Global Ophthalmic Viscosurgical Devices Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.76 Billion

USD

3.48 Billion

2025

2033

USD

1.76 Billion

USD

3.48 Billion

2025

2033

| 2026 –2033 | |

| USD 1.76 Billion | |

| USD 3.48 Billion | |

| % | |

|

Global Ophthalmic Viscosurgical Devices Market Segmentation, By Type (Dispersive, Cohesive, and Combined), Source (Animal, Biological, and Semi-Synthetic), Application (Cataract Surgery, Vitreoretinal Surgery, Refractive Surgery, and Keratoplasty), End Use (Hospitals, Diagnostic Centers, Eye Specialty Clinics, and Others), - Industry Trends and Forecast to 2033

Ophthalmic Viscosurgical Devices Market Size

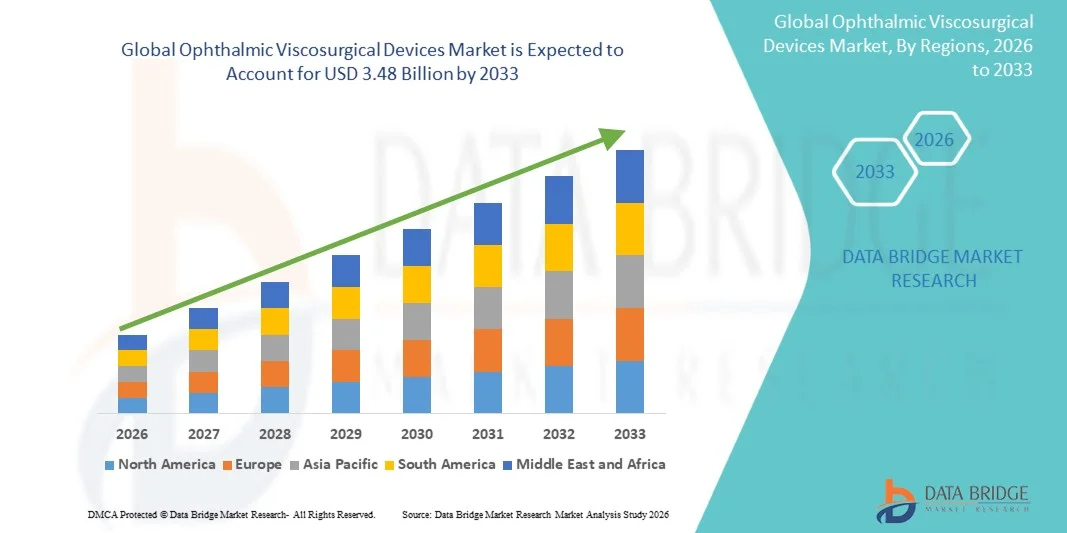

- The global ophthalmic viscosurgical devices market size was valued at USD 1.76 billion in 2025 and is expected to reach USD 3.48 billion by 2033, at a CAGR of 8.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ophthalmic disorders such as cataracts and glaucoma, along with the rising number of ophthalmic surgical procedures worldwide, leading to greater adoption of advanced surgical tools and technologies across hospitals and specialized eye care centers

- Furthermore, growing demand for minimally invasive ophthalmic surgeries, advancements in surgical techniques, and the expanding aging population prone to vision-related disorders are establishing ophthalmic viscosurgical devices as essential components in modern eye surgeries. These converging factors are accelerating the uptake of Ophthalmic Viscosurgical Devices solutions, thereby significantly boosting the industry's growth

Ophthalmic Viscosurgical Devices Market Analysis

- Ophthalmic viscosurgical devices (OVDs), viscoelastic solutions used during ophthalmic surgeries to maintain space, protect intraocular tissues, and facilitate surgical procedures, are increasingly vital components of modern eye surgeries across hospitals and specialized ophthalmology clinics due to their ability to improve surgical precision and patient outcomes

