Global Integrated Passive Device Market

Размер рынка в млрд долларов США

CAGR :

%

USD

2.01 Billion

USD

4.21 Billion

2025

2033

USD

2.01 Billion

USD

4.21 Billion

2025

2033

| 2026 –2033 | |

| USD 2.01 Billion | |

| USD 4.21 Billion | |

| % | |

|

Global Integrated Passive Device Market Segmentation, By Material (Silicon, Glass, and Others), Passive Devices (Baluns, Filter, Couplers, Diplexers, Customized IPDs, and Others), Wireless Technology (WLAN, Bluetooth, Cellular, GPS, and Others), Application (ESD/EMI, RF IPD, Digital and Mixed Signals, and Others), End Use Industry (Consumer Electronics, Automotive, Communication, Aerospace and Defense, and Healthcare and Lifesciences) - Industry Trends and Forecast to 2033

Integrated Passive Device Market Size

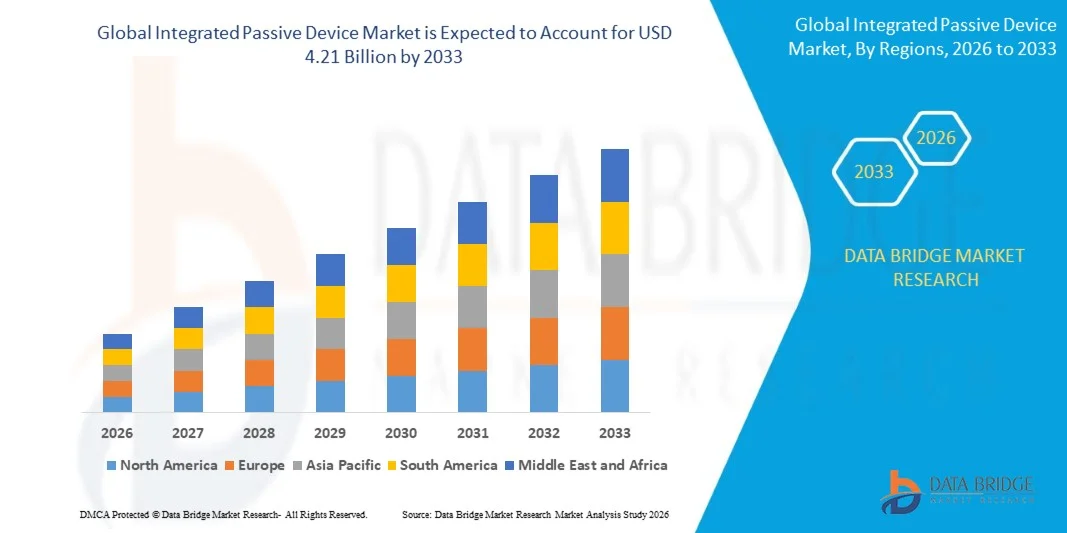

- The global integrated passive device market size was valued at USD 2.01 billion in 2025 and is expected to reach USD 4.21 billion by 2033, at a CAGR of 9.65% during the forecast period

- The market growth is largely fueled by the increasing adoption of connected devices, IoT systems, and advanced communication technologies, which drive the demand for miniaturized and high-performance integrated passive devices across consumer electronics, automotive, and telecommunications sectors

- Furthermore, rising industry requirements for energy-efficient, compact, and multifunctional components in RF modules, smartphones, wearable devices, and automotive electronics are encouraging manufacturers to deploy integrated passive devices, thereby accelerating market growth

Integrated Passive Device Market Analysis

- Integrated passive devices are compact components that combine passive elements such as resistors, capacitors, inductors, baluns, filters, and couplers into a single package, enabling smaller form factors, improved performance, and simplified PCB designs for electronic devices

- The escalating demand for integrated passive devices is primarily driven by the proliferation of smartphones, IoT applications, 5G infrastructure, automotive electronics, and other high-frequency communication systems, which require reliable, high-density, and cost-effective passive solutions

- Europe dominated the integrated passive device market with a share of 40% in 2025, due to a strong presence of advanced electronics manufacturers, stringent quality standards, and high adoption of connected devices across industries

