Global Ip Multimedia Subsystem Ims Market

Размер рынка в млрд долларов США

CAGR :

%

USD

3.84 Billion

USD

11.82 Billion

2025

2033

USD

3.84 Billion

USD

11.82 Billion

2025

2033

| 2026 –2033 | |

| USD 3.84 Billion | |

| USD 11.82 Billion | |

| % | |

|

Global Ip Multimedia Subsystem (Ims) Market Segmentation, By Component (Product and Services), Mobile Operator (Mobile operators and Fixed operators) - Industry Trends and Forecast to 2033

Ip Multimedia Subsystem (Ims) Market Size

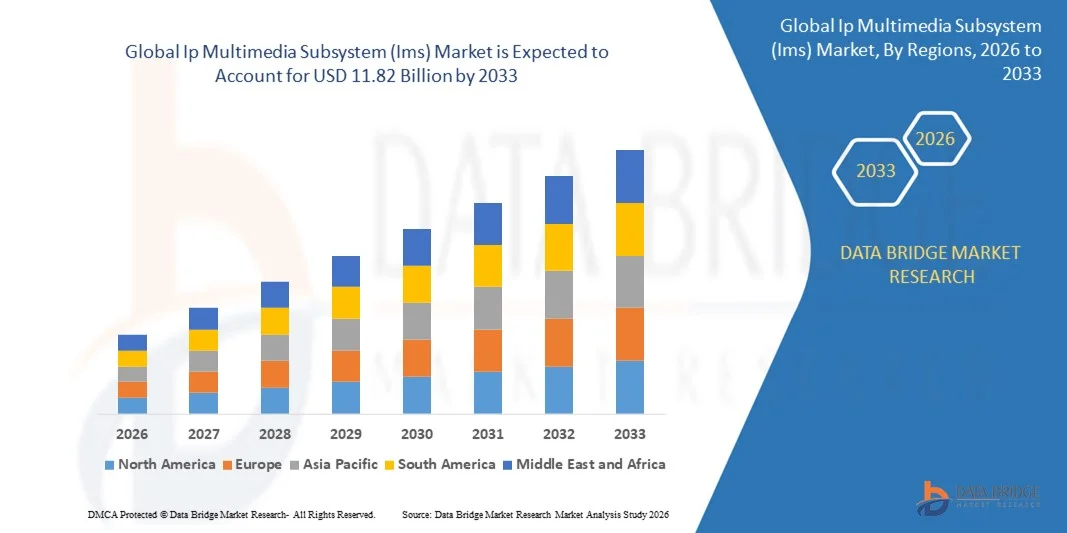

- The global Ip Multimedia Subsystem (Ims) market size was valued at USD 3.84 billion in 2025 and is expected to reach USD 11.82 billion by 2033, at a CAGR of 15.10% during the forecast period

- The market growth is largely fueled by the rapid expansion of LTE and 5G networks and the ongoing transition from legacy circuit-switched systems to all-IP communication infrastructures, leading to increased deployment of advanced multimedia communication services across telecom networks

- Furthermore, rising demand for high-quality voice, video, and unified communication services across mobile and fixed networks is positioning IMS as a critical core architecture for operators. These converging factors are accelerating investments in cloud-native and virtualized IMS platforms, thereby significantly boosting the industry's growth

Ip Multimedia Subsystem (Ims) Market Analysis

- Ip Multimedia Subsystem (IMS), enabling IP-based voice, video, and multimedia services over unified core networks, has become a foundational element of modern telecom architectures due to its ability to ensure service interoperability, scalability, and seamless session management across LTE and 5G environments

- The escalating demand for IMS solutions is primarily driven by increasing 5G commercialization, rising consumption of real-time multimedia services, and the growing need among telecom operators to modernize core networks while improving operational efficiency and service delivery quality

- North America dominated the Ip Multimedia Subsystem (Ims) market with a share of 41.76% in 2025, due to early adoption of LTE and 5G networks and strong investments in IP-based communication infrastructure

- Asia-Pacific is expected to be the fastest growing region in the Ip Multimedia Subsystem (Ims) market during the forecast period due to rapid expansion of mobile subscriber bases and accelerated 5G rollouts in emerging economies

