Global Zig Bee Automation Market

Размер рынка в млрд долларов США

CAGR :

%

USD

32.03 Billion

USD

79.30 Billion

2025

2033

USD

32.03 Billion

USD

79.30 Billion

2025

2033

| 2026 –2033 | |

| USD 32.03 Billion | |

| USD 79.30 Billion | |

| % | |

|

Global Zig-Bee Automation Market Segmentation, By Product (Zigbee Home Automation, Zigbee Light Link, Zigbee Smart Energy and Others), Application (Smart Homes, Connected Light, Utility and Retail Services)- Industry Trends and Forecast to 2033

Zig-Bee Automation Market Size

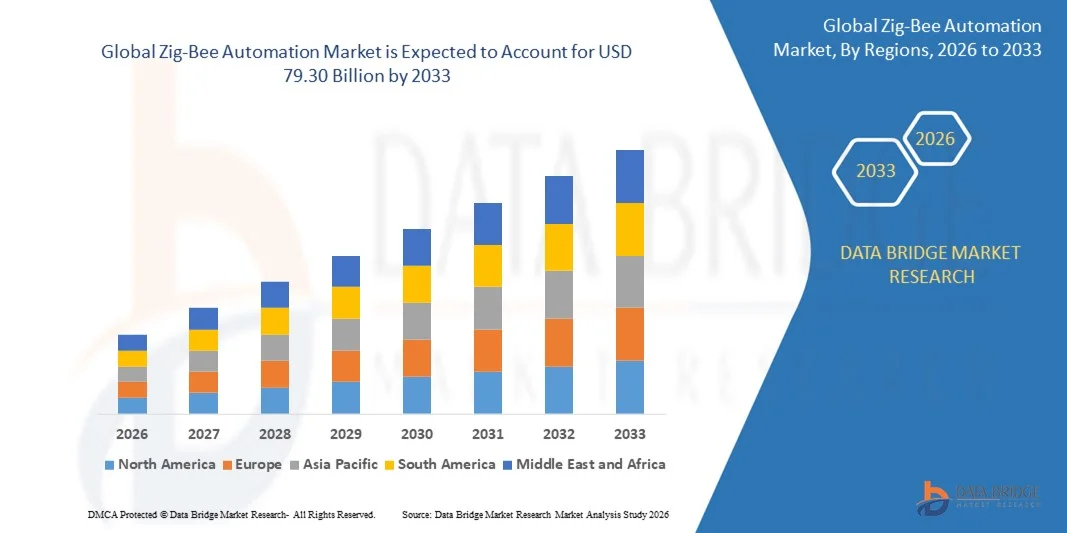

- The global zig-bee automation market size was valued at USD 32.03 billion in 2025 and is expected to reach USD 79.30 billion by 2033, at a CAGR of 12.00% during the forecast period

- The market growth is largely fuelled by the increasing adoption of smart home devices, industrial automation solutions, and IoT-enabled applications

- Rising demand for energy-efficient, low-power, and reliable wireless communication systems is further driving the market

Zig-Bee Automation Market Analysis

- The market is witnessing strong growth due to the widespread integration of zig-bee protocols in consumer electronics, lighting systems, and industrial applications

- Technological advancements, such as improved mesh networking, enhanced security features, and interoperability with other wireless protocols, are contributing to market development

- North America dominated the zig-bee automation market with the largest revenue share of 42.15% in 2025, driven by the growing adoption of smart home devices, industrial automation solutions, and IoT-enabled applications

- Asia-Pacific region is expected to witness the highest growth rate in the global zig-bee automation market, driven by rapid technological advancements, growing disposable incomes, and expansion of smart home and industrial IoT deployments

- The Zigbee Home Automation segment held the largest market revenue share in 2025, driven by increasing adoption of connected devices for home security, lighting, and climate control. Zigbee home automation solutions offer seamless interoperability, low-power consumption, and reliable network connectivity, making them a preferred choice for residential users

Report Scope and Zig-Bee Automation Market Segmentation

|

Attributes |

Zig-Bee Automation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Zig-Bee Automation Market Trends

Rising Adoption of Smart Devices and Wireless Connectivity

- The growing focus on connected homes and industrial automation is significantly shaping the zig-bee automation market, as consumers and businesses increasingly prefer reliable, low-power wireless solutions. Zig-bee technology is gaining traction due to its ability to enable seamless communication between devices while maintaining energy efficiency and network stability. This trend strengthens adoption across smart homes, commercial buildings, and industrial IoT applications, encouraging manufacturers to innovate with new products and solutions that cater to evolving connectivity needs

- Increasing awareness around energy management, operational efficiency, and remote monitoring has accelerated the demand for zig-bee automation in lighting, HVAC, security, and smart appliance systems. Consumers and enterprises are actively seeking scalable and interoperable wireless solutions, prompting device manufacturers to prioritize zig-bee compatibility and network optimization