- Asia-Pacific is expected to be the fastest growing region in the integrated passive device market during the forecast period due to rapid urbanization, increasing electronics manufacturing, and rising demand for smartphones, IoT devices, and automotive applications in countries such as China, Japan, and South Korea

- Silicon segment dominated the market with a market share of 52.9% in 2025, due to its excellent electrical properties, scalability, and cost-effectiveness in mass production. Silicon-based IPDs are widely adopted in high-frequency and high-performance applications due to their reliability and integration ease with existing semiconductor processes. Manufacturers also favor silicon for its compatibility with miniaturized and multifunctional devices, enabling compact and efficient solutions across consumer electronics and automotive applications

Report Scope and Integrated Passive Device Market Segmentation

|

Attributes |

Integrated Passive Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Integrated Passive Device Market Trends

“Rising Adoption of Miniaturized and High-Frequency Electronic Devices”

- A key trend in the integrated passive device (IPD) market is the growing adoption of miniaturized and high-frequency components that support advanced electronic systems across multiple industries. The demand for smaller, multifunctional, and high-performance devices is driving manufacturers to innovate in design, packaging, and integration, enabling higher efficiency and enhanced signal integrity in constrained spaces

- For instance, Murata Manufacturing and TDK Corporation provide high-frequency multilayer capacitors and inductors that are widely implemented in smartphones, tablets, and wireless communication modules. These components support reliable performance at high frequencies while reducing overall device footprint

- The expansion of 5G networks is accelerating the need for compact, high-frequency IPDs that can handle increased bandwidth and faster signal processing. Such devices are critical for enabling stable connectivity and low-latency communication in telecommunication infrastructures

- Automotive electronics are increasingly integrating IPDs for electric vehicles (EVs), advanced driver-assistance systems (ADAS), and infotainment units, where space constraints and performance demands are significant. This is encouraging the adoption of high-density, miniaturized passive devices that enhance system reliability and energy efficiency

- Consumer electronics applications, including wearables and smart home devices, are driving the design of IPDs capable of supporting multifunctionality in limited spaces. Manufacturers are focusing on developing components that maintain high performance while reducing power consumption and size

- The industrial sector is adopting IPDs for automation, robotics, and IoT devices, where high-frequency and compact components enable precise control and data processing. The market is witnessing strong growth in these segments as reliable, miniaturized IPDs become essential for modern smart systems

Integrated Passive Device Market Dynamics

Driver

“Growing Demand for Compact and Energy-Efficient Electronic Components”

- The rising need for compact and energy-efficient electronic components is a significant driver for the integrated passive device market, as end-users seek higher performance in smaller form factors. These requirements are promoting innovation in multilayer, high-density passive components that reduce space, improve thermal management, and enhance power efficiency

- For instance, Skyworks Solutions offers multilayer IPDs that support low-power wireless communication in mobile devices and IoT modules. These solutions help reduce energy consumption while maintaining high signal integrity, meeting the performance expectations of modern electronics

- The increasing deployment of wearable devices, smartphones, and tablets requires IPDs that provide superior integration without compromising reliability or efficiency. This trend is driving investment in research and development to create compact solutions that fit evolving application needs

- Demand for energy-efficient devices in automotive electronics is encouraging the use of IPDs that contribute to overall system power optimization. Such components are integral in managing energy consumption in EV powertrains, battery management systems, and infotainment electronics

- Expansion of high-speed communication networks and 5G infrastructure is boosting the adoption of IPDs that ensure minimal signal loss and stable performance in dense electronic assemblies. These devices support faster, more efficient data transmission while maintaining low power usage across critical applications

Restraint/Challenge

“Complex Manufacturing Processes and Material Limitations”

- The integrated passive device market faces challenges due to the complexity of manufacturing high-density, multilayer components that meet stringent performance standards. Advanced materials, precise fabrication techniques, and controlled assembly processes are required, which increase production complexity and cost

- For instance, Murata Manufacturing employs specialized ceramic processing and thin-film deposition techniques to produce high-performance multilayer IPDs. These intricate processes demand advanced equipment, skilled labor, and strict quality control, which elevate manufacturing costs and operational challenges

