Global Software Defined Data Center Market

Размер рынка в млрд долларов США

CAGR :

%

USD

88.43 Billion

USD

420.00 Billion

2025

2033

USD

88.43 Billion

USD

420.00 Billion

2025

2033

| 2026 –2033 | |

| USD 88.43 Billion | |

| USD 420.00 Billion | |

| % | |

|

Global Software-Defined Data Center Market Segmentation, By Component (Hardware, Software, and Services), Type (Software-Defined Computing (SDC), Software-Defined Storage (SDS), Software-Defined Data Center Networking (SDDCN), and Automation and Orchestration), Organization Size (Large Enterprises and Small and Medium-sized Enterprises (SMEs)), Vertical (BFSI, IT and Telecom, Government and Defense, Healthcare, Education, Retail, Manufacturing, and Others) - Industry Trends and Forecast to 2033

Software-Defined Data Center Market Size

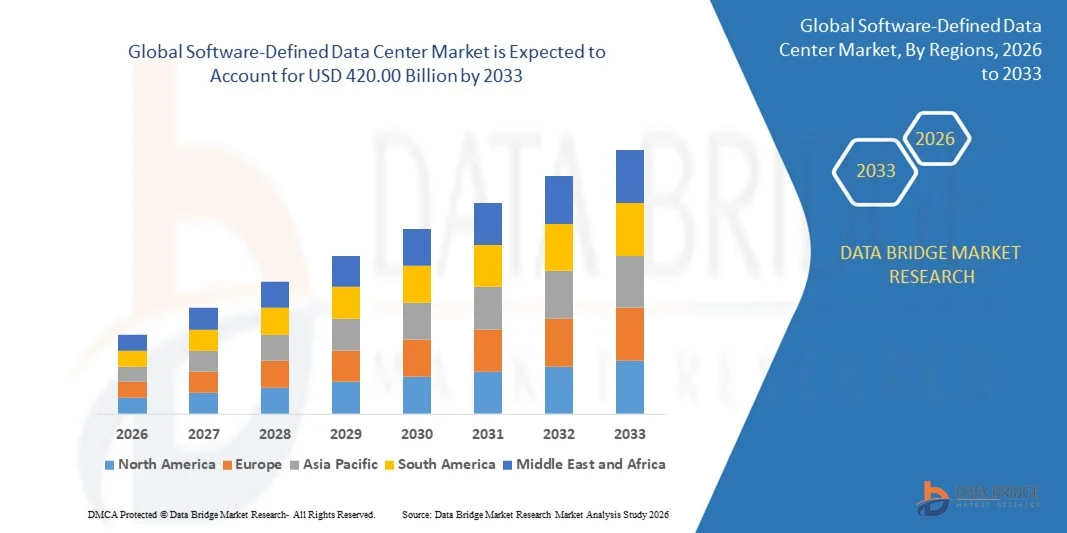

- The global software-defined data center market size was valued at USD 88.43 billion in 2025 and is expected to reach USD 420.00 billion by 2033, at a CAGR of 21.50% during the forecast period

- The market growth is largely fueled by the increasing adoption of cloud computing, virtualization, and hybrid IT infrastructures across enterprises, leading to higher demand for flexible, scalable, and automated data center operations

- Furthermore, rising enterprise requirements for centralized management, improved resource utilization, and enhanced security are establishing software-defined data center solutions as the preferred choice for modern IT infrastructure. These converging factors are accelerating the deployment of SDDC technologies, thereby significantly boosting the market's growth

Software-Defined Data Center Market Analysis

- Software-defined data centers, offering virtualized compute, storage, and networking resources managed through software-based orchestration, are becoming essential for modern enterprises to optimize performance, reduce costs, and improve operational agility

- The escalating demand for SDDC solutions is primarily driven by the need for automation, workload mobility, hybrid cloud integration, and advanced analytics, as enterprises seek efficient and scalable IT infrastructure to support digital transformation initiatives

- North America dominated the software-defined data center market with a share of 40.7% in 2025, due to increasing adoption of virtualization, cloud computing, and hybrid IT infrastructure across enterprises