- The escalating demand for ophthalmic viscosurgical devices is primarily fueled by the rising prevalence of cataracts and other vision-related disorders, the growing geriatric population, and the increasing number of ophthalmic surgical procedures performed worldwide

- North America dominated the ophthalmic viscosurgical devices market with the largest revenue share of approximately 41.3% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic surgical technologies, and the strong presence of leading ophthalmic device manufacturers. The U.S. is experiencing substantial growth in ophthalmic viscosurgical device usage across hospitals and specialized eye care centers due to the increasing number of cataract and refractive surgeries

- Asia-Pacific is expected to be the fastest-growing region in the ophthalmic viscosurgical devices market during the forecast period, registering a CAGR of approximately 9.0%, driven by expanding healthcare infrastructure, rising awareness regarding eye health, and the increasing volume of ophthalmic surgeries across countries such as China, India, and Japan

- The Cataract Surgery segment dominated the largest market revenue share of approximately 57.8% in 2025, driven by the high global prevalence of cataracts, particularly among elderly populations

Report Scope and Ophthalmic Viscosurgical Devices Market Segmentation

|

Attributes |

Ophthalmic Viscosurgical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Carl Zeiss Meditec (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ophthalmic Viscosurgical Devices Market Trends

“Increasing Demand for Advanced Ophthalmic Surgical Procedures”

- A significant and accelerating trend in the global ophthalmic viscosurgical devices market is the growing demand for advanced ophthalmic surgical procedures, particularly cataract and glaucoma surgeries, which require specialized surgical materials to protect delicate eye tissues. Ophthalmic viscosurgical devices (OVDs) play a crucial role in maintaining space within the anterior chamber of the eye, protecting corneal endothelial cells, and facilitating precise intraocular procedures

- For instance, companies such as Alcon and Johnson & Johnson Vision offer widely used OVD products including Healon and Healon GV, which are commonly utilized by ophthalmic surgeons during cataract surgeries to maintain intraocular space and protect ocular tissues

- The increasing prevalence of age-related eye disorders such as cataracts, glaucoma, and retinal diseases is significantly driving the need for ophthalmic surgical interventions worldwide. As the global population ages, the number of patients requiring vision correction procedures continues to grow, thereby increasing the demand for OVDs in surgical settings

- Technological advancements in ophthalmic surgery, including micro-incision cataract surgery and improved phacoemulsification techniques, are also contributing to the rising adoption of advanced OVD formulations designed to improve surgical precision and patient outcomes

- Furthermore, the growing number of specialized ophthalmology clinics, ambulatory surgical centers, and advanced eye care hospitals across developed and emerging economies is improving access to vision correction procedures and boosting the demand for ophthalmic viscosurgical devices

- As healthcare systems continue to prioritize vision care and ophthalmic disease management, the demand for high-quality surgical tools and materials such as OVDs is expected to expand steadily in the coming years

Ophthalmic Viscosurgical Devices Market Dynamics

Driver

“Rising Prevalence of Cataracts and Growing Aging Population”

- The increasing prevalence of cataracts and other age-related ophthalmic disorders, combined with the rapid growth of the global aging population, is a major factor driving the expansion of the ophthalmic viscosurgical devices market. Cataract surgery remains one of the most commonly performed surgical procedures worldwide, and OVDs are essential components used during these procedures to protect ocular structures

- For instance, healthcare organizations such as the World Health Organization report that cataracts remain one of the leading causes of vision impairment globally, encouraging hospitals and eye care centers to expand surgical capacity and adopt advanced ophthalmic surgical technologies

- Increasing government initiatives aimed at reducing preventable blindness and improving access to vision care services are also supporting the growth of ophthalmic surgical procedures in both developed and developing regions

- In addition, continuous innovation in OVD formulations, including cohesive and dispersive viscosurgical devices, is improving surgical efficiency and patient safety, further encouraging adoption among ophthalmic surgeons

- The expansion of ophthalmology departments in hospitals and the increasing number of specialized eye care centers worldwide are also contributing to the rising demand for ophthalmic viscosurgical devices in clinical practice

