Global Industrial Radiography Equipment Market

Размер рынка в млрд долларов США

CAGR :

%

USD

2.03 Billion

USD

6.27 Billion

2025

2033

USD

2.03 Billion

USD

6.27 Billion

2025

2033

| 2026 –2033 | |

| USD 2.03 Billion | |

| USD 6.27 Billion | |

| % | |

|

Global Industrial Radiography Equipment Market Segmentation, By Type (Film-Based Radiography and Digital Radiography), Component (Hardware and Software), Radiation Type (X-Rays and Gamma Rays), End-User (Petrochemical and Gas, Power Generation, Manufacturing, Aerospace, Automotive and Transportation, and Others) - Industry Trends and Forecast to 2033

What is the Global Industrial Radiography Equipment Market Size and Growth Rate?

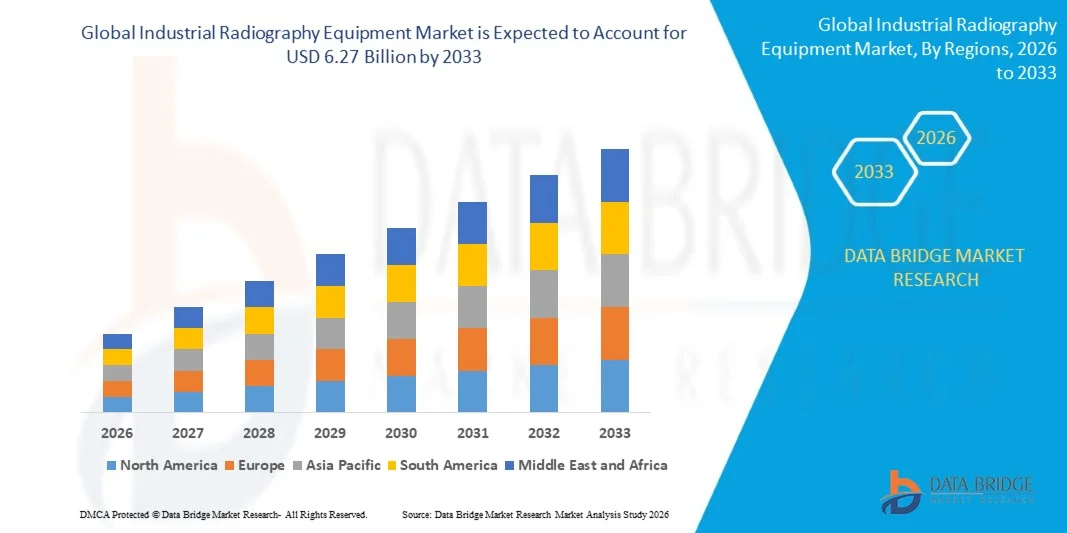

- The global industrial radiography equipment market size was valued at USD 2.03 billion in 2025 and is expected to reach USD 6.27 billion by 2033, at a CAGR of 15.10% during the forecast period

- The integrating capability of 2D and 3D in single system is a key element driving market expansion. The industrial radiography equipment market is also being driven by factors such as technical innovations and maintenance of industrial equipment

- Furthermore, the advent of new type of materials and surging usage of product in petrochemicals, buildings and chemical industries will enhance the growth rate of industrial radiography equipment market

What are the Major Takeaways of Industrial Radiography Equipment Market?

