Global In Vitro Diagnostics Ivd Quality Control Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.24 Billion

USD

1.73 Billion

2025

2033

USD

1.24 Billion

USD

1.73 Billion

2025

2033

| 2026 –2033 | |

| USD 1.24 Billion | |

| USD 1.73 Billion | |

| % | |

|

Global In Vitro Diagnostics (IVD) Quality Control Market Segmentation, By Product and Service (Quality Control Products, Data Management Solutions, and Quality Assurance Services), Application (Immunochemistry/Immunoassay, Clinical Chemistry, Hematology, Molecular Diagnostics, Coagulation and Hemostasis, Microbiology, and Others), Manufacturer Type (Third-Party Control Manufacturers, and Original Equipment Manufacturers), End- Users (Hospitals, Clinical Laboratories, Academic and Research Institutes, and Other End Users) - Industry Trends and Forecast to 2033

In Vitro Diagnostics (IVD) Quality Control Market Size

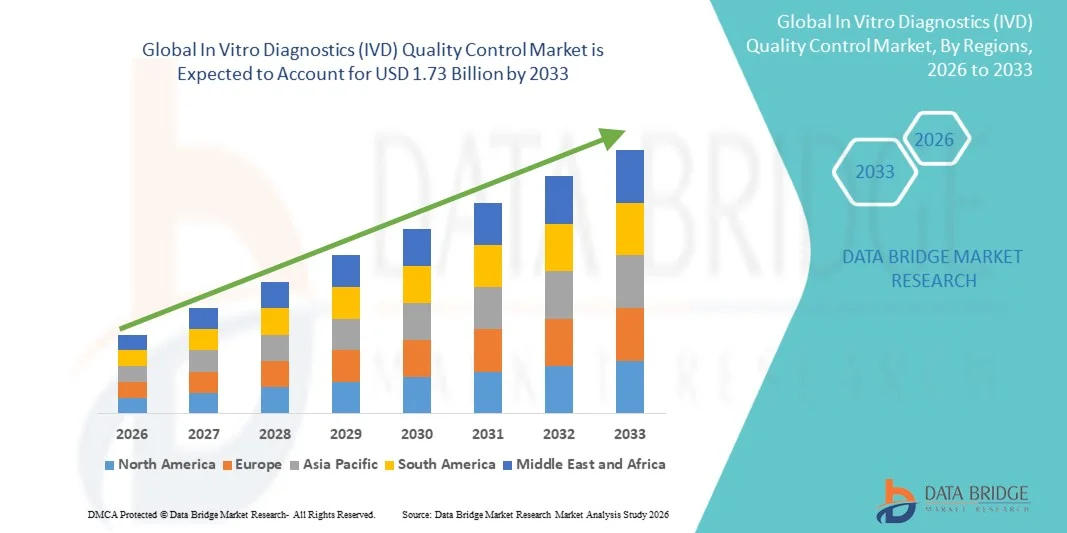

- The global In vitro diagnostics (IVD) quality control market size was valued at USD 1.24 billion in 2025 and is expected to reach USD 1.73 billion by 2033, at a CAGR of 4.30% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced diagnostic technologies, growing emphasis on patient safety, and the rising need for accurate and reliable laboratory testing in both clinical and research settings

- Furthermore, stringent regulatory standards, coupled with the demand for standardized and reproducible test results, are driving the uptake of In Vitro Diagnostics (IVD) Quality Control solutions, thereby significantly boosting the industry's growth

In Vitro Diagnostics (IVD) Quality Control Market Analysis

- In Vitro Diagnostics (IVD) Quality Control solutions, offering automated and AI-assisted systems for laboratories and hospitals, are increasingly vital components of modern clinical and research workflows in both healthcare and diagnostic settings due to their enhanced accuracy, efficiency, and seamless integration with laboratory information system

- The escalating demand for IVD Quality Control solutions is primarily fueled by the widespread adoption of advanced diagnostic technologies, increasing regulatory requirements, and a rising preference for reliable, real-time quality monitoring and standardized testing protocols

- North America dominated the in vitro diagnostics (IVD) quality control market with the largest revenue share of 46.5% in 2025, characterized by advanced laboratory infrastructure, high adoption of automated diagnostic technologies, and a strong presence of key IVD companies, with the U.S. experiencing substantial growth in QC system installations, particularly in hospitals, clinical laboratories, and research centers, driven by innovations from both established and emerging players focusing on automation and AI-based monitoring features

- Asia-Pacific is expected to be the fastest growing region in the in vitro diagnostics (IVD) quality control market during the forecast period, with a projected CAGR of 12.3%, fueled by increasing healthcare expenditure, rising prevalence of chronic and infectious diseases, and expanding adoption of automated quality control systems in countries such as China, India, and Japan

