Global Medical Sensors Market

Размер рынка в млрд долларов США

CAGR :

%

USD

3.08 Billion

USD

6.30 Billion

2025

2033

USD

3.08 Billion

USD

6.30 Billion

2025

2033

| 2026 –2033 | |

| USD 3.08 Billion | |

| USD 6.30 Billion | |

| % | |

|

Global Medical Sensors Market Segmentation, By Type (Pressure Sensor, Accelerator (Inertial) Sensors, Motion Sensor, Image Sensor, Electrocardiogram Sensor, Temperature Sensor, Blood Glucose, and Blood Oxygen Sensor), Sensor Placement (Strip Sensors, Wearable Sensors, Implantable Sensors, Non-Invasive and Invasive Sensors, and Ingestible Sensors), Application (Diagnostic, Therapeutics, Monitoring, Imaging, Fitness and Wellness, and Others), End Users (Hospitals, Ambulatory Centers, Clinics, and Community Healthcare), Distribution Channel (Retail and Direct Tenders) - Industry Trends and Forecast to 2033

What is the Global Medical Sensors Market Size and Growth Rate?

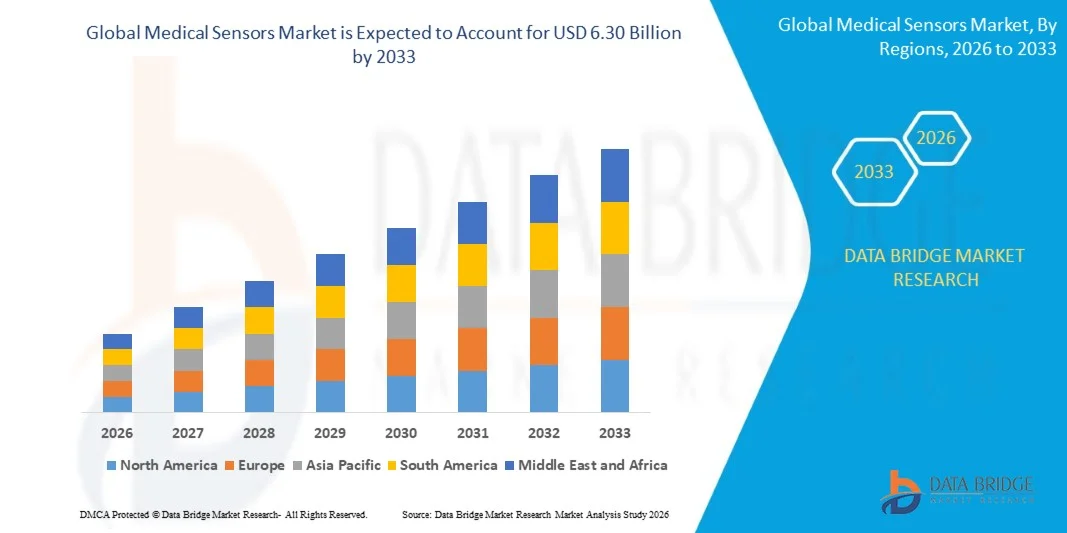

- The global medical sensors market size was valued at USD 3.08 billion in 2025 and is expected to reach USD 6.30 billion by 2033, at a CAGR of 9.35% during the forecast period

- Major factors that are expected to boost the growth of the medical sensors market in the forecast period are the rise in the uses of sensors in the clinics and home applications and the increasing knowledge regarding the patients for monitoring and diagnosing of the disease

- Furthermore, the rising investment in research and development of devices based on sensors is further anticipated to propel the growth of the medical sensors market

What are the Major Takeaways of Medical Sensors Market?

- The growing adoption of IoT-based medical devices is further estimated to cushion the growth of the medical sensors market. On the other hand, the decrease in the penetration of medical devices in the advancing countries is further projected to impede the growth of the medical sensors market in the timeline period

- In addition, the development in the sensors and digital technologies will further provide potential opportunities for the growth of the medical sensors market in the coming years. However, the strict regulatory environment and requirement of product approvals might further challenge the growth of the medical sensors market in the near future

- North America dominated the medical sensors market with a 36.31% revenue share in 2025, driven by strong growth in advanced healthcare infrastructure, increasing adoption of wearable health devices, and rapid expansion of digital health technologies across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 8.34% from 2026 to 2033, driven by rapid expansion of healthcare infrastructure, increasing adoption of wearable devices, and rising demand for affordable diagnostic solutions across China, Japan, India, South Korea, and Southeast Asia

- The Blood Glucose Sensor segment dominated the market with a 28.6% share in 2025, driven by the rising global prevalence of diabetes and increasing adoption of continuous glucose monitoring (CGM) systems

Report Scope and Medical Sensors Market Segmentation

|

Attributes |

Medical Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Medical Sensors Market?

