Global Memory Disorders Market

Размер рынка в млрд долларов США

CAGR :

%

USD

7.90 Billion

USD

14.51 Billion

2025

2033

USD

7.90 Billion

USD

14.51 Billion

2025

2033

| 2026 –2033 | |

| USD 7.90 Billion | |

| USD 14.51 Billion | |

| % | |

|

Global Memory Disorders Market Segmentation, By Types (Dementia, Amnesia, and Others), Medication (Drugs, Physical Therapy, Psychotherapy, and Others), By Route of Administration (Oral, Parenteral, and Others), By End-Users (Hospitals, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Others) - Industry Trends and Forecast to 2033

Memory Disorders Market Size

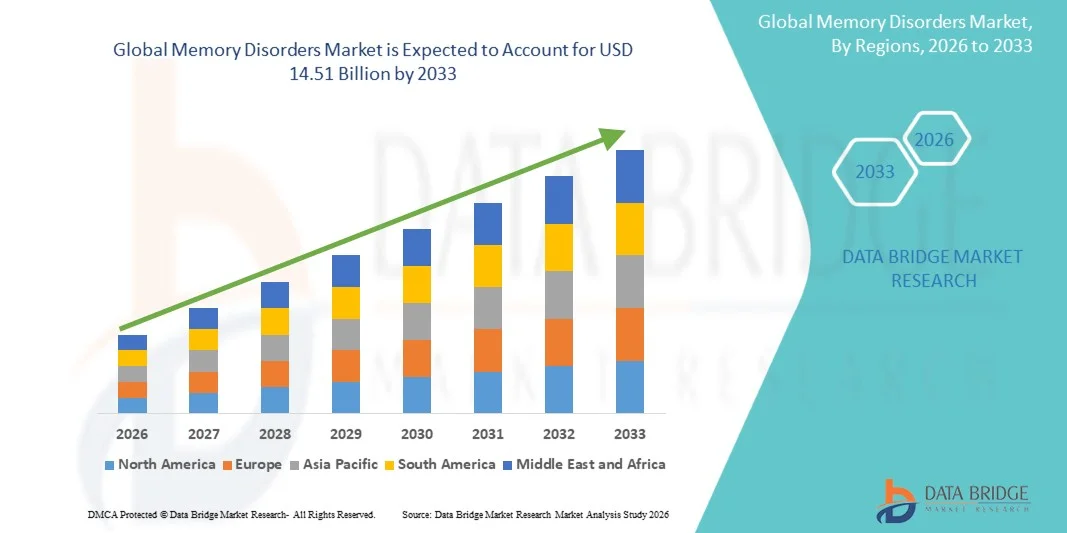

- The global memory disorders market size was valued at USD 7.90 billion in 2025 and is expected to reach USD 14.51 billion by 2033, at a CAGR of 7.90% during the forecast period

- The market growth is largely fueled by increasing prevalence of neurodegenerative conditions such as Alzheimer’s disease, dementia, and other cognitive impairments, leading to higher demand for early diagnosis and effective therapeutic interventions in the Memory Disorders market across healthcare systems

- Furthermore, rising awareness regarding mental health, cognitive screening programs, and advancements in neurology-focused research and drug development are establishing Memory Disorders solutions as a critical area of modern healthcare. These converging factors are accelerating the uptake of Memory Disorders treatments, thereby significantly boosting the industry's growth

Memory Disorders Market Analysis

- Memory Disorders therapeutics and diagnostics, including pharmacological treatments, cognitive therapies, and digital cognitive assessment tools, are increasingly vital components of modern neurology and mental healthcare systems due to rising prevalence of Alzheimer’s disease, dementia, and other cognitive impairments, along with growing emphasis on early diagnosis and long-term disease management

- The escalating demand for Memory Disorders solutions is primarily fueled by the increasing aging population, rising incidence of neurodegenerative diseases, and growing awareness regarding early cognitive screening and intervention, along with advancements in neuroscience research and drug development

- North America dominated the memory disorders market with the largest revenue share of 43% in 2025, characterized by strong healthcare infrastructure, high adoption of advanced neurological treatments, significant R&D investments, and the presence of leading pharmaceutical and biotechnology companies focused on CNS disorders

- Asia-Pacific is expected to be the fastest growing region in the memory disorders market during the forecast period due to rapid population aging, improving healthcare access, increasing government initiatives for neurological disease management, and rising awareness of mental health conditions

