Global Thrombotic Thrombocytopenic Purpura Moschcowitz Disease Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.25 Billion

USD

1.77 Billion

2025

2033

USD

1.25 Billion

USD

1.77 Billion

2025

2033

| 2026 –2033 | |

| USD 1.25 Billion | |

| USD 1.77 Billion | |

| % | |

|

Global Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Segmentation, By Type (Inherited TTP and Acquired TTP), Treatment (Plasma Exchange, Corticosteroids, Rituximab, Caplacizumab, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Speciality Centres, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy) - Industry Trends and Forecast to 2033

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Size

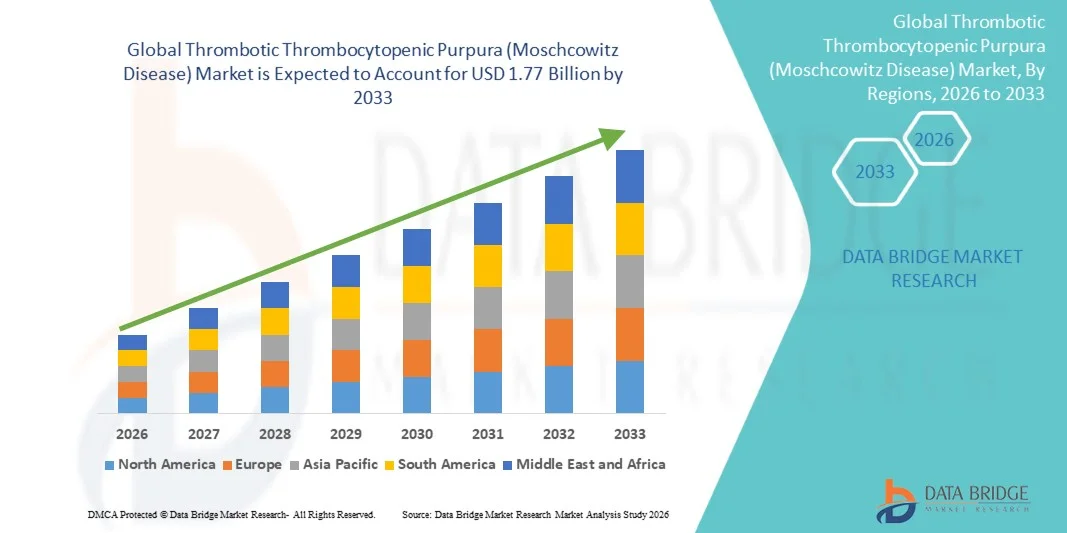

- The global thrombotic thrombocytopenic purpura (moschcowitz disease) market size was valued at USD 1.25 billion in 2025 and is expected to reach USD 1.77 billion by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is largely fueled by increasing awareness of rare blood disorders, technological advancements in diagnostic tools, and the adoption of innovative treatment solutions

- Furthermore, rising demand for safe, effective, and rapid therapeutic options for managing Thrombotic Thrombocytopenic Purpura (TTP) is driving the uptake of plasma exchange therapies, immunosuppressive treatments, and novel biologics, significantly boosting the industry’s growth

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Analysis

- Smart therapies, advanced diagnostics, and targeted biologics are increasingly vital components in the management of Thrombotic Thrombocytopenic Purpura (TTP), due to their enhanced efficacy, safety, and ability to reduce disease recurrence

- The escalating demand for TTP treatments is primarily fueled by growing awareness of rare blood disorders, rising incidence rates, and a preference for personalized, rapid, and minimally invasive therapies

- North America dominated the thrombotic thrombocytopenic purpura (moschcowitz disease) market with the largest revenue share of 42.5% in 2025, characterized by high adoption of advanced diagnostic tools, well-established healthcare infrastructure, and a strong presence of key pharmaceutical players, with the U.S. leading in TTP treatment adoption and innovative biologic therapies

- Asia-Pacific is expected to be the fastest growing region in the thrombotic thrombocytopenic purpura (moschcowitz disease) market during the forecast period, with a projected growth rate of 14.8% CAGR, driven by increasing healthcare spending, rising awareness, and expanding access to advanced therapies

- Parenteral administration dominated with 63.2% revenue share in 2025, as intravenous plasma exchange, rituximab, and caplacizumab are primary treatment methods

Report Scope and Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Segmentation

|

Attributes |

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Grifols (Spain) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Trends

“Enhanced Convenience Through AI and Voice Integration”

