Global Tank Insulation Market

Размер рынка в млрд долларов США

CAGR :

%

USD

3.84 Billion

USD

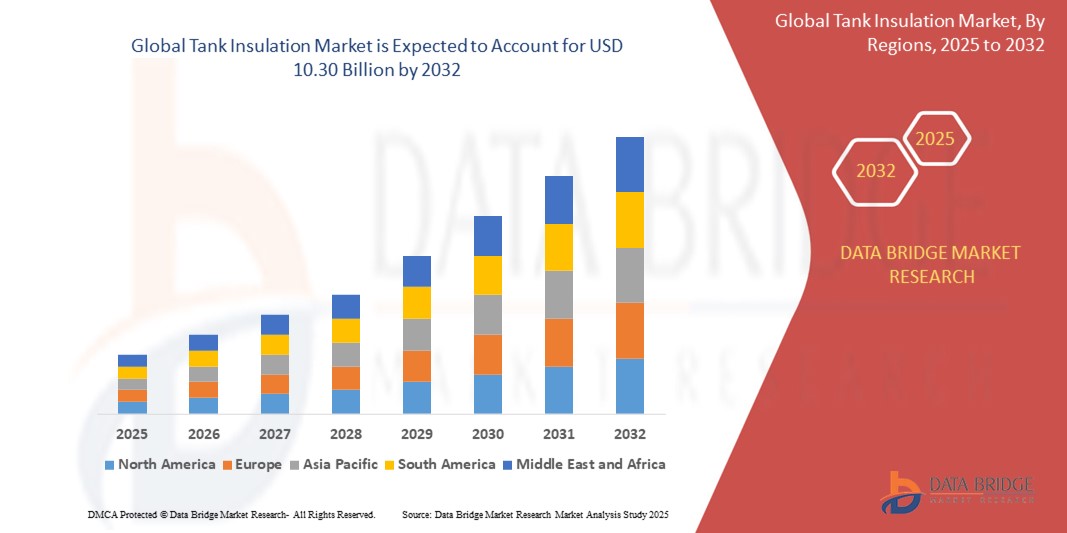

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

Сегментация глобального рынка изоляции резервуаров по типу (хранение и транспортировка), типу материалов (расширенный полистирол (EPS), шерсть, стекловолокно, стекловолокно, эластомерная пена, полиуретан (PU) и другие), типу температуры (горячая изоляция и холодная изоляция), типу резервуара (вертикальный танк, горизонтальный танк, фиксированный танк и фиксированный танк), концам резервуара (параболическая тара и плоский), конечному пользователю (нефть и газ, энергия и энергия, химические вещества, продукты питания и напитки, очистка воды, очистка отработанной воды и другие) - отраслевые тенденции и прогноз до 2032 года

Tank Insulation Market Size

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Содержание

СТАТЬЯ СОДЕРЖАНИЯ ГЛОБАЛЬНОГО ИНСУЛЯЦИОННОГО РЫНКА

1 Введение

1.1 Цели исследования 1.2 МАРКЕТНОЕ ОБЯЗАТЕЛЬСТВО 1.3 ОБРАЩЕНИЕ МАРКЕТа ГЛОБАЛЬНОГО ИНСУЛЯЦИОННОГО ИНСУЛЯЦИОННОГО ИНСУЛЯЦИОННОГО ИНСУЛЯЦИИ 1.4 КУРРЕНИЯ И ПРИКАЗЫВАНИЯ 1.5 ОГРАНИЧЕНИЯ 1.6 МАРКЕТОВ