- The Oral segment dominated the largest market revenue share of 72.1% in 2025, driven by ease of administration and high patient compliance in long-term therapy

Report Scope and Memory Disorders Market Segmentation

|

Attributes |

Memory Disorders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Memory Disorders Market Trends

“Advancements in Precision Medicine, Digital Health Integration, and Neurotherapeutic Innovation”

- A significant and accelerating trend in the global Memory Disorders market is the growing integration of artificial intelligence (AI), digital health platforms, and advanced neurodiagnostic technologies, which is transforming how memory-related conditions such as Alzheimer’s disease and other cognitive impairments are detected, monitored, and managed

- For instance, AI-powered cognitive assessment tools and digital biomarkers are increasingly being used to detect early signs of memory decline through speech analysis, behavioral tracking, and memory performance monitoring via mobile applications

- Wearable devices and remote patient monitoring systems are enabling continuous tracking of cognitive health indicators, allowing clinicians to intervene earlier and more effectively

- For instance, digital therapeutics platforms are being developed to deliver personalized cognitive training programs designed to slow disease progression and improve patient outcomes

- The integration of neuroimaging, genomics, and machine learning is further enhancing diagnostic accuracy and supporting precision medicine approaches in memory disorder treatment

- This shift toward data-driven, personalized neurological care is fundamentally reshaping clinical decision-making and patient management strategies

- Growing adoption of tele-neurology and digital care platforms is also improving access to specialist care, particularly in underserved and rural region

Memory Disorders Market Dynamics

Driver

“Increasing Prevalence of Neurodegenerative Diseases and Aging Population”

- The rising global prevalence of Alzheimer’s disease and other neurodegenerative conditions is a key driver of the memory disorders market, primarily due to the rapidly aging population worldwide

- For instance, a growing proportion of individuals aged 60 and above is increasing the incidence of age-related cognitive decline and dementia cases across both developed and emerging economies

- Expanding awareness of early diagnosis and cognitive health screening is encouraging more patients to seek medical evaluation at earlier disease stages

- For instance, healthcare systems are increasingly implementing routine cognitive screening programs for elderly populations to support early intervention strategies

- Strong investment in neuroscience research and drug development is accelerating the discovery of novel disease-modifying therapies targeting amyloid and tau pathways

- For instance, pharmaceutical companies are actively conducting clinical trials for monoclonal antibodies and other biologics aimed at slowing disease progression in Alzheimer’s patients

- Improved diagnostic infrastructure and increasing healthcare expenditure are further supporting market expansion globally

Restraint/Challenge

“High Treatment Costs, Limited Curative Therapies, and Diagnostic Complexity”

- One of the major challenges in the memory disorders market is the lack of curative treatments, with most available therapies focusing only on symptom management rather than disease reversal

- For instance, commonly used medications may temporarily improve cognitive function but do not halt the progression of Alzheimer’s disease

- High cost of advanced diagnostic procedures such as PET scans and biomarker testing limits accessibility in low- and middle-income regions

- For instance, cerebrospinal fluid testing and advanced neuroimaging remain expensive and are not widely available in many healthcare systems

- Complex disease pathology and variability in patient response make early and accurate diagnosis difficult, delaying effective treatment initiation

- In addition, long-term care requirements place a significant financial and emotional burden on families and healthcare systems

- Addressing these challenges requires increased investment in affordable diagnostics, development of disease-modifying therapies, and expansion of public healthcare support programs

Memory Disorders Market Scope

The market is segmented on the basis of types, medication, route of administration, end-users, and distribution channel.

• By Types

On the basis of types, the Memory Disorders market is segmented into Dementia, Amnesia, and Others. The Dementia segment dominated the largest market revenue share of 64.5% in 2025, driven by the rapidly rising global aging population and increasing prevalence of Alzheimer’s disease and other neurodegenerative conditions. Growing awareness regarding early diagnosis and treatment is further supporting market expansion. Increasing healthcare burden associated with cognitive decline is boosting demand for long-term care solutions. Advancements in diagnostic imaging and biomarker identification are improving detection rates. Rising healthcare expenditure globally enhances access to treatment. Strong clinical focus on managing dementia symptoms supports pharmaceutical adoption. Expanding geriatric population significantly contributes to disease prevalence. Government initiatives for mental health awareness further strengthen diagnosis rates. Increasing caregiver support programs are improving patient management. Continuous R&D in neurotherapeutics is enhancing treatment outcomes. Overall, dementia remains the dominant segment due to its high prevalence and chronic nature.

