Global Seasonal Influenza Market

Размер рынка в млрд долларов США

CAGR :

%

USD

13.47 Billion

USD

57.91 Billion

2025

2033

USD

13.47 Billion

USD

57.91 Billion

2025

2033

| 2026 –2033 | |

| USD 13.47 Billion | |

| USD 57.91 Billion | |

| % | |

|

Global Seasonal Influenza Market Segmentation, By Type (Influenza A Viruses, Influenza B Viruses, Influenza C Virus, Influenza D Viruses, and Others), Treatment (Antiviral, Neuraminidase Inhibitors, Vaccination, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy)- Industry Trends and Forecast to 2033

Seasonal Influenza Market Size

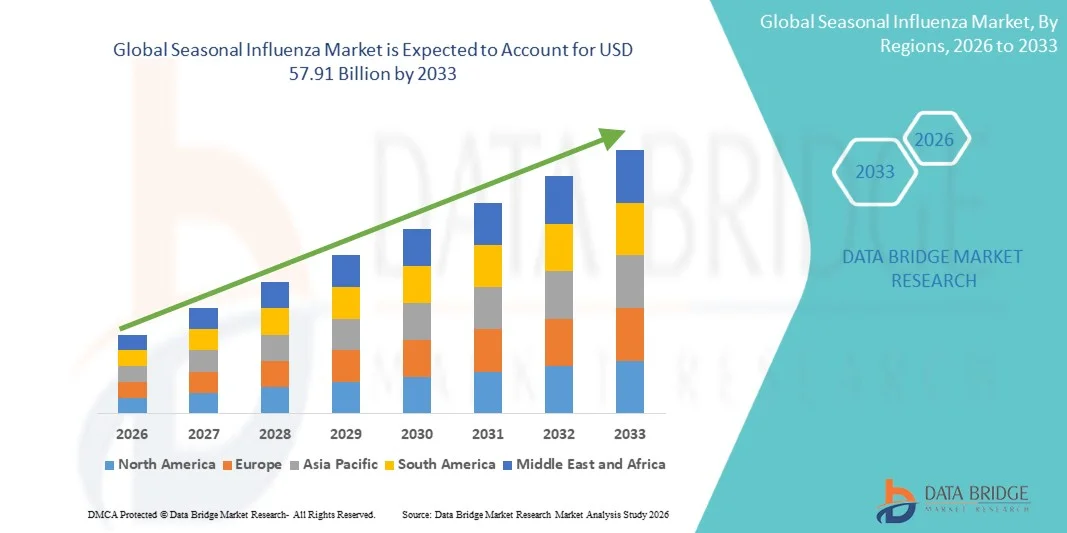

- The global seasonal influenza market size was valued at USD 13.47 billion in 2025 and is expected to reach USD 57.91 billion by 2033, at a CAGR of 20.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of influenza outbreaks, growing awareness regarding annual flu vaccinations, and advancements in vaccine technology, including quadrivalent and cell-based vaccines

- Furthermore, rising government initiatives and immunization programs, along with growing consumer preference for preventive healthcare measures, are driving the adoption of seasonal influenza vaccines. These converging factors are accelerating the uptake of influenza prevention solutions, thereby significantly boosting the industry's growth

Seasonal Influenza Market Analysis

- Seasonal influenza vaccines and treatments, offering preventive and therapeutic protection against influenza viruses, are increasingly vital components of public health strategies in both developed and developing countries due to their effectiveness in reducing infection rates, hospitalizations, and associated healthcare costs

- The escalating demand for seasonal influenza solutions is primarily fueled by increasing awareness of flu-related complications, growing prevalence of respiratory infections, and government-led immunization campaigns promoting annual vaccination and antiviral therapies

- North America dominated the seasonal influenza market with the largest revenue share of 39.4% in 2025, characterized by high vaccination coverage, strong healthcare infrastructure, and a robust presence of leading vaccine and antiviral manufacturers, with the U.S. experiencing substantial uptake driven by innovations in quadrivalent vaccines and neuraminidase inhibitors

- Asia-Pacific is expected to be the fastest growing region in the seasonal influenza market during the forecast period due to expanding healthcare access, rising awareness of preventive healthcare, and increasing adoption of influenza immunization and antiviral programs in countries such as China and India

- Influenza A viruses segment dominated the market segment with a share of 52.3% in 2025, driven by their higher prevalence and associated complications