- Product segment dominated the market with a market share of 72.38% in 2025, due to rising deployment of core IMS solutions such as Call Session Control Functions, Home Subscriber Servers, and Media Resource Functions across telecom networks. Telecom operators are investing heavily in IMS core infrastructure to enable VoLTE, VoWiFi, and Rich Communication Services while ensuring network interoperability and scalability

Report Scope and Ip Multimedia Subsystem (Ims) Market Segmentation

|

Attributes |

Ip Multimedia Subsystem (Ims) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Ip Multimedia Subsystem (Ims) Market Trends

Adoption of Cloud-Native and Virtualized IMS Architectures

- A significant trend in the Ip Multimedia Subsystem (IMS) market is the growing adoption of cloud-native and virtualized architectures, driven by telecom operators shifting from hardware-centric core networks to software-defined and containerized environments. This transition is enhancing network scalability, operational flexibility, and faster service deployment across LTE and 5G infrastructures

- For instance, Telefonaktiebolaget LM Ericsson has deployed cloud-native IMS solutions that support VoLTE and VoNR on 5G standalone networks, enabling operators to modernize core systems while reducing infrastructure dependency. Such deployments strengthen service agility and allow telecom providers to introduce advanced multimedia offerings with improved efficiency

- Telecom operators are increasingly integrating IMS with network function virtualization and container platforms to support automated lifecycle management and dynamic resource allocation. This is enabling faster rollout of communication services while improving network resilience and uptime

- The expansion of 5G standalone networks is accelerating the need for IMS platforms capable of supporting Voice over New Radio and enhanced multimedia applications. Operators are prioritizing virtualized IMS cores to ensure seamless service continuity across heterogeneous access networks

- Enterprises adopting private 5G networks are also driving demand for flexible and software-driven IMS deployments that can support mission-critical communication services. This shift is expanding IMS adoption beyond traditional public telecom networks into enterprise environments

- The market is witnessing sustained momentum toward fully cloud-native IMS ecosystems that align with digital transformation strategies in telecommunications. This rising transition to virtualization is reinforcing IMS as a central component of next-generation IP communication frameworks

Ip Multimedia Subsystem (Ims) Market Dynamics

Driver

Rapid Expansion of 5G Networks and VoNR Deployment

- The rapid expansion of 5G networks worldwide is a primary driver for the Ip Multimedia Subsystem (IMS) market, as IMS serves as the core platform enabling IP-based voice and multimedia services across advanced mobile infrastructures. Growing commercialization of 5G standalone networks is accelerating demand for IMS solutions capable of supporting Voice over New Radio and rich communication services

- For instance, Nokia has supported multiple operators globally in deploying IMS cores optimized for 5G standalone and VoNR services, enabling seamless migration from VoLTE to next-generation voice capabilities. These deployments enhance network performance while ensuring service continuity during technological transitions

- The increasing consumption of high-definition voice and video communication is encouraging telecom providers to upgrade legacy switching systems with IMS-based architectures. This modernization ensures interoperability across devices and access technologies

- Mobile network operators are investing in IMS to deliver integrated communication services across smartphones, IoT devices, and enterprise platforms. The demand for consistent service quality across varied network environments is strengthening IMS integration

- The continuous rollout of 5G infrastructure and VoNR capabilities is reinforcing IMS as an essential enabler of advanced IP communication services. This sustained expansion of next-generation mobile networks remains a fundamental growth driver for the market

Restraint/Challenge

Integration Complexity with Legacy Telecom Infrastructure

- The Ip Multimedia Subsystem (IMS) market faces challenges related to the integration of modern IP-based platforms with existing legacy circuit-switched and hybrid telecom infrastructures. Many operators continue to operate traditional core systems, creating technical complexities during migration to fully virtualized IMS environments

- For instance, Huawei Technologies Co., Ltd. has undertaken large-scale network transformation projects requiring phased integration of IMS with legacy mobile switching centers, illustrating the operational intricacies involved in modernization. Such projects demand extensive planning, interoperability testing, and resource allocation

- Interfacing IMS with multi-vendor legacy equipment often results in compatibility issues that can impact service stability and deployment timelines. Operators must ensure seamless coexistence of new and old systems during transition phases

- The migration process frequently requires significant capital expenditure and skilled technical expertise, increasing financial and operational burdens for telecom providers. These complexities may delay full-scale IMS implementation in certain markets

- The continued presence of legacy telecom frameworks in various regions is slowing the pace of complete IMS adoption. These integration challenges collectively act as a restraint on rapid market expansion despite strong technological momentum

Ip Multimedia Subsystem (Ims) Market Scope

The market is segmented on the basis of component and mobile operator.

