- Growing awareness initiatives by governments and health organizations regarding HPV prevention, screening, and treatment are significantly contributing to early diagnosis and increased treatment uptake

- Expansion of screening programs, including Pap smears and HPV DNA testing, is enabling early detection of HPV-related abnormalities, thereby increasing the demand for therapeutic interventions

- Rising healthcare expenditure and improved access to medical facilities are supporting the adoption of HPV-related treatments across both developed and emerging markets

- Increasing focus on women’s health and reproductive health is also driving demand for effective HPV management solutions

- In addition, the growing number of HPV-related cases among both men and women is expanding the target patient population for treatment

- Ongoing research and development activities aimed at improving treatment efficacy and reducing recurrence rates are further accelerating market growth

- The combined impact of increasing disease burden, awareness, and healthcare accessibility is significantly driving the expansion of the HPV Infection Drugs market

Restraint/Challenge

“Limited Availability of Curative Treatments and High Treatment Costs”

- One of the key challenges in the Human Papillomavirus Infection Drugs market is the limited availability of definitive curative treatments, as most existing therapies focus on managing symptoms and lesions rather than completely eradicating the virus

- For instance, commonly used treatments such as cryotherapy, topical agents, and surgical procedures primarily remove visible warts or lesions but do not eliminate the underlying HPV infection, leading to potential recurrence

- The absence of highly effective antiviral drugs specifically targeting HPV limits treatment outcomes and creates an unmet clinical need in the market

- High treatment costs, particularly for advanced therapies and procedures, can restrict access for patients in low- and middle-income regions

- Social stigma and lack of awareness associated with sexually transmitted infections often delay diagnosis and treatment, further complicating disease management

- Variability in treatment response and recurrence rates also pose challenges for healthcare providers in selecting optimal treatment strategies

- Limited access to healthcare services and screening programs in certain regions continues to hinder early diagnosis and timely treatment

- In addition, regulatory challenges and lengthy clinical trial processes for new therapies slow down the introduction of innovative treatment options

- Addressing these challenges through increased research, improved access to care, and development of more effective therapies will be critical for sustained market growth

Human Papillomavirus Infection Drugs Market Scope

The market is segmented on the basis of diseases, drugs, route of administration, end-users, and distribution channel.

• By Diseases

On the basis of diseases, the Human Papillomavirus Infection Drugs market is segmented into Cervical Cancer, Anal Cancer, Genital Warts, and Others. The Cervical Cancer segment dominated the market with the largest revenue share of 42.7% in 2025, driven by the high global prevalence of HPV-related cervical cancer among women. Increasing awareness regarding early screening and HPV-related complications significantly contributes to treatment demand. Governments and healthcare organizations are actively promoting cervical cancer screening programs, boosting diagnosis rates. Strong clinical focus on targeted therapies and immunotherapies enhances treatment adoption. Availability of multiple therapeutic options including antineoplastics and immunomodulators supports growth. Rising healthcare expenditure and improved access to oncology treatments further strengthen the segment. Hospitals and specialty clinics remain key treatment centers for cervical cancer. Continuous advancements in precision medicine improve patient outcomes. Favorable reimbursement policies in developed regions enhance accessibility. Overall, cervical cancer remains the dominant disease segment in the market.

The Genital Warts segment is expected to witness the fastest CAGR of 15.9% from 2026 to 2033, driven by increasing incidence of HPV infections and rising awareness regarding sexually transmitted diseases. Genital warts represent one of the most common manifestations of HPV, particularly among younger populations. Growing demand for early-stage treatment and non-invasive therapies supports market growth. Availability of topical drugs such as immunomodulators and keratolytics enhances accessibility. Increasing adoption of outpatient treatment options further accelerates demand. Expanding sexual health awareness programs contribute to higher diagnosis rates. Rising preference for cost-effective and quick treatment solutions supports uptake. Pharmaceutical innovations in topical formulations improve efficacy and patient compliance. Increasing presence of retail and online pharmacies enhances drug availability. Overall, genital warts represent the fastest-growing disease segment.