Report Scope and Seasonal Influenza Market Segmentation

|

Attributes |

Seasonal Influenza Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Seasonal Influenza Market Trends

“Advancements in Vaccine Technology and mRNA Integration”

- A significant and accelerating trend in the global seasonal influenza market is the development and adoption of next-generation vaccines, including mRNA-based and quadrivalent formulations, enhancing both efficacy and coverage

- For instance, Moderna and Pfizer have introduced updated mRNA flu vaccines that target multiple influenza strains, allowing faster production and improved immune response in diverse populations

- mRNA integration enables rapid adaptation to emerging influenza strains, providing higher protection rates and reducing seasonal outbreak severity. For instance, clinical trials of these vaccines demonstrate stronger antibody responses compared to traditional egg-based vaccines

- The seamless incorporation of advanced vaccine technology into public immunization programs facilitates broader coverage and timely protection for high-risk groups such as the elderly, children, and immunocompromised individuals

- This trend towards more effective and rapidly adaptable influenza vaccines is fundamentally reshaping expectations for seasonal flu prevention, driving pharmaceutical companies such as Seqirus and Sanofi to invest in next-generation formulations

- The demand for innovative and highly effective influenza vaccines is growing rapidly across both developed and emerging markets, as governments and healthcare providers increasingly prioritize preventive healthcare and pandemic preparedness

- Collaborative research partnerships between biotech companies and public health agencies are accelerating the development of universal influenza vaccines, aiming for long-term protection across multiple flu seasons

Seasonal Influenza Market Dynamics

Driver

“Increasing Government Initiatives and Preventive Healthcare Awareness”

- The growing emphasis on preventive healthcare and widespread government vaccination campaigns is a significant driver for the heightened demand for seasonal influenza vaccines and antiviral treatments

- For instance, in October 2025, the U.S. CDC expanded its seasonal influenza vaccination guidelines, encouraging broader coverage among adults and children, which is expected to drive market growth

- As populations become more aware of flu-related complications and potential hospitalizations, vaccines and antiviral treatments offer an essential preventive strategy, particularly for high-risk groups

- Furthermore, rising healthcare budgets and public health initiatives promoting annual immunization are making influenza prevention a central component of national health strategies

- The convenience of widespread vaccination programs, coupled with improved accessibility to vaccines in pharmacies and clinics, is propelling the adoption of influenza prevention solutions across diverse demographics

- Expansion of employer-sponsored flu vaccination programs is further increasing uptake, particularly in corporate and industrial sectors, reducing absenteeism and improving workforce health

- Growing investment in advanced vaccine technologies, such as high-dose and adjuvanted formulations, is enabling better protection for vulnerable populations and boosting overall market adoption

Restraint/Challenge

“Vaccine Hesitancy and Supply Chain Constraints”

- Concerns surrounding vaccine safety, efficacy, and potential side effects pose a significant challenge to broader market penetration, as hesitant populations may delay or avoid annual immunization

- For instance, reports of mild adverse reactions to influenza vaccines have contributed to public skepticism, impacting uptake rates in certain regions despite proven benefits

- Addressing hesitancy through awareness campaigns, transparent communication, and healthcare provider education is crucial for building trust and improving vaccination coverage

- In addition, supply chain disruptions, cold-chain requirements, and production limitations can constrain timely distribution of vaccines, particularly in emerging markets or during peak influenza seasons

- Overcoming these challenges through enhanced public education, robust logistics, and diversified vaccine manufacturing will be vital for sustained growth in the global seasonal influenza market

- Limited public funding in certain regions may restrict the availability of vaccines, creating accessibility gaps for lower-income populations

- Regulatory approval delays for new vaccine formulations can slow market entry, impacting the timely adoption of innovative influenza prevention solutions

Seasonal Influenza Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the seasonal influenza market is segmented into Influenza A viruses, Influenza B viruses, Influenza C virus, Influenza D viruses, and others. The Influenza A viruses segment dominated the market with the largest revenue share of 52.3% in 2025, driven by their higher prevalence, frequent mutations, and significant contribution to seasonal flu outbreaks worldwide. Influenza A strains are associated with more severe illness and hospitalizations, prompting greater demand for vaccines and antivirals targeting these strains. Public health authorities often prioritize vaccination against Influenza A due to its potential for pandemics, further boosting market adoption. Vaccine manufacturers focus on developing quadrivalent formulations to cover multiple Influenza A strains, increasing the segment’s reach. The segment also benefits from widespread awareness campaigns emphasizing protection against highly transmissible Influenza A viruses. Furthermore, healthcare providers actively recommend vaccination for high-risk populations, including the elderly, children, and immunocompromised individuals.