- By Component

On the basis of component, the Ip Multimedia Subsystem (IMS) market is segmented into product and services. The product segment dominated the market with the largest market revenue share of 72.38% in 2025, driven by rising deployment of core IMS solutions such as Call Session Control Functions, Home Subscriber Servers, and Media Resource Functions across telecom networks. Telecom operators are investing heavily in IMS core infrastructure to enable VoLTE, VoWiFi, and Rich Communication Services while ensuring network interoperability and scalability. The transition toward 5G architecture has further strengthened demand for IMS products as they serve as the backbone for delivering IP-based multimedia services with improved reliability and performance.

The services segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for integration, consulting, maintenance, and managed services. As operators migrate from legacy circuit-switched networks to all-IP environments, they require specialized expertise to ensure seamless deployment and optimization of IMS platforms. The growing complexity of multi-vendor environments and continuous software upgrades is driving long-term service contracts, contributing to rapid expansion of this segment.

- By Mobile Operator

On the basis of mobile operator, the Ip Multimedia Subsystem (IMS) market is segmented into mobile operators and fixed operators. The mobile operators segment dominated the market with the largest market revenue share in 2025, driven by the widespread rollout of LTE and 5G networks globally. Mobile operators rely on IMS to deliver advanced communication services such as HD voice, video calling, and unified messaging while ensuring seamless mobility and session continuity. The increasing smartphone penetration and demand for data-intensive multimedia services continue to reinforce IMS adoption among mobile carriers.

The fixed operators segment is projected to witness the fastest growth rate from 2026 to 2033, supported by the modernization of fixed broadband infrastructure and the integration of fiber-to-the-home networks with IP-based voice services. Fixed-line providers are adopting IMS to replace traditional PSTN systems and to offer bundled communication services across voice, video, and data platforms. The shift toward converged networks and unified communication solutions is accelerating IMS deployment among fixed operators worldwide.

Ip Multimedia Subsystem (Ims) Market Regional Analysis

- North America dominated the Ip Multimedia Subsystem (Ims) market with the largest revenue share of 41.76% in 2025, driven by early adoption of LTE and 5G networks and strong investments in IP-based communication infrastructure

- Telecom operators in the region prioritize advanced multimedia services such as VoLTE, VoWiFi, and unified communications to enhance customer experience and network efficiency

- The presence of leading telecom equipment providers and continuous upgrades from legacy systems to all-IP networks are strengthening IMS deployment across mobile and fixed networks

U.S. Ip Multimedia Subsystem (IMS) Market Insight

The U.S. Ip Multimedia Subsystem (IMS) market captured the largest revenue share within North America in 2025, fueled by aggressive 5G rollouts and increasing demand for high-speed multimedia services. Major telecom carriers are investing in IMS core modernization to support seamless voice and video communication over IP networks. The strong ecosystem of network infrastructure providers and rapid migration from circuit-switched networks to packet-based systems continue to accelerate market growth.

Europe Ip Multimedia Subsystem (IMS) Market Insight

The Europe Ip Multimedia Subsystem (IMS) market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the region’s focus on network modernization and cross-border communication interoperability. Telecom operators are enhancing IMS frameworks to comply with regulatory standards and to deliver high-definition voice and multimedia services. Increasing 5G penetration and the shift toward cloud-based core networks are further contributing to market expansion across European countries.

U.K. Ip Multimedia Subsystem (IMS) Market Insight

The U.K. Ip Multimedia Subsystem (IMS) market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by nationwide 5G deployment strategies and investments in next-generation broadband infrastructure. Telecom providers are leveraging IMS to ensure reliable IP-based voice services and improved network scalability. The increasing demand for unified communication solutions across enterprises is also supporting adoption.