• By Drugs

On the basis of drugs, the market is segmented into Immunomodulators, Keratolytics, Antineoplastics, and Others. The Immunomodulators segment dominated the market with a revenue share of 37.8% in 2025, driven by their effectiveness in enhancing the body’s immune response against HPV infections. These drugs are widely used in treating genital warts and early-stage HPV infections. Increasing preference for non-invasive and topical treatment options boosts adoption. Immunomodulators such as imiquimod are commonly prescribed due to favorable safety profiles. Rising awareness regarding immune-based therapies supports market growth. Strong demand in outpatient and homecare settings enhances accessibility. Pharmaceutical advancements improve drug formulations and reduce side effects. Physicians prefer immunomodulators for their targeted action and ease of use. Growing incidence of HPV infections globally further drives demand. Overall, immunomodulators remain the dominant drug segment.

The Antineoplastics segment is expected to witness the fastest CAGR of 16.6% from 2026 to 2033, driven by increasing cases of HPV-related cancers such as cervical and anal cancer. Rising adoption of chemotherapy and targeted oncology therapies significantly contributes to growth. Strong pipeline of advanced cancer drugs enhances treatment outcomes. Increasing investment in oncology research and drug development accelerates market expansion. Hospitals and specialty oncology centers are key adopters of antineoplastic therapies. Growing awareness regarding early cancer treatment boosts demand. Integration of combination therapies improves effectiveness and survival rates. Favorable reimbursement for cancer treatments supports accessibility. Expanding healthcare infrastructure in emerging markets further drives growth. Overall, antineoplastics represent the fastest-growing drug segment.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Parenteral, and Others. The Oral segment dominated the market with a revenue share of 49.5% in 2025, driven by ease of administration and high patient compliance. Oral drugs are widely prescribed for HPV-related conditions due to convenience and non-invasive delivery. Patients prefer oral medications for long-term therapy management. Availability of cost-effective generic oral drugs enhances accessibility. Strong distribution through retail pharmacies supports widespread adoption. Physicians commonly recommend oral therapies for initial and maintenance treatment. High patient adherence rates contribute to consistent demand. Pharmaceutical companies focus on improving oral formulations for better absorption. Increasing prevalence of HPV infections supports sustained growth. Overall, oral administration remains the dominant segment.

The Parenteral segment is expected to witness the fastest CAGR of 15.4% from 2026 to 2033, driven by rising use of injectable therapies for HPV-related cancers. Parenteral administration ensures rapid drug delivery and higher bioavailability. Hospitals widely adopt injectable treatments for advanced-stage cancer patients. Increasing demand for targeted and biologic therapies supports segment growth. Technological advancements in drug delivery systems enhance safety and effectiveness. Growing preference for hospital-based treatments boosts demand. Expansion of oncology care infrastructure further accelerates adoption. Rising healthcare expenditure supports access to advanced therapies. Overall, parenteral administration is the fastest-growing segment.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated the market with a revenue share of 51.2% in 2025, driven by high patient inflow for diagnosis and treatment of HPV-related conditions. Hospitals provide advanced diagnostic tools and specialized care for cancer treatment. Availability of skilled healthcare professionals supports effective disease management. Strong adoption of oncology therapies and immunotherapies enhances market share. Hospitals serve as primary centers for complex procedures and drug administration. Government funding and reimbursement policies improve accessibility. Increasing number of hospital-based screening programs boosts diagnosis rates. Collaboration with pharmaceutical companies supports adoption of advanced therapies. Overall, hospitals dominate the end-user segment.