“Rising Adoption of Miniaturized, Wearable, and IoT-Integrated Medical Sensors”

- The medical sensors market is witnessing strong adoption of miniaturized, wireless, and wearable sensor technologies designed to support continuous health monitoring, remote patient care, and real-time diagnostics

- Manufacturers are introducing high-precision, multi-parameter, and low-power sensors with advanced data analytics, AI integration, and compatibility with digital health platforms

- Growing demand for cost-efficient, portable, and patient-friendly monitoring solutions is driving adoption across hospitals, home healthcare, and telemedicine applications

- For instance, companies such as Koninklijke Philips N.V., Honeywell International Inc, STMicroelectronics, and Medtronic are developing advanced biosensors, wearable monitoring devices, and smart diagnostic systems

- Increasing need for real-time health tracking, early disease detection, and remote monitoring is accelerating the shift toward connected and AI-enabled medical sensors

- As healthcare becomes more digital, personalized, and preventive, medical sensors will remain critical for improving patient outcomes and enabling next-generation healthcare delivery

What are the Key Drivers of Medical Sensors Market?

- Rising demand for accurate, real-time, and non-invasive monitoring devices to support chronic disease management, patient safety, and early diagnosis

- For instance, in 2025, leading companies such as Sensirion AG, NXP Semiconductors, and Danaher expanded their sensor portfolios with enhanced precision, connectivity, and low-power capabilities

- Growing adoption of wearable devices, IoT-enabled healthcare systems, robotics, and smart medical equipment is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in MEMS technology, biosensing materials, signal processing, and wireless communication have improved sensor performance, reliability, and energy efficiency

- Rising use of AI-based diagnostics, remote patient monitoring, and digital therapeutics is creating demand for multi-functional and high-sensitivity sensors

- Supported by increasing investments in healthcare infrastructure, digital health ecosystems, and medical device innovation, the Medical Sensors market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Medical Sensors Market?

- High costs associated with advanced biosensors, wearable devices, and integrated monitoring systems limit adoption in cost-sensitive healthcare settings and emerging markets

- For instance, during 2024–2025, fluctuations in semiconductor supply, sensor component costs, and regulatory compliance requirements increased production expenses for several global manufacturers

- Complexity in integrating multi-sensor systems, data analytics platforms, and AI-based diagnostics increases the need for specialized expertise and technical infrastructure

- Limited awareness and lack of standardization in digital health technologies in developing regions slow down widespread adoption

- Stringent regulatory approvals, data privacy concerns, and cybersecurity risks create additional challenges for market expansion

- To address these issues, companies are focusing on cost-effective designs, regulatory compliance, cloud integration, and enhanced data security, which will support broader adoption of medical sensors globally

How is the Medical Sensors Market Segmented?

The market is segmented on the basis of type, sensor placement, application, distribution channel, and end users.

• By Type

On the basis of type, the medical sensors market is segmented into Pressure Sensors, Accelerometer (Inertial) Sensors, Motion Sensors, Image Sensors, Electrocardiogram Sensors, Temperature Sensors, Blood Glucose Sensors, and Blood Oxygen Sensors. The Blood Glucose Sensor segment dominated the market with a 28.6% share in 2025, driven by the rising global prevalence of diabetes and increasing adoption of continuous glucose monitoring (CGM) systems. These sensors are widely used in wearable and implantable devices for real-time tracking, improving patient outcomes and disease management. Their high accuracy, ease of use, and integration with digital health platforms further support strong adoption across home healthcare and clinical settings.

The Image Sensor segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing use in advanced diagnostic imaging, endoscopy, and minimally invasive procedures. Rising demand for high-resolution imaging and AI-assisted diagnostics is accelerating growth in this segment.