- Asia-Pacific is expected to be the fastest growing region in the software-defined data center market during the forecast period due to rapid digitalization, increasing enterprise IT investments, and the rise of cloud-first strategies in countries such as China, Japan, and India

- Software segment dominated the market with a market share of 75.36% in 2025, due to the critical role of virtualization, management, and orchestration software in optimizing data center operations. Enterprises increasingly rely on software solutions for workload automation, resource allocation, and centralized management across hybrid environments

Report Scope and Software-Defined Data Center Market Segmentation

|

Attributes |

Software-Defined Data Center Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Software-Defined Data Center Market Trends

Adoption of Hybrid and Multi-Cloud Architectures

- A significant trend in the software-defined data center (SDDC) market is the increasing adoption of hybrid and multi-cloud architectures, driven by the rising need for flexible, scalable, and resilient IT infrastructures across enterprises. This adoption allows organizations to balance workloads between on-premises and public cloud environments while optimizing cost, performance, and security

- For instance, VMware provides VMware Cloud Foundation solutions that enable enterprises to seamlessly integrate private and public clouds, offering consistent infrastructure management and workload mobility. These offerings accelerate digital transformation initiatives and improve operational agility across multi-cloud environments

- Enterprises are increasingly implementing SDDCs to achieve centralized management of virtualized compute, storage, and network resources, reducing dependence on physical hardware and manual operations. This shift enhances efficiency and enables dynamic resource allocation to meet evolving business demands

- The demand for automated provisioning and orchestration of IT resources is growing as organizations seek to improve operational efficiency, minimize downtime, and reduce human error. SDDC platforms provide unified dashboards and automation tools that streamline management across complex IT ecosystems

- Security and compliance considerations are influencing SDDC adoption, as hybrid and multi-cloud deployments require integrated monitoring, policy enforcement, and threat detection capabilities. These capabilities help maintain data integrity and regulatory compliance while supporting rapid application deployment

- The market is witnessing increased interest in edge computing integration within SDDC frameworks to support latency-sensitive workloads and real-time analytics. This trend is reinforcing the role of software-defined infrastructure as a foundation for agile, scalable, and secure enterprise IT architectures

Software-Defined Data Center Market Dynamics

Driver

Rising Demand for Automated, Centralized Data Center Management

- The growing complexity of enterprise IT environments is driving demand for automated and centralized data center management solutions that provide visibility, control, and orchestration across virtualized and hybrid infrastructures. These solutions reduce operational costs and improve service delivery across distributed workloads

- For instance, Nutanix provides enterprise cloud platforms that enable automated infrastructure management, resource optimization, and unified monitoring across multi-cloud deployments. Organizations leveraging Nutanix platforms experience reduced administrative overhead and faster time-to-service for critical applications

- The shift toward software-defined networking and storage is enhancing the capability of data centers to dynamically allocate resources based on workload requirements, supporting operational efficiency and business agility

- Cloud-native applications and containerized workloads are increasing the need for centralized orchestration platforms that can provision resources automatically and enforce policies consistently across diverse environments

- The growing adoption of AI and machine learning in IT operations is boosting the deployment of software-defined management tools that provide predictive analytics, anomaly detection, and intelligent optimization for data center performance

Restraint/Challenge

Complexity of Integrating with Legacy Systems

- The software-defined data center market faces challenges due to the difficulty of integrating SDDC platforms with existing legacy systems, which often involve heterogeneous hardware, proprietary protocols, and outdated management frameworks. This complexity can slow adoption and increase implementation costs

- For instance, organizations migrating from traditional data centers to HPE GreenLake SDDC solutions often encounter integration challenges with legacy storage arrays and network infrastructure. These challenges require additional planning, testing, and customization to ensure seamless operation

- Ensuring compatibility with existing applications and workflows requires careful orchestration and may necessitate re-architecting of certain services, increasing deployment time and resource requirements

- Legacy systems may lack APIs or automation capabilities, limiting the ability of SDDC platforms to provide fully automated, centralized management across all resources

- The market continues to navigate constraints related to balancing modernization with operational continuity, as organizations aim to adopt advanced software-defined solutions while maintaining service availability and minimizing disruption to existing IT operations

Software-Defined Data Center Market Scope

The market is segmented on the basis of component, type, organization size, and vertical.

