Global Polyurethane Market

Размер рынка в млрд долларов США

CAGR :

%

USD

78.65 Billion

USD

132.40 Billion

2025

2033

USD

78.65 Billion

USD

132.40 Billion

2025

2033

| 2026 –2033 | |

| USD 78.65 Billion | |

| USD 132.40 Billion | |

| % | |

|

Сегментация мирового рынка полиуретана по типу материала (полиол, MDI, TDI и другие), типу продукции (гибкая пена, жесткая пена, покрытия, клеи и герметики, эластомеры и другие), конечному пользователю (строительство, автомобилестроение и транспорт, постельные принадлежности и мебель, обувь, бытовая техника и другие) — тенденции отрасли и прогноз до 2033 года.

Размер рынка полиуретана

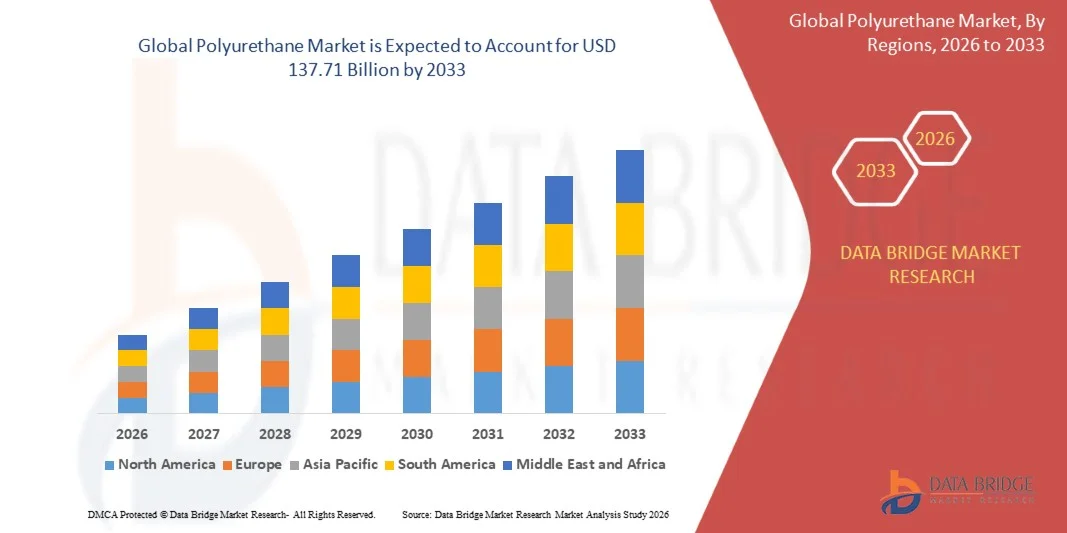

- Объем мирового рынка полиуретана в 2025 году оценивался в 85,11 млрд долларов США и, как ожидается, достигнет 137,71 млрд долларов США к 2033 году , демонстрируя среднегодовой темп роста в 6,2% в течение прогнозируемого периода.

- Рост рынка в значительной степени обусловлен увеличением спроса в строительной, автомобильной, мебельной и текстильной отраслях, где полиуретан предлагает легкие, прочные и энергоэффективные решения. Растущая урбанизация, развитие инфраструктуры и расширение автомобильного сектора ускоряют внедрение полиуретана в теплоизоляцию, элементы интерьера и высокоэффективные материалы.

- Кроме того, растущее внимание к устойчивому развитию, соблюдению экологических норм и энергоэффективности стимулирует использование перерабатываемых полиуретановых изделий с низким уровнем выбросов углерода. Производители все чаще инвестируют в передовые рецептуры, биополиолы и системы, пригодные для вторичной переработки, чтобы соответствовать меняющимся нормативным стандартам и предпочтениям потребителей, что значительно способствует расширению рынка.

Анализ рынка полиуретана

- Полиуретан, включающий в себя гибкие и жесткие пенопласты, покрытия, клеи, эластомеры и герметики, приобретает все большее значение в современном производстве и строительстве благодаря своей универсальности, механической прочности и адаптивности к различным областям применения. Этот материал обеспечивает улучшенную теплоизоляцию, амортизацию, долговечность и химическую стойкость, что делает его незаменимым для энергоэффективных зданий, легких автомобильных деталей и комфортной мебели.

- Растущий спрос на полиуретан в первую очередь обусловлен быстрой индустриализацией, расширением автомобильной и строительной отраслей, а также растущими предпочтениями потребителей в отношении экологически чистых и высокоэффективных материалов. Достижения в химии полиуретанов, инновации в области переработки и биооснованных систем, а также растущее внедрение специализированных составов дополнительно способствуют росту рынка в различных регионах мира.