- The increase in the adoption of industrial radiography technique in aerospace and automotive industry and growing demand for portable radiography equipment will create beneficial opportunities for the growth of the market

- However, high deployment cost imposed on industrial radiography will hamper the market’s growth rate. Also, the dearth of highly skilled professionals will further pose a challenge to the growth of industrial radiography equipment market

- Asia-Pacific dominated the industrial radiography equipment market with a 39.8% revenue share in 2025, driven by strong growth in automotive manufacturing, heavy industrial production, oil & gas infrastructure, aerospace component manufacturing, and rapid expansion of non-destructive testing (NDT) activities across China, Japan, India, South Korea, and Southeast Asia

- North America is projected to register the fastest CAGR of 9.8% from 2026 to 2033, driven by rapid adoption of digital radiography, advanced CT inspection systems, and AI-enabled defect analysis tools across the U.S. and Canada

- The Digital Radiography segment dominated the market with a 64.8% share in 2025, as it remains the preferred technology for modern non-destructive testing applications across critical industries

Report Scope and Industrial Radiography Equipment Market Segmentation

|

Attributes |

Industrial Radiography Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Industrial Radiography Equipment Market?

“Increasing Shift Toward Digital, Portable, and AI-Integrated Industrial Radiography Equipment”

- The industrial radiography equipment market is witnessing strong adoption of digital radiography (DR), computed radiography (CR), and real-time radiography (RTR) systems designed for fast, non-destructive inspection across critical industries

- Manufacturers are introducing portable X-ray systems, flat-panel detectors, and AI-enabled imaging software that offer real-time defect detection, higher image resolution, and automated reporting workflows

- Growing demand for lightweight, field-deployable, and high-speed inspection equipment is driving usage across oil & gas pipelines, aerospace components, automotive weld inspection, and power generation facilities

- For instance, companies such as Teledyne, Nikon, FUJIFILM, Carl Zeiss, and Comet Group have upgraded their industrial X-ray and CT inspection systems with advanced digital imaging capabilities

- Increasing need for real-time flaw detection, weld inspection, corrosion analysis, and structural integrity testing is accelerating the shift toward portable and digital radiography systems

- As industrial assets become more complex and safety-critical, Industrial Radiography Equipment will remain vital for non-destructive testing (NDT), predictive maintenance, and quality assurance

What are the Key Drivers of Industrial Radiography Equipment Market?

- Rising demand for accurate, non-destructive testing solutions to support quality assurance across aerospace, automotive, oil & gas, and energy sectors is a major growth driver

- For instance, in 2025–2026, leading companies such as Teledyne Technologies, Nikon Corporation, and General Electric expanded their digital radiography and industrial CT portfolios for advanced inspection applications

- Growing adoption of EV batteries, lightweight aerospace structures, additive manufacturing, and aging pipeline infrastructure is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in digital detectors, AI-based image processing, robotics-assisted inspection, and cloud-based diagnostics have strengthened speed, portability, and efficiency

- Rising use of complex alloys, composite materials, and volumetric inspection systems is creating demand for high-precision radiographic equipment

- Supported by steady investments in industrial safety compliance, manufacturing automation, and infrastructure inspection, the market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Industrial Radiography Equipment Market?

- High costs associated with premium digital radiography systems, CT scanners, and portable X-ray inspection devices restrict adoption among small manufacturers and service providers

- For instance, during 2024–2025, fluctuations in detector panels, semiconductor components, and radiation shielding materials increased equipment manufacturing costs for several global vendors

- Complexity in handling radiation safety compliance, image interpretation, and advanced defect analysis increases the need for certified technicians and specialized training

- Limited awareness in emerging markets regarding digital radiography benefits, NDT protocols, and regulatory standards slows adoption

- Competition from ultrasonic testing, eddy current inspection, and alternative NDT technologies creates pricing pressure and reduces differentiation

- To address these issues, companies are focusing on cost-optimized portable systems, AI-enabled analytics, cloud-connected platforms, and workforce training to increase global adoption of industrial radiography equipment

How is the Industrial Radiography Equipment Market Segmented?

The market is segmented on the basis of type, component, radiation type, and end-user.

• By Type

On the basis of type, the industrial radiography equipment market is segmented into Film-Based Radiography and Digital Radiography. The Digital Radiography segment dominated the market with a 64.8% share in 2025, as it remains the preferred technology for modern non-destructive testing applications across critical industries. Digital radiography offers faster image capture, real-time defect detection, higher resolution imaging, and reduced inspection time compared to conventional film-based systems. Its ability to integrate with AI-based analysis tools, cloud platforms, and automated reporting software has further strengthened adoption across aerospace, manufacturing, oil & gas, and automotive sectors.

