Middle East And Africa Active Medical Implantable Devices Market

Размер рынка в млрд долларов США

CAGR :

%

USD

826.38 Million

USD

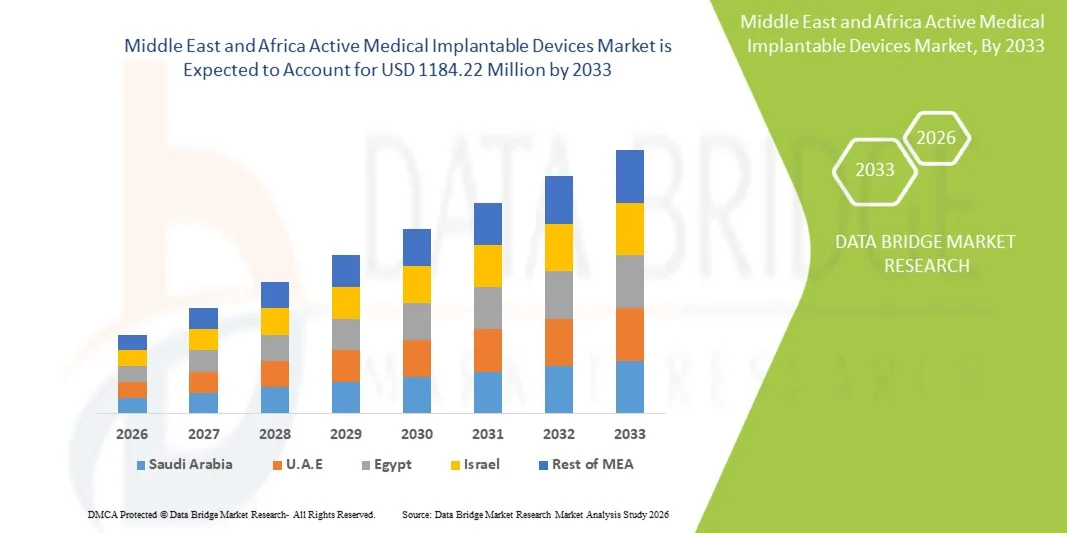

1,184.22 Million

2025

2033

USD

826.38 Million

USD

1,184.22 Million

2025

2033

| 2026 –2033 | |

| USD 826.38 Million | |

| USD 1,184.22 Million | |

| % | |

|

Сегментация рынка активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке по продуктам (устройства для сердечной ресинхронизационной терапии (CRT-D), имплантируемые кардиовертеры-дефибрилляторы, имплантируемые кардиостимуляторы, глазные имплантаты, нейростимуляторы, активные имплантируемые слуховые аппараты, устройства вспомогательной поддержки желудочков, имплантируемые кардиомониторы/вставляемые петлевые регистраторы, брахитерапия, имплантируемые глюкометры, имплантаты для лечения синдрома опущенной стопы, плечевые имплантаты, имплантируемые инфузионные насосы и имплантируемые аксессуары), типу хирургического вмешательства (традиционные хирургические методы и малоинвазивная хирургия), процедуре (нейрососудистая, сердечно-сосудистая, слуховая и другие), конечным пользователям (больницы, специализированные клиники, амбулаторные хирургические центры и клиники) - тенденции отрасли и прогноз до 2033 года.

Размер рынка активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке

- Объем рынка активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке в 2025 году оценивался в 826,38 млн долларов США и, как ожидается, достигнет 1184,22 млн долларов США к 2033 году , демонстрируя среднегодовой темп роста в 4,60% в течение прогнозируемого периода.

- Рост рынка в значительной степени обусловлен увеличением распространенности хронических заболеваний, старением населения и непрерывным технологическим прогрессом в области активных медицинских имплантируемых устройств, таких как кардиостимуляторы, имплантируемые кардиовертеры-дефибрилляторы, нейростимуляторы и имплантируемые системы доставки лекарств, что приводит к улучшению результатов лечения пациентов и долгосрочного контроля заболеваний.