Germany Ip Multimedia Subsystem (IMS) Market Insight

The Germany Ip Multimedia Subsystem (IMS) market is expected to expand at a considerable CAGR during the forecast period, fueled by strong industrial digitalization and advanced telecom infrastructure. German operators are modernizing their core networks to support seamless multimedia services and enterprise communication platforms. The country’s emphasis on high-quality connectivity and secure communication networks is promoting steady IMS integration.

Asia-Pacific Ip Multimedia Subsystem (IMS) Market Insight

The Asia-Pacific Ip Multimedia Subsystem (IMS) market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid expansion of mobile subscriber bases and accelerated 5G rollouts in emerging economies. Governments across the region are promoting digital transformation and broadband connectivity, increasing demand for IP-based communication services. Rising investments in telecom infrastructure and large-scale network upgrades are strengthening regional market growth.

Japan Ip Multimedia Subsystem (IMS) Market Insight

The Japan Ip Multimedia Subsystem (IMS) market is gaining momentum due to advanced telecom technologies and early commercialization of 5G services. Japanese operators are focusing on delivering high-quality voice and multimedia services through IMS-enabled architectures. Continuous innovation in network virtualization and cloud-native core deployment is further supporting market expansion.

China Ip Multimedia Subsystem (IMS) Market Insight

The China Ip Multimedia Subsystem (IMS) market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to extensive 5G infrastructure development and a vast mobile subscriber base. Telecom providers are deploying IMS solutions at scale to enable HD voice, video calling, and integrated communication services. Strong government support for digital infrastructure and the presence of major telecom equipment manufacturers are key factors propelling the market in China.

Ip Multimedia Subsystem (Ims) Market Share

The Ip Multimedia Subsystem (Ims) industry is primarily led by well-established companies, including:

- Telefonaktiebolaget LM Ericsson (Sweden)

- Huawei Technologies Co., Ltd. (China)

- NEC Technologies India Private Limited (India)

- Nokia (Finland)

- ZTE Corporation (China)

- Athonet srl (Italy)

- Cirpack SAS (France)

- Cisco Systems, Inc. (U.S.)

- CommVerge Solutions (Singapore)

- Dialogic Corporation (U.S.)

- Interop Technologies (U.S.)

- Italtel S.p.A. (Italy)

- Metaswitch Networks (U.K.)

- Mavenir (U.S.)

- Oracle (U.S.)

- Radisys Corporation (U.S.)

- Ribbon Communications Operating Company, Inc. (U.S.)

- Samsung (South Korea)

- WIT Software (Portugal)

- IBM (U.S.)

Latest Developments in Global Ip Multimedia Subsystem (Ims) Market

- In February 2025, Mavenir and O2 Telefónica Germany signed a five-year cloud-native IMS extension agreement that converges VoLTE and VoNR on a single core network, strengthening the transition toward fully virtualized and 5G-ready architectures. This development enhances operational efficiency for operators while accelerating the commercialization of advanced IP-based voice services, reinforcing the demand for scalable IMS platforms across Europe

- In February 2025, Kyocera, Ataya, and Ecrio unveiled a private 5G kit featuring mission-critical VoNR and Rich Communication Services tailored for first responders. The solution expands IMS adoption into enterprise and public safety networks, driving new revenue streams beyond traditional telecom operators and strengthening the role of IMS in mission-critical communications

- In January 2025, Alianza announced plans to complete the acquisition of Metaswitch from Microsoft, consolidating a large base of service-provider customers under a unified cloud communications portfolio. This consolidation is reshaping the competitive landscape of the IMS market, creating integration opportunities while prompting other vendors to enhance support and modernization services

- In November 2024, Swisscom and Ericsson launched a fully standalone private 5G network offering for Swiss enterprises, built on advanced IMS capabilities. The initiative accelerates enterprise adoption of IP-based voice and multimedia services over private networks, highlighting the growing importance of IMS in enabling secure and dedicated communication infrastructures

- In October 2024, Nokia introduced an upgraded cloud-native IMS solution designed to support 5G standalone deployments and enhanced VoNR services. This launch strengthens vendor competition in the IMS ecosystem and supports telecom operators in migrating from legacy systems to fully virtualized core networks, further driving global IMS market expansion

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.