- The OEMs segment dominated the largest market revenue share of 51.3% in 2025, as hospitals and laboratories prefer integrated QC products designed specifically for their diagnostic instruments

Report Scope and In Vitro Diagnostics (IVD) Quality Control Market Segmentation

|

Attributes |

In Vitro Diagnostics (IVD) Quality Control Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Bio-Rad Laboratories (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

In Vitro Diagnostics (IVD) Quality Control Market Trends

“Advancements in Diagnostic Technologies and Automation”

- A key trend in the global IVD quality control market is the growing adoption of automated quality control systems and next-generation diagnostic platforms. Laboratories are increasingly implementing high-throughput, automated analyzers that reduce human error, improve efficiency, and ensure consistency in testing results

- For instance, major diagnostic laboratories in Europe and North America are integrating multiplexed quality control panels that allow simultaneous monitoring of multiple assays, enhancing efficiency and ensuring reliable results across diverse test types

- Another emerging trend is the integration of advanced assay validation software that supports real-time monitoring of test performance, helping laboratories comply with regulatory standards and maintain high-quality testing workflows

- Furthermore, there is an increased focus on standardized quality control protocols across global laboratory networks. Leading hospitals and diagnostic centers are implementing centralized QC dashboards to track performance metrics across multiple sites, improving consistency, reducing turnaround times, and minimizing operational inefficiencies

- The trend towards miniaturized and portable QC solutions is also gaining momentum. These devices enable rapid on-site testing in outpatient clinics, emergency settings, and remote areas, ensuring timely and accurate diagnostics without relying on large centralized laboratories

In Vitro Diagnostics (IVD) Quality Control Market Dynamics

Driver

“Rising Demand for Accurate and Rapid Diagnostic Testing”

- The increasing prevalence of chronic diseases, infectious diseases, and lifestyle-related conditions is driving the demand for reliable IVD quality control solutions. Accurate diagnostic results are critical for effective treatment planning, early intervention, and patient management

- For instance, in 2025, hospitals and clinical laboratories in the U.S., Germany, and Japan reported heightened adoption of automated IVD QC systems to support high-volume testing during outbreaks such as influenza and dengue, as well as routine monitoring of metabolic disorders

- Growing regulatory compliance requirements from organizations such as the FDA, ISO, and CLIA are pushing laboratories to implement standardized QC procedures, ensuring consistent accuracy and reliability in test outcomes

- The rising adoption of personalized medicine and targeted therapies is further fueling the market. Laboratories require highly accurate quality control systems to validate diagnostic tests that guide individualized treatment plans, such as cancer biomarker panels and immunoassays

- In addition, the increasing collaboration between diagnostic manufacturers and hospitals to streamline QC protocols is enhancing operational efficiency, reducing test errors, and improving overall patient care

Restraint/Challenge

“High Costs and Limited Infrastructure in Developing Regions”

- The high initial cost of advanced IVD quality control systems, coupled with ongoing maintenance and calibration expenses, poses challenges to adoption, particularly for smaller laboratories and healthcare facilities in developing regions

- For instance, clinics in Southeast Asia, Africa, and parts of Latin America still rely on manual QC procedures due to the prohibitive cost of automated platforms, limited infrastructure, and scarcity of skilled laboratory personnel

- Addressing these challenges requires cost-effective solutions, such as modular QC systems, subscription-based models, and shared laboratory facilities, which can provide access to high-quality diagnostics at reduced capital expense

- Furthermore, inconsistent electricity supply, limited access to high-quality reagents, and inadequate technical training can hinder the reliability and performance of QC systems, especially in remote or resource-constrained settings

- Government initiatives, international funding programs, and partnerships with global diagnostic companies are essential to build infrastructure, provide training, and improve the accessibility of IVD quality control systems, thereby supporting long-term market growth

- In addition, the perception of high operational complexity associated with automated QC systems may discourage adoption in smaller clinics. Simplified, user-friendly platforms with robust technical support are critical to overcoming this barrier

In Vitro Diagnostics (IVD) Quality Control Market Scope

The market is segmented on the basis of Product & Service, Application, Manufacturer Type, End-Users, and Distribution Channel.