- Кроме того, растущий спрос на малоинвазивные методы лечения, повышенную надежность устройств, увеличенный срок службы батарей и улучшенную интеграцию цифровых медицинских технологий превращают активные имплантируемые медицинские устройства в важнейшие решения в современной системе здравоохранения. Эти факторы в совокупности ускоряют внедрение активных имплантируемых медицинских устройств, тем самым значительно стимулируя рост отрасли.

Анализ рынка активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке

- Активные имплантируемые медицинские устройства, включая кардиостимуляторы, имплантируемые кардиовертеры-дефибрилляторы (ИКД), нейростимуляторы и имплантируемые системы доставки лекарств, становятся все более важными компонентами современной системы здравоохранения благодаря своей способности непрерывно контролировать, регулировать и лечить хронические и угрожающие жизни заболевания с высокой точностью и долгосрочной надежностью.

- Растущий спрос на активные имплантируемые медицинские устройства в первую очередь обусловлен увеличением распространенности сердечно-сосудистых и неврологических заболеваний, старением населения и растущим предпочтением малоинвазивных и технологически продвинутых методов лечения, улучшающих результаты лечения и качество жизни пациентов.

- Саудовская Аравия доминировала на рынке активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке, занимая наибольшую долю выручки в размере приблизительно 35,4% в 2025 году. Это обусловлено значительными государственными инвестициями в инфраструктуру здравоохранения, расширением сети больниц третичного уровня и растущим внедрением передовых технологий кардиологической и неврологической имплантации, поддерживаемых национальными инициативами по модернизации здравоохранения.

- Ожидается, что в прогнозируемый период ОАЭ станут самой быстрорастущей страной на рынке активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке, чему способствуют быстрое расширение частных медицинских учреждений, рост медицинского туризма, увеличение доступности специализированных кардиологических и неврологических центров, а также растущее внедрение технологически продвинутых имплантируемых методов лечения.

- В 2025 году на традиционные хирургические методы приходилась наибольшая доля выручки — 61,9%, что обусловлено их многолетним клиническим признанием и доступностью в широком спектре медицинских учреждений по всему миру.

Обзор отчета и сегментация рынка активных медицинских имплантируемых устройств на Ближнем Востоке и в Африке

|

Атрибуты |

Ключевые рыночные тенденции в сегменте имплантируемых медицинских устройств на Ближнем Востоке и в Африке. |

|

Охваченные сегменты |

|

|

Охваченные страны |

Ближний Восток и Африка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных, представляющие добавленную стоимость |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Active Medical Implantable Devices Market Trends

“Advancements in Miniaturization and Remote Monitoring Integration”

- A key and accelerating trend in the Middle East and Africa Active Medical Implantable Devices Market is the rapid advancement in device miniaturization combined with integrated remote monitoring capabilities, enabling more efficient long-term patient management

- For instance, next-generation implantable cardiac rhythm management devices and neurostimulators are increasingly designed with compact form factors, allowing minimally invasive implantation procedures and improved patient comfort

- Modern implantable devices are now frequently equipped with wireless telemetry systems that enable continuous transmission of physiological data to healthcare providers, supporting real-time monitoring and early detection of complications

- Integration with digital health platforms allows clinicians to remotely adjust therapy settings, monitor device performance, and assess patient adherence without requiring frequent in-person visits, improving clinical outcomes and operational efficiency

- Furthermore, the adoption of cloud-connected implantable monitoring systems is facilitating predictive healthcare approaches, enabling physicians to identify disease progression patterns and intervene earlier

- As healthcare systems worldwide increasingly emphasize remote patient monitoring and value-based care, the demand for compact, connected implantable medical technologies is expected to expand significantly across cardiovascular, neurological, and orthopedic applications

Middle East and Africa Active Medical Implantable Devices Market Dynamics

Driver

“Rising Prevalence of Chronic Diseases and Aging Population”