- A significant and accelerating trend in the global thrombotic thrombocytopenic purpura (moschcowitz disease) market is the increasing emphasis on early diagnosis and patient awareness

- Enhanced awareness among healthcare providers and patients is facilitating timely detection, which is crucial for improving patient outcomes

- For instance, in 2024, multiple U.S. hospitals introduced rapid ADAMTS13 activity assays, which can confirm TTP cases within hours, enabling clinicians to initiate plasma exchange therapy promptly

- The adoption of advanced diagnostic techniques is helping reduce misdiagnosis and delays in treatment, which historically contributed to high mortality rates

- Increased education and awareness campaigns by healthcare organizations are informing clinicians about key symptoms such as thrombocytopenia, microangiopathic hemolytic anemia, and neurological complications, ensuring early intervention

- This trend is also driving collaboration between hematologists and general practitioners to streamline patient referral pathways and implement standardized care protocols

- The growing focus on early diagnosis is ultimately reshaping the market by encouraging adoption of advanced treatment regimens and improving overall disease management outcomes

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Dynamics

Driver

“Rising Demand Due to Advancements in Therapeutics and Treatment Protocols”

- The increasing availability of targeted therapies and biologics for TTP is a major driver of market growth, as these interventions improve survival rates and reduce relapses

- For instance, in 2023, European centers reported that combining caplacizumab with plasma exchange significantly reduced hospitalization time and relapse rates, prompting wider adoption across clinical practices

- Improvements in treatment options encourage physicians to adopt newer therapies, enhancing patient confidence in outcomes and driving market expansion

- Moreover, the integration of patient support programs and treatment guidelines across specialized hematology centers ensures consistent and effective care

- Growing investments in research and development of novel therapeutics further support the trend of enhanced patient outcomes and better disease management

Restraint/Challenge

“High Treatment Costs and Limited Access in Developing Regions”

- Despite advances in therapy, high costs and the need for specialized care infrastructure remain major challenges for broader adoption, particularly in low- and middle-income countries

- For instance, in Southeast Asia, several hospitals face delays in plasma exchange therapy due to limited trained personnel and equipment, restricting access for patients in urgent need

- Limited awareness among primary care providers can result in misdiagnosis, delaying critical treatment and reducing survival chances

- In addition, the financial burden of biologics and hospitalization costs can deter patients from seeking early intervention

- Addressing these challenges requires increased healthcare funding, capacity-building programs, and awareness campaigns to expand access and affordability

- Developing cost-effective therapies, improving diagnostic infrastructure, and training healthcare professionals are crucial for sustained market growth

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

• By Type

On the basis of type, the Thrombotic Thrombocytopenic Purpura (TTP) market is segmented into Inherited TTP and Acquired TTP. The Acquired TTP segment dominated the largest market revenue share of 61.5% in 2025, driven by its higher prevalence in adults and the association with autoimmune disorders, infections, and other secondary conditions. The segment benefits from extensive clinical awareness, early diagnostic programs, and established treatment protocols including plasma exchange and immunosuppressive therapies. Hospitals and specialty centers are primary providers due to the need for intensive monitoring. Adoption is supported by government and insurance coverage, increasing patient awareness, and robust hematology infrastructure. Rising investment in research and clinical trials on disease management further boosts growth. The presence of trained specialists, well-equipped facilities, and established emergency care protocols strengthens market dominance. High adoption of supportive care therapies ensures optimal outcomes, reducing mortality and morbidity rates. Awareness campaigns, professional guidelines, and medical education programs also reinforce utilization. Patient registries and rare disease initiatives facilitate early detection and treatment planning.

The Inherited TTP segment is expected to witness the fastest CAGR of 13.4% from 2026 to 2033, owing to increasing recognition of genetic disorders and better access to advanced diagnostic tools. Early detection in neonates and pediatric patients drives demand. Growth is fueled by gene therapy research, personalized treatment options, and expanded orphan drug development. Patient advocacy groups and registries improve awareness, accessibility, and adherence. Adoption is further supported by training programs for clinicians in rare disease management. Emerging healthcare infrastructure in developing markets enables better care delivery. Telemedicine and home-based monitoring facilitate early intervention and compliance. Technological advancements in genetic testing enhance early diagnosis rates. Insurance coverage expansion and governmental initiatives improve affordability. Increased research funding and rare disease focus encourage rapid development and adoption. Public-private collaborations in healthcare further support growth.

