Global Vapor Recovery Units Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.06 Billion

USD

1.66 Billion

2025

2033

USD

1.06 Billion

USD

1.66 Billion

2025

2033

| 2026 –2033 | |

| USD 1.06 Billion | |

| USD 1.66 Billion | |

| % | |

|

Global Vapour Recovery Units Market Segmentation, By Type (Convectional Vapour Recovery Unit and Ejected Vapour Recovery Unit), Process (Absorption, Condensation, and Membrane Separation), Application (Upstream and Downstream in Oil and Gas, Landfills, and Pharmaceuticals) - Industry Trends and Forecast to 2033

Vapour Recovery Units Market Size

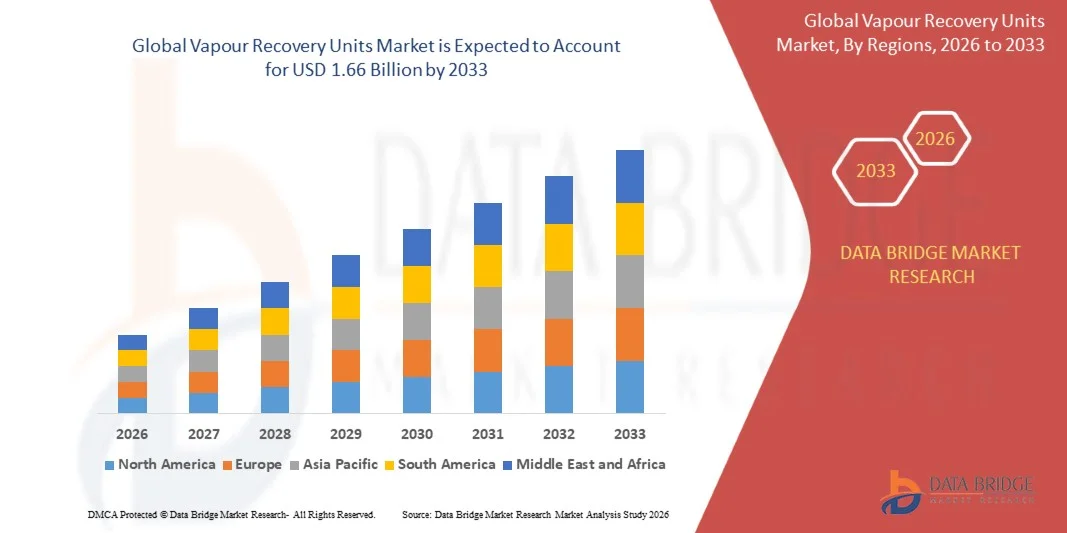

- The global vapour recovery units market size was valued at USD 1.06 billion in 2025 and is expected to reach USD 1.66 billion by 2033, at a CAGR of 5.8% during the forecast period

- The market growth is largely fueled by the increasing focus on reducing volatile organic compound (VOC) and greenhouse gas (GHG) emissions across oil and gas, chemical, and landfill operations, driving widespread adoption of vapour recovery units for environmental compliance and resource efficiency

- Furthermore, rising industrial demand for energy-efficient and cost-saving hydrocarbon recovery solutions is establishing VRUs as a critical component in upstream and downstream processes. These factors are accelerating the installation of advanced recovery systems, thereby significantly boosting market growth

Vapour Recovery Units Market Analysis

- Vapour recovery units are systems designed to capture and recover vapours released during storage, loading, or processing of hydrocarbons and other volatile compounds. These units integrate absorption, condensation, and membrane technologies to minimize emissions, enhance operational efficiency, and enable compliance with environmental regulations

- The escalating demand for vapour recovery units is primarily driven by stricter global emission standards, rising industrial production, and the need to recover valuable hydrocarbons for reuse, supporting both sustainability goals and economic benefits for industrial operators

- North America dominated the vapour recovery units market with a share of 39.51% in 2025, due to stringent environmental regulations, increasing focus on reducing hydrocarbon emissions, and the widespread presence of oil refineries and storage terminals

- Asia-Pacific is expected to be the fastest growing region in the vapour recovery units market during the forecast period due to rapid industrialization, rising energy demand, and strict environmental regulations in countries such as China, Japan, and India

- Convectional vapour recovery unit segment dominated the market with a market share of 62.5% in 2025, due to its proven efficiency in recovering hydrocarbon vapors across refineries and storage terminals. Industries often prefer convectional units for their reliability in continuous operations and lower maintenance requirements compared to more complex systems. The market also sees strong adoption of convectional vapour recovery units due to their compatibility with a wide range of storage and transportation setups and the availability of standardized designs that simplify integration

Report Scope and Vapour Recovery Units Market Segmentation

|

Attributes |

Vapour Recovery Units Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Vapour Recovery Units Market Trends