• By Sensor Placement

On the basis of sensor placement, the market is segmented into Strip Sensors, Wearable Sensors, Implantable Sensors, Non-Invasive and Invasive Sensors, and Ingestible Sensors. The Wearable Sensors segment dominated the market with a 34.2% share in 2025, owing to the growing popularity of smart health devices such as fitness trackers, smartwatches, and remote monitoring systems. These sensors enable continuous tracking of vital parameters such as heart rate, oxygen levels, and physical activity, making them essential for preventive healthcare and chronic disease management. Their convenience, portability, and integration with mobile health applications have significantly boosted adoption among consumers and healthcare providers.

The Implantable Sensors segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by advancements in biosensor technology, increasing use in cardiac monitoring, neurostimulation, and long-term disease management, and rising demand for real-time internal health data.

• By Application

On the basis of application, the medical sensors market is segmented into Diagnostic, Therapeutics, Monitoring, Imaging, Fitness and Wellness, and Others. The Monitoring segment dominated the market with a 31.8% share in 2025, supported by increasing demand for continuous patient monitoring in hospitals, home care, and remote healthcare settings. Medical sensors are extensively used for tracking vital signs such as heart rate, blood pressure, oxygen saturation, and temperature. The rise in chronic diseases and aging populations has further strengthened demand for real-time monitoring solutions.

The Diagnostic segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by advancements in early disease detection, point-of-care testing, and AI-based diagnostic tools. Increasing focus on preventive healthcare and rapid testing solutions is accelerating adoption across healthcare systems globally.

• By End Users

On the basis of end users, the market is segmented into Hospitals, Ambulatory Centers, Clinics, and Community Healthcare. The Hospitals segment dominated the market with a 40.5% share in 2025, due to high patient inflow, availability of advanced medical infrastructure, and extensive use of monitoring and diagnostic equipment. Hospitals rely heavily on medical sensors for critical care, surgical procedures, and patient monitoring, driving consistent demand.

The Community Healthcare segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by the shift toward decentralized healthcare, increasing adoption of home-based monitoring devices, and government initiatives promoting primary healthcare access. Rising demand for cost-effective and accessible healthcare solutions is further supporting growth in this segment.

• By Distribution Channel

On the basis of distribution channel, the medical sensors market is segmented into Retail and Direct Tenders. The Direct Tenders segment dominated the market with a 62.3% share in 2025, as hospitals, healthcare institutions, and government organizations procure medical sensors in bulk through contracts and tenders. This channel ensures cost efficiency, consistent supply, and compliance with regulatory standards, making it the preferred procurement method for large-scale healthcare providers.

The Retail segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing consumer adoption of wearable health devices, home diagnostic kits, and over-the-counter medical sensors. Growth in e-commerce platforms and digital health awareness is further accelerating retail channel expansion.

Which Region Holds the Largest Share of the Medical Sensors Market?

- North America dominated the medical sensors market with a 36.31% revenue share in 2025, driven by strong growth in advanced healthcare infrastructure, increasing adoption of wearable health devices, and rapid expansion of digital health technologies across the U.S. and Canada. High demand for real-time patient monitoring, chronic disease management, and minimally invasive diagnostics continues to fuel adoption of medical sensors across hospitals, home healthcare, and clinical research centres

- Leading companies in North America are introducing advanced biosensors, AI-integrated diagnostic tools, and remote monitoring solutions, strengthening the region’s technological leadership. Continuous investment in telehealth, connected healthcare systems, and precision medicine drives long-term market expansion

- High healthcare spending, strong R&D ecosystems, and increasing focus on preventive and personalized medicine further reinforce regional market dominance

U.S. Medical Sensors Market Insight

The U.S. is the largest contributor in North America, supported by advanced healthcare infrastructure, strong adoption of digital health solutions, and extensive utilization of wearable and implantable sensors across hospitals, clinics, and home care settings. Increasing prevalence of chronic diseases, rising demand for remote patient monitoring, and rapid development of AI-based diagnostic platforms intensify demand for high-precision medical sensors. Presence of leading medical device companies, strong startup ecosystems, and high investment in healthcare innovation further drive market growth.

Canada Medical Sensors Market Insight

Canada contributes significantly to regional growth, driven by expanding healthcare digitization, rising adoption of remote monitoring technologies, and growing investment in medical research and innovation. Hospitals and healthcare institutions increasingly utilize medical sensors for patient monitoring, diagnostics, and chronic disease management. Government-supported healthcare initiatives, skilled workforce availability, and increasing demand for telemedicine and smart healthcare solutions strengthen market adoption across the country.

