Middle East And Africa Clinical Trial Supplies Market

Размер рынка в млрд долларов США

CAGR :

%

USD

81.28 Billion

USD

139.65 Billion

2025

2033

USD

81.28 Billion

USD

139.65 Billion

2025

2033

| 2026 –2033 | |

| USD 81.28 Billion | |

| USD 139.65 Billion | |

| % | |

|

Middle East and Africa Clinical Trial Supplies Market Segmentation, By Services (Storage, Manufacturing, Packaging And Labelling), Clinical Phase (Phase III, Phase II, Phase IV, Phase I), Therapeutic Uses (Oncology, Cardiovascular Diseases, Dermatology, Metabolic Disorders, Infectious Diseases, Respiratory Diseases, CNS And Mental Disorders, Blood Disorders, Others), By End User (Contract Research Organizations, Pharmaceutical And Biotechnology Companies) - Industry Trends and Forecast to 2033

Middle East and Africa Clinical Trial Supplies Market Size

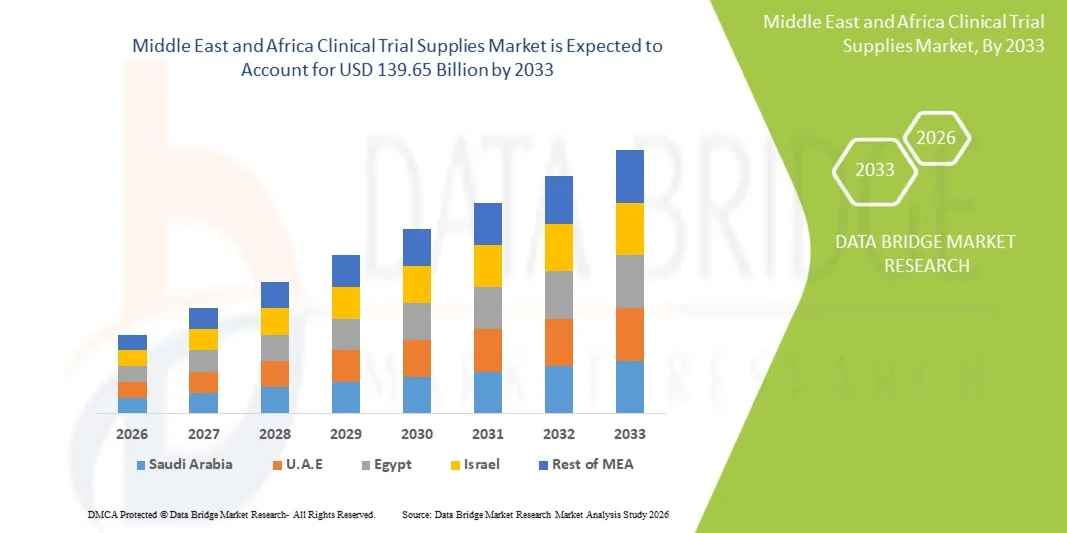

- The Middle East and Africa Clinical Trial Supplies Market size was valued at USD 81.28 billion in 2025 and is expected to reach USD 139.65 billion by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing number of clinical trials and rising investments in pharmaceutical and biotechnology research, leading to higher demand for efficient supply chain and logistics solutions in clinical studies

- Furthermore, growing complexity of clinical trials, including multi-regional studies and personalized medicine approaches, is increasing the need for advanced clinical trial supply management solutions. These converging factors are accelerating the uptake of Clinical Trial Supplies solutions, thereby significantly boosting the industry's growth

Middle East and Africa Clinical Trial Supplies Market Analysis

- Clinical trial supplies, including investigational drugs, packaging, labeling, and logistics services, are increasingly vital components of modern clinical research due to their role in ensuring efficient trial execution, regulatory compliance, and patient safety across global studies

- The escalating demand for clinical trial supplies is primarily fueled by the growing number of clinical trials, increasing complexity of study protocols, and rising adoption of decentralized and multi-regional trials

- Saudi Arabia dominated the Middle East and Africa Clinical Trial Supplies Market with the largest revenue share of approximately 31.7% in 2025, characterized by improving healthcare infrastructure, increasing investments in clinical research, and growing presence of pharmaceutical companies, with the country witnessing steady growth driven by supportive government initiatives and rising demand for advanced clinical trial services