“Growth in Advanced Membrane and Absorption VRUs”

- A significant trend in the vapour recovery units market is the rising adoption of advanced membrane and absorption-based vapour recovery units, driven by increasing environmental regulations and operational efficiency goals. These technologies are enhancing the capture of volatile organic compounds (VOCs) and greenhouse gases (GHGs) from storage tanks and pipelines across petroleum and chemical facilities

- For instance, companies such as Honeywell UOP and Parker Hannifin supply advanced membrane VRUs that efficiently recover hydrocarbons from storage terminals and refineries. These systems reduce emissions while enabling the recovery of valuable products for reuse, strengthening both environmental compliance and operational economics

- The deployment of compact and modular vapour recovery unit systems is expanding as operators seek scalable solutions for smaller terminals and distributed storage networks. This trend is positioning membrane and absorption units as versatile options across diverse industrial setups

- Integration of vapour recovery units with automated monitoring and control systems is becoming more common, allowing real-time tracking of recovery efficiency and emissions. This technological convergence is driving smarter operation and preventive maintenance, optimizing system uptime and reducing operational losses

- Industries such as oil and gas and petrochemicals are prioritizing low-emission solutions to meet sustainability targets, reinforcing VRUs as essential assets in refinery modernization and expansion projects

- The market is witnessing innovation in hybrid recovery systems that combine adsorption, condensation, and membrane technologies. These hybrid solutions are offering higher recovery rates, reduced energy consumption, and compliance with stricter emission norms, enhancing overall market growth

Vapour Recovery Units Market Dynamics

Driver

“Stricter VOC and GHG Emission Regulations”

- The growing enforcement of VOC and GHG emission standards by organizations such as the U.S. Environmental Protection Agency (EPA) and the European Union is driving the adoption of VRUs across oil and gas, chemical, and storage industries. These regulations mandate the capture and control of evaporative emissions to limit environmental impact and ensure compliance with industrial guidelines

- For instance, Honeywell UOP has implemented VRU systems that comply with EPA’s NSPS Subpart K regulations for storage tanks, enabling refineries to reduce VOC emissions while recovering hydrocarbons for resale. Such compliance measures are accelerating the replacement of conventional recovery methods with advanced VRU technologies

- The increasing focus on sustainability and corporate environmental responsibility is pushing companies to adopt recovery solutions that lower their carbon footprint. Operators are investing in vapour recovery units to meet both regulatory requirements and internal ESG targets

- Expanding refinery capacities and storage infrastructures are increasing the need for efficient emission control solutions, which is reinforcing vapour recovery unit deployment globally

- Growing awareness of the economic benefits of recovered hydrocarbons, such as reduced product losses and improved profitability, is further driving market adoption. This is motivating companies to integrate advanced vapour recovery unit technologies into existing and new facilities

Restraint/Challenge

“High Installation and Maintenance Costs”

- The vapour recovery units market faces challenges due to the high capital and operational expenditures associated with advanced vapour recovery unit systems. Installation involves complex integration with storage tanks, pipelines, and refinery units, which can significantly elevate project costs

- For instance, Parker Hannifin’s absorption-based vapour recovery unit systems require specialized installation and periodic maintenance, including membrane replacements and system calibration, leading to considerable lifecycle costs. These financial requirements may limit adoption, particularly in small and medium-scale facilities

- Maintenance complexity and the need for trained personnel to operate and monitor systems further contribute to cost challenges. Companies must invest in skilled technicians and continuous training to ensure optimal vapour recovery unit performance

- Operational costs are also affected by energy consumption, particularly in vapor compression and cryogenic recovery systems, which can impact the return on investment

- The market continues to face constraints in balancing system efficiency, reliability, and cost-effectiveness. These factors collectively limit faster adoption in regions where cost sensitivity is high, despite regulatory and environmental pressures

Vapour Recovery Units Market Scope

The market is segmented on the basis of type, process, and application.

• By Type

On the basis of type, the Vapour Recovery Units market is segmented into Convectional Vapour Recovery Unit and Ejected Vapour Recovery Unit. The Convectional vapour recovery units segment dominated the largest market revenue share of 62.5% in 2025, driven by its proven efficiency in recovering hydrocarbon vapors across refineries and storage terminals. Industries often prefer convectional units for their reliability in continuous operations and lower maintenance requirements compared to more complex systems. The market also sees strong adoption of convectional VRUs due to their compatibility with a wide range of storage and transportation setups and the availability of standardized designs that simplify integration. Their established operational track record and cost-effectiveness make them a preferred choice for large-scale oil and gas facilities.