2 МАРКЕТНАЯ СЕГМЕНТАЦИЯ

2.1 МАРКЕТЫ ПРЕДОСТАВЛЯЕТСЯ 2.2 ГЕОГРАФИЧЕСКАЯ ШКОЛА 2.3 ГОДА КОНСИДЕНЦИЯ ДЛЯ СТУДИИ 2.4 КУРРЕНСИРОВАНИЯ И ПРИГЛАШЕНИЯ 2.5 ДБМР ТРИПОД ДАННЫЙ КАЛЛИДИРОВАНИЕ МОДЕЛЬ 2.6 ТЕХНОЛОГИЧЕСКАЯ ЖИЗНЬ 2.7 МУЛЬТИВАРИАТНАЯ МОДЕЛЛЯЦИЯ 2.8 ПРАВИТЕЛЬНЫЕ ИНТЕРВЬЮЫ С КЛЮЧЕВЫМИ ЛИДЕРАМИ 2.9 ДБМР МАРКЕТНАЯ ПОЛИЦИЯ ГРИД 2.10 МАРКЕТНАЯ ПОЛИТИКА КОВЕРАГ 2.11 ДБМР МАРКЕТ КАЛЛЕНГИЧЕСКАЯ МАТРИКА 2.12 ВАЖНО-ЭКСПОРТНЫЕ

3 МАРКЕТНЫЙ ОБЗОР

3.1 Водители

3.1.1 Уменьшение спроса со стороны нефтяной и газовой промышленности 3.1.2 Растущее требование к регулированию криогенной нагрузки при сжиженном природном газе и транспортировке 3.1.3 Растущее требование к температуре, урегулированное при упаковке фармацевтических материалов 3.1.4 Растущее требование к струям мака в банках для обеспечения функционирования термобарьера

3.2 УВЕДОМЛЕНИЯ

3.2.1 ФЛУКТУАЦИЯ РЕАЛЬНЫХ МАТЕРИАЛЬНЫХ ЦЕН 3.2.2 ИЗМЕНЕНИЕ ХИМИЧЕСКОЙ СТРУКТУРЫ ДЛЯ ПОДДЕРЖИВАНИЯ МАТЕРИАЛЬНОГО ИНСУЛЯЦИОННОГО ИНСУЛЯЦИОННОГО МАТЕРИАЛЬНЫХ МАТЕРИАЛОВ ДЛЯ ИРОНА И СТЕЛЬНОЙ ИНДУСТРИИ ДЛЯ ХОЛЬТЕННОГО МЕТАЛА В ТАНКТАХ 3.2.4 ФРЕКТУАЛЬНАЯ ДЕГРАДАЦИЯ ИНСУЛЯЦИОННЫХ МАТЕРИАЛОВ В ХИМИЧЕСКОЙ ИНДУСТРИИ

3.3 Положения

3.3.1 ВЫСОКОЕ ПРЕДУПРЕЖДЕНИЕ ДЛЯ ПЕТРОХИМИЧЕСКОЙ ПРОМЫШЛЕННОСТИ В КИТАЕ И ИНДИЯ 3.3.2 ВЫСОКИЙ ПРЕДУПРЕЖДЕНИЕ ПРЕДУПРЕЖДЕНИЯ МАТЕРИАЛОВ В ВОДНЫХ БАНКАХ ДЛЯ МУЛЬТИСТОРИИ И КОММЕРЧЕСКИХ СТРУКЦИЙ 3.3.3 УСИЛЕНИЕ ИНДУСТИАЛИЗАЦИИ В ЭМЕРГИРОВАНИИ ЭКОНОМИКИ

3.4 Вызовы

3.4.1 Огнестрельная и ЭКСПЛОЗИЦИОННАЯ ДУМА ДЛЯ ХИМИЧЕСКОЙ ОТВЕТСТВЕННОСТИ С ИНСУЛЯЦИЕЙ МАТЕРИАЛЬНОЙ В ТАНКЕ 3.4.2 ЗДОРОВЬЯ ЗДОРОВЬЯ МЕДИАЦИИ

4 Исполнительный отчет 5 Премиальных Впечатлений 6 Индустриальные идеи 7 ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ, ПО ТИПУ

7.1 ОБРАЩЕНИЕ 7.2 ТРАНСПОРТАЦИЯ 7.3

8 ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ В МАТЕРИАЛЬНОМ ТИПЕ

8.1 ОБЗОР 8.2 Расширенный полистирол (ЕРС) 8.3 РОКВУЛЬ 8.4 ЦЕЛЛАРНЫЙ ЗАГЛАС 8.5 ФИБЕРГЛАСС 8.6 ЭЛАСТОМЕРНЫЙ ФОМ 8.7 ПОЛИУРЕТАН (ПУ) 8.8 ДРУГИЕ