- U.A.E. is expected to be the fastest growing country in the Middle East and Africa Clinical Trial Supplies Market during the forecast period, with a projected CAGR of around 8.5%, due to rising clinical research activities, increasing healthcare expenditure, growing adoption of advanced medical technologies, and expanding presence of contract research organizations

- The Phase III segment held the largest market revenue share of 41.2% in 2025, driven by the large scale, complexity, and higher patient enrollment associated with late-stage trials

Report Scope and Middle East and Africa Clinical Trial Supplies Market Segmentation

|

Attributes |

Clinical Trial Supplies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Clinical Trial Supplies Market Trends

“Advancements in Supply Chain Optimization and Digital Trial Management”

- A significant and accelerating trend in the global Middle East and Africa Clinical Trial Supplies Market is the increasing adoption of advanced supply chain technologies, including real-time tracking systems, predictive analytics, and digital inventory management solutions. These innovations are enhancing operational efficiency, minimizing delays, and ensuring the timely and accurate distribution of clinical trial materials across regions

- For instance, global clinical supply providers are increasingly deploying interactive response technologies (IRT) and cloud-based platforms to manage complex multi-country trials, enabling better coordination between sponsors, sites, and logistics partners

- The integration of advanced data analytics tools allows stakeholders to forecast demand more accurately, optimize inventory levels, and reduce wastage of high-value investigational products, particularly in large-scale and multi-phase trials

- Furthermore, the rise of decentralized and hybrid clinical trials worldwide is transforming supply chain models, with increased adoption of direct-to-patient delivery systems and remote monitoring of trial material

- This ongoing shift toward digitization and automation is significantly improving transparency, compliance, and responsiveness in clinical trial logistics, especially in emerging markets where infrastructure is rapidly evolving

- As a result, the demand for integrated, flexible, and technology-driven clinical trial supply solutions is expanding across pharmaceutical, biotechnology, and research organizations globally

Middle East and Africa Clinical Trial Supplies Market Dynamics

Driver

“Increasing Global Clinical Trial Activity and Rising R&D Investments”

- The growing number of clinical trials worldwide, supported by increasing investments in pharmaceutical and biotechnology research, is a key driver of the Middle East and Africa Clinical Trial Supplies Market

- For instance, the expansion of research in therapeutic areas such as oncology, infectious diseases, and rare disorders has significantly increased the demand for specialized supply chain services, including cold chain logistics and customized packaging solutions

- The rising focus on personalized medicine and biologics is further driving demand, as these therapies require highly controlled, small-batch production and precise distribution across multiple trial sites

- In addition, globalization of clinical trials, with studies being conducted across North America, Europe, Asia-Pacific, and emerging regions, is increasing the complexity of supply chains and driving the need for efficient logistics solutions

- Government initiatives, regulatory support, and funding programs in various countries are also encouraging clinical research activities, thereby contributing to market growth

- Moreover, the increasing trend of outsourcing clinical trial supply management to specialized vendors is enabling pharmaceutical companies to improve operational efficiency, reduce costs, and focus on core research activities

Restraint/Challenge

“Stringent Regulatory Frameworks and Global Supply Chain Complexities”

- Strict regulatory requirements related to the storage, transportation, and handling of clinical trial materials remain a major challenge for market participants, often increasing operational burden and costs

- For instance, compliance with international standards such as Good Clinical Practice (GCP) and Good Distribution Practice (GDP) requires extensive documentation, monitoring, and validation processes across different regions

- The complexity of managing global, multi-site clinical trials—each governed by distinct regulatory frameworks—can lead to logistical inefficiencies and delays in trial execution

- In addition, supply chain disruptions caused by geopolitical uncertainties, transportation constraints, and shortages of critical raw materials can significantly impact the timely delivery of trial supplies

- Maintaining cold chain integrity for temperature-sensitive products such as biologics, vaccines, and cell & gene therapies continues to be a critical challenge, requiring advanced infrastructure and real-time monitoring system

- Addressing these issues through regulatory harmonization, adoption of digital supply chain technologies, and investment in resilient logistics networks will be crucial for sustaining long-term market growth.

Middle East and Africa Clinical Trial Supplies Market Scope

The market is segmented on the basis of services, clinical phase, therapeutic uses, and end user.

