Global Veterinary Endoscopy Market

Размер рынка в млрд долларов США

CAGR :

%

USD

253.06 Billion

USD

407.92 Billion

2025

2033

USD

253.06 Billion

USD

407.92 Billion

2025

2033

| 2026 –2033 | |

| USD 253.06 Billion | |

| USD 407.92 Billion | |

| % | |

|

Global Veterinary Endoscopy Market Segmentation, By Product Type (Flexible Endoscopes, Capsule Endoscopes, Robot Assisted Endoscopes, Rigid Endoscope, and Other Endoscopes), Procedure (Flexible Endoscopy, Rigid Endoscopy, and Other Procedures), Animal Type (Companion Animals, Large Animals, and Other Animals), End- User (Hospitals and Academic Institutes, Clinics, Veterinary Hospitals, and Research Institutes) - Industry Trends and Forecast to 2033

Veterinary Endoscopy Market Size

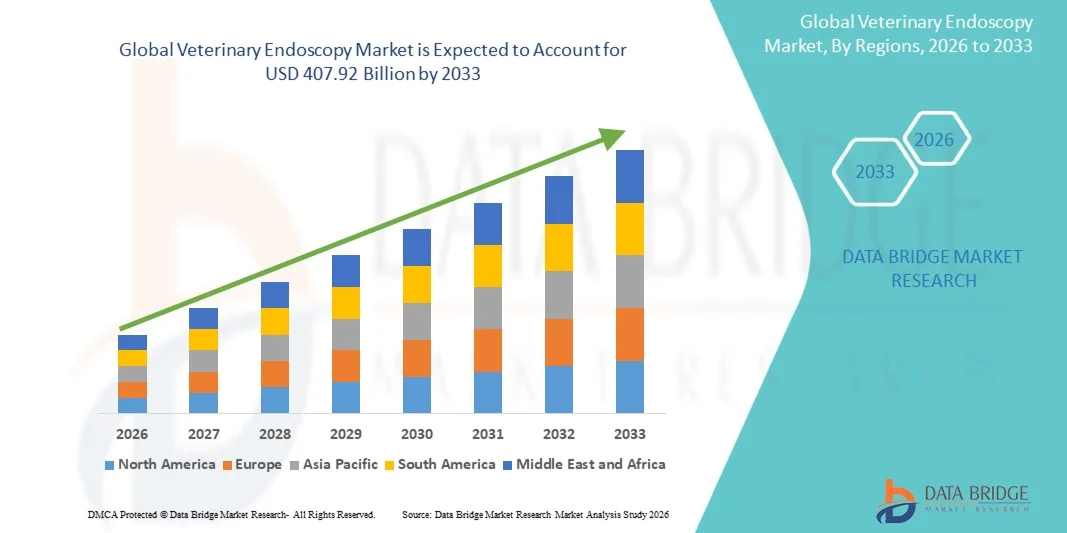

- The global veterinary endoscopy market size was valued at USD 253.06 billion in 2025 and is expected to reach USD 407.92 billion by 2033, at a CAGR of 6.15% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced diagnostic and minimally invasive surgical procedures in veterinary medicine, along with technological advancements in endoscopic imaging systems. Growing pet ownership, rising expenditure on animal healthcare, and improved veterinary infrastructure are contributing to higher demand for veterinary endoscopy solutions across specialty clinics and animal hospitals

- Furthermore, rising awareness among pet owners regarding early disease diagnosis and minimally invasive treatment options is establishing veterinary endoscopy as a preferred diagnostic and therapeutic tool in modern veterinary practice. These converging factors are accelerating the uptake of Veterinary Endoscopy solutions, thereby significantly boosting the industry's growth

Veterinary Endoscopy Market Analysis

- Veterinary endoscopy systems, including rigid and flexible endoscopes, are increasingly vital tools in modern animal healthcare, enabling minimally invasive diagnostic and therapeutic procedures across companion animals and livestock. These systems enhance visualization of internal organs, reduce surgical trauma, and support faster recovery times, making them essential in specialty veterinary practices and advanced animal hospitals

- The escalating demand for veterinary endoscopy is primarily fueled by rising pet ownership, increasing expenditure on companion animal healthcare, growing awareness of minimally invasive surgical options, and advancements in high-definition imaging technologies. In addition, expanding veterinary specialty services and referral centers are further contributing to market growth

