Global Poliomyelitis Market

Размер рынка в млрд долларов США

CAGR :

%

USD

904.57 Billion

USD

1,339.52 Billion

2025

2033

USD

904.57 Billion

USD

1,339.52 Billion

2025

2033

| 2026 –2033 | |

| USD 904.57 Billion | |

| USD 1,339.52 Billion | |

| % | |

|

Global Poliomyelitis Market Segmentation, By Type (Nonparalytic Polio, Nonparalytic Polio, and Post-Polio Syndrome), Treatment (Medication, Vaccination, Supportive Treatments, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy) - Industry Trends and Forecast to 2033

Poliomyelitis Market Size

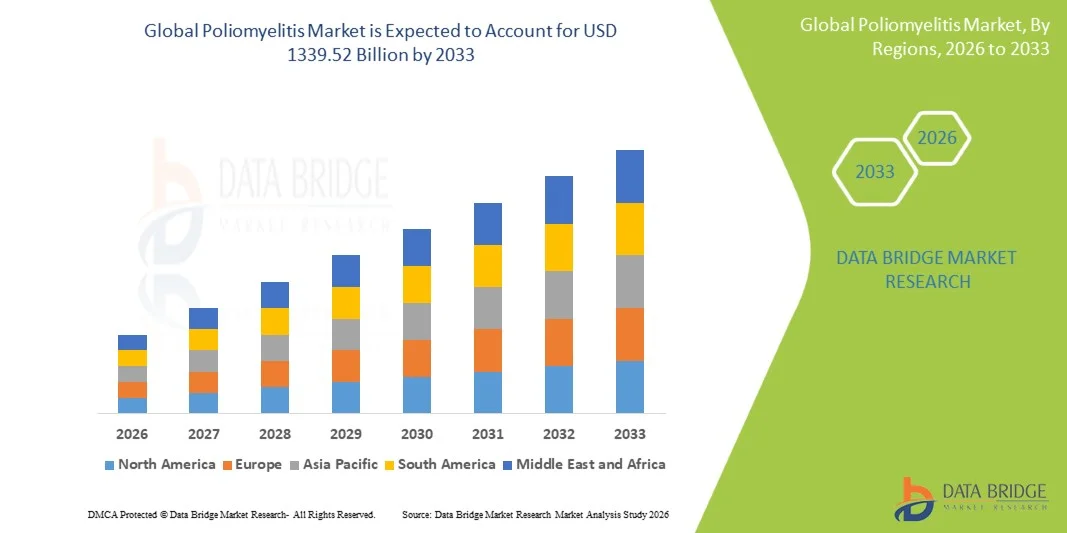

- The global poliomyelitis market size was valued at USD 904.57 billion in 2025 and is expected to reach USD 1339.52 billion by 2033, at a CAGR of 5.03% during the forecast period

- The market growth is largely fueled by the ongoing global efforts toward polio eradication, supported by extensive immunization campaigns and initiatives led by governments and international health organizations, leading to increased adoption of poliomyelitis vaccines across both developed and developing regions

- Furthermore, rising focus on routine and supplementary vaccination programs, along with growing demand for effective and accessible immunization solutions, is establishing poliomyelitis vaccines as a critical component of global public health strategies. These converging factors are accelerating the uptake of poliomyelitis solutions, thereby significantly boosting the industry's growth

Poliomyelitis Market Analysis

- Poliomyelitis, a highly infectious viral disease primarily affecting children, remains a key focus of global immunization and eradication programs due to its potential to cause permanent paralysis and its continued presence in select regions

- The escalating demand for poliomyelitis vaccines is primarily fueled by ongoing eradication initiatives, routine immunization programs, and the need for maintaining high vaccination coverage to prevent disease resurgence

- North America dominated the poliomyelitis market with the largest revenue share of 37.9% in 2025, characterized by strong immunization infrastructure, high awareness levels, and consistent government support, with the U.S. maintaining steady demand through routine vaccination schedules and stockpiling strategies

