Global Medical Tubing Market

Размер рынка в млрд долларов США

CAGR :

%

USD

13.17 Billion

USD

26.82 Billion

2025

2033

USD

13.17 Billion

USD

26.82 Billion

2025

2033

| 2026 –2033 | |

| USD 13.17 Billion | |

| USD 26.82 Billion | |

| % | |

|

Global Medical Tubing Market Segmentation, By Product (Silicone, Polyolefin, Polyvinyl Chloride, Polycarbonates, Fluoropolymers, and Others), Structure (Single-Lumen, Multi-Lumen, Co-Extruded, Tapered or Bump Tubing, Braided Tubing, Balloon Tubing, and Heat Shrink Tubing), End-User (Hospitals and Clinics, Ambulatory Surgical Centers, Medical Labs, and Others), Application (Bulk Disposable Tubing, Drug Delivery Systems, Catheters, Biopharmaceutical Laboratory Equipment, and Others) - Industry Trends and Forecast to 2033

Medical Tubing Market Size

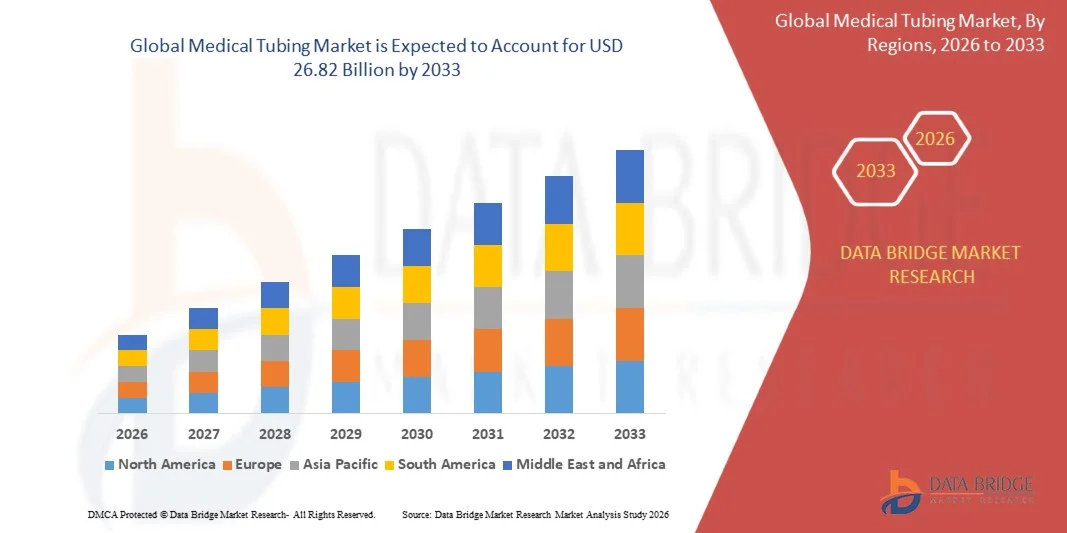

- The global medical tubing market size was valued at USD 13.17 billion in 2025 and is expected to reach USD 26.82 billion by 2033, at a CAGR of 9.30% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive procedures, advanced drug delivery systems, and biopharmaceutical processing, leading to higher demand for biocompatible, flexible, and sterilizable medical tubing across hospitals, clinics, and laboratories

- Furthermore, rising demand for disposable, single-use, and high-performance tubing solutions is establishing silicone, polyolefin, and specialty polymer tubing as the preferred choice for fluid management, catheter applications, and laboratory equipment. These converging factors are accelerating the uptake of medical tubing solutions, thereby significantly boosting the industry’s growth

Medical Tubing Market Analysis

- Medical tubing comprises biocompatible, flexible, and durable tubes used in drug delivery systems, catheters, laboratory equipment, and biopharmaceutical processing. These tubes must meet strict regulatory standards, provide chemical resistance, and ensure safety and reliability for critical healthcare applications