The Homecare segment is expected to witness the fastest CAGR of 16.1% from 2026 to 2033, driven by increasing preference for self-administered and home-based treatments. Patients prefer convenient and cost-effective care options for managing HPV-related conditions. Growing availability of topical and oral therapies supports homecare adoption. Telemedicine and remote consultations enhance treatment accessibility. Rising awareness about personal health management boosts demand. Aging population and chronic disease prevalence further support growth. Healthcare systems promote homecare to reduce hospital burden. Easy-to-use drug formulations improve patient compliance. Overall, homecare is the fastest-growing end-user segment.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Retail Pharmacy segment dominated the market with a revenue share of 45.6% in 2025, driven by widespread availability of HPV treatment drugs and easy accessibility. Retail pharmacies serve as key points for dispensing oral and topical medications. Strong presence in both urban and rural areas enhances reach. Pharmacists play an important role in patient guidance and adherence. Availability of generic drugs improves affordability. Increasing prescription volume for HPV-related conditions supports growth. Established supply chains ensure consistent availability. Patients prefer retail pharmacies for convenience and repeat purchases. Overall, retail pharmacy dominates the distribution channel segment.

The Online Pharmacy segment is expected to witness the fastest CAGR of 17.3% from 2026 to 2033, driven by increasing digital healthcare adoption and consumer preference for convenience. Online platforms offer home delivery, competitive pricing, and subscription-based services. Rising internet penetration supports rapid growth. Integration with telehealth services enhances prescription access. Patients prefer discreet purchasing options for sensitive conditions. Expanding logistics infrastructure ensures timely delivery. Regulatory support for e-pharmacies boosts trust. Growing awareness of digital health solutions accelerates adoption. Overall, online pharmacy is the fastest-growing distribution channel segment.

Human Papillomavirus Infection Drugs Market Regional Analysis

- North America dominated the Human Papillomavirus Infection Drugs market with the largest revenue share of 37.6% in 2025, characterized by strong healthcare infrastructure, high awareness levels, and widespread screening programs

- The region benefits from well-established cervical cancer screening initiatives and increasing use of prescription treatments for HPV-related conditions. For instance, the widespread adoption of therapies such as imiquimod and other topical agents in the U.S. and Canada is supporting effective management of HPV-related lesions and genital warts

- This dominance is further supported by high diagnosis rates, availability of advanced therapeutics, strong presence of key pharmaceutical players, and favorable reimbursement frameworks, establishing North America as a leading market for HPV infection treatment

U.S. Human Papillomavirus Infection Drugs Market Insight

The U.S. human papillomavirus infection drugs market captured the largest revenue share in 2025 within North America, driven by increased diagnosis rates, strong awareness programs, and availability of advanced treatment options. Healthcare providers and patients are increasingly focusing on early detection and timely treatment of HPV-related conditions, particularly cervical cancer and genital warts. In addition, the presence of leading pharmaceutical companies and ongoing clinical research is supporting the introduction of innovative therapies. Moreover, strong government initiatives, widespread screening programs such as Pap tests and HPV DNA testing, and improved access to healthcare services are significantly contributing to the growth of the HPV Infection Drugs market in the United States.

Europe Human Papillomavirus Infection Drugs Market Insight

The Europe human papillomavirus infection drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness regarding HPV-related diseases and strong public healthcare systems. The region is witnessing rising adoption of screening and treatment programs. For instance, countries such as Germany and France have implemented national cervical cancer screening initiatives, improving early diagnosis and treatment rates. In addition, growing government support, increasing vaccination coverage, and improved access to healthcare services are contributing to steady market growth across Europe.

U.K. Human Papillomavirus Infection Drugs Market Insight

The U.K. human papillomavirus infection drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong public health initiatives and increasing awareness regarding HPV infections. National screening programs and awareness campaigns are encouraging early diagnosis and treatment of HPV-related conditions. Furthermore, the availability of effective treatment options through public healthcare systems is supporting market expansion. The increasing focus on women’s health and preventive care is further contributing to the growth of the HPV Infection Drugs market in the U.K.

Germany Human Papillomavirus Infection Drugs Market Insight

The Germany human papillomavirus infection drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and strong emphasis on preventive healthcare. Germany is witnessing increased adoption of both screening and treatment solutions. For instance, structured cervical cancer screening programs are enabling early detection and improving treatment outcomes for HPV-related conditions. In addition, increasing healthcare expenditure, strong regulatory frameworks, and growing awareness are supporting market growth in the country.