Asia-Pacific Medical Sensors Market

Asia-Pacific is projected to register the fastest CAGR of 8.34% from 2026 to 2033, driven by rapid expansion of healthcare infrastructure, increasing adoption of wearable devices, and rising demand for affordable diagnostic solutions across China, Japan, India, South Korea, and Southeast Asia. Growing population, increasing prevalence of chronic diseases, and rising healthcare awareness are boosting demand for medical sensors. Expansion of telehealth services, digital health platforms, and government healthcare initiatives further accelerates market growth across the region.

China Medical Sensors Market Insight

China is the largest contributor to Asia-Pacific due to massive healthcare investments, expanding medical device manufacturing, and strong government support for digital healthcare transformation. Rising adoption of wearable health devices, AI-powered diagnostics, and remote monitoring systems drives demand for advanced medical sensors. Local manufacturing capabilities and cost advantages further enhance domestic and export market growth.

Japan Medical Sensors Market Insight

Japan shows steady growth supported by advanced healthcare infrastructure, aging population, and strong focus on precision medical technologies. Increasing demand for minimally invasive procedures, robotic surgeries, and high-performance diagnostic systems drives adoption of high-quality medical sensors. Continuous innovation in healthcare electronics and smart medical devices supports long-term market expansion.

India Medical Sensors Market Insight

India is emerging as a major growth hub, driven by expanding healthcare access, rising adoption of wearable devices, and government initiatives promoting digital health and telemedicine. Growing demand for affordable diagnostic tools, remote monitoring solutions, and chronic disease management systems fuels adoption of medical sensors. Increasing investment in healthcare infrastructure and rising startup activity further accelerate market penetration.

South Korea Medical Sensors Market Insight

South Korea contributes significantly due to strong demand for advanced healthcare technologies, smart hospitals, and high-performance medical devices. Rapid development of digital health platforms, AI-based diagnostics, and wearable monitoring systems drives adoption of medical sensors. Technological innovation, strong manufacturing capabilities, and growing healthcare digitalization support sustained market growth.

Which are the Top Companies in Medical Sensors Market?

The medical sensors industry is primarily led by well-established companies, including:

- Koninklijke Philips N.V. (Netherlands)

- Sensirion AG (Switzerland)

- Honeywell International Inc (U.S.)

- Smiths Group plc (U.K.)

- STMicroelectronics (Switzerland)

- OmniVision Technologies, Inc. (U.S.)

- MEMSIC, Inc (U.S.)

- Universal Biosensors (Australia)

- Biosensors International Group, Ltd. (Singapore)

- GeekWire, LLC (U.S.)

- General Electric Company (U.S.)

- Medtronic (Ireland)

- First Sensor AG (Germany)

- NXP Semiconductors (Netherlands)

- Danaher (U.S.)

What are the Recent Developments in Global Medical Sensors Market?

- In March 2024, Stryker expanded its medical device testing laboratory in India with a 55,600-square-foot advanced facility equipped with enhanced infrastructure, upgraded microbiology capabilities, and a skilled workforce to support innovation and ensure high product quality across its medical technology portfolio, thereby strengthening its R&D capabilities and regional presence

- In October 2023, Siemens Healthineers introduced a breakthrough non-invasive blood glucose monitoring technology that enables pain-free testing using advanced sensor systems, improving patient comfort and compliance in diabetes management, thereby enhancing the adoption of next-generation diagnostic solutions

- In September 2023, Medtronic launched an upgraded continuous glucose monitoring system that provides real-time readings and alerts for blood sugar levels, helping patients and healthcare providers optimize insulin administration and improve disease management, thereby advancing patient outcomes and digital healthcare integration

- In August 2023, GE Healthcare introduced an advanced wearable cardiac monitoring device designed for continuous 24-hour heart rhythm tracking and remote patient monitoring, enabling timely medical intervention and reducing hospital readmissions, thereby supporting the growth of remote healthcare solutions

- In June 2023, OmniVision Technologies Inc. launched the OVMed OCHTA cable module for single-use endoscopes, featuring ultra-thin cables and compact imaging technology with customizable lengths and optional mini-LED illumination, thereby enhancing precision and flexibility in minimally invasive medical procedures

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.