- The escalating demand for medical tubing is primarily fueled by the growing number of surgical procedures, increasing outpatient care facilities, and rising investments in healthcare infrastructure. In addition, the preference for precision fluid handling, sterilizable materials, and integration with advanced medical devices continues to drive market expansion across global healthcare and laboratory sectors

- North America dominated the medical tubing market with a share of 35.8% in 2025, due to the presence of advanced healthcare infrastructure, high adoption of minimally invasive procedures, and increasing demand for disposable and biocompatible tubing solutions

- Asia-Pacific is expected to be the fastest growing region in the medical tubing market during the forecast period due to rising healthcare expenditure, urbanization, and expansion of modern hospitals in countries such as China, Japan, and India

- Silicone segment dominated the market with a market share of 43% in 2025, due to its biocompatibility, flexibility, and chemical inertness, making it suitable for a wide range of medical applications. Hospitals and laboratories often prefer silicone tubing for drug delivery systems and catheter assemblies due to its durability and sterilization compatibility. The segment’s widespread adoption is further supported by the availability of various diameters and wall thicknesses, allowing precise customization for different procedures

Report Scope and Medical Tubing Market Segmentation

|

Attributes |

Medical Tubing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Tubing Market Trends

“Rising Adoption of Biocompatible and Advanced Polymer Medical Tubing”

- A notable trend in the medical tubing market is the increasing adoption of biocompatible and advanced polymer tubing, driven by the growing emphasis on patient safety and minimally invasive procedures. These materials are enhancing the performance, flexibility, and durability of tubing used across hospitals, clinics, and biopharmaceutical applications

- For instance, companies such as Saint-Gobain and Becton Dickinson manufacture advanced polymer medical tubing that is widely used in intravenous delivery systems and catheters. This adoption is improving fluid management, reducing contamination risks, and supporting a broad range of therapeutic procedures

- The trend toward miniaturized and high-precision medical devices is increasing the demand for tubing with tight tolerances and specialized coatings, which enable better control in surgical and diagnostic procedures. This is positioning medical tubing as a critical component in next-generation medical equipment

- Hospitals and clinical settings are increasingly implementing single-use tubing solutions to minimize infection risks, optimize operational efficiency, and comply with strict hygiene protocols. This is reinforcing the preference for polymer-based, disposable tubing products

- Biopharmaceutical manufacturing processes are adopting advanced tubing for sterile fluid transfer and drug delivery applications where chemical resistance and flexibility are essential. This trend is driving innovation in tubing designs that meet stringent regulatory and performance requirements

- The market is witnessing growth in customized medical tubing solutions where materials, diameters, and lengths are tailored to specific procedures. This rising demand for application-specific tubing is shaping the overall market expansion and technological development

Medical Tubing Market Dynamics

Driver

“Growing Demand from Hospitals, Clinics, and Biopharmaceutical Applications”

- The increasing requirement for reliable and high-performance tubing across hospitals, clinics, and biopharmaceutical manufacturing is driving market growth. These applications necessitate biocompatible, chemically resistant, and flexible tubing to ensure patient safety and process efficiency

- For instance, companies such as Tygon (Saint-Gobain) supply tubing solutions specifically designed for IV therapy and pharmaceutical fluid transfer. Their products help maintain sterility, reduce contamination, and improve procedural outcomes in healthcare and laboratory environments

- The expansion of minimally invasive surgeries and outpatient procedures is fueling demand for precision tubing that supports catheterization, endoscopy, and infusion devices. This demand is encouraging manufacturers to innovate tubing with improved mechanical and chemical properties

- The rise in biopharmaceutical production is increasing the need for sterile tubing capable of handling complex fluids in drug manufacturing and delivery. These requirements are influencing material selection and design innovation within the medical tubing market

- Medical device manufacturers are investing in advanced tubing to enhance the safety and efficiency of medical instruments. This investment is strengthening the integration of high-performance tubing across diverse healthcare applications

Restraint/Challenge

“High Production Costs and Stringent Regulatory Compliance”