- Maintaining reliability and performance in high-frequency applications requires tight tolerances and uniform material properties across all layers of the device. This adds difficulty in scaling production while keeping defect rates low

- Supply constraints in raw materials such as high-purity ceramics and conductive metals can affect production timelines and cost stability. Manufacturers must balance material selection with economic feasibility while ensuring device performance

- The market continues to face challenges in integrating complex IPDs into increasingly compact electronic systems without compromising functionality. These factors collectively limit production flexibility and place pressure on manufacturers to optimize processes and reduce costs while meeting growing demand

Integrated Passive Device Market Scope

The market is segmented on the basis of material, passive devices, wireless technology, application, and end-use industry.

• By Material

On the basis of material, the Integrated Passive Device market is segmented into silicon, glass, and others. The silicon segment dominated the largest market revenue share of 52.9% in 2025, driven by its excellent electrical properties, scalability, and cost-effectiveness in mass production. Silicon-based IPDs are widely adopted in high-frequency and high-performance applications due to their reliability and integration ease with existing semiconductor processes. Manufacturers also favor silicon for its compatibility with miniaturized and multifunctional devices, enabling compact and efficient solutions across consumer electronics and automotive applications. The material’s robustness and thermal stability further contribute to its strong market presence and consistent demand.

The glass segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption in high-frequency RF and microwave applications. Glass IPDs offer superior insulation, reduced signal loss, and enhanced performance in harsh environments, making them attractive for aerospace, defense, and advanced communication systems. The increasing need for precision and high-performance passive components in next-generation wireless devices drives the adoption of glass-based IPDs.

• By Passive Devices

On the basis of passive devices, the market is segmented into baluns, filters, couplers, diplexers, customized IPDs, and others. The filters segment dominated the largest market revenue share in 2025, supported by its critical role in signal conditioning, noise reduction, and interference management across RF and wireless systems. Filters are extensively used in smartphones, IoT devices, and communication modules, providing reliable performance and maintaining signal integrity. The broad range of filter designs and tunable options further strengthens their adoption in both consumer electronics and automotive electronics.

The customized IPDs segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the growing demand for tailor-made solutions optimized for specific applications. For instance, Murata Manufacturing develops customized IPDs for high-frequency 5G and automotive radar systems, offering integration and miniaturization advantages. Customized IPDs provide flexibility in design, allowing end-users to achieve precise electrical characteristics and meet complex application requirements, boosting their rapid adoption.

• By Wireless Technology

On the basis of wireless technology, the IPD market is segmented into WLAN, Bluetooth, cellular, GPS, and others. The cellular segment dominated the largest market revenue share in 2025, owing to the proliferation of smartphones, mobile communication devices, and 4G/5G infrastructure. Cellular-enabled IPDs ensure robust signal filtering, matching, and integration in complex RF front-end modules, making them indispensable for modern mobile networks. Their adoption in IoT, automotive telematics, and communication infrastructure further contributes to market dominance.

The Bluetooth segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing adoption of short-range wireless connectivity in wearable devices, smart home electronics, and medical devices. Bluetooth-enabled IPDs support low-power operation and compact design, making them ideal for portable electronics and localized wireless communication. Their integration facilitates simplified design, cost savings, and reliable performance in consumer and industrial applications.

• By Application

On the basis of application, the IPD market is segmented into ESD/EMI, RF IPD, digital and mixed signals, and others. The RF IPD segment dominated the largest market revenue share in 2025, driven by its essential role in high-frequency signal transmission, impedance matching, and noise suppression in wireless communication systems. RF IPDs are extensively used in smartphones, base stations, and IoT devices to ensure performance stability across complex RF front-ends. Their integration reduces component count, improves efficiency, and allows miniaturized designs, meeting the growing demand for compact and high-performance devices.

The digital and mixed-signal segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising adoption of high-speed digital circuits and mixed-signal processing in advanced electronics. For instance, Analog Devices offers mixed-signal IPDs for signal conditioning and filtering in precision instrumentation and communication systems. Their ability to handle both analog and digital signals in compact form factors drives demand across automotive, consumer electronics, and industrial applications.