- Energy efficiency and sustainability trends are influencing purchasing decisions, with organizations and consumers emphasizing reduced power consumption, eco-friendly deployments, and compliance with wireless communication standards. These factors help differentiate products in a competitive market and build trust, while also driving the adoption of certified zig-bee-enabled devices

- For instance, in 2024, Philips Lighting in the U.S. and Schneider Electric in France expanded their smart lighting and building automation portfolios by integrating zig-bee modules in residential and commercial solutions. These deployments were introduced in response to rising demand for energy-efficient, connected devices, with distribution across retail, online, and professional installation channels

- While demand for zig-bee automation is growing, sustained market expansion depends on continuous R&D, cost-effective module production, and maintaining reliable performance across large-scale networks. Manufacturers are also focusing on improving interoperability with other wireless standards, network security, and scalable deployment solutions for broader adoption

Zig-Bee Automation Market Dynamics

Driver

Growing Preference for Connected, Low-Power Wireless Solutions

- Rising consumer and enterprise demand for smart homes, industrial automation, and IoT connectivity is a major driver for the zig-bee automation market. Manufacturers are increasingly integrating zig-bee modules into devices to enable low-power, secure, and reliable wireless communication while supporting scalable network topologies

- Expanding applications in lighting, HVAC, security, and industrial monitoring are influencing market growth. Zig-bee technology helps enhance operational efficiency, remote control, and energy management while maintaining interoperability with multiple devices and platforms. Increasing adoption of smart cities and intelligent building systems globally further reinforces this trend

- Device manufacturers are actively promoting zig-bee-enabled solutions through product innovation, marketing campaigns, and industry certifications. These efforts are supported by growing demand for energy-efficient, automated, and remotely controllable systems, and they also encourage partnerships between technology providers, device manufacturers, and service integrators

- For instance, in 2023, Samsung SmartThings in South Korea and Honeywell in the U.S. reported increased incorporation of zig-bee modules in lighting, HVAC, and security solutions. This expansion followed higher demand for connected, low-power wireless systems, driving repeat adoption and product differentiation. Both companies also highlighted energy efficiency and interoperability in marketing campaigns to strengthen brand credibility

- Although rising connected device adoption supports growth, wider implementation depends on cost optimization, regulatory compliance, and network scalability. Investment in reliable chipsets, standardized protocols, and advanced software solutions will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Implementation Cost and Interoperability Issues

- The relatively higher cost of zig-bee modules compared to traditional wireless solutions remains a key challenge, limiting adoption among price-sensitive manufacturers. Chipset costs, certification fees, and integration complexity contribute to elevated pricing. In addition, inconsistent network performance in multi-vendor environments can further affect adoption rates

- Consumer and enterprise awareness of zig-bee benefits remains uneven, particularly in developing markets where smart device penetration is still emerging. Limited understanding of network reliability and energy-saving advantages restricts adoption across certain applications. This also leads to slower innovation uptake in emerging economies where educational initiatives on zig-bee technology are minimal

- Integration and interoperability challenges also impact market growth, as zig-bee networks require compatibility with existing systems and adherence to wireless standards. Technical complexities, network security concerns, and firmware updates increase operational efforts. Companies must invest in robust testing, certification, and support infrastructure to ensure seamless performance

- For instance, in 2024, distributors in India and Thailand supplying smart home and industrial automation brands such as Philips and Schneider Electric reported slower uptake due to higher module costs and limited awareness of zig-bee advantages compared to Wi-Fi or Bluetooth solutions. Integration challenges with legacy devices and certification compliance were additional barriers

- Overcoming these challenges will require cost-efficient production, expanded educational initiatives for manufacturers and end-users, and enhanced interoperability solutions. Collaboration with device manufacturers, standardization bodies, and IoT platform providers can help unlock the long-term growth potential of the global zig-bee automation market. Furthermore, developing scalable, secure, and energy-efficient modules while strengthening marketing strategies around functional and sustainability benefits will be essential for widespread adoption

Zig-Bee Automation Market Scope

The market is segmented on the basis of product and application.

- By Product

On the basis of product, the zig-bee automation market is segmented into Zigbee Home Automation, Zigbee Light Link, Zigbee Smart Energy, and Others. The Zigbee Home Automation segment held the largest market revenue share in 2025, driven by increasing adoption of connected devices for home security, lighting, and climate control. Zigbee home automation solutions offer seamless interoperability, low-power consumption, and reliable network connectivity, making them a preferred choice for residential users.

The Zigbee Light Link segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for energy-efficient smart lighting systems and scalable wireless control solutions. Zigbee Light Link-enabled devices are particularly popular for their ease of installation, remote management capabilities, and compatibility with multiple lighting brands, supporting both new installations and retrofits.

- By Application

On the basis of application, the market is segmented into Smart Homes, Connected Light, Utility, and Retail Services. The Smart Homes segment dominated in 2025 due to increasing consumer preference for automated home environments that integrate lighting, HVAC, security, and entertainment systems. Smart home applications leverage Zigbee technology for reliable, low-power wireless communication and simplified device management.