- The growing global burden of chronic diseases such as cardiovascular disorders, neurological conditions, and diabetes is a major driver accelerating demand for active medical implantable devices

- For instance, the increasing incidence of arrhythmias, heart failure, Parkinson’s disease, and chronic pain conditions is leading to higher adoption of implantable pacemakers, defibrillators, neurostimulators, and drug-delivery systems

- The rapidly expanding geriatric population, which is more susceptible to chronic and degenerative diseases, is further fueling the need for long-term therapeutic implant solutions that provide continuous treatment and monitoring

- Technological improvements that enhance device longevity, battery efficiency, and therapeutic precision are also encouraging physicians to recommend implantable therapies as preferred treatment options over repeated surgical or pharmacological interventions

- In addition, improved reimbursement frameworks and expanding healthcare infrastructure in emerging economies are increasing patient access to implantable device therapies, contributing to sustained market growth during the forecast period

Restraint/Challenge

“High Procedure Costs and Stringent Regulatory Requirements”

- High overall treatment costs, including device prices, surgical implantation procedures, and post-operative care, remain a significant barrier to widespread adoption, particularly in cost-sensitive healthcare markets

- For instance, implantable cardiac devices and neurostimulation systems often involve substantial upfront expenses, limiting accessibility for uninsured or underinsured patient populations in several regions

- Stringent regulatory approval processes for implantable medical technologies also present challenges for manufacturers, as extensive clinical trials and long evaluation timelines increase development costs and delay product commercialization

- Concerns related to device safety, long-term reliability, and potential complications such as infections or device malfunctions further necessitate rigorous compliance requirements, increasing operational complexity for companies

- Addressing these challenges through cost-effective manufacturing strategies, improved reimbursement coverage, and streamlined regulatory pathways will be critical to ensuring broader accessibility and sustained expansion of the Middle East and Africa Active Medical Implantable Devices Market

Middle East and Africa Active Medical Implantable Devices Market Scope

The market is segmented on the basis of product, surgery type, procedure, and end user.

• By Product

On the basis of product, the Medical Implantable Devices market is segmented into Cardiac Resynchronization Therapy Devices (CRT-D), Implantable Cardioverter Defibrillators, Implantable Cardiac Pacemakers, Eye Implants, Neurostimulators, Active Implantable Hearing Devices, Ventricular Assist Devices, Implantable Heart Monitors/Insertable Loop Recorders, Brachytherapy, Implantable Glucose Monitors, Dropped Foot Implants, Shoulder Implants, Implantable Infusion Pumps, and Implantable Accessories. Implantable Cardiac Pacemakers dominated the market with a revenue share of 28.6% in 2025, driven by the increasing global prevalence of arrhythmias and aging populations requiring long-term cardiac rhythm management. Pacemakers remain one of the most widely implanted cardiac devices due to their clinical reliability, established reimbursement frameworks, and continuous technological advancements such as MRI-compatible and leadless pacemakers. Healthcare providers increasingly prefer next-generation pacemakers offering extended battery life, wireless monitoring, and improved patient safety. The strong adoption across both developed and emerging economies further contributes to the segment’s dominance. Rising awareness regarding early cardiac disease detection and growing screening programs also support procedural growth. In addition, the integration of remote patient monitoring systems enhances long-term patient outcomes, encouraging physician preference. Government healthcare initiatives aimed at cardiovascular disease management also increase implantation rates. The widespread availability of trained cardiac specialists and procedural infrastructure supports steady utilization. Technological innovations that reduce procedural complexity further strengthen adoption trends. Increasing hospital procurement volumes and strong manufacturer investments also drive revenue growth. Continuous upgrades and replacement cycles for older pacemaker systems further sustain demand. As cardiovascular diseases remain a leading cause of mortality globally, pacemakers are expected to maintain a strong market position over the forecast period.