- By Component

On the basis of component, the SDDC market is segmented into hardware, software, and services. The software segment dominated the market with the largest revenue share of 75.36% in 2025, driven by the critical role of virtualization, management, and orchestration software in optimizing data center operations. Enterprises increasingly rely on software solutions for workload automation, resource allocation, and centralized management across hybrid environments. Software offerings often provide integration with cloud platforms and advanced analytics, enhancing operational efficiency and reducing total cost of ownership. The strong demand for software solutions is supported by their ability to enable scalable, flexible, and secure data center operations.

The services segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising demand for deployment, consulting, and managed services. For instance, companies such as IBM offer professional services that assist organizations in implementing SDDC solutions while ensuring minimal disruption. Services also provide ongoing monitoring, support, and optimization, making them attractive for enterprises that require expert guidance in managing complex software-defined environments. The increasing shift toward outsourced IT management and cloud integration further accelerates service adoption.

- By Type

On the basis of type, the SDDC market is segmented into Software-Defined Computing (SDC), Software-Defined Storage (SDS), Software-Defined Data Center Networking (SDDCN), and Automation and Orchestration. The Software-Defined Computing segment dominated the market in 2025, driven by the widespread adoption of virtualized compute resources and the need for efficient workload management. Organizations prioritize SDC solutions for their ability to optimize server utilization, improve scalability, and reduce hardware dependency. SDC also supports dynamic provisioning and integration with other SDDC components, enhancing operational flexibility and performance. Its established presence in enterprise IT infrastructure contributes to its dominant market share.

The Automation and Orchestration segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by increasing demand for automated workflows and self-service IT operations. For instance, VMware’s vRealize suite enables enterprises to automate provisioning, monitoring, and management across hybrid cloud environments. Automation reduces manual intervention, accelerates deployment, and ensures consistency in operations, making it highly attractive for organizations undergoing digital transformation. Rising adoption of AI-driven orchestration tools further strengthens market growth in this segment.

- By Organization Size

On the basis of organization size, the SDDC market is segmented into large enterprises and small and medium-sized enterprises (SMEs). Large enterprises dominated the market in 2025, driven by their extensive IT infrastructure and the need to optimize operational efficiency across multiple data centers. Enterprises implement SDDC solutions to reduce complexity, improve scalability, and support hybrid cloud strategies. Large organizations often invest in comprehensive virtualization and orchestration solutions that provide centralized control and enhanced security. Their established IT budgets and focus on innovation enable early adoption of advanced SDDC technologies.

The SME segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing awareness of the benefits of software-defined infrastructure and the availability of cost-effective, scalable solutions. For instance, Nutanix offers simplified SDDC platforms tailored for SMEs, enabling cloud-like flexibility and reduced IT management burden. SMEs increasingly leverage SDDC to achieve agility, support remote operations, and improve competitiveness without heavy capital expenditure. The growing focus on digital transformation and hybrid IT adoption drives adoption among smaller organizations.

- By Vertical

On the basis of vertical, the SDDC market is segmented into BFSI, IT and Telecom, Government and Defense, Healthcare, Education, Retail, Manufacturing, and Others. The IT and Telecom vertical dominated the market in 2025, driven by the need for scalable, agile, and highly available data center infrastructure to support cloud services, telecom operations, and managed services. Organizations in this vertical prioritize SDDC solutions for rapid deployment, multi-tenant support, and centralized management of compute, storage, and networking resources. The high degree of digitalization, cloud adoption, and service automation in this sector reinforces its dominant market share.