The Connected Light segment is projected to witness the highest growth from 2026 to 2033, supported by growing demand for energy-efficient lighting solutions, smart city initiatives, and advanced building automation systems. Zigbee-enabled connected lighting provides flexible control, scheduling, and integration with other smart devices, making it increasingly popular across residential, commercial, and industrial spaces.

Zig-Bee Automation Market Regional Analysis

- North America dominated the zig-bee automation market with the largest revenue share of 42.15% in 2025, driven by the growing adoption of smart home devices, industrial automation solutions, and IoT-enabled applications

- Consumers and businesses in the region highly value the energy efficiency, low-power consumption, and reliable wireless connectivity offered by zig-bee-enabled devices for home automation, lighting, HVAC, and security systems

- This widespread adoption is further supported by high disposable incomes, a technology-savvy population, and government initiatives promoting smart infrastructure, establishing zig-bee automation as a preferred solution across residential, commercial, and industrial sectors

U.S. Zig-Bee Automation Market Insight

The U.S. zig-bee automation market captured the largest revenue share in 2025 within North America, fueled by rapid adoption of connected devices and smart building solutions. Consumers and enterprises are increasingly prioritizing energy-efficient wireless communication, remote monitoring, and device interoperability. The growing demand for smart homes, industrial IoT applications, and voice-controlled systems further propels the zig-bee automation market. Moreover, integration with platforms such as Amazon Alexa, Google Assistant, and Apple HomeKit is significantly contributing to market expansion.

Europe Zig-Bee Automation Market Insight

The Europe zig-bee automation market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent energy efficiency regulations and the increasing need for connected industrial and residential solutions. Rising urbanization and the adoption of smart devices are fostering zig-bee deployments. European consumers and businesses are drawn to the convenience, remote control, and energy savings provided by zig-bee technology. The region is experiencing notable growth across smart homes, commercial buildings, and industrial applications, with zig-bee systems being incorporated in both new constructions and modernization projects.

U.K. Zig-Bee Automation Market Insight

The U.K. zig-bee automation market is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand for smart home automation, energy-efficient lighting, and industrial IoT solutions. Concerns regarding energy consumption, operational efficiency, and sustainability are encouraging households and businesses to adopt zig-bee-enabled systems. The U.K.’s robust e-commerce and smart device infrastructure is expected to continue stimulating market growth.

Germany Zig-Bee Automation Market Insight

The Germany zig-bee automation market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising awareness of energy efficiency, digital building management, and industrial automation. Germany’s strong industrial base and emphasis on sustainable, technology-driven solutions promote zig-bee adoption, particularly in residential, commercial, and industrial buildings. Integration of zig-bee systems with smart grids, lighting, and HVAC solutions is becoming increasingly prevalent, supported by local consumer preference for reliable and eco-conscious technologies.

Asia-Pacific Zig-Bee Automation Market Insight

The Asia-Pacific zig-bee automation market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, increasing disposable incomes, and technological advancements in countries such as China, Japan, and India. The region's rising inclination towards smart homes and industrial automation, along with government initiatives promoting digitalization, is accelerating zig-bee adoption. Furthermore, as APAC becomes a manufacturing hub for zig-bee modules and IoT components, affordability and accessibility are expanding the market to a broader consumer base.

Japan Zig-Bee Automation Market Insight

The Japan zig-bee automation market is expected to witness strong growth from 2026 to 2033 due to the country’s high-tech culture, demand for connected homes, and energy-efficient automation solutions. Japanese consumers and businesses emphasize reliability and interoperability, driving adoption of zig-bee-enabled smart home, industrial, and lighting systems. Integration with IoT platforms and building management systems, combined with aging population needs for easier-to-use and automated solutions, is fueling market growth.

China Zig-Bee Automation Market Insight

The China zig-bee automation market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and high rates of technological adoption. China is one of the largest markets for smart devices, with zig-bee technology increasingly adopted in residential, commercial, and industrial applications. Government-led smart city initiatives, availability of cost-effective zig-bee modules, and strong domestic manufacturing capabilities are key factors propelling market growth in China.

Zig-Bee Automation Market Share

The Zig-Bee Automation industry is primarily led by well-established companies, including:

- Digi International Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- Renesas Electronics Corporation (Japan)

- Microchip Technologies (U.S.)

- STMicroelectronics (Switzerland)

- Texas Instruments Incorporated (U.S.)

- GreenPeak Technologies (Netherlands)

- Silicon Laboratories (U.S.)

- Atmel Corporation (U.S.)

- AAC Technologies (China)

- Itron Inc. (U.S.)

- Tendril Networks, Inc. (U.S.)

- Freescale Semiconductor, Inc. (U.S.)

- Aclara Technologies LLC (U.S.)

- Energate Inc. (U.S.)

- Legrand (France)

- Melange Systems Private Limited (India)

- MMB Networks (U.S.)

- OKi Electric Industry Co., Ltd. (Japan)

- SENA Technologies, Inc. (U.S.)

- Profile Systems Holdings (U.K.)

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.