• By Treatment

On the basis of treatment, the market is segmented into Plasma Exchange, Corticosteroids, Rituximab, Caplacizumab, and Others. Plasma Exchange held the largest market share of 46.8% in 2025, as it is the established gold-standard therapy for rapidly removing ultra-large von Willebrand factor multimers. It is widely adopted in hospitals and specialty centers with trained hematologists. Adoption is driven by clinical guidelines, proven efficacy, and life-saving potential during acute episodes. Insurance reimbursement and government healthcare programs further support utilization. Hospital infrastructure, availability of trained staff, and intensive care capabilities reinforce its dominance. Plasma exchange ensures improved survival rates and reduced organ damage. Integration with immunosuppressive therapies increases treatment effectiveness. Educational programs and clinical training for healthcare professionals promote broader use. High adoption in developed markets and emerging coverage in developing regions sustain its leading position. Ongoing clinical studies and real-world evidence strengthen physician confidence and continued preference.

The Rituximab and Caplacizumab segment is expected to register the fastest CAGR of 14.1% from 2026 to 2033, driven by growing awareness of relapse prevention and targeted therapy benefits. Adoption is fueled by guideline recommendations, increasing physician confidence, and demonstrated efficacy in autoimmune-mediated TTP. Expansion of specialty centers and outpatient care facilities supports growth. Research into combination therapies, biosimilars, and new formulations enhances accessibility and affordability. Clinical trial success and regulatory approvals accelerate adoption. Homecare and outpatient infusion programs further drive uptake. Patient education programs increase compliance and treatment success. Telehealth monitoring and remote follow-ups facilitate broader use. Increasing prevalence in emerging markets provides additional growth opportunities. Pharmaceutical innovation and marketing efforts strengthen segment momentum.

• By Route of Administration

On the basis of route, the market is segmented into Oral, Parenteral, and Others. Parenteral administration dominated with 63.2% revenue share in 2025, as intravenous plasma exchange, rituximab, and caplacizumab are primary treatment methods. Hospitals and specialty centers are the main providers due to need for controlled clinical environments. Adoption is reinforced by established clinical protocols, proven efficacy, and preference among hematologists. Parenteral treatments ensure rapid therapeutic response, critical for survival. Advanced infusion systems and safety protocols enhance compliance. Availability of trained staff and infrastructure supports market leadership. Government and insurance programs improve accessibility. Clinical research and guideline recommendations maintain physician preference. Patient monitoring technologies enhance treatment adherence. Strong adoption in developed markets and increasing implementation in emerging regions reinforce dominance.

The Oral segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, driven by the development of oral corticosteroids and supportive medications. Convenience, home-based administration, and patient preference fuel growth. Expansion of telehealth services and remote prescription systems facilitates adoption. Growing awareness among caregivers and patients enhances compliance. Oral alternatives for supportive care reduce hospital dependency. Formulation innovations and affordability improvements further accelerate uptake. Insurance coverage expansion and reimbursement policies increase accessibility. Integration with chronic care management models supports growth. Emerging markets are increasingly adopting oral therapies. Patient adherence programs strengthen uptake. Collaboration between pharmaceutical companies and healthcare providers encourages segment expansion.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Centers, and Others. Hospitals accounted for the largest revenue share of 58.7% in 2025, driven by the need for intensive monitoring, plasma exchange facilities, and critical care support. Advanced hematology units ensure immediate treatment, enhancing survival rates. Physician expertise, hospital infrastructure, and centralized care protocols reinforce dominance. Insurance coverage and government support further enable adoption. Hospital pharmacies maintain consistent treatment availability. Training programs and clinical guidelines ensure quality care. Hospital-based monitoring and ICU facilities improve patient outcomes. Technological adoption in hospitals strengthens efficiency and efficacy. High prevalence of acute TTP episodes supports continuous hospital-based demand. Collaborative care models further promote adoption. Established supply chains and resource availability maintain segment leadership.