- North America dominated the veterinary endoscopy market with the largest revenue share of 42.8% in 2025, driven by advanced veterinary infrastructure, high pet healthcare spending, strong presence of leading veterinary device manufacturers, and increasing adoption of minimally invasive procedures in animal hospitals across the U.S. and Canada

- Asia-Pacific is expected to be the fastest-growing region in the veterinary endoscopy market during the forecast period, projected to expand at a CAGR of 12.9%, supported by rising companion animal adoption, improving veterinary healthcare facilities, growing awareness regarding early disease diagnosis, and increasing investments in animal health across countries such as China, India, Japan, and Australia

- The companion animals segment held the largest market revenue share of 62.4% in 2025, driven by increasing pet ownership globally

Report Scope and Veterinary Endoscopy Market Segmentation

|

Attributes |

Veterinary Endoscopy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Karl Storz SE & Co. KG (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Veterinary Endoscopy Market Trends

“Technological Advancements and Minimally Invasive Innovations in Veterinary Diagnostics”

- A significant and accelerating trend in the global veterinary endoscopy market is the continuous advancement of minimally invasive diagnostic and surgical technologies designed specifically for animal healthcare

- Modern endoscopic systems are increasingly incorporating high-definition imaging, improved illumination systems, and flexible scopes that allow veterinarians to perform precise internal examinations with minimal trauma

- For instance, advanced veterinary endoscopy systems equipped with HD visualization and enhanced maneuverability are being widely adopted in specialty veterinary hospitals to perform procedures such as gastrointestinal examinations, bronchoscopy, and laparoscopy with greater accuracy and reduced recovery time for animals. These innovations are significantly improving diagnostic capabilities and procedural outcomes

- The integration of digital imaging platforms and video recording systems is further enhancing clinical efficiency, enabling better case documentation, real-time consultation, and improved communication with pet owners regarding diagnosis and treatment plans

- This growing emphasis on minimally invasive procedures is reshaping veterinary practice standards, as clinics increasingly prefer endoscopic techniques over traditional open surgeries due to reduced postoperative pain, shorter hospitalization, and faster recovery in companion animals

- Consequently, manufacturers are focusing on developing compact, cost-efficient, and species-specific endoscopic equipment to meet the evolving needs of veterinary professionals

Veterinary Endoscopy Market Dynamics

Driver

“Rising Pet Ownership and Growing Expenditure on Animal Healthcare”

- The increasing global pet population, along with rising awareness regarding animal health and preventive care, is a major driver propelling the Veterinary Endoscopy market. Pet owners are increasingly seeking advanced diagnostic and treatment solutions to ensure early detection and effective management of diseases in companion animals

- For instance, the growing prevalence of gastrointestinal disorders, respiratory conditions, and urogenital diseases in small animals has led veterinary clinics to adopt endoscopic procedures for accurate diagnosis and minimally invasive treatment. The expansion of specialty veterinary hospitals and referral centers is further supporting the demand for advanced endoscopy systems

- Increasing disposable incomes and the humanization of pets have significantly boosted spending on high-quality veterinary care, including advanced imaging and surgical interventions. This trend is particularly prominent in developed regions where pet insurance coverage and access to specialized veterinary services are expanding

- In addition, advancements in veterinary education and training programs are equipping practitioners with the skills required to perform endoscopic procedures effectively, thereby accelerating the adoption of these systems across both urban and semi-urban veterinary facilities

Restraint/Challenge

“High Equipment Costs and Limited Access in Small Clinics”

- The high initial investment required for veterinary endoscopy equipment remains a key challenge, especially for small and independent veterinary clinics with limited financial resources. Advanced endoscopic towers, imaging processors, and specialized instruments involve substantial capital expenditure, which can restrict widespread adoption

- For instance, complete endoscopy setups with high-definition cameras, light sources, and flexible scopes can represent a significant financial burden for smaller practices, often requiring additional maintenance and periodic upgrades that further increase operational costs

- Moreover, the need for specialized training to operate endoscopic systems and interpret findings accurately can act as a barrier, particularly in regions where access to advanced veterinary training programs is limited

- Limited awareness among pet owners in developing economies regarding the benefits of minimally invasive diagnostic procedures may also slow market growth

- Addressing these challenges through cost-effective product innovations, flexible financing options, expanded training initiatives, and awareness programs will be essential to ensure sustainable expansion of the Veterinary Endoscopy market

Veterinary Endoscopy Market Scope

The market is segmented on the basis of product type, procedure, animal type, and end-user.