• By Product and Service

On the basis of product and service, the In Vitro Diagnostics (IVD) Quality Control market is segmented into Quality Control Products, Data Management Solutions, and Quality Assurance Services. The Quality Control Products segment dominated the largest market revenue share of 47.5% in 2025, driven by their essential role in ensuring accurate and reliable diagnostic results. Hospitals and clinical laboratories prioritize validated QC products to meet regulatory standards. Adoption is fueled by the increasing prevalence of chronic and infectious diseases. QC products help reduce diagnostic errors and improve patient safety. Integration with laboratory automation enhances workflow efficiency. Consistent product quality builds trust among clinicians and lab technicians. The growing number of high-throughput labs and diagnostic centers supports dominance. Standardized QC products reduce variability in test results. Market leadership is reinforced by established global suppliers. The segment benefits from continuous technological innovations in assay calibration. Regulatory compliance and accreditation programs further strengthen adoption.

The Data Management Solutions segment is expected to witness the fastest CAGR of 15.2% from 2026 to 2033, driven by the rising need for centralized laboratory data monitoring and analytics. Cloud-based QC platforms enable real-time performance tracking. AI-enabled dashboards improve error detection and reporting. Interfacing with multiple diagnostic instruments enhances lab efficiency. Hospitals increasingly adopt digital solutions for quality assurance. Growing demand for remote monitoring supports market expansion. Integration with laboratory information systems ensures seamless operations. Advanced analytics help identify trends and deviations in QC results. Telehealth and decentralized testing increase reliance on digital management. Expansion of large diagnostic networks accelerates adoption. Investments in cybersecurity and compliance boost confidence in digital solutions.

• By Application

On the basis of application, the market is segmented into Immunochemistry/Immunoassay, Clinical Chemistry, Hematology, Molecular Diagnostics, Coagulation and Hemostasis, Microbiology, and Others. The Clinical Chemistry segment dominated with a market revenue share of 42.8% in 2025, owing to its wide adoption for routine blood and biochemical testing. Automation in clinical chemistry laboratories reduces errors and turnaround times. Hospitals and large diagnostic chains prioritize QC for chemistry analyzers. Standardization of reagents enhances reliability. Growing prevalence of metabolic and cardiovascular disorders drives demand. Regulatory bodies mandate stringent QC protocols for clinical chemistry. Integration with laboratory management software improves operational efficiency. Urban laboratories show higher adoption due to advanced infrastructure. Continuous innovations in analyzers strengthen segment leadership. Availability of ready-to-use controls enhances convenience. Clinical chemists rely on QC to maintain accreditation standards. Expansion of outpatient labs further supports growth.

The Molecular Diagnostics segment is expected to witness the fastest CAGR of 16.5% from 2026 to 2033, driven by the increasing use of PCR, NGS, and other molecular techniques. Rising infectious disease outbreaks boost molecular testing demand. QC ensures accurate pathogen detection and minimizes false positives/negatives. Integration with automated workflows supports efficiency. Expansion of genetic testing for hereditary diseases accelerates growth. Advanced digital QC solutions support high-throughput molecular labs. Government funding for pandemic preparedness strengthens adoption. Hospital and research labs invest in robust molecular QC protocols. Growing awareness about personalized medicine fuels demand. AI-assisted molecular QC improves result accuracy. Increased molecular lab capacity in emerging markets supports expansion. Remote monitoring and centralized reporting enhance operational control.

• By Manufacturer Type

On the basis of manufacturer type, the market is segmented into Third-Party Control Manufacturers and Original Equipment Manufacturers (OEMs). The OEMs segment dominated the largest market revenue share of 51.3% in 2025, as hospitals and laboratories prefer integrated QC products designed specifically for their diagnostic instruments. OEMs ensure compatibility and validated performance. Strong after-sales support and warranty services boost adoption. Market leadership is supported by long-standing relationships with diagnostic device manufacturers. Continuous product innovation and alignment with regulatory standards strengthen positioning. Integration with new analyzers enhances accuracy. Established OEMs offer global distribution networks. Training and technical support increase end-user confidence. Strategic collaborations with research institutes accelerate adoption. OEMs benefit from brand recognition and trust. Partnerships with healthcare systems further reinforce market dominance.