- Asia-Pacific is expected to be the fastest growing region in the poliomyelitis market during the forecast period due to large population base, increasing healthcare investments, and intensified vaccination drives in countries such as India and Pakistan

- The vaccination segment dominated the largest market revenue share of 61.8% in 2025, driven by global immunization programs led by WHO and national health agencies. Vaccination remains the most effective preventive measure against poliovirus transmission

Report Scope and Poliomyelitis Market Segmentation

|

Attributes |

Poliomyelitis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Poliomyelitis Market Trends

“Strengthening Global Eradication Initiatives and Vaccination Programs”

- A significant and accelerating trend in the global poliomyelitis market is the intensification of global eradication efforts and widespread immunization programs aimed at eliminating Poliomyelitis worldwide

- International collaborations led by organizations such as the World Health Organization and the Global Polio Eradication Initiative are playing a crucial role in reducing the incidence of polio through mass vaccination campaigns

- The increased use of oral polio vaccines (OPV) and inactivated polio vaccines (IPV) in routine immunization schedules has significantly contributed to controlling the spread of the disease

- For instance, large-scale immunization drives in endemic and high-risk regions have led to a substantial decline in global polio cases over the past decades

- In addition, advancements in vaccine formulations, including the development of novel OPV (nOPV), are helping address challenges such as vaccine-derived poliovirus strains

- The growing emphasis on surveillance systems and rapid response strategies is improving early detection and containment of outbreaks

- Increased funding and support from global health organizations and governments are further strengthening eradication initiatives

- This trend toward comprehensive immunization coverage and coordinated global efforts is significantly shaping the growth and direction of the poliomyelitis market

Poliomyelitis Market Dynamics

Driver

“Growing Need Due to Rising Security Concerns and Smart Home Adoption”

- The increasing focus on immunization and the implementation of large-scale public health programs are major drivers of the poliomyelitis market

- Governments across the globe are prioritizing routine vaccination programs to ensure high immunization coverage, particularly among infants and children

- For instance, national immunization campaigns in developing regions continue to play a critical role in preventing the re-emergence of polio cases

- Support from international organizations such as UNICEF is facilitating vaccine distribution and awareness campaigns in underserved areas

- Increasing awareness among populations regarding the importance of vaccination is encouraging higher participation in immunization drives

- The expansion of healthcare infrastructure and outreach programs is improving access to vaccines in remote and rural regions

- Rising government funding and strategic partnerships with non-governmental organizations are further supporting eradication efforts

- The integration of polio vaccination into routine immunization schedules ensures sustained demand for vaccines

- Collectively, these factors are driving continuous growth in the poliomyelitis market globally

Restraint/Challenge

“Vaccine Hesitancy, Accessibility Issues, and Emergence of Vaccine-Derived Strains”

- One of the primary challenges in the poliomyelitis market is vaccine hesitancy in certain regions, driven by misinformation, cultural beliefs, and lack of awareness regarding vaccine safety and efficacy

- In some areas, resistance to vaccination campaigns has hindered efforts to achieve complete immunization coverage

- In addition, logistical challenges such as maintaining cold chain systems and ensuring vaccine delivery in remote or conflict-affected regions limit effective implementation of immunization programs

- The emergence of circulating vaccine-derived poliovirus (cVDPV) in under-immunized populations poses an additional concern for eradication efforts

- For instance, inadequate vaccination coverage can lead to the spread of mutated strains of the virus, requiring intensified immunization responses

- Limited healthcare infrastructure in low-income countries further restricts access to timely vaccination and disease surveillance

- Political instability and geographic barriers in certain endemic regions also complicate eradication initiatives

- Furthermore, funding gaps and dependency on international aid can affect the sustainability of vaccination programs

- Addressing these challenges through strengthened healthcare systems, improved public awareness, and enhanced global coordination will be critical for achieving long-term eradication goals

Poliomyelitis Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

• By Type

On the basis of type, the Poliomyelitis market is segmented into nonparalytic polio, paralytic polio, and post-polio syndrome. The paralytic polio segment dominated the largest market revenue share of 52.4% in 2025, driven by the severe clinical impact of the condition and the high need for intensive medical management. Paralytic polio requires immediate hospitalization and long-term supportive care, increasing its demand for healthcare resources. The dominance of this segment is also supported by higher diagnosis rates in regions with lower immunization coverage. Increasing awareness programs and surveillance activities by global health organizations are further contributing to case identification. In addition, the long-term complications associated with paralysis drive sustained treatment demand. Governments and NGOs focusing on eradication efforts also allocate significant resources to managing paralytic cases.