• By Product Type

On the basis of product type, the Global Veterinary Endoscopy market is segmented into Flexible Endoscopes, Capsule Endoscopes, Robot-Assisted Endoscopes, Rigid Endoscopes, and Other Endoscopes. The flexible endoscopes segment dominated the largest market revenue share of 41.6% in 2025, primarily driven by its extensive application across gastrointestinal, respiratory, and urological examinations in animals. Flexible scopes provide superior maneuverability, enabling deep internal visualization with minimal trauma. Their ability to perform both diagnostic and therapeutic interventions enhances their clinical utility. Increasing prevalence of digestive disorders and foreign body ingestion among companion animals significantly supports demand. Veterinary practitioners prefer flexible systems due to improved patient comfort and faster recovery outcomes. Continuous advancements in high-definition imaging, fiber optics, and video integration further strengthen adoption. Growing pet humanization trends and higher veterinary spending also contribute to revenue expansion. The segment benefits from rising installation in specialty veterinary hospitals and referral centers. Expanding training programs for minimally invasive procedures support equipment penetration. The availability of reusable and cost-effective models increases accessibility in emerging markets. In addition, technological compatibility with digital record systems supports workflow efficiency.

The robot-assisted endoscopes segment is anticipated to witness the fastest CAGR of 19.8% from 2026 to 2033, driven by increasing demand for precision-guided and minimally invasive surgical procedures. Robotic systems enhance dexterity, stability, and visualization during complex interventions. Growing investment in advanced veterinary surgical infrastructure supports technology adoption. These systems reduce procedural complications and improve clinical outcomes. Increasing awareness among veterinary specialists about robotics-based procedures is accelerating growth. Expanding collaborations between device manufacturers and research institutes are fostering innovation. Higher procedural accuracy and reduced recovery time make robotic systems attractive in premium veterinary facilities. Rising demand for specialized animal surgeries further boosts the segment. The growing presence of corporate veterinary hospital chains also encourages procurement of advanced systems. Although initial costs remain high, long-term efficiency benefits promote uptake. Continuous product upgrades and AI integration are expected to sustain strong growth momentum.

• By Procedure

On the basis of procedure, the market is segmented into Flexible Endoscopy, Rigid Endoscopy, and Other Procedures. The flexible endoscopy segment accounted for the largest market revenue share of 47.3% in 2025, attributed to its widespread diagnostic and therapeutic use. Flexible procedures are commonly utilized for gastrointestinal examination, biopsy sampling, and foreign body removal. The increasing incidence of digestive and respiratory disorders among animals drives procedural volume. Minimally invasive nature results in reduced post-operative pain and shorter recovery duration. Growing preference for non-invasive diagnostic approaches among pet owners supports segment dominance. Rising awareness regarding early disease detection enhances utilization rates. Advanced visualization capabilities improve procedural accuracy and clinical confidence. Veterinary specialists increasingly recommend flexible techniques for internal examinations. The segment benefits from favorable reimbursement scenarios in developed markets. Increased training and certification programs further encourage adoption. Technological advancements in scope flexibility and imaging clarity continue to strengthen segment growth.

The rigid endoscopy segment is projected to register the fastest CAGR of 18.5% from 2026 to 2033, supported by rising use in orthopedic, laparoscopic, and thoracoscopic procedures. Rigid scopes provide enhanced durability and superior image resolution. Increasing demand for minimally invasive surgical interventions contributes to segment expansion. Veterinary surgeons prefer rigid systems for precise operative procedures. Growing investments in surgical equipment in veterinary hospitals accelerate adoption. Rising livestock surgical interventions also support growth. Technological refinements in lens systems and lighting improve outcomes. The expansion of specialty animal care centers further fuels demand. Increasing awareness regarding advanced surgical options among animal owners strengthens uptake. Improved training infrastructure enhances practitioner confidence. Collectively, these factors drive rapid CAGR during the forecast period.

• By Animal Type

On the basis of animal type, the market is segmented into Companion Animals, Large Animals, and Other Animals. The companion animals segment held the largest market revenue share of 62.4% in 2025, driven by increasing pet ownership globally. Dogs and cats account for the majority of endoscopic procedures performed. Rising pet humanization trends encourage higher spending on advanced diagnostics. Growing awareness regarding preventive healthcare further boosts demand. Increased prevalence of gastrointestinal and respiratory disorders supports procedural growth. Urbanization and expanding middle-class income levels enhance veterinary service utilization. Pet insurance penetration in developed countries also contributes to adoption. Companion animals frequently undergo minimally invasive procedures, supporting equipment demand. Technological accessibility in urban veterinary hospitals strengthens dominance. Rising adoption of specialty animal clinics further expands revenue share. Continuous innovation tailored for small animal anatomy supports sustained growth.