Restraint/Challenge

“High Cost of Ophthalmic Surgical Procedures and Limited Access in Developing Regions”

- Despite increasing demand for ophthalmic surgeries, the high cost associated with advanced eye care procedures and specialized surgical materials can limit the widespread adoption of ophthalmic viscosurgical devices in certain regions. Many healthcare systems in developing countries face financial constraints that restrict access to advanced surgical technologies

- For instance, reports from the International Agency for the Prevention of Blindness highlight that limited access to ophthalmic surgical facilities and trained eye surgeons remains a challenge in several low- and middle-income countries

- In many rural and underserved areas, inadequate healthcare infrastructure and shortages of specialized ophthalmologists can delay or prevent patients from receiving timely surgical treatment for cataracts and other vision disorders

- In addition, the cost of high-quality OVD products and surgical equipment may increase the overall cost of eye surgeries, which can discourage patients from undergoing procedures in regions without adequate healthcare reimbursement systems

- Addressing these challenges will require improved healthcare infrastructure, expanded training programs for ophthalmic surgeons, and increased investment in affordable eye care solutions to ensure broader access to vision-saving surgical procedures worldwide

Ophthalmic Viscosurgical Devices Market Scope

The Ophthalmic Viscosurgical Devices (OVDs) market is segmented on the basis of type, source, application, and end use.

• By Type

On the basis of type, the Ophthalmic Viscosurgical Devices market is segmented into Dispersive, Cohesive, and Combined. The Cohesive segment dominated the largest market revenue share of approximately 44.6% in 2025, driven by its superior ability to maintain anterior chamber stability during ophthalmic surgical procedures. Cohesive OVDs are widely used in cataract and intraocular lens implantation surgeries because they provide excellent space maintenance and can be easily removed from the eye at the end of surgery. Surgeons often prefer cohesive viscoelastic solutions due to their high molecular weight and viscosity, which allow better control during delicate ophthalmic procedures. The growing number of cataract surgeries worldwide, particularly among aging populations, significantly contributes to the dominance of this segment. Hospitals and specialized eye care centers frequently utilize cohesive OVDs to protect ocular tissues and ensure precise surgical outcomes. Technological advancements in viscoelastic formulations have further enhanced the performance and safety of cohesive devices. In addition, increased awareness regarding advanced ophthalmic surgical techniques and improved access to eye care services in developing regions are supporting segment growth. Rising healthcare investments and expanding ophthalmology departments globally further reinforce the segment’s strong market position.

The Combined segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, fueled by its ability to provide the advantages of both dispersive and cohesive viscoelastic properties in a single product. Combined OVDs are increasingly preferred in complex ophthalmic surgeries because they offer improved tissue protection and enhanced surgical efficiency. These devices maintain anterior chamber depth while also protecting sensitive ocular structures such as the corneal endothelium during surgery. The increasing adoption of advanced surgical techniques, including minimally invasive ophthalmic procedures, is driving demand for versatile viscoelastic devices. Technological innovations in dual-viscosity OVD formulations have significantly improved surgical performance and patient outcomes. Ophthalmic surgeons are increasingly adopting combined OVDs due to their ability to simplify surgical steps and improve intraoperative visibility. Growing investments in ophthalmology research and the expansion of specialized eye care centers further support the growth of this segment. In addition, rising awareness about advanced cataract treatment procedures in emerging economies is accelerating the adoption of combined viscoelastic solutions globally.