- Азиатско-Тихоокеанский регион доминировал на рынке полиуретана, занимая 46,76% рынка в 2025 году, благодаря росту строительной активности, увеличению автомобильного производства и росту спроса на мебель и постельные принадлежности.

- Ожидается, что Северная Америка станет самым быстрорастущим регионом на рынке полиуретана в течение прогнозируемого периода благодаря растущему спросу на полиуретан в автомобильной, строительной, мебельной и бытовой технике.

- Сегмент MDI доминировал на рынке с долей 35,40% в 2025 году благодаря широкому применению в производстве жестких пенопластов для изоляции и строительных работ. Полиуретаны на основе MDI предпочтительны благодаря высокой термической стабильности, механической прочности и совместимости с различными добавками, что делает их идеальными для энергоэффективных строительных решений. Развитая цепочка поставок и широкое промышленное внедрение еще больше укрепляют доминирующее положение MDI.

Обзор отчета и сегментация рынка полиуретана

|

Атрибуты |

Ключевые тенденции рынка полиуретана |

|

Охваченные сегменты |

|

|

Охваченные страны |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных, представляющие добавленную стоимость |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Polyurethane Market Trends

“Rising Adoption of Sustainable and Bio-Based Polyurethane Materials”

- A significant trend in the polyurethane market is the increasing shift toward sustainable and bio-based polyurethane materials, driven by growing environmental awareness and stricter regulations on chemical emissions in key industries. These materials are contributing to greener manufacturing processes and reducing dependence on fossil-based feedstocks

- For instance, Covestro supplies bio-based polyurethane systems for automotive and furniture applications, supporting manufacturers in achieving sustainability goals while maintaining performance standards. Such initiatives are encouraging wider adoption of eco-friendly polyurethane solutions

- The construction sector is increasingly incorporating polyurethane-based insulation and coatings due to their energy efficiency, thermal resistance, and durability. This trend is enhancing building sustainability credentials and improving long-term energy management

- Automotive manufacturers are adopting bio-based polyurethane foams and coatings in seating, dashboards, and interior components, where lighter and greener materials help meet fuel efficiency and emissions targets. This is positioning polyurethane as a key material for sustainable vehicle production

- Furniture and bedding industries are integrating eco-friendly polyurethane foams in mattresses and upholstery that meet environmental certifications and consumer demand for sustainable products. This trend is strengthening the market for high-performance, bio-based materials

- The market is witnessing technological innovations in waterborne and solvent-free polyurethane formulations, which reduce VOC emissions and support regulatory compliance. This rising adoption of cleaner chemistries is reinforcing the transition toward environmentally responsible polyurethane applications

Polyurethane Market Dynamics

Driver

“Increasing Demand from Construction, Automotive, and Furniture Industries”

- The growing utilization of polyurethane in insulation, coatings, and high-performance foams is driving demand across construction, automotive, and furniture sectors due to its versatility, lightweight nature, and energy efficiency benefits

- For instance, BASF provides polyurethane solutions for automotive seating and thermal insulation in buildings, enabling manufacturers to improve energy performance while maintaining comfort and safety standards. These applications reinforce polyurethane as an essential material across multiple industries

- The construction industry is expanding its use of polyurethane in spray foams, adhesives, and sealants that enhance thermal insulation, structural strength, and fire resistance. These applications are critical for meeting green building standards and reducing operational energy costs

- Automotive companies are increasingly using polyurethane in interior and exterior components to reduce vehicle weight, improve fuel efficiency, and meet sustainability targets. This trend supports cleaner mobility solutions while maintaining product quality

- The overall growth in infrastructure projects and urbanization globally is driving continuous demand for polyurethane materials that offer energy efficiency, structural performance, and environmental compliance, solidifying its role as a key industrial polymer

Restraint/Challenge

“Volatility in Raw Material Prices and Supply”

- The polyurethane market faces challenges due to fluctuations in the prices of raw materials such as polyols, isocyanates, and additives, which are sensitive to crude oil and chemical feedstock supply dynamics

- For instance, Wanhua Chemical experiences impacts from global MDI (methylene diphenyl diisocyanate) price fluctuations that affect polyurethane production costs and supply chain stability. Such volatility creates planning and budgeting challenges for manufacturers and downstream users

- Global disruptions in petrochemical supply chains, trade restrictions, and energy cost spikes further exacerbate material price instability, affecting profitability and market growth

- The dependence on limited suppliers for specialty polyols and isocyanates increases vulnerability to supply interruptions, impacting timely delivery of polyurethane products to end-use industries

- Manufacturers are compelled to balance cost management with maintaining product quality and performance, which can restrict expansion and investment in innovation. These challenges collectively create pressure on the market to optimize sourcing strategies and mitigate supply risks

Polyurethane Market Scope

The market is segmented on the basis of material type, product type, and end user.