The Amnesia segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by increasing cases of traumatic brain injuries and neurological disorders. Rising road accidents and sports-related injuries are contributing to demand growth. Improved diagnostic techniques are enabling earlier detection of memory impairment conditions. Increasing awareness about cognitive rehabilitation therapies supports adoption. Expanding neurological care infrastructure enhances treatment access. Growing research in brain recovery therapies is driving innovation. Rising mental health awareness is encouraging early consultation. Rehabilitation centers are increasingly adopting structured memory recovery programs. Technological advancements in neurotherapy are improving outcomes. Increasing healthcare investments in neurology departments further support growth. Overall, amnesia treatment is gaining traction due to rising neurological trauma cases.

• By Medication

On the basis of medication, the Memory Disorders market is segmented into Drugs, Physical Therapy, Psychotherapy, and Others. The Drugs segment dominated the largest market revenue share of 58.9% in 2025, driven by widespread use of cholinesterase inhibitors and NMDA receptor antagonists for managing dementia symptoms. Increasing prevalence of Alzheimer’s disease significantly boosts drug demand. Strong clinical adoption supports first-line pharmacological treatment. Growing geriatric population increases long-term medication usage. Pharmaceutical advancements are improving drug efficacy and safety. Rising awareness about cognitive disorders enhances early treatment uptake. Expanding healthcare infrastructure supports wider drug accessibility. Insurance coverage in developed regions improves affordability. Continuous R&D in neuropharmacology strengthens treatment options. Hospitals and specialty clinics frequently rely on drug-based management. Increasing patient dependency on long-term therapy supports segment dominance. Overall, drugs remain the leading treatment modality.

The Psychotherapy segment is expected to witness the fastest CAGR of 8.4% from 2026 to 2033, driven by increasing focus on non-pharmacological cognitive interventions. Growing awareness about mental health and cognitive rehabilitation supports adoption. Rising prevalence of early-stage memory disorders boosts demand. Expansion of specialized counseling and neuropsychology services enhances accessibility. Increasing use of cognitive behavioral therapy improves patient outcomes. Integration of digital mental health platforms supports growth. Growing preference for holistic treatment approaches further drives adoption. Rehabilitation centers are expanding psychotherapy offerings. Rising caregiver awareness contributes to early intervention. Technological tools supporting cognitive training enhance effectiveness. Overall, psychotherapy is rapidly gaining importance in comprehensive care.

• By Route of Administration

On the basis of route of administration, the Memory Disorders market is segmented into Oral, Parenteral, and Others. The Oral segment dominated the largest market revenue share of 72.1% in 2025, driven by ease of administration and high patient compliance in long-term therapy. Oral drugs are widely preferred for chronic management of dementia symptoms. Increasing availability of tablet formulations supports accessibility. Physicians commonly prescribe oral medications as first-line treatment. Strong patient preference for non-invasive therapy boosts demand. Expanding retail and hospital pharmacy networks enhance distribution. Rising geriatric population increases continuous drug usage. Improved drug formulations enhance tolerability and effectiveness. Growing awareness of memory disorders supports early treatment initiation. Cost-effectiveness compared to injectable therapies further drives adoption. Healthcare systems favor oral administration for outpatient care. Overall, oral route remains dominant due to convenience and effectiveness.

The Parenteral segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing use in severe neurological cases requiring rapid intervention. Injectable therapies are used in hospital-based acute care settings. Rising hospitalization rates for neurological disorders support demand. Advances in drug delivery systems improve safety and efficacy. Increasing clinical research in neurodegenerative diseases boosts adoption. Growing preference for controlled dosing enhances usage. Expansion of specialty neurology centers supports accessibility. Rising healthcare investments improve treatment infrastructure. Improved patient monitoring enhances therapeutic outcomes. Increasing prevalence of advanced dementia cases contributes to growth. Overall, parenteral route is growing in critical care settings.

• By End-Users

On the basis of end-users, the Memory Disorders market is segmented into Hospitals, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 55.6% in 2025, driven by high patient inflow for diagnosis and treatment of cognitive disorders. Hospitals provide advanced neurological diagnostic facilities. Strong presence of multidisciplinary care teams supports treatment efficiency. Increasing prevalence of Alzheimer’s and dementia boosts hospital visits. Rising healthcare infrastructure investments enhance capacity. Insurance coverage improves affordability of hospital-based care. Availability of specialized neurology departments supports demand. Growing elderly population increases patient admissions. Hospitals also serve as centers for clinical trials. Government initiatives strengthen hospital-based mental healthcare services. Increasing awareness of early diagnosis drives hospital utilization. Overall, hospitals remain the dominant end-user segment.