The Film-Based Radiography segment, while still relevant in specific legacy applications, is expected to witness slower growth. Meanwhile, Digital Radiography is projected to remain the fastest-growing segment from 2026 to 2033, driven by rising investments in portable X-ray systems, industrial CT, and smart inspection workflows.

• By Component

On the basis of component, the market is segmented into Hardware and Software. The Hardware segment dominated the market with a 71.2% share in 2025, driven by strong demand for X-ray generators, detectors, imaging panels, gamma ray sources, robotic arms, and portable inspection units. Hardware forms the core infrastructure of industrial radiography systems and accounts for significant capital expenditure across industrial testing environments. Increasing deployment of flat-panel detectors, digital imaging sensors, and mobile radiography units continues to support segment dominance.

The Software segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rising integration of AI-enabled defect recognition, automated reporting, 3D visualization, cloud-connected inspection systems, and predictive maintenance analytics. Growing need for faster image processing and data-driven quality assurance workflows is accelerating software adoption globally.

• By Radiation Type

On the basis of radiation type, the market is segmented into X-Rays and Gamma Rays. The X-Rays segment dominated the market with a 58.6% share in 2025, supported by its extensive use in high-resolution industrial inspection, weld testing, casting defect detection, and component integrity analysis. X-ray-based systems are widely preferred for precision inspection in aerospace, automotive, and electronics manufacturing due to superior image clarity and faster inspection speed. Their compatibility with digital radiography and computed tomography systems further strengthens adoption.

The Gamma Rays segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing use in field-based pipeline inspection, petrochemical plants, offshore platforms, and large infrastructure testing where portability and deep penetration capabilities are essential.

• By End-User

On the basis of end-user, the industrial radiography equipment market is segmented into Petrochemical and Gas, Power Generation, Manufacturing, Aerospace, Automotive and Transportation, and Others. The Manufacturing segment dominated the market with a 31.9% share in 2025, driven by extensive use in weld inspection, casting analysis, product quality control, and defect detection across heavy industrial production environments. Increasing demand for precision engineering, component validation, and automated inspection systems continues to support strong adoption.

The Aerospace segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by rising inspection requirements for lightweight materials, composite structures, turbine blades, and critical aircraft components. Stringent safety compliance and quality standards are further driving rapid growth in this segment.

Which Region Holds the Largest Share of the Industrial Radiography Equipment Market?

- Asia-Pacific dominated the industrial radiography equipment market with a 39.8% revenue share in 2025, driven by strong growth in automotive manufacturing, heavy industrial production, oil & gas infrastructure, aerospace component manufacturing, and rapid expansion of non-destructive testing (NDT) activities across China, Japan, India, South Korea, and Southeast Asia. High adoption of digital radiography systems, portable X-ray devices, and automated inspection tools continues to fuel demand across manufacturing plants, pipeline inspection facilities, shipbuilding yards, and power generation units

- Leading companies in Asia-Pacific are introducing advanced digital radiography, computed tomography (CT), and portable inspection systems, strengthening the region’s technological and manufacturing advantage. Continuous investment in infrastructure inspection, EV manufacturing, and industrial safety compliance drives long-term market expansion

- Strong industrial ecosystems, cost-efficient manufacturing capabilities, and sustained investment in precision inspection technologies further reinforce regional market leadership

China Industrial Radiography Equipment Market Insight

China is the largest contributor in Asia-Pacific, supported by strong industrial manufacturing capacity, large-scale infrastructure projects, and extensive oil & gas pipeline networks. Increasing production of automotive components, heavy machinery, and power equipment intensifies demand for industrial radiography systems for weld testing, casting inspection, and defect detection. Strong domestic manufacturing capabilities and government-backed industrial modernization initiatives further drive market growth.