The Ejected vapour recovery units segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for compact and energy-efficient recovery solutions in emerging markets. These units are particularly suited for areas with limited space or intermittent operations, offering high recovery efficiency with lower energy consumption. The technological advancements in ejector-based vapour recovery units, along with their scalability for small- and medium-sized storage tanks, are driving adoption across oil terminals and chemical plants. Their growing appeal is also linked to environmental regulations promoting reduced hydrocarbon emissions.

• By Process

On the basis of process, the Vapour Recovery Units market is segmented into Absorption, Condensation, and Membrane Separation. The Absorption segment dominated the largest market revenue share in 2025, driven by its effectiveness in capturing volatile organic compounds (VOCs) from vapor streams in refineries and chemical plants. Industries favor absorption due to its high recovery efficiency, adaptability to different vapor compositions, and lower operational costs compared to more complex technologies. The market also benefits from the widespread availability of solvents and proven engineering designs, which simplify installation and maintenance.

The Membrane Separation segment is expected to witness the fastest growth from 2026 to 2033, fueled by its compact design and energy-efficient operation for decentralized and small-scale recovery applications. Membrane-based systems are particularly suitable for remote facilities or landfills, offering high selectivity and reduced environmental footprint. Technological improvements in membrane materials and modular designs are enhancing recovery rates and lowering lifecycle costs, boosting market adoption in developing regions.

• By Application

On the basis of application, the Vapour Recovery Units market is segmented into Upstream and Downstream in Oil and Gas, Landfills, and Pharmaceuticals. The Downstream Oil and Gas segment dominated the largest market revenue share in 2025, driven by the extensive use of VRUs in refineries, storage tanks, and loading terminals to capture hydrocarbon vapors during production and transportation. Companies prioritize downstream installations due to strict environmental compliance requirements and the potential for significant recovered product value. The market also benefits from established process integration strategies that allow vapour recovery units to operate efficiently with minimal disruption to existing workflows.

The Landfill segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing regulations on VOC and greenhouse gas emissions from waste management facilities. VRUs for landfills provide energy recovery and emission reduction benefits while enabling cost-effective compliance with environmental standards. Rising awareness of sustainable waste management practices and the adoption of modular vapour recovery unit designs for decentralized sites are further driving rapid growth in this application segment.

Vapour Recovery Units Market Regional Analysis

- North America dominated the vapour recovery units market with the largest revenue share of 39.51% in 2025, driven by stringent environmental regulations, increasing focus on reducing hydrocarbon emissions, and the widespread presence of oil refineries and storage terminals

- Companies in the region prioritize VRUs to comply with VOC and GHG emission standards while recovering valuable hydrocarbons for reuse

- The market growth is further supported by advanced infrastructure, strong industrial investments, and adoption of technologically advanced recovery systems, establishing VRUs as a preferred solution across oil and gas, chemical, and pharmaceutical industries

U.S. Vapour Recovery Units Market Insight

The U.S. vapour recovery units market captured the largest revenue share in North America in 2025, fueled by strict federal and state regulations on hydrocarbon emissions and growing awareness of energy recovery technologies. Refineries, storage facilities, and chemical plants are increasingly implementing VRUs to improve operational efficiency and reduce environmental impact. The market is further supported by investments in modern recovery systems, increasing adoption of absorption and membrane-based units, and integration of VRUs with existing storage and processing infrastructure.

Europe Vapour Recovery Units Market Insight

The Europe vapour recovery unit market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strict EU directives on VOC emissions and environmental compliance. The region’s emphasis on sustainable industrial operations and adoption of advanced recovery technologies is boosting vapour recovery unit installations. European industries are increasingly integrating vapour recovery units in refineries, chemical plants, and pharmaceutical facilities to minimize losses and comply with environmental standards.

U.K. Vapour Recovery Units Market Insight

The U.K. vapour recovery unit market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by government mandates on emission reductions and the adoption of energy-efficient hydrocarbon recovery solutions. Industrial facilities, especially in oil and gas and chemical sectors, are focusing on minimizing environmental impact and improving resource recovery, which is fueling vapour recovery unit adoption. The country’s advanced industrial infrastructure and focus on sustainability further support the market’s growth.

Germany Vapour Recovery Units Market Insight

The Germany vapour recovery unit market is expected to expand at a considerable CAGR, fueled by growing awareness of emission control, technological advancements in recovery units, and the country’s focus on eco-conscious industrial operations. Refineries and chemical plants are investing in vapour recovery units to enhance hydrocarbon recovery while complying with environmental norms. Integration with advanced process systems and ongoing modernization of industrial infrastructure are contributing to market growth.