The Influenza B viruses segment is anticipated to witness the fastest growth rate during the forecast period due to increasing awareness of its contribution to seasonal influenza, especially among pediatric and adolescent populations. Influenza B infections, while generally less severe than Influenza A, can still cause complications, driving the need for targeted vaccines. Rising inclusion of Influenza B strains in quadrivalent vaccines enhances preventive coverage. The segment is further supported by government initiatives to expand immunization among school-aged children. Improved diagnostics for differentiating Influenza B from other strains are also boosting early treatment and prevention. Manufacturers are investing in broader-spectrum vaccines to address both Influenza A and B strains simultaneously.

- By Treatment

On the basis of treatment, the seasonal influenza market is segmented into antiviral, neuraminidase inhibitors, vaccination, and others. The vaccination segment dominated the market with a revenue share of 48.6% in 2025, driven by government-led immunization programs and growing awareness of preventive healthcare benefits. Vaccines remain the most effective tool for reducing influenza infections, hospitalizations, and mortality rates. Seasonal flu vaccination campaigns, supported by public and private healthcare providers, reinforce adoption. Continuous advancements, including mRNA and quadrivalent vaccines, enhance efficacy and broaden protection against multiple strains. Vaccination uptake is also encouraged through workplace programs and pharmacy-based immunization services. The segment benefits from high trust and acceptance among consumers due to proven safety and efficacy.

The antiviral segment is expected to witness the fastest growth rate during the forecast period due to increasing demand for early intervention treatments to reduce influenza severity and hospitalization. Antivirals, including neuraminidase inhibitors, are recommended for high-risk patients and those who cannot receive vaccines. Growing prevalence of influenza-related complications, especially among the elderly and immunocompromised, drives market expansion. Healthcare providers are increasingly prescribing antiviral treatments alongside vaccination campaigns. Advancements in oral and parenteral antiviral formulations enhance convenience and patient compliance. Furthermore, government stockpiling of antiviral drugs in preparation for seasonal outbreaks and potential pandemics supports market growth.

- By Route of Administration

On the basis of route of administration, the seasonal influenza market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with the largest share in 2025, driven by the widespread use of injectable vaccines for seasonal influenza. Parenteral administration ensures precise dosage, high immunogenicity, and strong protection, particularly for high-risk populations. Healthcare providers prefer parenteral vaccines in clinical settings for efficacy and safety monitoring. Mass vaccination programs and campaigns in schools, hospitals, and public centers support widespread adoption. Parenteral vaccines are often integrated with multivalent formulations covering both Influenza A and B strains. The segment’s dominance is also supported by strong regulatory backing and established cold-chain logistics ensuring vaccine stability.

The oral segment is anticipated to witness the fastest growth during the forecast period due to increasing research in oral vaccine formulations offering easier administration and improved patient compliance. Oral vaccines reduce the need for healthcare personnel to administer injections, making them suitable for large-scale immunization programs. They are particularly advantageous for pediatric and needle-phobic populations. Growing investment in novel delivery technologies, such as live-attenuated oral vaccines, is boosting adoption. Oral vaccines facilitate faster and more cost-effective distribution in emerging markets. Consumer preference for non-invasive vaccine options further drives the segment’s growth trajectory.

- By End-Users

On the basis of end-users, the seasonal influenza market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market in 2025 due to the centralized administration of vaccines, treatment of high-risk patients, and management of influenza outbreaks. Hospitals provide access to both vaccination and antiviral treatments, ensuring proper dosage and monitoring. They are also primary centers for awareness campaigns targeting patients and caregivers. The segment benefits from government and private health insurance coverage supporting influenza treatment. Hospitals are crucial for implementing large-scale immunization programs during peak flu seasons. Clinical staff are trained to provide both preventive and therapeutic influenza care efficiently.

The homecare segment is expected to witness the fastest growth rate during the forecast period due to the rising trend of in-home vaccination services, telemedicine consultations, and home-based antiviral administration. Homecare services provide convenience, reduce hospital congestion, and improve compliance among elderly or mobility-challenged patients. Mobile vaccination units and nurse-led homecare programs are expanding access in urban and rural areas. The COVID-19 pandemic accelerated the adoption of home-based healthcare delivery, including influenza prevention. Increased investment in homecare infrastructure and services further supports growth. Patient preference for personalized, at-home care options enhances adoption of home-based influenza solutions.