- The medical tubing market faces challenges due to high production costs associated with advanced polymer materials, specialized extrusion techniques, and precision manufacturing. These factors increase capital investment and operational expenses for manufacturers

- For instance, Becton Dickinson adheres to rigorous FDA and ISO 13485 compliance standards during tubing production, which requires extensive quality testing, validation, and documentation. These regulatory demands add complexity and cost to the manufacturing process

- Maintaining sterility and biocompatibility during production requires advanced facilities and stringent environmental controls. These requirements extend lead times and elevate overall production expenses for medical tubing

- The reliance on high-quality raw materials, including silicone and polyurethane polymers, contributes to cost volatility and supply chain dependency. Manufacturers must balance material performance with economic feasibility to remain competitive

- Scaling production while ensuring regulatory compliance, product consistency, and durability remains a critical challenge. These factors collectively constrain market growth and require continuous process optimization by industry players

Medical Tubing Market Scope

The market is segmented on the basis of product, structure, end-user, and application.

• By Product

On the basis of product, the medical tubing market is segmented into silicone, polyolefin, polyvinyl chloride, polycarbonates, fluoropolymers, and others. The silicone segment dominated the largest market revenue share of 43% in 2025, driven by its biocompatibility, flexibility, and chemical inertness, making it suitable for a wide range of medical applications. Hospitals and laboratories often prefer silicone tubing for drug delivery systems and catheter assemblies due to its durability and sterilization compatibility. The segment’s widespread adoption is further supported by the availability of various diameters and wall thicknesses, allowing precise customization for different procedures. Silicone’s thermal stability and resistance to kinking also enhance operational reliability, increasing its preference over other materials.

The polyolefin segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand in disposable medical devices and laboratory applications. Polyolefin tubing offers cost-effective manufacturing, chemical resistance, and lightweight properties, making it attractive for single-use setups. Its growing adoption is also driven by compatibility with automated production lines and ease of integration into drug delivery and biopharmaceutical systems. Manufacturers increasingly favor polyolefin tubing to meet the surge in outpatient procedures and minimally invasive interventions. The material’s recyclability and sustainability appeal further contribute to its rapid growth trajectory.

• By Structure

On the basis of structure, the medical tubing market is segmented into single-lumen, multi-lumen, co-extruded, tapered or bump tubing, braided tubing, balloon tubing, and heat shrink tubing. The single-lumen segment dominated the largest market revenue share in 2025, attributed to its simplicity, reliability, and broad applicability across medical devices. Single-lumen tubing is widely used in drug delivery systems, fluid management, and laboratory setups due to its straightforward design and ease of sterilization. Its compatibility with various connectors and fittings makes it a preferred choice in both hospitals and research laboratories.

The multi-lumen segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the need for simultaneous delivery of multiple fluids or medications through a single tubing assembly. Multi-lumen tubing enhances procedural efficiency in critical care, catheterization, and infusion therapy. For instance, manufacturers such as B. Braun have expanded multi-lumen product lines for advanced intravenous applications. Its adoption is increasing in ambulatory surgical centers and specialized clinics requiring compact, high-functionality solutions.

• By End-User

On the basis of end-user, the medical tubing market is segmented into hospitals and clinics, ambulatory surgical centers, medical labs, and others. Hospitals and clinics dominated the largest market revenue share in 2025, driven by their extensive procedural volumes and diverse medical needs. Hospitals require medical tubing for drug delivery systems, fluid management, catheters, and laboratory operations, creating steady demand. The preference for high-quality, sterilizable tubing in hospitals supports adoption across a broad range of applications.

Ambulatory surgical centers are anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising trend of outpatient procedures and minimally invasive surgeries. These centers favor lightweight, flexible, and disposable tubing solutions to enhance operational efficiency and reduce infection risks. For instance, Smiths Medical has developed specialized tubing sets for ambulatory care settings. The growth is further accelerated by increasing healthcare accessibility and cost-efficient procedural models.