The post-polio syndrome segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by the rising population of polio survivors experiencing long-term neurological complications. This condition typically appears years after initial infection, leading to progressive muscle weakness and fatigue. Increasing awareness among healthcare professionals and patients is improving diagnosis rates. The growing aging population of polio survivors is a key factor driving demand for long-term care solutions. In addition, advancements in rehabilitative therapies and supportive care are enhancing treatment options. Rising investments in neurological research are also contributing to better disease management strategies. The segment is expected to grow steadily as survival rates improve globally.

• By Treatment

On the basis of treatment, the Poliomyelitis market is segmented into medication, vaccination, supportive treatments, and others. The vaccination segment dominated the largest market revenue share of 61.8% in 2025, driven by global immunization programs led by WHO and national health agencies. Vaccination remains the most effective preventive measure against poliovirus transmission. High coverage of oral polio vaccine (OPV) and inactivated polio vaccine (IPV) has significantly reduced disease incidence worldwide. Strong government funding and mass immunization campaigns continue to support segment dominance. In addition, mandatory childhood vaccination policies in many countries further strengthen demand. Pharmaceutical advancements in vaccine development also contribute to improved efficacy and safety. The global push toward polio eradication continues to sustain high vaccination rates.

The supportive treatment segment is expected to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by increasing need for rehabilitation and long-term patient care. Patients with paralytic polio often require physiotherapy, mobility aids, and respiratory support. Rising awareness about post-infection complications is boosting demand for supportive therapies. In addition, advancements in rehabilitation technologies and assistive devices are improving patient outcomes. Growing healthcare infrastructure in emerging economies is also enhancing access to supportive care. Increased survival rates among polio patients are further contributing to long-term treatment demand. The segment is expected to expand significantly due to chronic disability management needs.

• By Route of Administration

On the basis of route of administration, the Poliomyelitis market is segmented into oral, parenteral, and others. The oral segment dominated the market with a revenue share of 57.6% in 2025, primarily due to the widespread use of oral polio vaccine (OPV) in global immunization programs. OPV is easy to administer, cost-effective, and highly suitable for mass vaccination campaigns. Its ability to induce intestinal immunity makes it highly effective in preventing transmission. Strong adoption in developing countries further supports segment dominance. Government-led vaccination drives and door-to-door immunization campaigns also contribute significantly. The simplicity of oral administration makes it ideal for large-scale public health initiatives.

The parenteral segment is expected to register the fastest CAGR of 8.9% from 2026 to 2033, driven by increasing adoption of inactivated polio vaccine (IPV). IPV provides stronger individual immunity and eliminates risks associated with vaccine-derived poliovirus. Growing preference for safer vaccine formulations is boosting demand for injectable routes. In addition, many developed countries have transitioned fully to IPV-based immunization schedules. Expanding healthcare infrastructure and improved cold-chain systems are supporting adoption. Rising awareness about vaccine safety is further accelerating growth. The segment is expected to grow steadily due to global immunization policy shifts.

• By End-Users

On the basis of end-users, the Poliomyelitis market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with a share of 48.9% in 2025, as hospitals serve as the primary centers for diagnosis, treatment, and vaccination. They provide advanced medical infrastructure and multidisciplinary care for severe polio cases. Hospitals are also essential for managing paralytic patients requiring intensive rehabilitation. Increasing hospital admissions and government healthcare funding further support segment growth. In addition, vaccination drives are often conducted in hospital settings, strengthening their role. Availability of skilled healthcare professionals contributes to improved patient outcomes.