Neurostimulators are expected to witness the fastest growth with a projected CAGR of 9.7% from 2026 to 2033, driven by expanding applications in chronic pain management, Parkinson’s disease, epilepsy, and spinal cord injuries. Increasing neurological disorder prevalence globally is significantly boosting demand for advanced neuromodulation therapies. Continuous technological developments, including rechargeable batteries, miniaturized implants, and adaptive stimulation systems, are improving treatment effectiveness and patient acceptance. Rising awareness among clinicians and patients regarding minimally invasive neuromodulation procedures is also encouraging adoption. Favorable reimbursement coverage in developed healthcare systems supports market expansion. Growing investments in neuroscience research and product innovation by major medical device manufacturers further accelerate adoption. Increasing preference for drug-free long-term pain management solutions also contributes to rising demand. Expansion of specialized neurology treatment centers worldwide is strengthening procedural accessibility. Improvements in device precision and programmable stimulation features enhance treatment outcomes, driving physician preference. In addition, aging populations prone to neurological disorders continue to create a strong patient pool. Regulatory approvals for new neuromodulation indications are expected to expand clinical usage significantly. These combined factors position neurostimulators as the fastest-growing product segment in the forecast period.

• By Surgery Type

On the basis of surgery type, the market is segmented into Traditional Surgical Methods and Minimally Invasive Surgery. Traditional surgical methods accounted for the largest revenue share of 61.9% in 2025, supported by their long-standing clinical acceptance and availability across a wide range of healthcare facilities globally. Many complex implantable device procedures, particularly advanced cardiovascular and orthopedic implants, still require open surgical techniques to ensure precise placement and optimal outcomes. Hospitals with established surgical infrastructure and experienced surgical teams continue to rely on conventional procedures for complicated cases. In addition, reimbursement frameworks in several regions remain more aligned with traditional surgical practices, supporting their continued utilization. The presence of standardized surgical protocols further enhances clinician confidence in these methods. Emerging economies with limited access to advanced minimally invasive equipment also contribute significantly to traditional procedure volumes. Complex device implantation involving multiple surgical steps often necessitates open surgical approaches, maintaining demand stability. Training programs for surgeons have historically focused on conventional procedures, reinforcing procedural familiarity. Certain high-risk patients also require open surgery for improved monitoring and control during implantation. Furthermore, cost considerations in developing healthcare systems often favor traditional procedures over advanced minimally invasive technologies. The continued necessity of these approaches for specific clinical indications ensures sustained segment dominance throughout the forecast period.

Прогнозируется, что малоинвазивная хирургия будет расти самыми быстрыми темпами, демонстрируя среднегодовой темп роста в 10,6% в период с 2026 по 2033 год, что обусловлено растущим спросом на сокращение времени восстановления, снижение хирургической травматизации и уменьшение затрат на госпитализацию. Технологические достижения в области визуализации, роботизированной хирургии и катетерной имплантации способствуют более широкому внедрению малоинвазивных процедур. Пациенты все чаще предпочитают малоинвазивные процедуры из-за более быстрой реабилитации и улучшенных косметических результатов. Медицинские учреждения также продвигают эти подходы, поскольку они снижают количество осложнений и затраты на послеоперационный уход. Растущая доступность специализированных программ обучения малоинвазивной хирургии способствует внедрению этих методов врачами. Производители медицинских устройств разрабатывают имплантаты, специально оптимизированные для катетерной или малоинвазивной имплантации, что еще больше способствует расширению сегмента. Рост инвестиций в передовую хирургическую инфраструктуру в здравоохранении ускоряет доступность во всем мире. Кроме того, благоприятная политика возмещения расходов на малоинвазивные процедуры в ряде развитых стран стимулирует их внедрение. Непрерывные инновации в роботизированных хирургических платформах еще больше повышают точность и успешность процедур. Расширение сети амбулаторных хирургических центров, оснащенных оборудованием для малоинвазивных операций, также способствует росту числа проводимых процедур. Повышение осведомленности пациентов о хирургических альтернативах стимулирует ускорение спроса. В совокупности эти факторы позволяют рассматривать малоинвазивную хирургию как наиболее быстрорастущий сегмент хирургической практики в прогнозируемый период.