9 ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ, ПО ТЕМПЕРАТУРЕ

9.1 ОБЯЗАТЕЛЬСТВО 9.2 ГОРЯЧАЯ ИНСУЛЯЦИЯ 9.3 ХОЛОДНАЯ ИНСУЛЯЦИЯ

10 МАРКЕТ ГЛОБАЛЬНОГО ИНСУЛЯЦИОННОГО ИНСУЛЯЦИИ В БАНКОВОМ ТИПЕ

10.1 ОБЗОР 10.2 ВЕРТИЧЕСКИЙ БАНК 10.3 ГОРИЗОНТАЛЬНЫЙ БАНК 10.4 ФИКСИРОВАННЫЙ БАНК 10.5 ГОРЯЧИЙ БАНК

11 МАРКЕТ ГЛОБАЛЬНОГО ИНСУЛЯЦИОННОГО ИНСУЛЯЦИОННОГО ТАНКА, ПО ТЕМЕ ВАНКОВЫХ ЭНДСОВ

11.1 ОБЩЕСТВО 11.2 ПАРАБОЛИЧЕСКИЙ ДИШ 11.3 ФЛАТ

12 ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ, ПОСЛЕДНИК

12.1 Проверка 12.2 Нефть и газ

12.2.1 Нефть

12.2.1.1 КРУДНОЕ НЕФТЬ 12.2.1.2 ПЕТРОХИМИЧЕСКОЕ 12.2.1.3 ДРУГИЕ КРУДНЫЕ НЕФТЕВЫ

12.2.2 ГАЗ

12.2.2.1 Естественный газ 12.2.2.2 Синтетический газ

12.3 ЭНЕРГИЯ И ВЛАСТЬ 12.4 ХИМИЧЕСКИЕ 12.5 ПИЩА И ПИВЕРЫ

12.5.1 Питание 12.5.2 СЕРДЦА

12.5.2.1 АЛКОХОЛОГИЧЕСКИЕ ПЕРЕВОДЫ 12.5.2.2 ДЕНЬ 12.5.2.3 САДОВЫЕ ПРИБАВКИ 12.5.2.4 ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ДРУГИЕ ВОДЫ

12.6 Очистка воды

12.6.1 КОММЕРЧЕСКИЕ СТРОИТЕЛЬСТВА 12.6.2 МУНИЦИПАЛЬНОСТЬ 12.6.3 ПРЕДСТАВЛЕНИЯ

12.7 Очистка сточных вод

12.7.1 КОММЕРЧЕСКИЕ СТРОИТЕЛЬСТВА 12.7.2 МУНИЦИПАЛЬНОСТЬ 12.7.3 ПРЕДСТАВЛЕНИЯ

12.8 Другие

13 ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ ГЕОГРАФИИ

13.1 Обзор 13.2 Северная Америка

13.2.1 США 13.2.2 CANADA 13.2.3 MEXICO

13.3 Европа

13.3.1 GERMANY 13.3.2 U.K 13.3.3 ITALY 13.3.4 FRANCE 13.3.5 SPAIN 13.3.6 SWITZERLAND 13.3.7 RUSSIA 13.3.8 TURKEY 13.3.9 BELGIUM 13.3.10 NETHERLANDS 13.3.11 ПЕСТ ЕВРОПЫ

13.4 ASIA-PACIFIC

13.4.1 Китай 13.4.2 Индия 13.4.3 Южная Корея 13.4.4 Япония 13.4.5 Австралия 13.4.6 Сингапур 13.4.7 Таиланд 13.4.8 Индонезия 13.4.9 Малайзия 13.4.10 Филиппины 13.4.11 ПЕСТ АСИА-ПАЦИФИКА