- By Distribution Channel

On the basis of distribution channel, the seasonal influenza market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market in 2025 due to direct access to vaccines, antivirals, and other influenza treatments within healthcare facilities. Hospital pharmacies ensure timely administration, proper storage, and adherence to dosing protocols. They are critical for high-risk patient groups requiring immediate treatment. Partnerships between vaccine manufacturers and hospital pharmacies support mass immunization programs. The segment benefits from insurance reimbursement policies facilitating patient access. Hospitals also monitor adverse reactions and provide follow-up care, increasing trust in the distribution channel.

The online pharmacy segment is anticipated to witness the fastest growth during the forecast period due to increasing consumer preference for convenient, contactless procurement of vaccines and antiviral medications. Online pharmacies provide doorstep delivery and improved accessibility for remote populations. Digital health platforms and mobile apps enhance awareness, ordering, and tracking of influenza medications. Rising e-commerce penetration and telemedicine integration drive online pharmacy adoption. Consumers increasingly rely on online services for preventive healthcare, including influenza management. Innovative digital marketing and subscription-based services further accelerate market growth in this segment.

Seasonal Influenza Market Regional Analysis

- North America dominated the seasonal influenza market with the largest revenue share of 39.4% in 2025, characterized by high vaccination coverage, strong healthcare infrastructure, and a robust presence of leading vaccine and antiviral manufacturers

- Consumers in the region prioritize annual flu vaccinations and antiviral treatments due to their proven effectiveness in reducing influenza-related hospitalizations and complications, particularly among high-risk populations

- This widespread adoption is further supported by government initiatives, employer-sponsored vaccination programs, and high healthcare spending, establishing influenza vaccines and treatments as the primary preventive solution for both adults and children

U.S. Seasonal Influenza Market Insight

The U.S. seasonal influenza market captured the largest revenue share of 42% in 2025 within North America, fueled by extensive vaccination programs, high public awareness of flu prevention, and well-established antiviral distribution channels. Consumers increasingly prioritize annual flu vaccination and preventive treatments to reduce hospitalization risks and influenza-related complications, particularly among high-risk groups such as the elderly, children, and immunocompromised individuals. The growing adoption of next-generation vaccines, including mRNA and quadrivalent formulations, alongside employer-sponsored vaccination initiatives, further propels the market. Moreover, government campaigns, school immunization programs, and widespread healthcare infrastructure significantly contribute to the market’s expansion. The rising use of digital health platforms for vaccine scheduling, reminders, and monitoring also enhances accessibility and patient compliance.

Europe Seasonal Influenza Market Insight

The Europe seasonal influenza market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong government immunization policies, growing public awareness of flu prevention, and healthcare infrastructure that supports widespread vaccination. Rising urbanization and an aging population are fostering greater vaccine adoption among high-risk groups, while increasing incidence of seasonal flu outbreaks further emphasizes preventive care. European consumers are increasingly valuing preventive healthcare solutions, leading to higher acceptance of both vaccines and antiviral treatments. Integration of influenza prevention programs across hospitals, specialty clinics, and pharmacies is boosting market penetration. Collaborative efforts between public health authorities and pharmaceutical companies to provide quadrivalent and cell-based vaccines are also supporting market growth.

U.K. Seasonal Influenza Market Insight

The U.K. seasonal influenza market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by government-led vaccination programs, rising awareness of influenza complications, and seasonal outbreak preparedness. Concerns regarding public health and healthcare system burden are encouraging higher adoption of vaccines and antiviral treatments across both pediatric and adult populations. The U.K.’s robust healthcare infrastructure, coupled with growing digital health initiatives such as online vaccination scheduling and telemedicine consultations, is expected to continue stimulating market growth. In addition, the introduction of high-efficacy vaccines and combination formulations ensures broader coverage, further supporting adoption.

Germany Seasonal Influenza Market Insight

The Germany seasonal influenza market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing public awareness of flu-related risks and strong government support for preventive healthcare. Germany’s advanced healthcare system, widespread immunization programs, and emphasis on early intervention promote high vaccine and antiviral uptake. Hospitals, specialty clinics, and corporate healthcare programs are actively implementing influenza prevention strategies, while consumers increasingly prefer high-efficacy vaccines, including quadrivalent and cell-based options, in line with regulatory recommendations. The market is also supported by educational campaigns highlighting the benefits of vaccination in reducing influenza complications and hospitalizations.