The Specialty Clinics segment is expected to witness the fastest CAGR of 8.2% from 2026 to 2033, driven by rising demand for focused neurological and memory care services. These clinics provide personalized treatment for cognitive disorders. Increasing awareness about mental health supports growth. Expansion of outpatient neurology services enhances accessibility. Rising preference for specialized care improves adoption. Growing elderly population increases patient pool. Advancements in cognitive rehabilitation programs support outcomes. Increasing availability of trained neurologists drives expansion. Improved healthcare infrastructure in urban areas boosts demand. Integration of digital cognitive therapy tools enhances care delivery. Overall, specialty clinics are emerging as a fast-growing segment.

• By Distribution Channel

On the basis of distribution channel, the Memory Disorders market is segmented into Hospital Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated the largest market revenue share of 52.3% in 2025, driven by high dependency on hospital-based prescriptions for neurological drugs. Hospitals are primary centers for diagnosis and treatment initiation. Strong supply chain systems ensure drug availability. Increasing hospital admissions for dementia care support demand. Physician-led prescribing patterns reinforce usage. Government healthcare programs enhance procurement efficiency. Rising prevalence of neurodegenerative diseases boosts consumption. Insurance coverage improves affordability in hospital settings. Availability of specialized drugs supports hospital pharmacy dominance. Growing number of neurology departments further drives demand. Clinical monitoring requirements strengthen hospital-based dispensing. Overall, hospital pharmacies remain the leading distribution channel.

The Retail Pharmacy segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing accessibility of maintenance therapies. Patients prefer retail pharmacies for convenience and repeat prescriptions. Expanding pharmacy chains improve drug availability. Rising awareness about cognitive health supports demand. Growth in outpatient care boosts retail distribution. Increasing availability of generic drugs enhances affordability. Digital prescription systems support pharmacy access. Expanding elderly population drives consistent medication demand. Improved healthcare infrastructure in emerging markets supports growth. Insurance coverage further encourages retail purchases. Overall, retail pharmacies are rapidly expanding as a key distribution channel.

Memory Disorders Market Regional Analysis

- North America dominated the memory disorders market with the largest revenue share of 40.01% in 2025, driven by strong healthcare infrastructure, high adoption of advanced neurological diagnostics, increased awareness of cognitive health disorders, and rising demand for early detection and monitoring solutions. The region benefits from extensive clinical research activity, strong reimbursement frameworks, and early adoption of innovative therapies and digital health solutions for neurodegenerative conditions

- Patients and healthcare providers in the region are increasingly focused on early screening, continuous cognitive monitoring, and personalized treatment approaches for conditions such as Alzheimer’s disease and dementia

- This widespread adoption is further supported by high healthcare expenditure, a technologically advanced population, and strong integration of digital health platforms into neurology care pathways, establishing North America as a key revenue-generating region in the global Memory Disorders market

U.S. Memory Disorders Market Insight

The U.S. memory disorders market captured the largest revenue share in North America in 2025, driven by rising prevalence of Alzheimer’s disease and other dementia-related conditions, along with strong adoption of advanced diagnostic and therapeutic solutions. The country has a highly developed neuroscience research ecosystem and rapid uptake of biomarker-based diagnostics, neuroimaging technologies, and digital cognitive assessment tools. For instance, healthcare providers in the U.S. are increasingly using AI-assisted cognitive screening platforms and blood-based biomarkers to support earlier and more accurate diagnosis of memory-related disorders. In addition, strong investment from pharmaceutical companies in disease-modifying therapies is further accelerating market growth.

Europe Memory Disorders Market Insight

The Europe memory disorders market is projected to expand at a substantial CAGR during the forecast period, supported by an aging population, increasing prevalence of neurodegenerative diseases, and strong public healthcare systems. For instance, European healthcare programs are increasingly implementing structured dementia screening initiatives to improve early diagnosis and care planning. The region also benefits from strong regulatory support for neurological drug development and expanding access to advanced diagnostic tools across major healthcare systems. Growing emphasis on patient-centered care and early intervention strategies is further supporting market expansion.