• По процедуре

В зависимости от вида процедуры рынок сегментируется на нейрососудистые, сердечно-сосудистые, слуховые и другие. Сердечно-сосудистые процедуры доминировали на рынке с долей выручки в 44,3% в 2025 году, что обусловлено высокой распространенностью в мире сердечных заболеваний, требующих имплантации кардиоустройств, таких как кардиостимуляторы, дефибрилляторы, устройства вспомогательного кровообращения и кардиомониторы. Рост заболеваемости гипертонией, ишемической болезнью сердца и нарушениями сердечного ритма значительно способствует увеличению объема процедур. Постоянное совершенствование технологий имплантации кардиоустройств улучшает клинические результаты и стимулирует внедрение процедур врачами. Государственные инициативы, направленные на снижение смертности от сердечно-сосудистых заболеваний, также способствуют расширению числа процедур. Наличие специализированных кардиологических больниц и квалифицированных кардиологов дополнительно стимулирует рост числа процедур. Расширение охвата медицинского страхования кардиологическими процедурами в различных регионах способствует доступности. Старение населения, особенно в развитых странах, значительно увеличивает спрос со стороны пациентов. Технологические инновации, такие как системы дистанционного мониторинга сердечной деятельности, также увеличивают долгосрочное использование имплантируемых кардиоустройств. Повышение осведомленности о ранней диагностике и профилактических кардиологических программах дополнительно способствует росту числа имплантаций. Постоянный выпуск новых продуктов и модернизация устройств поддерживают циклы спроса на замену. Высокая клиническая необходимость имплантации кардиостимуляторов обеспечивает сохранение доминирующего положения кардиохирургических процедур.

Прогнозируется, что нейроваскулярные процедуры продемонстрируют самый быстрый рост, увеличиваясь на 9,9% в год в период с 2026 по 2033 год, что обусловлено растущей распространенностью неврологических расстройств, таких как инсульт, эпилепсия и болезнь Паркинсона. Значительный рост числа процедур обусловлен растущим использованием нейростимуляторов и современных нейроваскулярных имплантатов для терапевтического лечения. Непрерывные технологические достижения, позволяющие точно воздействовать на нейроны и программируемую стимуляцию, повышают показатели клинической эффективности. Растущая осведомленность неврологов об эффективности нейромодуляционной терапии ускоряет ее внедрение. Расширение инвестиций в нейробиологические исследования также способствует появлению новых методов лечения. Увеличение численности пожилого населения, подверженного неврологическим заболеваниям, еще больше расширяет базу пациентов. Благоприятная система возмещения затрат на нейромодуляционную терапию на ряде развитых рынков стимулирует ее применение. Рост числа специализированных неврологических центров по всему миру повышает доступность процедур. Малоинвазивные методы имплантации еще больше повышают предпочтение пациентов к нейроваскулярным вмешательствам. Ожидается, что рост числа клинических исследований, изучающих новые показания к применению нейромодуляции, расширит сферу применения лечения. Усиление сотрудничества между производителями устройств и медицинскими учреждениями также способствует внедрению этих методов. В совокупности эти факторы делают нейроваскулярные процедуры самым быстрорастущим сегментом в прогнозируемый период.