13.5 Южная Америка

13.5.1 БРАЗИЛ 13.5.2 АРГЕНТИНА 13.5.3 ПРЕДОСТАВКА ЮЖНОЙ АМЕРИКИ

13.6 Средний Восток и Африка

13.6.1 ОАЭ 13.6.2 SAUDI ARABIA 13.6.3 ISRAEL 13.6.4 SOUTH AFRICA 13.6.5 EGYPT 13.6.6 REST OF MIDDLE EAST and AFRICA

14 ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ, КОМПАНИЯ ЛЭНДСКАП

14.1 КОМПАНИЯ ДЛЯ АНАЛИЗА: ГЛОБАЛ 14.2 КОМПАНИЯ ДЛЯ АНАЛИЗА: СЕВЕРНАЯ АМЕРИКА 14.3 КОМПАНИЯ ДЛЯ АНАЛИЗА: ЕВРОПА 14.4 КОМПАНИЯ ДЛЯ АНАЛИЗА: АСИА-ПАЦИФИК 14.5 МЕРГЕРЫ И АККУИСТИЦИИ 14.6 НОВОЕ ПРОДУКТСТВЕННОЕ РАЗВИТИЕ И АППРОВАЛЫ 14.7 ИСПОЛЬЗОВАНИЯ 14.8 СТРАТЕГИЧЕСКОЕ РАЗВИТИЕ

15 КОМИТЕТНЫХ ПРОФИЛ

15.1 BASF SE

15.1.1 КОМПАНИЯ СНАПШОТ 15.1.2 СВОТ АНАЛИЗ 15.1.3 РЕВЕНУЮ АНАЛИЗ 15.1.4 КОМПАНИЯ ДЕЛАЕТСЯ АНАЛИЗОМ 15.1.5 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.1.6 ПРОДУКТ ПОРТФОЛИО 15.1.7 РАЗВИТИЯ 15.1.8 ДАННЫХ МАРКЕТНЫХ ИССЛЕДОВАНИЙ

15.2 Нижняя химическая компания

15.2.1 КОМПАНИЯ СНАПШОТ 15.2.2 СВОТ АНАЛИЗ 15.2.3 РЕВЕНУЮ АНАЛИЗ 15.2.4 КОМПАНИЯ ДЕЛАЕТСЯ АНАЛИЗОМ 15.2.5 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.2.6 ПРОДУКТ ПОРТФОЛИО 15.2.7 РАЗВИТИЯ 15.2.8 ДАННЫХ МАРКЕТНЫХ ИССЛЕДОВАНИЙ

15.3 САИНТ-ГОБАИН

15.3.1 КОМПАНИЯ СНАПШОТ 15.3.2 СВОТ АНАЛИЗ 15.3.3 РЕВЕНУЮ АНАЛИЗ 15.3.4 КОМПАНИЯ ДЕЛАЕТСЯ АНАЛИЗОМ 15.3.5 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.3.6 ПРОДУКТ ПОРТФОЛИО 15.3.7 РАЗВИТИЯ 15.3.8 РАЗВИТИЯ ДАННЫХ МАРКЕТОВ АНАЛИЗ

15.4 Международная компания HUNTSMAN

15.4.1 КОМПАНИЯ СНАПШОТ 15.4.2 СВОТ АНАЛИЗ 15.4.3 РЕВЕНУЮ АНАЛИЗ 15.4.4 КОМПАНИЯ ДЕЛАЕТСЯ АНАЛИЗОМ 15.4.5 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.4.6 ПРОДУКТ ПОРТФОЛИО 15.4.7 РАЗВИТИЯ 15.4.8 РАЗВИТИЯ ДАННЫХ МАРКЕТОВ АНАЛИЗ

15.5 KINGSPAN GROUP

15.5.1 КОМПАНИЯ СНАПШОТ 15.5.2 СВОТ АНАЛИЗ 15.5.3 РЕВЕНУЮ АНАЛИЗ 15.5.4 КОМПАНИЯ ДЕЛАЕТСЯ АНАЛИЗОМ 15.5.5 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.5.6 ПРОДУКТ ПОРТФОЛИО 15.5.7 РАЗВИТИЯ 15.5.8 ДАННЫХ БРИКЕТНЫХ РЫНКОВ АНАЛИЗ

15.6 ООО «АРМАКЕЛЛ»

15.6.1 КОМПАНИЯ СНАПШОТ 15.6.2 РЕВЕНУЮ АНАЛИЗ 15.6.3 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.6.4 ПРОДУКТ ПОРТФОЛИО 15.6.5 РАЗВИТИЯ РЕЦЕНТОВ

15.7 Корпорация кабины

15.7.1 КОМПАНИЯ СНАПШОТ 15.7.2 РЕВЕНУЮ АНАЛИЗ 15.7.3 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.7.4 ПРОДУКТ ПОРТФОЛИО 15.7.5 РЕКЦИОННЫЕ РАЗВИТИЯ

15.8 ОБЩИЕ ТЕРМИЧЕСКИЕ РЕШЕНИЯ, ИНК.