U.K. Memory Disorders Market Insight

The U.K. memory disorders market is anticipated to grow at a notable CAGR during the forecast period, driven by rising awareness of dementia, strong National Health Service (NHS) support for cognitive health programs, and increasing adoption of early diagnostic screening initiatives. For instance, memory clinics across the U.K. are expanding services for early detection and management of Alzheimer’s disease. Growing investment in neuroscience research and clinical trials is further contributing to the development of innovative treatment approaches.

Germany Memory Disorders Market Insight

The Germany memory disorders market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong healthcare system, increasing geriatric population, and high focus on neurological research. For instance, German hospitals and research institutions are actively engaged in developing advanced diagnostic imaging and biomarker-based testing for early-stage dementia detection. The country’s emphasis on precision medicine and preventive healthcare is further supporting market growth.

Asia-Pacific Memory Disorders Market Insight

The Asia-Pacific memory disorders market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid population aging, increasing prevalence of neurodegenerative diseases, rising healthcare expenditure, and improving access to neurological care in emerging economies such as China, India, and Japan. For instance, governments in the region are expanding national dementia awareness programs and investing in neurology care infrastructure to improve early diagnosis rates. Expanding clinical research activities and growing adoption of digital health tools for cognitive assessment are further accelerating market growth.

Japan Memory Disorders Market Insight

The Japan memory disorders market is gaining momentum due to its rapidly aging population, advanced healthcare system, and strong focus on dementia care and neurological research. For instance, Japanese healthcare providers are increasingly implementing early cognitive screening programs for elderly populations to improve early intervention outcomes. The country’s emphasis on long-term elderly care and advanced biomedical research is further supporting steady market expansion.

China Memory Disorders Market Insight

The China memory disorders market accounted for the largest revenue share in Asia Pacific in 2025, driven by a rapidly aging population, increasing burden of Alzheimer’s disease, and expanding healthcare infrastructure. For instance, major hospitals in urban centers are increasingly adopting advanced neuroimaging and cognitive diagnostic tools to improve early detection of dementia-related disorders. Strong government initiatives focused on healthy aging, along with rising investment in neuroscience research and healthcare modernization, are further supporting market growth across the country.

Memory Disorders Market Share

The Memory Disorders industry is primarily led by well-established companies, including:

- Biogen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Roche Holding AG (Switzerland)

- Novartis AG (Switzerland)

- AstraZeneca (U.K.)

- AbbVie Inc. (U.S.)

- Merck & Co. (U.S.)

- Bristol Myers Squibb (U.S.)

- Eisai Co., Ltd. (Japan)

- Takeda Pharmaceutical Company (Japan)

- Lundbeck A/S (Denmark)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Sanofi (France)

- GSK plc (U.K.)

- Amgen Inc. (U.S.)

- Teva Pharmaceutical Industries (Israel)

- Sun Pharmaceutical Industries (India)

- H. Lundbeck (Denmark)

Latest Developments in Global Memory Disorders Market

- In June 2021, the U.S. Food and Drug Administration (FDA) granted accelerated approval to Aducanumab (Aduhelm) — a human monoclonal antibody targeting amyloid-beta plaques in the brain for the treatment of Alzheimer’s disease, marking a landmark event in memory disorder therapies after years without disease-modifying approvals

- In January 2023, the FDA approved Lecanemab (Leqembi) for early Alzheimer’s disease, based on clinical trial evidence showing slowed cognitive decline in patients with confirmed amyloid pathology, representing one of the first new disease-modifying treatments in the memory disorders space in decades

- In July 2024, the U.S. FDA approved Kisunla (donanemab-azbt) injection for the treatment of Alzheimer’s disease in adults with mild cognitive impairment or mild dementia, expanding available treatment options for early-stage memory disorder patients

- In January 2025, Eisai Inc. announced FDA approval of LEQEMBI (lecanemab-irmb) IV maintenance dosing for the treatment of early Alzheimer’s disease, with a maintenance regimen intended to prolong treatment benefits and potentially slow disease progression

- In April 2025, the European Commission authorized Eisai-Biogen’s Alzheimer’s drug Leqembi for treatment of early-stage Alzheimer’s disease in the EU, marking the first EU approval of a therapy targeting the underlying cause of Alzheimer’s rather than just symptoms

- In August 2025, the U.S. FDA approved an injectable, at-home weekly subcutaneous version of Leqembi (branded Leqembi IQLIK) as a maintenance therapy option for patients who have completed initial IV treatment, improving accessibility and convenience of ongoing Alzheimer’s therapy

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.