The homecare segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2033, driven by the increasing demand for long-term rehabilitation at home. Patients recovering from polio often require prolonged physiotherapy and supportive care. Homecare services offer convenience, cost-effectiveness, and personalized treatment. Rising adoption of tele-rehabilitation and remote monitoring tools is further boosting growth. In addition, improved access to assistive devices enables better mobility support at home. Growing awareness about chronic disability management is also contributing to demand. The segment is expected to expand as healthcare shifts toward decentralized care models.

• By Distribution Channel

On the basis of distribution channel, the Poliomyelitis market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with a revenue share of 46.7% in 2025, driven by high vaccine distribution and treatment administration within hospital settings. Hospital pharmacies ensure timely availability of vaccines, medications, and supportive care drugs. They play a critical role in immunization programs and outbreak control initiatives. Strong procurement systems and government supply chains further support dominance. In addition, hospitals remain the primary access point for severe case management.

The online pharmacy segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, driven by rapid digitalization of healthcare services. Online pharmacies provide convenient access to medications, supportive treatments, and rehabilitation products. Increasing internet penetration and smartphone usage are key growth drivers. The demand for home delivery services and privacy in healthcare purchases is further boosting adoption. Post-pandemic digital health expansion has accelerated this shift significantly. Improved regulatory frameworks and logistics infrastructure are also supporting growth. The segment is expected to expand strongly with rising consumer preference for digital healthcare solutions.

Poliomyelitis Market Regional Analysis

- North America dominated the poliomyelitis market with the largest revenue share of 37.9% in 2025, characterized by strong immunization infrastructure, high awareness levels, and consistent government support

- The region benefits from well-established vaccination programs, advanced healthcare systems, and efficient disease surveillance mechanisms that ensure high immunization coverage and rapid outbreak response

- In addition, continuous government funding and global health collaborations support long-term eradication efforts. The U.S. plays a key role in maintaining steady vaccine demand through routine immunization schedules and strategic vaccine stockpiling programs

U.S. Poliomyelitis Market Insight

The U.S. poliomyelitis market captured a significant share within North America in 2025, driven by strong adherence to routine immunization schedules and robust public health infrastructure. Demand is supported by continuous vaccination recommendations issued by the Centers for Disease Control and Prevention, ensuring widespread immunization across infants, children, and high-risk populations. The country also maintains strong preparedness through vaccine stockpiling and surveillance systems that help prevent disease resurgence. Public awareness initiatives and healthcare accessibility further strengthen immunization uptake across the population.

Europe Poliomyelitis Market Insight

The Europe poliomyelitis market is projected to grow steadily during the forecast period, supported by strong healthcare systems and coordinated immunization programs across countries. Organizations such as the European Centre for Disease Prevention and Control play a key role in monitoring disease trends and guiding vaccination strategies. Rising awareness regarding infectious disease prevention, along with structured national immunization schedules, is supporting consistent vaccine uptake. In addition, strong regulatory frameworks ensure vaccine safety, availability, and equitable distribution across the region.

U.K. Poliomyelitis Market Insight

The U.K. poliomyelitis market is expected to expand at a steady CAGR during the forecast period, driven by strong national immunization programs and sustained public health awareness. The healthcare system ensures efficient vaccine delivery through structured immunization schedules, particularly for infants and vulnerable groups. Continuous monitoring and public health campaigns support high vaccination coverage and help maintain low disease incidence across the country.

Germany Poliomyelitis Market Insight

The Germany poliomyelitis market is anticipated to grow at a moderate CAGR during the forecast period, supported by high healthcare standards and strong vaccination compliance. Well-established immunization programs, combined with strong public trust in healthcare institutions, ensure consistent vaccine uptake. In addition, Germany’s focus on preventive healthcare and disease control continues to support stable market growth.