The Third-Party Control Manufacturers segment is projected to witness the fastest CAGR of 14.8% from 2026 to 2033, driven by flexibility, cost-effectiveness, and multi-platform compatibility. Hospitals and labs increasingly adopt third-party QC for cross-instrument validation. Independent controls provide benchmarking for multiple analyzers. Growth is supported by expanding diagnostic laboratory networks. R&D innovations enhance product reliability and coverage. Compatibility with a wide range of assays fuels adoption. Vendors increasingly focus on user-friendly solutions for smaller labs. Regulatory approvals for independent QC products accelerate market expansion. Cost savings compared to OEM products drive preference. Emerging economies show increasing adoption due to affordability. Third-party QC solutions integrate with lab information systems. Partnerships with distributors and online platforms support reach.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Clinical Laboratories, Academic and Research Institutes, and Other End Users. The Hospitals segment dominated with a market revenue share of 58.7% in 2025, due to the presence of multi-specialty labs, advanced instrumentation, and high testing volumes. Hospitals require QC for accreditation and regulatory compliance. Emergency diagnostics and high patient inflow boost usage. Integration with laboratory information management systems enhances workflow efficiency. Urban hospitals demonstrate higher adoption rates. Government hospitals receive funding for QC standardization. Training and awareness programs among lab staff improve utilization. Partnerships with OEMs ensure supply consistency. Hospital chains adopt centralized QC protocols for multiple facilities. Technological innovations in QC improve test accuracy. Robust logistics ensure uninterrupted supply of QC products. Continuous product updates strengthen hospital reliance.

The Clinical Laboratories segment is expected to witness the fastest CAGR of 15.9% from 2026 to 2033, driven by independent labs expanding test portfolios and adopting automated QC solutions. Rising prevalence of outpatient testing boosts demand. Integration with LIS platforms enhances workflow efficiency. Small and medium labs benefit from flexible QC solutions. Digital dashboards and cloud-based monitoring enable remote oversight. Regulatory compliance requirements drive adoption. Growth in preventive health check-ups supports increased QC usage. Collaboration with third-party QC manufacturers enhances scalability. Emerging markets show high growth potential. AI-based QC analytics improve test accuracy and reduce errors. Expansion of lab networks and franchises fuels adoption. Homecare diagnostic kits integrating QC functionality also contribute to growth.

In Vitro Diagnostics (IVD) Quality Control Market Regional Analysis

- North America dominated the in vitro diagnostics (IVD) quality control market with the largest revenue share of 46.5% in 2025, characterized by advanced laboratory infrastructure, high adoption of automated diagnostic technologies, and a strong presence of key IVD companies. The U.S. experienced substantial growth in QC system installations, particularly in hospitals, clinical laboratories, and research centers, driven by innovations from both established and emerging players focusing on automation, accuracy, and high-throughput monitoring

- The widespread adoption in the region is further supported by robust healthcare spending, well-established regulatory frameworks, and a technologically adept workforce, enabling laboratories to implement sophisticated QC protocols and maintain compliance with international quality standards

- North American laboratories are increasingly leveraging high-capacity QC panels and centralized monitoring solutions to streamline operations, reduce human error, and ensure consistent test results across multiple locations, further strengthening market demand

U.S. In Vitro Diagnostics (IVD) Quality Control Market Insight

The U.S. in vitro diagnostics (IVD) quality control market captured the largest revenue share within North America in 2025, fueled by the growing need for accurate diagnostics and the expansion of hospital networks, research centers, and specialized clinical laboratories. Increasing prevalence of chronic and infectious diseases has accelerated the adoption of advanced QC systems to ensure reliable testing outcomes. Furthermore, collaborations between IVD manufacturers and healthcare providers are facilitating the implementation of standardized QC protocols and automated systems across diagnostic workflows.

Europe In Vitro Diagnostics (IVD) Quality Control Market Insight

The Europe in vitro diagnostics (IVD) quality control market is projected to expand at a substantial CAGR during the forecast period, driven by stringent regulatory requirements, growing healthcare investments, and the need for consistent laboratory quality standards. Countries such as Germany, France, and the U.K. are witnessing rapid adoption of automated QC systems in clinical and research laboratories. Enhanced focus on early disease diagnosis, particularly for cancer and cardiovascular disorders, is also propelling market growth.

U.K. In Vitro Diagnostics (IVD) Quality Control Market Insight

The U.K in vitro diagnostics (IVD) quality control market is expected to grow steadily, driven by national initiatives for improving laboratory efficiency and diagnostic accuracy. Government support for healthcare digitalization and laboratory modernization, combined with growing prevalence of chronic diseases, has increased demand for automated and standardized QC solutions. Clinical laboratories are increasingly investing in multiplexed QC panels and high-throughput systems to maintain compliance and improve patient outcomes.

Germany In Vitro Diagnostics (IVD) Quality Control Market Insight

The Germany in vitro diagnostics (IVD) quality control market is anticipated to grow at a considerable rate, fueled by the country’s strong healthcare infrastructure, advanced laboratory networks, and emphasis on technological innovation. German laboratories are increasingly adopting automated QC platforms that enable real-time monitoring of test performance, reduce operational errors, and ensure adherence to ISO and EU regulatory standards. The demand for reliable QC systems in both hospital and private laboratory settings continues to rise.