• By Services

On the basis of services, the Middle East and Africa Clinical Trial Supplies Market is segmented into storage, manufacturing, and packaging and labelling. The manufacturing segment dominated the largest market revenue share of 36.8% in 2025, driven by the increasing number of clinical trials and the need for large-scale production of investigational products. Manufacturing services play a critical role in ensuring consistency, quality, and regulatory compliance of trial materials. Rising demand for biologics and complex therapies further supports segment growth. Increasing outsourcing by pharmaceutical companies enhances reliance on specialized manufacturing providers. Expansion of global clinical pipelines strengthens demand. Technological advancements in drug formulation and production improve efficiency. Growing regulatory requirements ensure standardized manufacturing practices. Increasing investment in R&D activities boosts production needs. These factors collectively ensure dominance of the manufacturing segment.

The packaging and labelling segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by stringent regulatory requirements and the need for accurate labeling in clinical trials. Proper packaging ensures drug stability, safety, and traceability throughout the supply chain. Increasing globalization of clinical trials boosts demand for multilingual and region-specific labeling. Rising adoption of temperature-sensitive biologics supports advanced packaging solutions. Growth in personalized medicine enhances the need for customized packaging. Technological advancements such as smart packaging and tracking systems improve efficiency. Increasing outsourcing of packaging services further accelerates growth. These factors position packaging and labelling as the fastest-growing service segment.

• By Clinical Phase

On the basis of clinical phase, the Middle East and Africa Clinical Trial Supplies Market is segmented into Phase I, Phase II, Phase III, and Phase IV. The Phase III segment held the largest market revenue share of 41.2% in 2025, driven by the large scale, complexity, and higher patient enrollment associated with late-stage trials. Phase III trials require extensive supply chain management, including bulk drug production, storage, and distribution across multiple geographies. Increasing number of drugs entering late-stage development supports demand. Rising investment from pharmaceutical companies further strengthens the segment. Regulatory requirements and trial complexity increase dependency on supply services. Globalization of clinical trials boosts logistics demand. Higher costs associated with Phase III trials contribute to larger revenue share. These factors ensure dominance of the Phase III segment.

The Phase II segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by increasing focus on proof-of-concept studies and early efficacy evaluation. Growing number of drug candidates entering mid-stage trials supports growth. Rising innovation in biotechnology and specialty drugs enhances trial activity. Increased funding for clinical research accelerates Phase II studies. Expansion of precision medicine drives targeted trials. Faster regulatory approvals for innovative therapies boost progression to Phase II. These factors position Phase II as the fastest-growing clinical phase segment.

• By Therapeutic Uses

On the basis of therapeutic uses, the Middle East and Africa Clinical Trial Supplies Market is segmented into oncology, cardiovascular diseases, dermatology, metabolic disorders, infectious diseases, respiratory diseases, CNS and mental disorders, blood disorders, and others. The oncology segment accounted for the largest market revenue share of 38.5% in 2025, driven by the high number of ongoing cancer clinical trials worldwide. Increasing prevalence of cancer and demand for innovative therapies significantly support segment growth. Rising development of targeted therapies and immunotherapies boosts clinical trial activity. Substantial funding and investments in oncology research strengthen demand. Growing adoption of personalized medicine enhances trial complexity. Expansion of global oncology pipelines further drives growth. These factors ensure dominance of the oncology segment.

The CNS and mental disorders segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by rising awareness and increasing diagnosis of neurological and psychiatric conditions. Growing demand for innovative treatments for diseases such as Alzheimer’s and depression supports growth. Increasing research funding in neuroscience accelerates clinical trials. Expansion of novel drug pipelines strengthens the segment. Rising unmet medical needs drive investment. These factors position CNS and mental disorders as the fastest-growing therapeutic segment.

• By End User

On the basis of end user, the Middle East and Africa Clinical Trial Supplies Market is segmented into contract research organizations and pharmaceutical and biotechnology companies. The pharmaceutical and biotechnology companies segment dominated the largest market revenue share of 55.6% in 2025, driven by their direct involvement in drug development and clinical trials. These companies require extensive supply chain services to support global trials. Increasing R&D expenditure and drug pipelines boost demand. Expansion of biologics and specialty drugs strengthens reliance on supply services. Strategic collaborations and outsourcing further enhance growth. Rising number of clinical trials globally supports segment expansion. These factors ensure dominance of pharmaceutical and biotechnology companies.