• By Application

On the basis of application, the medical tubing market is segmented into bulk disposable tubing, drug delivery systems, catheters, biopharmaceutical laboratory equipment, and others. The drug delivery systems segment dominated the largest market revenue share in 2025, attributed to the rising use of intravenous therapy, infusion pumps, and controlled medication administration. Drug delivery tubing demands high precision, biocompatibility, and chemical resistance, driving the preference for materials such as silicone and polyolefin. Hospitals and clinics rely on this segment to ensure patient safety and efficient fluid administration, contributing to its market dominance.

The catheters segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the growing prevalence of cardiovascular diseases, minimally invasive interventions, and critical care procedures. Catheter tubing requires flexible, kink-resistant, and biocompatible materials, promoting innovation in design and material selection. For instance, Medtronic has introduced advanced catheter tubing solutions for complex interventions. Adoption is increasing across hospitals, surgical centers, and specialty clinics, supporting sustained growth in this application segment.

Medical Tubing Market Regional Analysis

- North America dominated the medical tubing market with the largest revenue share of 35.8% in 2025, driven by the presence of advanced healthcare infrastructure, high adoption of minimally invasive procedures, and increasing demand for disposable and biocompatible tubing solutions

- Healthcare providers in the region prioritize safety, reliability, and regulatory-compliant tubing for hospitals, clinics, and laboratories

- This widespread adoption is further supported by high healthcare expenditure, technologically advanced hospitals, and growing preference for innovative drug delivery and fluid management systems, establishing medical tubing as a critical component in healthcare delivery

U.S. Medical Tubing Market Insight

The U.S. medical tubing market captured the largest revenue share in 2025 within North America, fueled by rising hospital procedural volumes, increasing outpatient surgeries, and adoption of advanced drug delivery systems. Healthcare providers are emphasizing precision, biocompatibility, and sterilization-friendly tubing materials such as silicone and polyolefin. The growth is further propelled by demand for disposable tubing in ambulatory surgical centers and laboratories, alongside technological advancements in catheter and infusion device tubing.

Europe Medical Tubing Market Insight

The Europe medical tubing market is projected to expand at a substantial CAGR during the forecast period, primarily driven by well-established healthcare systems, stringent regulatory standards, and increasing demand for advanced medical devices. Rising adoption of laboratory automation, minimally invasive procedures, and precision fluid delivery systems is fostering market growth. European healthcare providers increasingly choose tubing solutions that ensure patient safety, reduce contamination risks, and improve procedural efficiency, supporting steady adoption across hospitals and clinics.

U.K. Medical Tubing Market Insight

The U.K. medical tubing market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing focus on outpatient care, surgical efficiency, and hospital modernization. Demand for flexible, kink-resistant, and sterilizable tubing is rising in hospitals and surgical centers. The U.K.’s emphasis on healthcare innovation and strong presence of medical device manufacturers is expected to continue driving market expansion.

Germany Medical Tubing Market Insight

The Germany medical tubing market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced hospital infrastructure, emphasis on precision medicine, and high adoption of biopharmaceutical and laboratory equipment. German healthcare facilities prioritize reliable and durable tubing solutions that comply with strict regulatory standards. Integration of tubing in automated drug delivery systems and critical care applications is increasing, supporting steady adoption in hospitals and laboratories.

Asia-Pacific Medical Tubing Market Insight

The Asia-Pacific medical tubing market is poised to grow at the fastest CAGR during 2026 to 2033, driven by rising healthcare expenditure, urbanization, and expansion of modern hospitals in countries such as China, Japan, and India. Increasing awareness of quality healthcare, growing surgical volumes, and adoption of minimally invasive procedures are fueling demand. APAC’s emergence as a hub for medical device manufacturing, coupled with affordable and accessible tubing solutions, is further driving the market.

Japan Medical Tubing Market Insight

The Japan medical tubing market is gaining momentum due to the country’s aging population, high healthcare standards, and technological adoption in hospitals and clinics. Demand for easy-to-use, safe, and biocompatible tubing in drug delivery and catheter applications is rising. Integration with advanced medical devices and laboratory systems is boosting growth in both hospital and research applications.