Asia-Pacific Seasonal Influenza Market Insight

The Asia-Pacific seasonal influenza market is poised to grow at the fastest CAGR of 26% during the forecast period of 2026 to 2033, driven by increasing awareness of flu-related health risks, expanding government vaccination campaigns, and improving healthcare access in countries such as China, Japan, and India. The region’s growing focus on preventive healthcare, coupled with digital health platforms and telemedicine initiatives, is driving widespread vaccine adoption. Improved cold-chain infrastructure, local manufacturing capacities, and affordable vaccine options are enhancing accessibility in both urban and rural populations. Partnerships between public health agencies and private pharmaceutical companies are further strengthening distribution and coverage. Rising adoption of quadrivalent and next-generation vaccines also supports market growth by offering broader protection against circulating influenza strains.

Japan Seasonal Influenza Market Insight

The Japan seasonal influenza market is gaining momentum due to the country’s high health awareness, aging population, and strong emphasis on preventive care. Vaccination campaigns targeting both children and the elderly drive high adoption rates, supported by school-based and workplace immunization programs. The integration of influenza vaccines with digital health tools such as online scheduling, reminders, and telemedicine consultations is further enhancing accessibility and compliance. Advancements in high-efficacy vaccines, including quadrivalent and mRNA formulations, are increasing public confidence and coverage. The growing number of smart hospitals and connected healthcare systems is also enabling more efficient vaccine administration, driving growth across both residential and corporate sectors.

India Seasonal Influenza Market Insight

The India seasonal influenza market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising government initiatives, increasing public health awareness, and expanding healthcare infrastructure. India’s growing middle class, urbanization, and increasing disposable incomes are driving demand for influenza vaccines and antiviral treatments across hospitals, specialty clinics, and retail pharmacies. Affordable vaccine options and strengthening local manufacturing capabilities are improving accessibility in both urban and rural regions. National immunization programs, public health campaigns, and corporate vaccination initiatives are key factors propelling market growth. In addition, the increasing focus on preventive healthcare and pandemic preparedness is encouraging higher adoption of vaccines and antivirals throughout the country.

Seasonal Influenza Market Share

The Seasonal Influenza industry is primarily led by well-established companies, including:

- GSK plc (U.K.)

- CSL Seqirus (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Moderna, Inc. (U.S.)

- AstraZeneca (U.K.)

- Abbott (U.S.)

- Sinovac Biotech Ltd. (China)

- Novavax, Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- BioNTech SE (Germany)

- Sanofi (France)

- Hualan Biological Engineering Inc. (China)

- Shanghai Institute of Biological Products Co., Ltd. (China)

- Gamma Vaccines Pty Ltd. (Australia)

- Altimmune, Inc. (U.S.)

- FluGen, Inc. (U.S.)

- VaxInnate Corporation (U.S.)

What are the Recent Developments in Global Seasonal Influenza Market?

- In February 2026, WHO published an assessment highlighting that next‑generation influenza vaccines with broader, longer‑lasting protection could save millions of lives, providing strategic guidance for investment and policy to support improved seasonal influenza vaccination programs globally

- In July 2025, GSK began shipping doses of its seasonal influenza vaccines FLULAVAL and FLUARIX for the 2025‑26 U.S. flu season after receiving FDA lot release approval, ensuring early supply to healthcare providers and pharmacies ahead of the flu season

- In March 2025, the World Health Organization (WHO) announced recommendations for the influenza vaccine composition for the 2026 southern hemisphere influenza season, guiding manufacturers on updated viral strains to include a key annual part of ensuring vaccine effectiveness worldwide

- In September 2024, the U.S. FDA approved FluMist (live attenuated nasal spray influenza vaccine) for self‑ or caregiver administration, making it the first flu vaccine not requiring healthcare provider administration, increasing convenience and access for patients aged 2–49 years

- In October 2021, Seqirus received expanded U.S. FDA approval for its FLUCELVAX® QUADRIVALENT cell‑based seasonal influenza vaccine, allowing use in children as young as six months marking broader protection across age groups and representing a shift toward cell‑based technologies in flu vaccine production

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.