The contract research organizations (CROs) segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by increasing outsourcing of clinical trial operations. CROs offer cost-effective and efficient trial management services. Growing complexity of clinical trials encourages outsourcing to specialized providers. Rising demand for faster trial completion supports CRO adoption. Expansion of global clinical research activities enhances growth. Increasing partnerships between pharma companies and CROs strengthen the segment. These factors position CROs as the fastest-growing end user segment.

Middle East and Africa Clinical Trial Supplies Market Regional Analysis

- The Middle East and Africa Clinical Trial Supplies Market is poised to grow at a steady CAGR of around 8.5% during the forecast period, driven by increasing clinical research activities, rising investments in pharmaceutical and biotechnology sectors, and growing outsourcing of clinical trials to emerging economies

- The region’s expanding healthcare infrastructure, along with supportive government initiatives and improving regulatory frameworks, is accelerating the adoption of efficient clinical trial supply solutions

- Furthermore, Middle East and Africa is emerging as a developing hub for clinical research, improving accessibility and demand for advanced supply chain and logistics services

Saudi Arabia Middle East and Africa Clinical Trial Supplies Market Insight

The Saudi Arabia Middle East and Africa Clinical Trial Supplies Market dominated with the largest revenue share of approximately 31.7% in 2025, characterized by improving healthcare infrastructure, increasing investments in clinical research, and growing presence of pharmaceutical companies. The country is witnessing steady growth driven by supportive government initiatives and rising demand for advanced clinical trial services, along with expanding healthcare facilities and increasing focus on research and development.

U.A.E. Middle East and Africa Clinical Trial Supplies Market Insight

The U.A.E. Middle East and Africa Clinical Trial Supplies Market is expected to be the fastest growing, with a projected CAGR of around 8.5% during the forecast period. This growth is driven by rising clinical research activities, increasing healthcare expenditure, and growing adoption of advanced medical technologies. Additionally, expanding presence of contract research organizations and improving access to modern healthcare infrastructure are further supporting the rapid growth of the market in the U.A.E.

Middle East and Africa Clinical Trial Supplies Market Share

The Clinical Trial Supplies industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- IQVIA Inc. (U.S.)

- Catalent, Inc. (U.S.)

- Parexel International Corporation (U.S.)

- Almac Group (U.K.)

- PCI Pharma Services (U.S.)

- Marken (UPS Healthcare) (U.S.)

- Sharp Services, LLC (U.S.)

- Movianto (Germany)

- KLIFO A/S (Denmark)

- Fisher Clinical Services (U.S.)

- Bilcare Limited (India)

- Myonex (U.S.)

- UDG Healthcare plc (Ireland)

- DHL Supply Chain (Germany)

- Lonza Group AG (Switzerland)

- Recipharm AB (Sweden)

- Eurofins Scientific (Luxembourg)

- Piramal Pharma Solutions (India)

- Aenova Group (Germany)

Latest Developments in Middle East and Africa Clinical Trial Supplies Market

- In November 2021, Thermo Fisher Scientific completed its acquisition of PPD, a leading clinical research organization, significantly expanding its clinical trial services and supply chain capabilities, including packaging, logistics, and distribution of clinical trial materials. This acquisition strengthened Thermo Fisher’s end-to-end clinical trial supply solutions and global reach

- In January 2025, Catalent announced the expansion of its clinical trial supply capabilities at its Philadelphia facility, adding advanced packaging lines to support cell and gene therapy trials requiring specialized handling and temperature control. This development highlights growing demand for complex biologics supply chain solutions

- In February 2025, AstraZeneca partnered with Thermo Fisher Scientific to streamline clinical trial supply chain operations, focusing on comparator sourcing and efficient global distribution for immunotherapy trials. This collaboration underscores increasing reliance on strategic partnerships to improve trial efficiency and logistics

- In March 2025, Novartis initiated hybrid clinical trials incorporating direct-to-patient (DTP) drug delivery models, using specialized packaging solutions to enhance patient access and reduce logistical complexities in global trials. This development reflects the growing adoption of decentralized clinical trial supply models

- In September 2025, industry analysis highlighted that leading companies such as Thermo Fisher Scientific, Sharp Services, and Parexel International were strengthening their clinical trial supply capabilities through partnerships, digital technologies, and expanded global logistics networks. This development emphasizes the increasing integration of AI, blockchain, and cloud systems in supply chain management

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.