China Medical Tubing Market Insight

The China medical tubing market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid hospital expansion, growing middle-class healthcare demand, and rising surgical procedures. Hospitals and clinics are increasingly adopting silicone, polyolefin, and PVC tubing for drug delivery, catheters, and laboratory use. The push towards healthcare modernization, domestic manufacturing of medical tubing, and government initiatives supporting medical device adoption are key factors driving market growth in China.

Medical Tubing Market Share

The medical tubing industry is primarily led by well-established companies, including:

- Saint-Gobain Group (France)

- The Lubrizol Corporation (U.S.)

- Optinova (Sweden)

- Tekni-Plex (U.S.)

- Zeus Industrial Products, Inc. (U.S.)

- Nordson Corporation (U.S.)

- Putnam Plastics (U.S.)

- W. L. Gore & Associates, Inc. (U.S.)

- RAUMEDIC AG (Germany)

- Teknor Apex (U.S.)

- Teleflex Incorporated (U.S.)

- Freudenberg Medical (Germany)

- Dow (U.S.)

- Avient Corporation (U.S.)

- Coloplast Corp. (Denmark)

- ConvaTec Group PLC (U.K.)

- Boston Scientific Corporation (U.S.)

- LVD Biotech (U.S.)

- A.P. Extrusion Incorporated (U.S.)

- Elkem ASA (Norway)

Latest Developments in Global Medical Tubing Market

- In September 2025, Junkosha announced at Medical Technology Ireland 2025 the expansion of its medical tubing portfolio, featuring new optically clear Peelable Heat Shrink Tubing designed for catheter manufacturing. This product offers superior optical clarity, reduces assembly risks, and streamlines manufacturing processes. By increasing production capacity by 300% from 2021 to 2025, including doubling output for Peelable Heat Shrink Tubing and Etched PTFE Liners, Junkosha is strengthening its market position and ensuring a reliable supply of innovative tubing solutions. This expansion supports growing demand in interventional device manufacturing and enhances the company’s ability to cater to high-volume, precision-critical applications

- In April 2025, DuPont launched its Liveo Pharma TPE Ultra-Low Temp Tubing for biopharmaceutical processing, designed to withstand extreme temperatures down to -86°C while providing resistance to bending, crushing, impact, burst pressure, and chemicals. The phthalate-free tubing is sterilizable, weldable, sealable, and compliant with USP Class VI, USP <665>, USP <232>, and ISO 10993 standards. This launch reinforces DuPont’s leadership in single-use fluid transport solutions, complements its silicone-based Liveo Pharma portfolio, and meets the growing market demand for high-performance, regulatory-compliant tubing in biopharma and laboratory applications

- In April 2024, Cobalt Polymers partnered with HnG Medical to distribute its heat shrink tubing products in Asia. This collaboration expands the company’s regional market presence and enhances accessibility to high-quality medical tubing for the growing medical device industry across Asia-Pacific. The partnership supports increased adoption of specialized tubing in catheter assemblies, drug delivery systems, and laboratory applications, contributing to market penetration and revenue growth in emerging healthcare markets

- In June 2023, TekniPlex announced a major investment in new medical tubing extrusion lines along with downstream processing equipment as part of its facility expansion in Costa Rica. This investment enhances production capacity and operational efficiency, enabling TekniPlex to meet the rising global demand for biocompatible and specialty tubing used in hospitals, surgical centers, and laboratories. The expansion positions the company to capture increased market share in North and Latin America and respond to growing demand in both standard and custom medical tubing applications

- In April 2023, Qosina collaborated with DuPont to introduce five new Liveo biopharmaceutical-grade tubing products to its portfolio. This development strengthens Qosina’s offering of high-performance tubing for single-use biopharma processes, supporting applications such as drug delivery, fluid management, and laboratory equipment. The collaboration enhances the company’s ability to meet stringent regulatory requirements and growing market needs for safe, durable, and flexible medical tubing solutions, reinforcing its position in the competitive biopharmaceutical tubing market

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.