• Конечным пользователем

В зависимости от конечного пользователя рынок сегментируется на больницы, специализированные клиники, амбулаторные хирургические центры и клиники. Больницы занимали наибольшую долю выручки в 2025 году – 58,7%, в основном благодаря развитой хирургической инфраструктуре, наличию многопрофильных специалистов и возможности проведения сложных имплантационных процедур, требующих интенсивного послеоперационного наблюдения. Большинство операций по имплантации устройств, особенно сердечно-сосудистых и неврологических, проводятся в больничных условиях из-за необходимости в современных системах визуализации и отделениях неотложной помощи. Больницы также обслуживают больший поток пациентов, что вносит значительный вклад в количество проводимых процедур. Благоприятные системы возмещения расходов часто поддерживают процедуры, проводимые в больницах, что укрепляет доминирование сегмента. Кроме того, больницы, как правило, поддерживают долгосрочные программы наблюдения за пациентами с имплантированными устройствами, что усиливает предпочтение учреждений. Увеличение государственных инвестиций в больничную инфраструктуру, особенно в развивающихся странах, еще больше расширяет возможности проведения процедур. Наличие высококвалифицированных хирургов и специализированных хирургических отделений повышает надежность процедур. Больницы также участвуют в клинических испытаниях и раннем внедрении передовых имплантационных технологий, укрепляя свои лидирующие позиции. Растущее сотрудничество между больницами и производителями медицинского оборудования в целях внедрения передовых технологий также способствует росту доходов. Высокий уровень доверия пациентов и практика направления пациентов к другим специалистам дополнительно стимулируют использование больниц. Эти факторы в совокупности обеспечивают сохранение доминирующего положения больниц на протяжении всего прогнозируемого периода.

Ambulatory Surgical Centers (ASCs) are expected to witness the fastest growth with a CAGR of 10.8% from 2026 to 2033, driven by increasing demand for cost-effective outpatient surgical procedures and the growing adoption of minimally invasive implantation techniques. ASCs offer shorter procedure times, reduced hospitalization costs, and faster patient turnover, making them attractive to both healthcare providers and patients. Improvements in minimally invasive device implantation technologies allow more procedures to be safely performed in outpatient settings. Favorable reimbursement models encouraging outpatient care are also supporting segment expansion. Increasing investments in advanced surgical equipment within ASCs enhance procedural capabilities. Patients increasingly prefer outpatient facilities due to reduced waiting times and quicker discharge. Expansion of private healthcare providers establishing specialized ASCs is also contributing to market growth. Regulatory support for decentralized surgical care further accelerates adoption. Continuous improvements in anesthesia and postoperative monitoring technologies enhance procedural safety in outpatient settings. Growing physician partnerships with ASCs also expand service availability. Rising healthcare system focus on cost optimization further supports outpatient surgical growth. These factors collectively position ASCs as the fastest-growing end-user segment in the medical implantable devices market.

Middle East and Africa Active Medical Implantable Devices Market Regional Analysis

- The Middle East and Africa Active Medical Implantable Devices Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare investments, expanding access to advanced surgical procedures, and the growing prevalence of cardiovascular and neurological disorders across the region

- Governments are actively strengthening healthcare infrastructure through modernization initiatives, establishment of specialized cardiac and neurology centers, and expansion of tertiary care hospitals, which is accelerating the adoption of implantable medical technologies

- In addition, rising awareness regarding early disease management and improved reimbursement frameworks in several countries are supporting broader patient access to implantable therapies across both public and private healthcare sectors

Saudi Arabia Middle East and Africa Active Medical Implantable Devices Market Insight

Saudi Arabia Middle East and Africa Active Medical Implantable Devices Market dominated the Middle East and Africa Active Medical Implantable Devices Market with the largest revenue share of approximately 35.4% in 2025, supported by strong government investment in healthcare infrastructure, expansion of tertiary care hospitals, and increasing adoption of advanced cardiac rhythm management devices, neurostimulators, and implantable drug-delivery systems. National healthcare transformation programs focusing on advanced treatment accessibility, combined with the growing burden of chronic cardiovascular and neurological diseases, are significantly driving demand for implantable therapeutic technologies in the country. Continuous investments in specialized treatment centers and training programs for advanced surgical procedures are further strengthening market growth.