• By End Use Industry

On the basis of end-use industry, the IPD market is segmented into consumer electronics, automotive, communication, aerospace and defense, and healthcare and lifesciences. The consumer electronics segment dominated the largest market revenue share in 2025, driven by the widespread use of smartphones, tablets, laptops, and wearables requiring compact, high-performance passive devices. IPDs in consumer electronics enhance device efficiency, reduce size, and support multi-band communication and high-frequency operation. The segment benefits from constant innovation, miniaturization trends, and rising adoption of smart and connected devices.

The automotive segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing integration of advanced driver-assistance systems (ADAS), infotainment systems, and EV electronics. For instance, TDK supplies IPDs for automotive radar and communication modules, supporting high reliability under harsh conditions. Growing demand for connected and autonomous vehicles drives the adoption of automotive-grade IPDs that ensure compactness, performance, and compliance with strict safety and operational standards.

Integrated Passive Device Market Regional Analysis

- Europe dominated the integrated passive device market with the largest revenue share of 40% in 2025, driven by a strong presence of advanced electronics manufacturers, stringent quality standards, and high adoption of connected devices across industries

- Manufacturers in the region benefit from established semiconductor and electronics ecosystems, supporting the production and integration of high-performance IPDs in applications such as consumer electronics, automotive, and communication systems

- Widespread adoption is further supported by technological innovation, high R&D investments, and government incentives promoting advanced electronics and smart technologies, establishing Europe as a key hub for IPD deployment

Germany Integrated Passive Device Market Insight

The Germany Integrated Passive Device market captured the largest revenue share in 2025 within Europe, fueled by the country’s strong automotive and industrial electronics sectors. Germany’s focus on high-quality, reliable electronic components encourages the adoption of Integrated Passive Devices in RF modules, automotive radar, and high-frequency devices. Increasing integration of Integrated Passive Devices in consumer electronics and communication infrastructure, combined with advanced manufacturing capabilities, strengthens market growth. Furthermore, demand for miniaturized and multifunctional components aligns with the country’s emphasis on innovation and precision engineering.

France Integrated Passive Device Market Insight

The France Integrated Passive Device market is projected to grow at a significant CAGR during the forecast period, driven by the country’s growing adoption of connected devices and smart systems. French electronics manufacturers are increasingly integrating Integrated Passive Devices in RF modules, sensors, and IoT applications to enhance device efficiency and performance. The focus on energy-efficient and compact electronic solutions, along with government support for smart technology adoption, supports market expansion.

Asia-Pacific Integrated Passive Device Market Insight

The Asia-Pacific Integrated Passive Device market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, increasing electronics manufacturing, and rising demand for smartphones, IoT devices, and automotive applications in countries such as China, Japan, and South Korea. The region’s status as a manufacturing hub ensures cost-effective production of Integrated Passive Devices, enabling wider adoption across consumer electronics, communication devices, and automotive modules. For instance, China’s growing electronics ecosystem, supported by domestic manufacturers and government initiatives promoting smart cities and advanced electronics, is driving high-volume adoption of Integrated Passive Devices.

China Integrated Passive Device Market Insight

The China Integrated Passive Device market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to increasing electronics production, urbanization, and high technology adoption. The availability of affordable Integrated Passive Devices for consumer electronics and communication devices, combined with strong local manufacturing capabilities, is boosting market penetration. Integration of Integrated Passive Devices in automotive electronics and smart home devices further supports market expansion.

Japan Integrated Passive Device Market Insight

The Japan Integrated Passive Device market is gaining traction due to the country’s advanced electronics industry, high-tech culture, and demand for miniaturized and high-performance components. Japanese manufacturers are integrating Integrated Passive Devices in RF systems, automotive modules, and wearable electronics to improve performance and reduce device size. The focus on reliability, precision, and IoT-enabled devices is expected to drive sustained growth in both consumer and industrial electronics applications.