• By Material Type

On the basis of material type, the polyurethane market is segmented into polyol, MDI, TDI, and others. The MDI segment dominated the market with the largest market revenue share of 35.40% in 2025, driven by its extensive use in rigid foam production for insulation and construction applications. MDI-based polyurethanes are preferred due to their high thermal stability, mechanical strength, and compatibility with various additives, making them ideal for energy-efficient building solutions. The established supply chain and wide industrial adoption further reinforce MDI’s dominant position. Manufacturers also favor MDI for producing high-performance coatings, adhesives, and elastomers, boosting overall demand.

The polyol segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for flexible foams in bedding, furniture, and automotive seating applications. Polyol-based polyurethane offers versatility in formulation, allowing customization of hardness, resilience, and comfort. Its growing adoption in lightweight automotive components and eco-friendly furniture materials contributes significantly to market expansion. Increasing consumer preference for comfort-enhancing products and sustainable manufacturing practices is expected to further drive polyol demand.

• By Product Type

On the basis of product type, the polyurethane market is segmented into flexible foam, rigid foam, coating, adhesive and sealants, elastomers, and others. The rigid foam segment held the largest market revenue share in 2025, driven by its use in insulation panels, cold storage, and building envelopes. Rigid polyurethane foams provide excellent thermal insulation, durability, and structural support, making them a preferred choice in residential and commercial construction. In addition, their lightweight nature and energy-saving properties encourage adoption in green building projects. Industries also rely on rigid foam for automotive components and industrial applications, ensuring steady market growth.

The flexible foam segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing use in furniture, bedding, and automotive seating. Flexible polyurethane foams offer superior comfort, cushioning, and durability, making them attractive for end users seeking ergonomic and long-lasting solutions. Growing demand from the automotive sector for lightweight interior components and from the furniture industry for comfort-oriented products further accelerates adoption. Advancements in eco-friendly polyol-based formulations also support market growth.

• By End User

On the basis of end user, the polyurethane market is segmented into building and construction, automotive and transportation, bedding and furniture, footwear, appliances and white goods, and others. The building and construction segment dominated the market in 2025, driven by the extensive use of polyurethane in insulation, roofing, and sealants. Polyurethane materials provide energy efficiency, durability, and reduced maintenance costs, which are highly valued in modern construction. For instance, BASF and Covestro supply advanced polyurethane systems for thermal insulation and facade panels, reinforcing market leadership. Rising construction activities and the shift toward green building standards contribute to sustained demand in this segment.

The automotive and transportation segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for lightweight, fuel-efficient vehicles. Polyurethane is increasingly used in seating, interior panels, and insulation for automotive applications due to its high strength-to-weight ratio and noise-dampening properties. Manufacturers are adopting advanced polyurethanes to meet evolving regulatory standards and improve passenger comfort. The segment benefits from increasing global vehicle production and the adoption of electric vehicles requiring specialized lightweight materials.

Polyurethane Market Regional Analysis

- Asia-Pacific dominated the polyurethane market with the largest revenue share of 46.76% in 2025, driven by growing construction activities, rising automotive production, and increasing demand for furniture and bedding products

- The region’s cost-effective manufacturing landscape, abundant raw material availability, and expanding industrial base are accelerating market growth

- Favorable government policies, rapid urbanization, and increasing adoption of energy-efficient insulation and lightweight automotive components are contributing to higher polyurethane consumption

China Polyurethane Market Insight

China held the largest share in the Asia-Pacific polyurethane market in 2025, owing to its position as a global manufacturing hub for automotive, construction, and furniture industries. The country’s strong industrial infrastructure, supportive policies for chemical and polymer production, and high export potential for polyurethane-based products are major growth drivers. Demand is also fueled by increasing investments in advanced insulation, flexible and rigid foams, and specialty polyurethane systems for domestic and international markets.

India Polyurethane Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rising construction projects, expanding automotive production, and increasing demand for furniture and bedding solutions. Initiatives promoting domestic chemical manufacturing, along with investments in specialty polyurethane production and R&D, are strengthening market growth. In addition, the adoption of energy-efficient building materials and lightweight automotive components is boosting polyurethane consumption.

Europe Polyurethane Market Insight

The Europe polyurethane market is expanding steadily, supported by stringent regulations on energy-efficient buildings, high demand for sustainable and high-performance materials, and growing automotive production. The region emphasizes quality, environmental compliance, and innovative polymer formulations, particularly in coatings, adhesives, and foams. Increasing use of polyurethane in insulation, lightweight components, and eco-friendly furniture enhances market growth.