The Specialty Centers and Homecare segment is expected to grow at the fastest CAGR of 12.9% from 2026 to 2033, fueled by outpatient infusion programs, home-based plasma exchange, and patient convenience. Telemedicine adoption and homecare infrastructure improvements accelerate uptake. Patient-centric care models and continuity of care programs drive growth. Emerging markets are investing in homecare services, enhancing accessibility. Supportive care programs for rare diseases improve adherence. Specialty centers facilitate targeted therapy delivery and follow-up. Remote monitoring and home infusion devices increase safety and compliance. Training of homecare professionals ensures quality care. Integration with patient registries enables early intervention. Awareness campaigns enhance adoption. Technological innovations in portable infusion systems further support growth. Reimbursement policies in homecare settings strengthen market expansion.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. Hospital pharmacies held the largest market share of 54.6% in 2025, reflecting immediate treatment requirements, availability of plasma exchange, and specialist-driven therapy. Centralized inventory, physician preference, and adherence to protocols reinforce dominance. Accessibility, insurance coverage, and regulatory compliance support adoption. Hospital pharmacies ensure uninterrupted treatment supply, reducing risk of delays. Integration with hospital management systems enhances efficiency. Clinical training programs maintain quality standards. Government initiatives and insurance reimbursements facilitate patient access. Hospitals continue to be primary distribution hubs for critical TTP therapies. Strong infrastructure and experienced staff support market leadership.

The Online and Retail Pharmacy segment is expected to register the fastest CAGR of 12.3% from 2026 to 2033, driven by increasing home delivery of oral medications, telemedicine prescriptions, and digital health platforms. Convenience, remote accessibility, and patient preference accelerate adoption. Expansion of logistics, cold-chain management, and e-commerce platforms support market growth. Insurance coverage and reimbursement policies enhance affordability. Awareness campaigns for rare diseases increase adoption. Partnerships with pharmaceutical companies enable broader distribution. Emerging markets show growing acceptance of online pharmacy channels. Technology integration facilitates monitoring, order tracking, and patient adherence. Patient support programs improve compliance. Expansion of retail pharmacy chains ensures wider reach.

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Regional Analysis

- North America dominated the thrombotic thrombocytopenic purpura (moschcowitz disease) market with the largest revenue share of 42.5% in 2025, characterized by high adoption of advanced diagnostic tools, well-established healthcare infrastructure, and a strong presence of key pharmaceutical players

- The U.S. continues to lead in TTP treatment adoption, with innovative biologic therapies such as caplacizumab and recombinant ADAMTS13 gaining widespread acceptance among hematologists. High awareness levels among clinicians and patients regarding early detection and advanced therapeutics are further driving market growth

- Supportive healthcare policies, insurance coverage for biologic therapies, and well-established patient management programs enhance treatment accessibility and market expansion

U.S. Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

The U.S. thrombotic thrombocytopenic purpura (moschcowitz disease) market captured the largest revenue share of approximately 81% within North America in 2025. This growth is fueled by rapid adoption of innovative biologic therapies, widespread use of advanced diagnostics such as ADAMTS13 activity assays, and robust infrastructure in tertiary care hospitals. For example, leading U.S. hematology centers have integrated caplacizumab therapy with plasma exchange protocols, significantly improving patient outcomes and reducing relapse rates. The market is further supported by strong research initiatives, clinical trials for new therapies, and increasing patient awareness regarding early diagnosis and treatment adherence.

Europe Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

The Europe thrombotic thrombocytopenic purpura (moschcowitz disease) market is projected to grow steadily, driven by rising awareness of TTP symptoms, adoption of standardized treatment protocols, and increasing access to biologic therapies. For instance, several UK hospitals have integrated caplacizumab with plasma exchange therapy into their hematology protocols, improving patient outcomes and reducing hospital stays. Expansion is supported by national health initiatives promoting early diagnosis and specialized hematology care centers across Germany, France, and Italy. Collaborations between pharmaceutical companies and healthcare institutions are facilitating access to innovative therapies for patients with refractory or relapsed TTP.

U.K. Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

The U.K. thrombotic thrombocytopenic purpura (moschcowitz disease) market is expected to grow at a noteworthy CAGR, driven by government-led awareness campaigns and the rising demand for specialized hematology services. For example, NHS centers have implemented rapid diagnostic panels for TTP, significantly improving early intervention and patient survival rates. The market is further strengthened by strong research initiatives and the adoption of advanced biologic therapies, ensuring comprehensive management of acute and chronic TTP cases.

Germany Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

Germany thrombotic thrombocytopenic purpura (moschcowitz disease) market is witnessing steady growth due to increasing clinician awareness, advanced hospital infrastructure, and early adoption of novel therapies. For instance, major hematology centers in Berlin and Munich have introduced recombinant ADAMTS13 therapy in addition to standard plasma exchange, improving treatment outcomes. A strong emphasis on patient monitoring, standardized care protocols, and accessibility to biologics supports Germany’s expanding TTP market.