The large animals segment is expected to witness the fastest CAGR of 17.2% from 2026 to 2033, driven by growing focus on livestock health and productivity. Increasing demand for efficient disease diagnosis in cattle and equine populations supports uptake. Governments emphasize animal health management programs, boosting procedural demand. Rising awareness among livestock owners about advanced diagnostic tools accelerates adoption. Expansion of rural veterinary infrastructure enhances accessibility. Technological advancements in portable endoscopic systems further support market growth. Growing research in equine and bovine healthcare contributes to demand. Increasing global meat and dairy consumption indirectly drives veterinary investments. Preventive care initiatives also strengthen procedural volume. These factors collectively propel strong forecast growth.

• By End-User

On the basis of end-user, the market is segmented into Hospitals and Academic Institutes, Clinics, Veterinary Hospitals, and Research Institutes. The veterinary hospitals segment dominated the market with a revenue share of 38.9% in 2025, attributed to the availability of advanced diagnostic and surgical infrastructure. These facilities handle high patient volumes and complex referral cases. Increasing number of specialty veterinary hospitals supports equipment demand. Skilled professionals and trained surgeons enhance procedural adoption. Availability of advanced imaging systems strengthens operational efficiency. Rising preference for comprehensive care centers among pet owners contributes to revenue growth. Corporate veterinary chains are expanding globally, boosting procurement of modern endoscopy units. Integration of digital systems further improves workflow management. Hospitals often lead in adopting new technologies, maintaining segment leadership. Continuous facility expansion in urban regions supports sustained dominance.

The research institutes segment is projected to witness the fastest CAGR of 20.1% from 2026 to 2033, driven by increasing research activities focused on surgical innovation and disease diagnostics. Academic collaborations with medical device companies foster technological advancements. Growing funding for animal health research enhances equipment procurement. Research centers utilize endoscopic tools for experimental and training purposes. Expanding veterinary education programs increase demand for advanced systems. Innovation in minimally invasive techniques further fuels adoption. Rising emphasis on evidence-based veterinary practice supports procedural growth. Development of next-generation endoscopic platforms contributes to expansion. Increasing global research initiatives in animal welfare also support demand. These factors collectively ensure strong CAGR during the forecast period.

Veterinary Endoscopy Market Regional Analysis

- North America dominated the veterinary endoscopy market with the largest revenue share of 42.8% in 2025, driven by advanced veterinary healthcare infrastructure, high expenditure on pet medical care, and the strong presence of leading veterinary device manufacturers. The increasing adoption of minimally invasive diagnostic and surgical procedures in animal hospitals and specialty clinics across the U.S. and Canada has significantly contributed to regional market growth

- Veterinary professionals in the region are increasingly utilizing endoscopic procedures for the diagnosis and treatment of gastrointestinal, respiratory, and urogenital disorders in companion animals. The availability of skilled veterinarians, well-equipped animal hospitals, and growing pet insurance coverage further supports the widespread adoption of advanced endoscopy systems

- This strong market position is reinforced by rising pet humanization trends, higher disposable incomes, and continuous technological advancements in imaging and minimally invasive surgical tools, establishing North America as a key revenue-generating region in the Veterinary Endoscopy market

U.S. Veterinary Endoscopy Market Insight

The U.S. veterinary endoscopy market captured the largest revenue share in 2025 within North America, supported by a well-developed network of veterinary hospitals and specialty referral centers. The growing prevalence of chronic conditions in companion animals, including gastrointestinal disorders and respiratory diseases, has increased the demand for precise and minimally invasive diagnostic techniques. High awareness among pet owners regarding advanced treatment options and increasing spending on animal healthcare are further driving market expansion. In addition, the presence of established veterinary device manufacturers and ongoing investments in clinical training programs continue to strengthen the U.S. market landscape.

Europe Veterinary Endoscopy Market Insight

The Europe veterinary endoscopy market is projected to expand at a substantial CAGR throughout the forecast period, supported by strong animal welfare regulations and increasing emphasis on high-quality veterinary care. Rising adoption of minimally invasive procedures across countries such as Germany, the U.K., and France is contributing to steady market growth. Furthermore, growing awareness regarding early disease detection and improved postoperative outcomes is encouraging veterinary clinics to invest in advanced endoscopic equipment.