Japan Industrial Radiography Equipment Market Insight

Japan contributes significantly to regional growth, driven by advanced automotive production, aerospace engineering, and high-precision industrial manufacturing. Industrial facilities increasingly utilize digital X-ray and CT inspection systems for component integrity testing, material inspection, and quality control. Strong focus on engineering excellence and high-end industrial automation strengthens market adoption across the country.

India Industrial Radiography Equipment Market Insight

India is emerging as a major growth hub, driven by expanding manufacturing infrastructure, oil refinery capacity, power generation projects, and government-backed industrial initiatives. Growing demand for weld inspection, pressure vessel testing, and infrastructure integrity analysis fuels adoption of industrial radiography equipment in testing and maintenance environments. Increasing investments in industrial automation and safety compliance further accelerate market penetration.

South Korea Industrial Radiography Equipment Market Insight

South Korea contributes significantly due to strong demand from shipbuilding, automotive, semiconductor equipment, and heavy engineering industries. Rapid development of EV components, battery systems, and advanced industrial machinery drives adoption of industrial radiography systems for precision inspection and structural testing. Technological innovation and strong manufacturing ecosystems support sustained market growth.

North America Industrial Radiography Equipment Market

North America is projected to register the fastest CAGR of 9.8% from 2026 to 2033, driven by rapid adoption of digital radiography, advanced CT inspection systems, and AI-enabled defect analysis tools across the U.S. and Canada. Growing investments in aerospace, defense, EV production, aging pipeline inspection, and power generation infrastructure are significantly increasing demand for advanced NDT solutions. Rising focus on predictive maintenance, structural integrity, and regulatory compliance continues to accelerate the need for portable and high-precision industrial radiography equipment across engineering and manufacturing applications.

U.S. Industrial Radiography Equipment Market Insight

The U.S. is the largest contributor to North America, supported by strong aerospace, oil & gas, automotive, and industrial manufacturing sectors. Increasing development of EV systems, aircraft components, defense equipment, and critical infrastructure inspection intensifies demand for industrial radiography equipment capable of high-resolution internal flaw detection and real-time digital imaging. Presence of major testing labs and strong industrial safety regulations further drives market growth.

Canada Industrial Radiography Equipment Market Insight

Canada contributes significantly to regional growth, driven by expanding oil sands, pipeline infrastructure, aerospace engineering, and heavy machinery manufacturing. Industrial facilities increasingly utilize radiography systems for corrosion monitoring, weld inspection, and equipment lifecycle management. Government-supported infrastructure modernization and strong industrial compliance standards strengthen market adoption across the country

Which are the Top Companies in Industrial Radiography Equipment Market?

The industrial radiography equipment industry is primarily led by well-established companies, including:

- Teledyne Technologies Incorporated (U.S.)

- FUJIFILM Holdings Corporation (Japan)

- General Electric (U.S.)

- Comet Group (Switzerland)

- Nikon Corporation (Japan)

- Shimadzu Corporation (Japan)

- METTLER TOLEDO (U.S.)

- 3DX-RAY (U.K.)

- Anritsu (Japan)

- Carl Zeiss AG (Germany)

- VJ Group, Inc. (U.S.)

- Nordson Corporation (U.S.)

- Measurement Control (U.S.)

- Smiths Group plc. (U.K.)

- C.E.I.A. S.p.A. (Italy)

- Ixar (Spain)

- X-Ray Associates, LLC (U.S.)

- North Star Imaging Inc. (U.S.)

- PerkinElmer Inc. (U.S.)

- Blue Star Limited (India)

- Illinois Tool Works Inc. (U.S.)

What are the Recent Developments in Global Industrial Radiography Equipment Market?

- In July 2025, Carestream’s Non-Destructive Testing division introduced the INDUSTREX HPX-ARC 1025 PH, an advanced digital radiography detector specifically designed for inspecting curved surfaces and operating efficiently in confined spaces

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.