• By Source

On the basis of source, the Ophthalmic Viscosurgical Devices market is segmented into Animal, Biological, and Semi-Synthetic. The Biological segment dominated the largest market revenue share of approximately 46.2% in 2025, driven by the widespread use of hyaluronic acid–based viscoelastic substances derived from biological sources. These products provide excellent viscoelastic properties, making them highly effective for protecting ocular tissues during surgical procedures. Biological OVDs are commonly used in cataract surgery and intraocular lens implantation because they help maintain the shape of the anterior chamber and reduce surgical complications. Hospitals and specialized ophthalmic clinics frequently adopt these devices due to their proven safety profile and high biocompatibility with human tissues. The rising prevalence of age-related eye disorders such as cataracts and glaucoma is significantly increasing the demand for effective surgical tools, including OVDs. Technological advancements in purification and formulation processes have further enhanced the safety and effectiveness of biologically derived viscoelastic substances. In addition, the growing number of ophthalmic surgeries performed worldwide continues to strengthen demand for biological OVDs. Increasing awareness of eye health and expanding healthcare infrastructure in emerging markets also contribute to segment growth.

The Semi-Synthetic segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, driven by the growing demand for advanced viscoelastic materials with improved stability and performance characteristics. Semi-synthetic OVDs are engineered to provide enhanced viscosity, durability, and consistency during surgical procedures. These materials offer better control during surgery while reducing the risk of postoperative complications. Ophthalmic surgeons are increasingly adopting semi-synthetic viscoelastic devices due to their improved shelf life and predictable clinical performance. Advances in biomaterial engineering have enabled the development of innovative viscoelastic compounds tailored for specific ophthalmic procedures. The increasing adoption of modern surgical technologies and advanced ophthalmic equipment is also supporting the growth of this segment. In addition, expanding research and development activities in biomaterials and ophthalmology are expected to further drive the adoption of semi-synthetic OVDs in the coming years.

• By Application

On the basis of application, the Ophthalmic Viscosurgical Devices market is segmented into Cataract Surgery, Vitreoretinal Surgery, Refractive Surgery, and Keratoplasty. The Cataract Surgery segment dominated the largest market revenue share of approximately 57.8% in 2025, driven by the high global prevalence of cataracts, particularly among elderly populations. Cataract surgery is one of the most commonly performed surgical procedures worldwide, and OVDs play a critical role in maintaining the anterior chamber and protecting intraocular tissues during the operation. Ophthalmic surgeons rely heavily on viscoelastic devices to stabilize the eye during lens removal and intraocular lens implantation. The increasing aging population, particularly in developed and emerging economies, is significantly driving the demand for cataract surgeries. Government initiatives and eye care programs focused on preventing blindness are also supporting the widespread adoption of cataract treatment procedures. Technological advancements in surgical equipment and intraocular lenses have further improved surgical success rates, increasing demand for high-quality viscoelastic devices. In addition, rising healthcare investments and expanding ophthalmology departments in hospitals contribute to strong segment growth.

The Vitreoretinal Surgery segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, fueled by the increasing incidence of retinal disorders such as diabetic retinopathy, retinal detachment, and macular degeneration. Vitreoretinal surgeries are highly delicate procedures that require precise surgical tools and materials to ensure optimal outcomes. OVDs are increasingly used in these procedures to maintain ocular stability and protect delicate retinal tissues during surgery. Advances in vitreoretinal surgical techniques and the development of specialized ophthalmic equipment have improved the effectiveness of these procedures. The rising prevalence of diabetes worldwide has also contributed to an increase in retinal complications, thereby driving demand for vitreoretinal surgeries. Hospitals and specialized eye care centers are increasingly adopting advanced surgical solutions to treat complex retinal disorders. In addition, the expansion of specialized ophthalmic treatment centers and the growing availability of skilled retinal surgeons are expected to support the rapid growth of this segment.

• By End Use

On the basis of end use, the Ophthalmic Viscosurgical Devices market is segmented into Hospitals, Diagnostic Centers, Eye Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of approximately 49.5% in 2025, due to the high volume of ophthalmic surgeries performed in hospital settings. Hospitals are equipped with advanced surgical infrastructure and experienced ophthalmic surgeons capable of performing complex eye procedures. The increasing number of cataract and retinal surgeries worldwide has significantly increased the demand for viscoelastic devices in hospitals. Hospitals also benefit from strong reimbursement frameworks and access to advanced ophthalmic technologies. In addition, hospitals often serve as referral centers for patients requiring specialized eye care procedures. The presence of multidisciplinary medical teams and comprehensive surgical facilities further strengthens the segment’s dominance. Rising healthcare investments and the expansion of hospital infrastructure in emerging economies also contribute to increasing adoption of OVDs in hospital settings.