15.8.1 КОМПАНИЯ СНАПШОТ 15.8.2 ПРОДУКТ ПОРТФОЛИО 15.8.3 ПРОДУКТ РАЗВИТИЯ

15.9 Коррозионно-резистентные технологии, ИНК.

15.9.1 КОМПАНИЯ СНАПШОТ 15.9.2 ПРОДУКТ ПОРТФОЛИО 15.9.3 ПРОДУКТ РАЗВИТИЯ

15.10 МЕСТО

15.10.1 КОМПАНИЯ СНАПШОТ 15.10.2 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.10.3 ПРОДУКТ ПОРТФОЛИО 15.10.4 РАЗВИТИЯ РЕЦЕНТОВ

15.11 ГИЛСУЛАТНЫЙ МЕЖДУНАРОДНЫЙ, ИНК.

15.11.1 КОМПАНИЯ СНАПШОТ 15.11.2 ПРОДУКТ ПОРТФОЛИО 15.11.3 ДЕВОЛЮЦИИ РЕЦЕНТОВ

15.12 ФАКТОРИЯ КОЛЕВОЙ КОЛЕВЫ

15.12.1 КОМПАНИЯ СНАПШОТ 15.12.2 ПРОДУКТ ПОРТФОЛИО 15.12.3 РАЗВИТИЕ РЕЦЕНТОВ

15.13 ИНСУЛЯЦИОННЫЕ СИСТЕМЫ ИТВ

15.13.1 КОМПАНИЯ СНАПШОТ 15.13.2 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.13.3 ПРОДУКТ ПОРТФОЛИО 15.13.4 РАЗВИТИЕ РЕКТОВ

15.14 Джон Манвилль

15.14.1 КОМПАНИЯ СНАПШОТ 15.14.2 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.14.3 ПРОДУКТ ПОРТФОЛИО 15.14.4 РАЗВИТИЯ РЕЦЕНТОВ

15.15 J.H. ZIEGLER GMBH

15.15.1 КОМПАНИЯ СНАПШОТ 15.15.2 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.15.3 ПРОДУКТ ПОРТФОЛИО 15.15.4 РАЗВИТИЕ РЕКТА

15.16 ИНСУЛЯЦИЯ КНАУФОВ

15.16.1 КОМПАНИЯ СНАПШОТ 15.16.2 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.16.3 ПРОДУКТ ПОРТФОЛИО 15.16.4 РАЗВИТИЯ РЕЦЕНТОВ

15.17 МЕЖДУ КОТОРЫ И ИНСУЛЯЦИЯ, ИНК.

15.17.1 КОМПАНИЯ СНАПШОТ 15.17.2 ПРОДУКТ ПОРТФОЛИО 15.17.3 РАЗВИТИЯ РЕЦЕНТОВ

15.18 СОБСТВЕННОСТЬ

15.18.1 КОМПАНИЯ СНАПШОТ 15.18.2 РЕВЕНУЮ АНАЛИЗ 15.18.3 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.18.4 ПРОДУКТ ПОРТФОЛИО 15.18.5 РЕКТЫ РАЗВИТИЯ

15.19 ИНСУЛЯЦИЯ ПОЛАРКЛАДСКИХ БАНКОВ

15.19.1 КОМПАНИЯ СНАПШОТ 15.19.2 ПРОДУКТ ПОРТФОЛИО 15.19.3 РАЗВИТИЕ РЕЦЕНТОВ

15.20 RÖCHLING GROUP

15.20.1 КОМПАНИЯ СНАПШОТ 15.20.2 GEOGRAPHICAL PRESENCE 15.20.3 PRODUCT PORTFOLIO 15.20.4 RECENT DEVELOPMENTS

15.21 МЕЖДУНАРОДНАЯ А/С

15.21.1 КОМПАНИЯ СНАПШОТ 15.21.2 РЕВЕНУАЛЬНЫЙ АНАЛИЗ 15.21.3 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.21.4 ПРОДУКТ ПОРТФОЛИО 15.21.5 РЕКЦИЯ РАЗВИТИЯ