The Healthcare vertical is expected to witness the fastest growth from 2026 to 2033, fueled by the rising need for secure, scalable, and compliant data center solutions to manage patient records and digital health services. For instance, Philips Healthcare implements software-defined infrastructure to enhance data accessibility, improve resource utilization, and support telemedicine platforms. SDDC adoption in healthcare ensures robust security, disaster recovery, and integration with cloud-based analytics tools, driving rapid deployment across hospitals and medical research institutions.

Software-Defined Data Center Market Regional Analysis

- North America dominated the software-defined data center market with the largest revenue share of 40.7% in 2025, driven by increasing adoption of virtualization, cloud computing, and hybrid IT infrastructure across enterprises

- Organizations in the region highly value the flexibility, scalability, and centralized management offered by software-defined data center solutions, enabling seamless integration of compute, storage, and networking resources

- This widespread adoption is further supported by high IT budgets, a technologically advanced workforce, and the growing demand for automated, software-driven data center operations, establishing software-defined data center as a preferred solution for large-scale enterprises

U.S. Software-Defined Data Center Market Insight

The U.S. software-defined data center market captured the largest revenue share in North America in 2025, fueled by rapid cloud adoption and the increasing need for agile, software-managed IT infrastructure. Enterprises are prioritizing software-defined data center solutions to optimize data center performance, reduce operational costs, and enhance security. The growing emphasis on hybrid cloud strategies, in addition to the integration of AI-driven monitoring and orchestration tools, further propels market growth. Moreover, the increasing adoption of containerization and microservices architecture supports the expansion of software-defined data center across multiple industries.

Europe Software-Defined Data Center Market Insight

The Europe software-defined data center market is projected to grow at a substantial CAGR throughout the forecast period, primarily driven by digital transformation initiatives and stringent regulatory compliance requirements. The rise in enterprise cloud deployments, coupled with the need for high-performance computing and energy-efficient data centers, is fostering the adoption of software-defined data center. European organizations are also investing in software-defined storage and networking solutions to enhance operational flexibility. The region is witnessing considerable growth across BFSI, IT, healthcare, and government sectors, with software-defined data center solutions integrated into both new and existing infrastructure projects.

U.K. Software-Defined Data Center Market Insight

The U.K. software-defined data center market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing enterprise cloud adoption and the need for secure, scalable IT infrastructure. Organizations are leveraging software-defined data center solutions to enhance resource utilization and simplify data center management. The U.K.’s strong IT services ecosystem and emphasis on digital innovation are expected to further stimulate market growth. Government-led initiatives supporting digital transformation and smart infrastructure adoption also contribute to the rising demand for software-defined data center solutions.

Germany Software-Defined Data Center Market Insight

The Germany software-defined data center market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of software-defined infrastructure and the focus on energy-efficient and sustainable data centers. Enterprises are increasingly adopting software-defined data center solutions for enhanced automation, workload management, and reduced operational complexity. Germany’s robust IT infrastructure, in addition to its emphasis on innovation and cybersecurity, encourages the integration of software-defined data center across industries. The preference for solutions that align with local compliance standards and sustainability goals drives market growth in both commercial and government segments.

Asia-Pacific Software-Defined Data Center Market Insight

The Asia-Pacific software-defined data center market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid digitalization, increasing enterprise IT investments, and the rise of cloud-first strategies in countries such as China, Japan, and India. The region’s growing focus on smart city initiatives, technological infrastructure, and digital transformation in enterprises is boosting software-defined data center adoption. Moreover, as APAC emerges as a hub for data center infrastructure development and software solutions, affordability and accessibility of software-defined data center platforms are expanding across multiple industry verticals.

Japan Software-Defined Data Center Market Insight

The Japan software-defined data center market is gaining momentum due to the country’s advanced IT ecosystem, high cloud adoption rates, and increasing demand for efficient, automated data center management. Enterprises are investing in software-defined data center solutions to enhance performance, scalability, and operational agility. The integration of software-defined networking, storage, and compute resources with AI-driven analytics is driving adoption. Japan’s aging workforce and focus on operational efficiency further encourage the use of automated, software-managed data centers across industries.