Asia-Pacific In Vitro Diagnostics (IVD) Quality Control Market Insight

The Asia-Pacific in vitro diagnostics (IVD) quality control market is expected to grow at the fastest CAGR of 12.3% during the forecast period, driven by rising healthcare expenditure, increasing prevalence of chronic and infectious diseases, and rapid expansion of hospital and diagnostic laboratory infrastructure in countries such as China, India, and Japan. Growing awareness about laboratory quality standards and rising adoption of automated QC systems for high-throughput testing are significant factors propelling market growth.

Japan In Vitro Diagnostics (IVD) Quality Control Market Insight

The Japan in vitro diagnostics (IVD) quality control market is gaining momentum due to the country’s advanced healthcare system, high-quality laboratory infrastructure, and strong focus on preventive healthcare. The demand for reliable, rapid, and standardized QC solutions is increasing, particularly in clinical laboratories handling high-volume diagnostic tests for cardiovascular, metabolic, and infectious diseases.

China In Vitro Diagnostics (IVD) Quality Control Market Insight

The China in vitro diagnostics (IVD) quality control market accounted for the largest revenue share in Asia-Pacific in 2025, driven by expanding healthcare infrastructure, rising prevalence of chronic and infectious diseases, and increasing investments in laboratory modernization. The adoption of automated quality control platforms is growing rapidly in hospitals, private laboratories, and research centers to improve diagnostic accuracy, standardize testing, and reduce turnaround times. Government initiatives supporting healthcare digitalization and local manufacturing of QC systems are further boosting market growth.

In Vitro Diagnostics (IVD) Quality Control Market Share

The In Vitro Diagnostics (IVD) Quality Control industry is primarily led by well-established companies, including:

• Bio-Rad Laboratories (U.S.)

• Siemens Healthineers (Germany)

• Abbott (U.S.)

• Beckman Coulter (U.S.)

• Thermo Fisher Scientific (U.S.)

• Randox Laboratories (U.K.)

• Cirion (Italy)

• Lonza Group (Switzerland)

• Ortho Clinical Diagnostics (U.S.)

• Spectrum Chemicals (U.S.)

• Instrumentation Laboratory (U.S.)

• Roche Diagnostics (Switzerland)

• Awareness Technology (U.K.)

• Streck, Inc. (U.S.)

• Horiba Medical (France)

• Siemens Healthcare Diagnostics (Germany)

• LifeAssays (Australia)

• LGC Group (U.K.)

• DiaSys Diagnostic Systems (Germany)

• Werfen (Spain)

Latest Developments in Global In Vitro Diagnostics (IVD) Quality Control Market

- In April 2021, LGC Group launched the ACCURUN SARS‑CoV‑2 Antigen Reference Material Kit, a quality control tool designed to support laboratories in validating the performance of COVID‑19 antigen testing during the global pandemic. This product helped standardize diagnostic accuracy at a time of urgent global demand

- In July 2023, LGC Group completed the acquisition of Kova International, Inc., a manufacturer of in‑vitro urinalysis and toxicology quality control products. This acquisition expanded LGC’s footprint and product offerings in the clinical laboratory QC segment, particularly in the U.S. market

- In October 2023, Technopath Clinical Diagnostics expanded the availability of its Multichem QC and IAMQC software solutions in Australia, enabling laboratories to implement unified quality control tracking and analytics across multiple analyzers and assay types

- In November 2024, Bio‑Techne Corporation obtained In Vitro Diagnostic Regulation (IVDR) certification for its R&D Systems Hematology Controls and Calibrators, confirming compliance with stringent EU diagnostic standards and enabling wider adoption of these QC products in European laboratories

- In September 2024, LGC Limited partnered with AccuGenomics, Inc. to innovate molecular quality control solutions for next‑generation sequencing (NGS), combining LGC’s QC expertise with AccuGenomics’ technologies to address precision medicine and oncology assay validation requirements

- In March 2025, Siemens Healthineers announced a strategic partnership with Randox Laboratories to co‑develop and distribute standardized QC materials and data‑management solutions for molecular diagnostic platforms, aiming to harmonize quality control across different diagnostic systems

- In June 2025, Randox Laboratories Ltd. launched a new RIQAS EQA (External Quality Assessment) programme for pre‑eclampsia testing, broadening the range of external QC services and expanding global participation in proficiency assessment schemes

- In June 2025, ZeptoMetrix Corporation introduced the NATtrol Influenza A H5N1 Quantitative Stock, a molecular diagnostic QC product verified for assay validation in laboratories monitoring avian influenza pathogens, supporting labs in ensuring assay accuracy for high‑priority infectious disease testing

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.