The Eye Specialty Clinics segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by the increasing number of specialized ophthalmology clinics offering advanced eye care services. These clinics focus exclusively on eye disorders and frequently perform high volumes of cataract and refractive surgeries. Patients increasingly prefer specialty clinics due to shorter waiting times, specialized expertise, and access to advanced ophthalmic technologies. The growing trend toward outpatient surgical procedures also supports the expansion of eye specialty clinics. In addition, increasing investments in private ophthalmology practices and the rising availability of advanced surgical equipment in these facilities are accelerating segment growth. The expansion of specialized eye care networks and rising awareness regarding early diagnosis and treatment of eye diseases further contribute to the rapid adoption of ophthalmic viscosurgical devices in specialty clinics.

Ophthalmic Viscosurgical Devices Market Regional Analysis

- North America dominated the ophthalmic viscosurgical devices market with the largest revenue share of approximately 41.3% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic surgical technologies, and the strong presence of leading ophthalmic device manufacturers

- The market accounted for the majority of this share, experiencing substantial growth in ophthalmic viscosurgical device usage across hospitals and specialized eye care centers due to the increasing number of cataract and refractive surgeries

- Growth is further driven by rising patient awareness regarding eye health, government initiatives to improve ophthalmic care, and continuous investments in modern surgical technologies

U.S. Ophthalmic Viscosurgical Devices Market Insight

The U.S. ophthalmic viscosurgical devices market captured a significant share of the North American market in 2025, fueled by the rapid adoption of advanced surgical techniques and the increasing number of ophthalmic procedures. Hospitals and specialized eye care facilities are actively expanding their usage of these devices to support the growing demand for cataract and refractive surgeries. In addition, the presence of leading ophthalmic device manufacturers and ongoing innovation in surgical technologies continues to strengthen market growth in the country.

Europe Ophthalmic Viscosurgical Devices Market Insight

The Europe ophthalmic viscosurgical devices market is projected to grow steadily over the forecast period, driven by an aging population, increasing prevalence of ocular disorders, and rising healthcare expenditure. Germany and the U.K. are key markets in the region, with hospitals and ophthalmic clinics adopting advanced devices to improve surgical outcomes. Germany’s well-developed healthcare system and emphasis on innovation encourage adoption, while the U.K. benefits from expanding ophthalmic care centers and increased patient awareness regarding modern eye treatments.

U.K. Ophthalmic Viscosurgical Devices Market Insight

The U.K. ophthalmic viscosurgical devices market is expected to grow at a notable CAGR during the forecast period, driven by the increasing number of eye care centers, rising patient demand for advanced cataract and refractive surgeries, and adoption of minimally invasive surgical technologies. The country’s robust healthcare infrastructure and growing awareness of vision health further propel market expansion.

Germany Ophthalmic Viscosurgical Devices Market Insight

Germany’s ophthalmic viscosurgical devices market is anticipated to expand steadily, supported by the country’s strong healthcare infrastructure, emphasis on technological innovation, and growing prevalence of age-related eye disorders. Hospitals and specialized clinics are increasingly adopting advanced devices to enhance surgical precision and patient outcomes, while sustainability and efficiency considerations also contribute to market growth.

Asia-Pacific Ophthalmic Viscosurgical Devices Market Insight

The Asia-Pacific ophthalmic viscosurgical devices market is expected to be the fastest-growing region during the forecast period, registering a CAGR of approximately 9.0%. Growth is driven by expanding healthcare infrastructure, rising awareness of eye health, and increasing volumes of ophthalmic surgeries in countries such as China, India, and Japan. China dominated the Asia-Pacific market in 2025, supported by rapid urbanization, a growing middle class, and high adoption of advanced ophthalmic procedures. India is expected to emerge as the fastest-growing country in the region due to increasing disposable incomes, rising awareness of vision care, expansion of ophthalmic clinics, and growing demand for modern surgical solutions.