North America Integrated Passive Device Market Insight

The North America Integrated Passive Device market is anticipated to grow steadily, driven by adoption in high-performance communication devices, automotive electronics, and consumer gadgets. The United States, as a leading market within North America, is witnessing strong demand for Integrated Passive Devices in smartphones, 5G infrastructure, and connected automotive systems. High R&D investment, robust semiconductor infrastructure, and increasing focus on next-generation electronics and IoT integration are key factors supporting market growth.

U.S. Integrated Passive Device Market Insight

The U.S. Integrated Passive Device market captured the largest revenue share of 78% in North America in 2025, propelled by widespread adoption of advanced consumer electronics, 5G devices, and automotive modules. Growing preference for miniaturized, multifunctional components and integration of Integrated Passive Devices in RF front-end modules is driving demand. The country’s strong electronics manufacturing ecosystem, coupled with high consumer awareness and technological adoption, further reinforces market expansion.

Integrated Passive Device Market Share

The integrated passive device industry is primarily led by well-established companies, including:

- JCET Group Co., Ltd. (China)

- Semiconductor Components Industries, LLC (U.S.)

- Infineon Technologies AG (Germany)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics (Switzerland)

- Murata Manufacturing Co., Ltd. (Japan)

- Johanson Technology (U.S.)

- OnChip Devices, Inc. (U.S.)

- Global Communication Semiconductors, LLC (U.S.)

- 3DiS Technologies (U.S.)

- AFSC (U.S.)

- Qorvo, Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- Broadcom (U.S.)

- Taiwan Semiconductor Manufacturing Company Limited (Taiwan)

- MACOM (U.S.)

- CTS Corporation (U.S.)

Latest Developments in Global Integrated Passive Device Market

- In July 2025, Samsung Electro-Mechanics expanded its production capacity for multilayer ceramic capacitors, reflecting a strategic move to address the growing global demand for compact electronic devices. This expansion strengthens Samsung’s leadership in the integrated passive devices market by enhancing its ability to meet increasing customer requirements and ensuring supply chain reliability. The move highlights a broader industry trend of scaling production capabilities to support high-volume demand across consumer electronics, automotive, and telecommunications applications, positioning Samsung to capitalize on the rising adoption of miniaturized and multifunctional electronic components

- In September 2024, AVX Corporation introduced a new line of integrated passive devices tailored for high-frequency applications. This launch demonstrates AVX’s proactive approach in the rapidly evolving telecommunications sector, particularly with the growth of 5G networks. By focusing on high-frequency performance, the company enhances its competitive position and addresses increasing market requirements for advanced RF components. This development signals a strategic emphasis on innovation and market responsiveness, enabling AVX to capture emerging opportunities in high-performance wireless communications and IoT applications

- In August 2024, Yageo Corporation completed the acquisition of a leading passive component manufacturer, a move that strengthens its market presence and broadens its product portfolio. The acquisition enables Yageo to meet growing customer demand for integrated solutions while enhancing its manufacturing capabilities. Such strategic consolidation reflects a shift toward a more competitive and scale-driven market, where companies with extensive product breadth and robust production capacity are better positioned to capture market share in integrated passive devices across consumer electronics, automotive, and communication sectors

- In June 2024, Johanson Technology unveiled its new 900 MHz directional RF SMD coupler, P/N 0898CP14C0035001T, designed for diverse wireless applications including IoT, cellular, LoRa systems, and ISM. The device’s compact EIA 0603 form factor and RoHS compliance facilitate easy PCB integration, appealing to manufacturers seeking miniaturized and environmentally compliant components. This launch enhances Johanson Technology’s position in the RF and wireless segment of the integrated passive devices market, supporting the growing adoption of connected devices and the need for high-performance passive components in emerging wireless applications

- In February 2023, STMicroelectronics launched nine RF-integrated passive devices, featuring antenna baluns, harmonic filters, and impedance-matching circuits optimized for STM32WL wireless microcontrollers. These IPDs enable more efficient wireless module design and integration, strengthening STMicroelectronics’ market offering for IoT and low-power wide-area network applications. By delivering enhanced RF performance and simplified integration, this development positions the company to address increasing demand for compact, energy-efficient, and high-performance wireless solutions in the global integrated passive devices market

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.