U.A.E. Middle East and Africa Active Medical Implantable Devices Market Insight

The U.A.E. Middle East and Africa Active Medical Implantable Devices Market is expected to be the fastest-growing country in the Middle East and Africa Active Medical Implantable Devices Market during the forecast period, driven by rapid expansion of private healthcare facilities, increasing medical tourism, and the growing availability of highly specialized cardiac and neurology treatment centers. Rising adoption of technologically advanced implantable therapies, supported by favorable healthcare policies and increasing investments in digital health and precision medicine initiatives, is further accelerating market expansion. In addition, the presence of internationally accredited hospitals and strong collaboration between global device manufacturers and regional healthcare providers is enhancing accessibility to next-generation implantable medical technologies across the country.

Middle East and Africa Active Medical Implantable Devices Market Share

The Active Medical Implantable Devices industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- LivaNova PLC (U.K.)

- Cochlear Limited (Australia)

- Sonova Holding AG (Switzerland)

- Demant A/S (Denmark)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- MicroPort Scientific Corporation (China)

- Lepu Medical Technology (China)

- Nihon Kohden Corporation (Japan)

- Olympus Corporation (Japan)

- Nurotron Biotechnology Co., Ltd. (China)

- Integer Holdings Corporation (U.S.)

- Smith & Nephew plc (U.K.)

- Stryker Corporation (U.S.)

- Terumo Corporation (Japan)

- Siemens Healthineers AG (Germany)

Latest Developments in Middle East and Africa Active Medical Implantable Devices Market

- In July 2023, Abbott, a global healthcare technology leader, announced that the U.S. Food and Drug Administration (FDA) approved the AVEIR DR dual-chamber leadless pacemaker system, the world’s first leadless pacemaker capable of pacing both the right atrium and right ventricle simultaneously. The device utilizes implant-to-implant (i2i) communication technology to enable synchronized beat-to-beat communication between two miniature pacemakers implanted directly in the heart, eliminating the need for traditional pacing leads and surgical pockets. This approval significantly expanded access to leadless pacing therapy for patients with abnormal heart rhythms and marked a major advancement in minimally invasive cardiac implantable device technology

- In June 2024, Abbott announced that the AVEIR DR dual-chamber leadless pacemaker system received CE Mark approval in Europe, expanding the availability of the world’s first dual-chamber leadless pacing technology to European markets. The system enables wireless synchronization between two implanted devices using high-frequency conductive communication, reducing complications associated with traditional leads while enhancing patient comfort and recovery outcomes. This regulatory milestone strengthened Abbott’s presence in the cardiac rhythm management segment and accelerated adoption of next-generation leadless implantable cardiac devices globally

- In September 2024, Senseonics Holdings announced that the U.S. FDA cleared the Eversense® 365 implantable continuous glucose monitoring (CGM) system, the first implantable CGM designed to operate continuously for up to one year. The small implantable sensor, inserted beneath the skin of the upper arm, provides real-time glucose readings every five minutes to a mobile application, significantly extending device longevity compared with earlier six-month implantable CGM models. This development represented a major advancement in implantable diabetes monitoring technology and improved long-term patient adherence and convenience

- In February 2025, Medtronic announced that the U.S. Food and Drug Administration (FDA) approved its adaptive deep brain stimulation (DBS) system for the treatment of Parkinson’s disease, marking the first brain-implant system capable of adjusting stimulation in real time based on patient neurological signals. The adaptive implant dynamically responds to brain activity to improve symptom control and reduce involuntary movements, representing a significant milestone in intelligent neurostimulation technology and strengthening the role of smart implantable devices in neurological disorder management

- В октябре 2025 года компания Abbott объявила о коммерческом запуске в Индии двухкамерной беспроводной системы кардиостимуляции AVEIR DR, представив в регионе первую в мире двухкамерную беспроводную технологию кардиостимуляции. Миниатюрная имплантируемая система, размером меньше батарейки AAA, имплантируется с помощью малоинвазивной катетерной процедуры и обеспечивает синхронизированную стимуляцию без проводов, снижая риск осложнений и сокращая время восстановления пациента. Региональный запуск расширил глобальный доступ к передовым имплантируемым кардиотехнологиям и поддержал растущее внедрение малоинвазивных имплантируемых устройств на развивающихся рынках здравоохранения.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.