Germany Polyurethane Market Insight

Germany’s polyurethane market is driven by its strong automotive industry, advanced chemical manufacturing capabilities, and focus on R&D and innovation in high-performance polymers. The country benefits from established networks between academic institutions and chemical producers, fostering development of specialty polyurethane products. Demand is particularly strong for automotive interiors, industrial insulation, and construction applications.

U.K. Polyurethane Market Insight

The U.K. market is supported by a mature construction sector, increasing adoption of lightweight automotive materials, and growing focus on sustainable polymer production. Efforts to localize manufacturing and increase R&D investment in polyurethane-based solutions for insulation, coatings, and adhesives are supporting market expansion. The country continues to emphasize high-quality, high-value polyurethane applications across multiple industries.

North America Polyurethane Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for polyurethane in automotive, construction, furniture, and appliance applications. Rising focus on lightweight materials, energy-efficient building solutions, and high-performance foams is boosting adoption. In addition, reshoring of chemical production and growing collaboration between manufacturers and R&D centers are supporting market growth.

U.S. Polyurethane Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its expansive automotive and construction industries, strong R&D infrastructure, and significant investment in specialty polyurethane production. The country’s emphasis on sustainability, innovation, and regulatory compliance is encouraging the use of advanced polyurethane foams, coatings, and elastomers. Presence of key players and an established distribution network further reinforce the U.S.'s leading position in the region.

Polyurethane Market Share

The polyurethane industry is primarily led by well-established companies, including:

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- INEOS (Switzerland)

- SABIC (Saudi Arabia)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- DuPont (U.S.)

- Royal Dutch Shell plc (the Netherlands)

- Bayer AG (Germany)

- Clariant (Switzerland)

- Huntsman International LLC (U.S.)

- Wanhua Chemical Group Co., Ltd. (China)

- Mitsui Chemicals, Inc. (Japan)

- Lanxess AG (Germany)

- Woodbridge Foam Corporation (Canada)

- Lubrizol Corporation (U.S.)

Latest Developments in Global Polyurethane Market

- In March 2026, BASF announced the commercial launch of its biomass balance polyether polyol product portfolio at its Geismar, Louisiana site, expanding its sustainable raw material offerings across sleep products, automotive, and CASE industries. This development strengthens BASF’s position in the fast-growing sustainable polyurethane segment by enabling manufacturers to reduce carbon footprint, meet rising regulatory and consumer sustainability demands, and access high-performance, eco-friendly formulations for diverse applications. The portfolio also supports increased adoption of renewable raw materials in flexible and rigid foams, coatings, and adhesives

- In March 2026, BASF began local production of Elastollan flame-retardant TPU grades in Shanghai, improving responsiveness to Asia-Pacific market demands for specialized polyurethane solutions. This move enhances the company’s ability to meet stringent safety and performance standards in cable, industrial, and automotive applications, while supporting faster delivery and localized customization. The expansion also positions BASF to capture rising demand for high-performance thermoplastic polyurethanes in emerging economies

- In December 2025, BASF expanded its spray polyurethane foam (SPF) portfolio with WALLTITE RSB, a closed-cell foam incorporating recycled and renewable raw materials to lower product carbon footprint. This innovation addresses growing consumer and regulatory focus on sustainability in building insulation, improves energy efficiency in residential and commercial construction, and offers manufacturers a versatile, eco-friendly alternative to conventional SPF products. The enhanced performance of WALLTITE RSB also strengthens BASF’s competitive edge in high-performance, low-emission insulation solutions

- В октябре 2025 года компания Pearl Group открыла завод Pearl Deutschland в Леверкузене, Германия, в рамках своей инициативы по расширению PearlX2, направленной на удвоение масштабов бизнеса к 2026 году. Этот стратегический шаг укрепляет позиции Pearl на европейском рынке полиуретанов, поддерживает расширение ассортимента специализированной продукции и обеспечивает доступ к передовой производственной инфраструктуре. Он также позволяет ускорить доставку, обеспечить более тесное взаимодействие с клиентами и укрепить партнерские отношения в автомобильном, строительном и промышленном секторах.

- В августе 2025 года компания Rymbal выпустила FluidX — полностью перерабатываемую полиуретановую систему с водорастворимой формулой, которая значительно снижает воздействие на окружающую среду и углеродный след. Продукт отвечает растущему спросу на устойчивые решения в рамках экономики замкнутого цикла для применения в гибких и жестких пенополиуретановых материалах. Благодаря возможности полного восстановления материалов посредством химической и физической переработки, FluidX помогает производителям достигать целей устойчивого развития без ущерба для производительности, упругости или комфорта в производстве постельных принадлежностей, мебели и автомобильной промышленности.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.