China Software-Defined Data Center Market Insight

The China software-defined data center market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid digital transformation, growing cloud adoption, and large-scale enterprise IT infrastructure investments. China is experiencing strong demand for software-defined computing, storage, and networking solutions across BFSI, IT, and manufacturing sectors. Government initiatives promoting smart cities, coupled with the presence of domestic software-defined data center solution providers, are accelerating adoption. The availability of cost-effective, scalable solutions further strengthens the market, enabling widespread deployment in both enterprise and government segments.

Software-Defined Data Center Market Share

The software-defined data center industry is primarily led by well-established companies, including:

- Dell Technologies (U.S.)

- Hewlett Packard Enterprise Development LP (U.S.)

- VMware, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Microsoft Corporation (U.S.)

- Nokia Corporation (Finland)

- Oracle Corporation (U.S.)

- ARYAKA NETWORKS, INC. (U.S.)

- Citrix Systems, Inc. (U.S.)

- Extreme Networks, Inc. (U.S.)

- Infovista (France)

- NEC Corporation (Japan)

- Nutanix, Inc. (U.S.)

- Pluribus Networks, Inc. (U.S.)

- Red Hat, Inc. (U.S.)

- SUSE (Germany)

- Adaptiv Networks, Inc. (U.S.)

- Arista Networks, Inc. (U.S.)

- Bigleaf Networks, Inc. (U.S.)

Latest Developments in Global Software-Defined Data Center Market

- In May 2025, Hewlett-Packard Enterprise Development LP expanded its HPE Aruba Networking portfolio by introducing the Aruba CX 10K distributed services switches. Featuring integrated AMD Pensando DPUs, these switches offload network and security tasks from server CPUs, thereby freeing up compute resources for AI and other intensive workloads. This development is expected to significantly enhance operational efficiency and scalability in modern data center environments, strengthening HPE’s position in the SDDC and enterprise networking market. By enabling high-performance network management alongside AI-ready infrastructure, HPE is addressing the growing demand for agile, software-driven data centers

- In April 2025, Dell Inc., through a strategic collaboration, launched its PowerFlex software-defined storage solution integrated with the Nutanix Cloud Platform (NCP) and Nutanix Cloud Infrastructure (NCI). The joint solution supports Nutanix’s native hypervisor, AHV, within a scalable, two-tiered architecture, enhancing flexibility, performance, and resource optimization for hybrid cloud deployments. This launch reinforces Dell’s role in the SDDC market by providing enterprises with a unified, high-performance storage and cloud management solution, enabling seamless integration across on-premises and cloud environments while addressing the increasing demand for scalable, automated infrastructure

- In April 2025, Last Energy announced plans to construct 30 microreactors in Texas, targeting a generation capacity of approximately 600 megawatts dedicated to data centers. This initiative addresses the rising energy demands of expanding data center operations, enabling high-density computing environments without overloading the existing power grid. By providing a stable, localized energy source, this development is expected to positively impact the SDDC and high-performance computing markets, supporting sustainable and reliable data center growth while attracting enterprises focused on energy efficiency and operational resilience

- In March 2025, Rackspace Technology launched its Rackspace SDDC Flex service in partnership with VMware and Dell, offering a cloud solution that combines public and private cloud capabilities with flexible infrastructure, self-service options, and automated deployment. Designed on a consumption-based pricing model, the service enhances operational agility for enterprises, reducing deployment times and simplifying hybrid cloud management. This move strengthens Rackspace’s market position by addressing the growing demand for scalable, software-defined data center solutions that integrate automation, flexibility, and rapid provisioning across hybrid IT environments

- In January 2025, TerraPower and Sabey signed a memorandum of understanding to explore the deployment of microreactors across Sabey’s software-defined data centers. The initiative aims to enhance energy efficiency, sustainability, and resilience in data center operations while addressing power limitations in critical markets. By integrating advanced, low-carbon energy solutions into SDDC infrastructures, this development supports the adoption of high-density computing and positions both companies as leaders in the emerging intersection of energy innovation and software-defined data center technologies

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.