Asia-Pacific Vapour Recovery Units Market Insight

The Asia-Pacific vapour recovery unit market is poised to grow at the fastest CAGR during 2026–2033, driven by rapid industrialization, rising energy demand, and strict environmental regulations in countries such as China, Japan, and India. Increasing oil and gas production, landfill gas recovery projects, and pharmaceutical industry expansion are fueling vapour recovery unit adoption. Government initiatives promoting emission reduction and sustainability are further accelerating market growth.

Japan Vapour Recovery Units Market Insight

The Japan vapour recovery unit market is gaining momentum due to the country’s focus on industrial efficiency, strict emission control policies, and technological innovation in recovery systems. Refineries and chemical plants are increasingly installing vapour recovery units to reduce hydrocarbon losses and comply with environmental regulations. The integration of vapour recovery units with advanced monitoring systems and the demand for compact, energy-efficient units are driving growth in both industrial and pharmaceutical sectors.

China Vapour Recovery Units Market Insight

The China vapour recovery unit market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding oil and gas infrastructure, rapid industrialization, and growing focus on emission reduction. China’s push towards sustainable energy recovery, combined with strong domestic manufacturing of vapour recovery units and cost-effective solutions, is encouraging widespread adoption. The development of smart city projects and regulatory enforcement on VOC and GHG emissions are further supporting market expansion.

Vapour Recovery Units Market Share

The vapour recovery units industry is primarily led by well-established companies, including:

- Cool Sorption A/S (Denmark)

- Kilburn Engineering Ltd. (U.K.)

- FLOGISTIX LP (U.S.)

- HY-BON/EDI (U.K.)

- Kappa Gi s.r.l. (Italy)

- Wintek Corporation (U.S.)

- BORSIG GmbH (Germany)

- Zeeco, Inc. (U.S.)

- VOCZero Ltd. (U.K.)

- Cimarron Energy (U.S.)

- ABB (Switzerland)

- Eaton (U.S.)

- Accel Compression Inc. (U.S.)

- Whirlwind Methane Recovery Systems, LLC (U.S.)

- PETROGAS SYSTEMS (U.S.)

- PSG (U.S.)

- S&S Technical, Inc. (U.S.)

- AQT S.R.L (Italy)

- OTA Compression (U.S.)

- Unimac (U.K.)

- Flotech Performance Systems (U.S.)

- Warner Nicholson Engineering, Inc. (U.S.)

- Cimarron Energy Power Service (U.S.)

- PREMATECNICA, S.A. (Spain)

- Petrogas Systems (U.S.)

Latest Developments in Global Vapour Recovery Units Market

- In April 2025, Emerson Electric announced a strategic partnership with Baker Hughes to co‑develop advanced vapour recovery unit and automation solutions, marking a major shift toward highly integrated systems that combine vapor recovery hardware with real‑time data analytics. This collaboration is expected to accelerate adoption of digital vapour recovery units by enabling operators to monitor emissions, optimize performance, and predict maintenance needs, which in turn can reduce downtime, improve compliance with environmental regulations, and lower lifecycle costs for large industrial and energy sector users

- In February 2025, Siemens secured a significant contract to implement automated VRU control and digital performance monitoring systems for Petrobras offshore platforms, reinforcing the trend toward smart, connected vapor recovery infrastructure. By leveraging automation and remote diagnostics, this deployment helps Petrobras enhance emission control, improve energy efficiency, and reduce manual intervention, which signals growing demand for automated VRU solutions in offshore oil and gas operations where reliability and regulatory compliance are critical

- In January 2025, ANDRITZ introduced a new polymer‑carrier membrane VRU technology capable of operating efficiently at moderate temperatures (50–60 °C) with a minimal physical footprint, expanding the potential use cases for vapor recovery beyond large refineries to more compact and space‑limited facilities. This innovation is expected to drive growth in markets such as small terminals, chemical plants, and mobile installations by offering an energy‑efficient, easy‑to‑install alternative to traditional recovery units, thereby broadening the customer base and increasing overall market penetration

- In December 2024, John Zink Hamworthy Combustion completed the acquisition of Clyde Union’s VRU business, significantly expanding its vapor recovery product portfolio and technical capabilities. This strategic move is anticipated to accelerate consolidation within the VRU market, enable the development of more diversified and customizable recovery solutions, and strengthen the company’s ability to offer end‑to‑end emission control systems, which benefits customers seeking integrated, high‑performance technologies

- In September 2024, Schneider Electric launched a next‑generation VRU control platform featuring predictive analytics, remote diagnostics, and enhanced cybersecurity, setting a new standard for intelligent recovery operations. By enabling operators to proactively identify performance issues and optimize system efficiency, this platform supports better regulatory compliance, reduces unplanned outages, and enhances operational safety, which is increasingly important as emission standards tighten globally and industries seek cost‑effective ways to meet environmental targets

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.