15.22 SPX TRANSFORMER SOLUTIONS INC.

15.22.1 КОМПАНИЯ СНАПШОТ 15.22.2 ПРОДУКТ ПОРТФОЛИО 15.22.3 ПРОДУКТ РАЗВИТИЯ

15.23 SYNAVAX

15.23.1 КОМПАНИЯ СНАПШОТ 15.23.2 РАЗДЕЛЕНИЕ ПОРТФОЛИО 15.23.3 РАЗВИТИЯ РЕЦЕНТОВ

15.24 Термакон

15.24.1 КОМПАНИЯ СНАПШОТ 15.24.2 ПРОДУКТ ПОРТФОЛИО 15.24.3 ПРОДУКТ РАЗВИТИЯ

15.25 T.F.WARREN

15.25.1 КОМПАНИЯ СНАПШОТ 15.25.2 ГЕОГРАФИЧЕСКОЕ ПРЕДСТАВЛЕНИЕ 15.25.3 ПРОДУКТ ПОРТФОЛИО 15.25.4 РАЗВИТИЯ РЕЦЕНТОВ

16 вопросов 17 Выводы 18 Связанные поправки

Список таблиц

Список табличек ГЛОБАЛЬНЫЙ ИНСУЛЯЦИОННЫЙ МАРКЕТ

СТАТЬЯ 1 ВАЖНЫЕ ДАННЫЕ РЕЗЕРВОВ, ТАНКОВ, НДС И СИМИЛЬНЫХ КОНТАЙНЕРОВ, ИРНОЙ ИЛИ СТЕЛЬНОЙ, ДЛЯ ЛЮБОГО МАТЕРИАЛЬНОГО "ДРУГОГО, КОТОРЫЕ КОМПРЕДСТАВЛЯЮТСЯ ИЛИ ЖИЗНЕННЫХ ГАЗОВ", КАПАКТИКИ 300 л, не связанные с механической или ТЕМРАЛЬНОЙ УСЛОВИЯМИ, независимо от того, установлены они или нет (за исключением контейнеров, специально сконструированных или уравновешенных для одного или большего количества видов транспорта); СТАТЬЯ 7309 (USD MILLION) СТАТЬЯ 2 ЭКСПОРТНЫЕ ДАННЫЕ РЕЗЕРВОВ, БАНКОВ, НДС и СИМИЛЯРНЫХ КОНТАЙНЕРОВ, ИРОНА или СТЕЛА, для любого МАТЕРИАЛЬНОГО "ДРУГОГО, КОТОРЫЕ КОМПРЕДСТАВЛЯЮТСЯ ИЛИ ЖИЗНЕННЫХ ГАЗОВ", КАПАКТИЧЕСКОГО ГАЗа 300 Л, НЕ ОБЯЗАННЫЕ С МЕХАНИКАЛЬНЫМ И ТЕРМИНАЛЬНЫМ ТАМПЕТОМ, ИЛИ НЕ ОБЯЗАТЕЛЬНЫМ ТЕХНОЛОГИЧЕСКИМ ОТНОШЕНИЕМ (ОТ ТЕХНОЛОГИЧЕСКИМ ОТВЕТСТВЕННЫМ ОТВЕТСТВЕННЫМ ТЕХНОЛОГИЧЕСКИМ ОТВЕТСТВЕННОМУ ТРАНСПОРТУ) ; ГОСУДАРСТВЕННЫМ ОТВЕТСТВЕННЫМ ОТВЕТСТВЕННОМУ ТРАНСПОРТУ 3 СТАБЛИОНА, ТАБЛОГИЧЕСКИМ ОТВЕТСТВЕННОМУ ТРАНСПОРТУ, ТАБЛОГИЧЕСКИМ МАРКЕТОМ, ТАБЛОГИЧЕСКИМ МАРКЕТОМ, ТАБЛОГИЧЕСКИМ МАРК

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.