Asia-Pacific Human Papillomavirus Infection Drugs Market Insight

The Asia-Pacific human papillomavirus infection drugs market is expected to be the fastest growing region during the forecast period due to increasing population, rising awareness of HPV-related diseases, improving healthcare access, and expanding vaccination and screening initiatives. The region is experiencing a growing burden of HPV infections, particularly in developing countries. For instance, countries such as China and India are expanding national screening and vaccination programs, which is increasing diagnosis and treatment rates. Furthermore, improving healthcare infrastructure, rising disposable incomes, and growing focus on women’s health are significantly contributing to regional market growth.

Japan Human Papillomavirus Infection Drugs Market Insight

The Japan human papillomavirus infection drugs market is gaining momentum due to strong healthcare infrastructure and increasing awareness regarding HPV-related diseases. The country is focusing on early detection and effective management of HPV infections. For instance, increased adoption of screening programs and treatment options is supporting better disease management outcomes. In addition, rising healthcare expenditure and government initiatives aimed at improving preventive healthcare are driving demand for HPV infection drugs in Japan.

China Human Papillomavirus Infection Drugs Market Insight

The China human papillomavirus infection drugs market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to its large population base, increasing healthcare investments, and rising awareness of HPV-related conditions. The country is witnessing significant improvements in screening and treatment accessibility. For instance, expansion of cervical cancer screening programs and increased availability of treatment options are supporting higher diagnosis and therapy adoption rates. Government initiatives, growing healthcare infrastructure, and increasing focus on women’s health are further propelling the growth of the Human Papillomavirus Infection Drugs market in China.

Human Papillomavirus Infection Drugs Market Share

The Human Papillomavirus Infection Drugs industry is primarily led by well-established companies, including:

- Pfizer (U.S.)

- Merck & Co. (U.S.)

- GSK (U.K.)

- F. Hoffmann-La Roche (Switzerland)

- Bristol Myers Squibb (U.S.)

- Novartis (Switzerland)

- Sanofi (France)

- AstraZeneca (U.K.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries (Israel)

- Bayer (Germany)

- AbbVie (U.S.)

- Amgen (U.S.)

- Sun Pharmaceutical Industries (India)

- Dr. Reddy’s Laboratories (India)

- Lupin (India)

- Cipla (India)

- Zydus Lifesciences (India)

- Aurobindo Pharma (India)

- Glenmark Pharmaceuticals (India)

Latest Developments in Global Human Papillomavirus Infection Drugs Market

- In October 2021, the U.S. Food and Drug Administration (FDA) approved an expanded indication for Gardasil 9 (Human Papillomavirus 9-valent Vaccine, Recombinant) manufactured by Merck, supporting its continued use in preventing HPV-related cancers and diseases, reinforcing vaccination as a key preventive strategy alongside therapeutic interventions

- In December 2022, the World Health Organization (WHO) recommended a single-dose schedule for HPV vaccines, marking a major global policy shift aimed at improving vaccine access and coverage, particularly in low- and middle-income countries, thereby influencing the broader HPV treatment and prevention landscape

- In July 2023, Precigen, Inc. reported positive Phase 2 clinical trial results for PRGN-2012, an investigational gene therapy targeting recurrent respiratory papillomatosis (RRP) caused by HPV, demonstrating meaningful clinical responses and advancing therapeutic innovation beyond traditional treatments

- In April 2024, Inovio Pharmaceuticals announced continued progress of its DNA-based immunotherapy candidate VGX-3100 for the treatment of HPV-related cervical dysplasia, with late-stage clinical development focusing on non-surgical treatment options for HPV-associated precancerous lesions

- In June 2024, the European Commission granted approval for expanded use of Gardasil 9 across broader populations in Europe, strengthening prevention strategies and indirectly impacting demand for HPV-related therapeutic management

- In March 2025, Precigen, Inc. announced further positive data from its ongoing clinical program for PRGN-2012, reinforcing its potential as a novel immunotherapy for HPV-driven diseases and supporting continued advancement toward regulatory submission

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.