U.K. Veterinary Endoscopy Market Insight

The U.K. veterinary endoscopy market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing pet ownership and expanding veterinary specialty services. The country’s focus on preventive healthcare for companion animals and the presence of structured veterinary education systems are fostering the adoption of modern diagnostic technologies. Growing demand for minimally invasive procedures that reduce recovery time and improve animal comfort is further supporting market growth.

Germany Veterinary Endoscopy Market Insight

The Germany veterinary endoscopy market is expected to expand at a considerable CAGR during the forecast period, fueled by strong veterinary infrastructure and increasing investments in advanced medical technologies for animals. Germany’s emphasis on high clinical standards and precision-based treatment approaches is encouraging veterinary hospitals to adopt high-definition endoscopic systems. In addition, rising pet insurance penetration and structured disease management programs are contributing to sustained market expansion.

Asia-Pacific Veterinary Endoscopy Market Insight

The Asia-Pacific veterinary endoscopy market is poised to grow at the fastest CAGR of 12.9% during the forecast period of 2026 to 2033, supported by rising companion animal adoption, improving veterinary healthcare facilities, and increasing awareness regarding early disease diagnosis. Expanding urbanization and growing disposable incomes in countries such as China, India, Japan, and Australia are driving higher spending on animal healthcare services. Moreover, increasing investments in veterinary infrastructure and training programs are strengthening the adoption of minimally invasive diagnostic and surgical solutions across the region.

Japan Veterinary Endoscopy Market Insight

The Japan veterinary endoscopy market is gaining steady momentum due to high pet ownership rates and growing demand for advanced animal healthcare services. The country’s focus on quality medical care and technological sophistication is promoting the use of minimally invasive endoscopic procedures in veterinary clinics. In addition, Japan’s aging pet population is increasing the need for accurate diagnostic solutions to manage chronic and age-related conditions effectively.

China Veterinary Endoscopy Market Insight

The China veterinary endoscopy market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid growth in pet ownership, expanding middle-class population, and rising awareness regarding animal health. The modernization of veterinary hospitals and increasing availability of advanced diagnostic equipment are accelerating market penetration. Strong domestic manufacturing capabilities and growing investments in veterinary education and specialty services are key factors propelling sustained growth of the Veterinary Endoscopy market in China.

Veterinary Endoscopy Market Share

The Veterinary Endoscopy industry is primarily led by well-established companies, including:

• Karl Storz SE & Co. KG (Germany)

• Olympus Corporation (Japan)

• FUJIFILM Holdings Corporation (Japan)

• Stryker Corporation (U.S.)

• Richard Wolf GmbH (Germany)

• Medtronic plc (Ireland)

• Smith & Nephew plc (U.K.)

• B. Braun Melsungen AG (Germany)

• Biovision Veterinary Endoscopy, LLC (U.S.)

• Dr. Fritz Endoscopes GmbH (Germany)

• MDS Incorporated (U.S.)

• Endoscope-i Ltd. (U.K.)

• Optomed Oy (Finland)

• Ambu A/S (Denmark)

• VetVu (U.S.)

• Jorgensen Laboratories (U.S.)

• AVS Endoscopy (U.S.)

• XION GmbH (Germany)

• ConMed Corporation (U.S.)

• Hugemed Medical (China)

Latest Developments in Global Veterinary Endoscopy Market

- In November 2024, Boston Scientific Corporation entered into a strategic partnership with Ethicon Animal Health (Johnson & Johnson) to co-develop advanced veterinary endoscopic solutions for large animals, combining Boston Scientific’s endoscopy technology with Ethicon’s veterinary product expertise

- In February 2025, Olympus Corporation completed the acquisition of EndoTech, a U.S. veterinary endoscope manufacturer, strengthening its veterinary imaging and endoscopy product portfolio and expanding its presence in the animal healthcare segment

- In May 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to the VIDA 1.9 mm veterinary endoscope by Karl Storz GmbH & Co. KG, enabling the device’s clinical use for accessing hard-to-reach areas in small animal procedures and improving diagnostic precision

- In June 2025, JeetVet showcased the RAE-500 Portable Smart Veterinary Otoscope and RAE-105 Portable USB Veterinary Endoscope at the ACVIM Forum in Louisville, Kentucky. These portable, high-resolution devices featured enhanced wireless connectivity and ergonomic design, highlighting the trend toward mobile, user-friendly endoscopic solutions for general and specialty veterinary practitioners

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.