Asia-Pacific Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

The Asia-Pacific thrombotic thrombocytopenic purpura (moschcowitz disease) market is expected to grow at the fastest CAGR of 14.8% during the forecast period, fueled by rising healthcare spending, improving access to advanced therapies, and increasing awareness of TTP symptoms. In countries such as Japan, China, and India, government initiatives promoting hematology specialization and the adoption of rapid diagnostic tools are accelerating disease management. For example, in 2025, leading hospitals in Shanghai began integrating caplacizumab with plasma exchange therapy, resulting in reduced hospitalization times and lower relapse rates. Expansion of healthcare infrastructure, growing access to biologics, and rising clinician awareness are major contributors to the APAC market’s rapid growth.

Japan Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

Japan’s thrombotic thrombocytopenic purpura (moschcowitz disease) market is gaining momentum due to a strong focus on early detection, availability of specialized hematology centers, and high adoption of novel therapies. For instance, major urban hospitals have implemented rapid ADAMTS13 assays and integrated biologic treatments, improving prognosis for acute TTP patients. An aging population, coupled with growing awareness of hematologic disorders, supports sustained market growth in both inpatient and outpatient care.

China Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Insight

China thrombotic thrombocytopenic purpura (moschcowitz disease) market accounted for the largest share of the Asia-Pacific TTP market in 2025, attributed to rapid urbanization, increasing healthcare investment, and expanding access to advanced therapeutics. For example, hospitals in Beijing and Shanghai have started using caplacizumab combined with plasma exchange for faster recovery in TTP patients. Government initiatives to improve hematology services and increase insurance coverage for biologic therapies are key factors driving market growth in China, making advanced treatment accessible to a wider patient population.

Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market Share

The Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) industry is primarily led by well-established companies, including:

• Grifols (Spain)

• Takeda Pharmaceutical Company (Japan)

• Octapharma AG (Switzerland)

• Sanofi (France)

•Alexion Pharmaceuticals (U.S.)

• Baxter International (U.S.)

• CSL Behring (Australia)

• Emergent BioSolutions (U.S.)

• Sobi (Swedish Orphan Biovitrum) (Sweden)

• Vifor Pharma (Switzerland)

• BioProducts Laboratory (BPL) (U.K.)

• Hansa Biopharma (Sweden)

• Amgen (U.S.)

• Novartis (Switzerland)

• Pfizer (U.S.)

• Roche (Switzerland)

• Regeneron Pharmaceuticals (U.S.)

• Boehringer Ingelheim (Germany)

• ViroPharma (Shire acquired) (U.S.)

Latest Developments in Global Thrombotic Thrombocytopenic Purpura (Moschcowitz Disease) Market

- In November 2021, the U.S. Thrombotic Thrombocytopenic Purpura (TTP) Market Research Report was published, providing an in‑depth epidemiology forecast and treatment landscape covering both acquired and congenital TTP, including the role of standard therapies (plasma exchange, immunosuppression) and emerging drug candidates like TAK‑755

- In March 2024, a 100‑year retrospective review on thrombotic thrombocytopenic purpura was published, summarizing the historical progression of understanding and treating TTP — from a nearly universally fatal condition to one benefiting from targeted therapies such as caplacizumab and recombinant ADAMTS13, and highlighting ongoing progress in patient management

- In March 2024, the International Society on Thrombosis and Haemostasis (ISTH) convened a multidisciplinary panel to update evidence and recommendations for TTP management, laying the groundwork for guideline revisions that would emerge the following year

- In July 2025, updated ISTH management guidelines for TTP (focused on evidence from immune TTP and congenital TTP) were released, refining treatment recommendations especially for congenital TTP and reinforcing the evolving role of targeted therapies, diagnostic improvements, and tailored patient care

- In July 2025, a clinical review published in Intensive Care Medicine highlighted modern advances in early diagnosis, pathophysiology insights, and effective treatments for TTP, marking progress in how this rare disease is recognized and managed in critical care settings around its centenary

- In March 2025, research on challenges in managing immune TTP with caplacizumab therapy was published, emphasizing ongoing clinical observations around treatment limitations, such as anti‑ADAMTS13 inhibitor boosting and complexities in achieving ADAMTS13 recovery despite caplacizumab’s benefits

- In November 2025, post‑market safety concerns emerged when the U.S. FDA began investigating Takeda’s Adzynma (a recombinant ADAMTS13 therapy approved for congenital TTP) following reports of antibody‑mediated treatment complications, highlighting the evolving safety and regulatory monitoring landscape in TTP therapies

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.