Japan Ophthalmic Viscosurgical Devices Market Insight

Japan’s ophthalmic viscosurgical devices market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong emphasis on eye care. Hospitals and specialized eye care centers are increasingly adopting modern surgical devices to improve cataract and refractive surgery outcomes. The market is further supported by high patient awareness and technological innovation in ophthalmic treatments.

China Ophthalmic Viscosurgical Devices Market Insight

China accounted for the largest share of the Asia-Pacific ophthalmic viscosurgical devices market in 2025, driven by rapid urbanization, increasing disposable incomes, and expanding medical facilities. The country has witnessed significant adoption of ophthalmic viscosurgical devices across hospitals, eye clinics, and specialized surgical centers. Strong domestic and international presence of device manufacturers, along with the growing number of ophthalmic procedures, continues to propel market growth in China.

Ophthalmic Viscosurgical Devices Market Share

The Ophthalmic Viscosurgical Devices industry is primarily led by well-established companies, including:

• Carl Zeiss Meditec (Germany)

• Hoya Surgical Optics (Japan)

• Dexter Ophthalmics (U.S.)

• Rayner Intraocular Lenses (U.K.)

• Ophtec BV (Netherlands)

• STAAR Surgical (U.S.)

• Kestrel Surgical (U.S.)

• Eagle Vision (U.S.)

• Geuder AG (Germany)

• Hanita Lenses (Israel)

• MediWorks (China)

• Santen Pharmaceutical (Japan)

• Oculentis GmbH (Germany)

• Essilor Instruments (France)

• PhysIOL (Belgium)

• Microsurgical Technology (U.S.)

• Appasamy Associates (India)

• Toric Lens (China)

Latest Developments in Global Ophthalmic Viscosurgical Devices Market

- In April 2025, Johnson & Johnson Vision presented clinical data supporting advanced cataract surgery technologies and ophthalmic surgical solutions at the American Society of Cataract and Refractive Surgery (ASCRS) meeting. The presentation highlighted innovations designed to improve surgical outcomes and strengthen the company’s ophthalmic surgical portfolio used alongside procedures requiring ophthalmic viscosurgical devices

- In August 2025, Rayner, a global ophthalmic device manufacturer, announced the launch of the RayOne Galaxy and RayOne Galaxy Toric intraocular lenses in Brazil, introducing AI-designed spiral lens technology to improve continuous vision range and reduce visual disturbances after cataract surgery. The launch reflects ongoing technological advancements in ophthalmic surgical ecosystems, including complementary products used with OVDs during procedures

- In December 2024, HOYA Surgical Optics launched VisuPro advanced focus spectacle lenses aimed at addressing early presbyopia and digital eye strain. The lenses utilize binocular harmonization technology to improve near-vision comfort and visual clarity, reflecting broader innovation trends in ophthalmic care and surgical ecosystems connected with cataract and refractive treatment solutions

- In April 2023, Bausch + Lomb, a global eye health company, announced the U.S. launch of StableVisc cohesive ophthalmic viscosurgical device and the TotalVisc Viscoelastic System. These solutions provide surgeons with dual-action protection during cataract surgery by maintaining space in the anterior chamber and protecting ocular tissues. The system combines cohesive and dispersive OVD technologies formulated with sodium hyaluronate and sorbitol to enhance surgical efficiency and patient outcomes

- In April 2021, Bausch + Lomb received U.S. FDA approval for ClearVisc dispersive ophthalmic viscosurgical device, designed to protect the corneal endothelium and improve visualization during ophthalmic surgery. The product contains sorbitol, which helps reduce free-radical damage during procedures such as cataract extraction and intraocular lens implantation, supporting better postoperative outcomes

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.