Asia-Pacific Poliomyelitis Market Insight

The Asia-Pacific poliomyelitis market is expected to be the fastest-growing region, driven by a large population base, increasing healthcare investments, and intensified vaccination drives in countries such as India and Pakistan. Expanding immunization programs, improving healthcare infrastructure, and rising public awareness are significantly boosting vaccine adoption across the region. Furthermore, international collaborations and government-led eradication initiatives are strengthening immunization coverage in rural and underserved areas.

Japan Poliomyelitis Market Insight

The Japan poliomyelitis market is driven by a highly advanced healthcare system, strong preventive care culture, and high vaccination awareness. Structured immunization programs ensure consistent coverage across the population. In addition, growing focus on adult immunization and an aging population further support stable vaccine demand in the country.

China Poliomyelitis Market Insight

The China poliomyelitis market accounted for a major share in Asia-Pacific in 2025, supported by large-scale immunization programs and strong government initiatives. Rapid urbanization, expanding healthcare access, and increasing awareness of vaccine-preventable diseases are driving consistent vaccine demand. Strong domestic manufacturing capabilities and public health campaigns further strengthen long-term market growth.

Poliomyelitis Market Share

The Poliomyelitis industry is primarily led by well-established companies, including:

- GlaxoSmithKline plc (U.K.)

- Sanofi S.A. (France)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Serum Institute of India Pvt. Ltd. (India)

- Bharat Biotech International Ltd. (India)

- Biological E. Limited (India)

- Panacea Biotec Ltd. (India)

- CSL Limited (Australia)

- Emergent BioSolutions Inc. (U.S.)

- Valneva SE (France)

- Bavarian Nordic A/S (Denmark)

- Sinovac Biotech Ltd. (China)

- Sinopharm Group Co., Ltd. (China)

- Astellas Pharma Inc. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Zydus Lifesciences Ltd. (India)

- Takeda Pharmaceutical Company Limited (Japan)

Latest Developments in Global Poliomyelitis Market

- In July 2022, the global polio eradication effort accelerated research and implementation of novel oral polio vaccine type 2 (nOPV2) to reduce the risk of vaccine-derived poliovirus outbreaks, as this next-generation vaccine is engineered to be more genetically stable than traditional OPVs and less likely to revert to a harmful form

- In March 2024, India continued its national polio immunization strategy by conducting annual National Immunization Days (NIDs) and Sub-National Immunization Days (SNIDs) to maintain high population immunity against poliovirus, reflecting ongoing large-scale vaccination campaigns to prevent outbreaks

- In April 2025, countries participating in the Global Polio Eradication Initiative (GPEI) scaled up the use of novel oral polio vaccine type 2 (nOPV2) to stop variant poliovirus outbreaks safely and quickly, while also exploring new delivery tools such as microneedle patches and needle-free injectors to simplify vaccination

- In July 2025, global surveillance data showed that coverage for the third dose of polio vaccine (POL3) improved to approximately 84% in 2024, up from 83% in 2023, indicating gradual progress in routine immunization reach worldwide

- In August 2025, the World Health Organization reported that Israel discontinued routine use of the bivalent oral polio vaccine (bOPV) in March 2025 but continued administering inactivated polio vaccine (IPV) as part of its immunization schedule, maintaining high immunity levels and monitoring for vaccine-derived poliovirus

- In December 2025, the Ministry of Health and Family Welfare in India conducted targeted polio vaccination drives, appealing to parents and guardians to bring eligible children to polio booths, reinforcing efforts to reach missed children and sustain immunity

- In February 2026, the WHO prequalified an additional novel oral polio vaccine type 2 (nOPV2) product, significantly strengthening the global vaccine supply and outbreak response capacity by enabling broader access to a critical tool for controlling type 2 poliovirus outbreaks

- In March 2026, the WHO’s Polio IHR Emergency Committee reported that wild poliovirus type 1 (WPV1) cases continued in endemic regions (Afghanistan and Pakistan) in 2025, underscoring ongoing challenges in achieving global eradication despite reductions compared to prior years

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.