Middle East And Africa Neurosurgery Market

Размер рынка в млрд долларов США

CAGR :

%

USD

232.23 Million

USD

542.94 Million

2025

2033

USD

232.23 Million

USD

542.94 Million

2025

2033

| 2026 –2033 | |

| USD 232.23 Million | |

| USD 542.94 Million | |

| % | |

|

Middle East and Africa Neurosurgery Market Segmentation, By Product Type (Neurosurgery Devices, Neurosurgery Software, and Consumables), Application (Aneurysms, Arteriovenous Malformation (AVM), Brain Tumors, Carotid Artery Blockage/Stenosis, Cerebrovascular Surgery, Cortical Mapping, Epilepsy, Functional Neurosurgery, Intraoperative Angiography, Parkinson's Disease and Tremors, Peripheral Nerve Surgery, Pituitary Tumors, Radiosurgery, Skull Base Surgery, Spine Surgery, Stereotactic Neurosurgery, Trauma Surgery, Trigeminal Neuralgia, and Others), Age Group (Pediatric, Adult, and Geriatric), End User (Hospitals, Neurosurgery Centers, Research Centers, Ambulatory Surgical Centers, and Others), Distribution Channel (Direct Tender, Third Party Distributors, and Others)- Industry Trends and Forecast to 2033

Middle East and Africa Neurosurgery Market Size

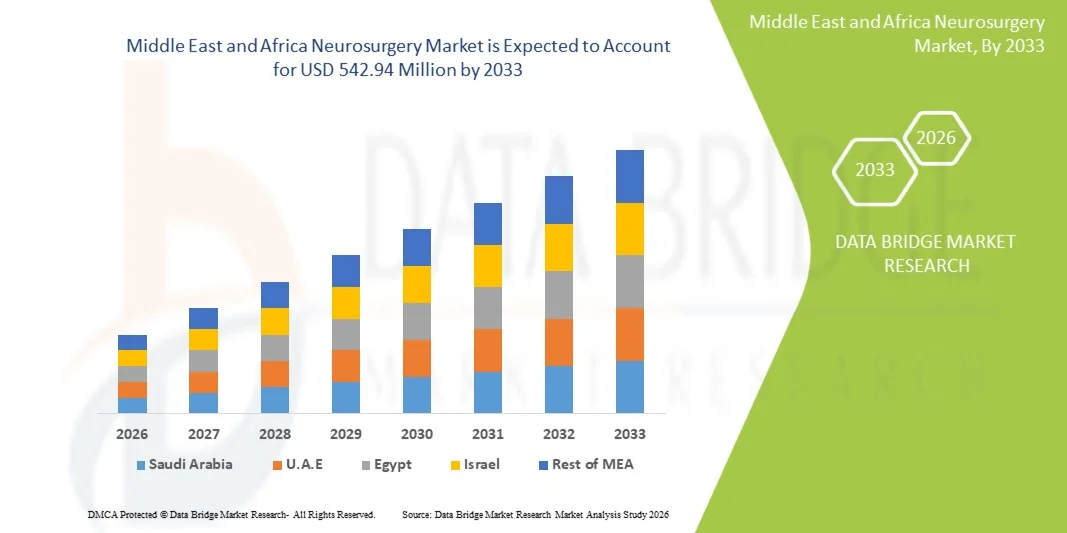

- The Middle East and Africa neurosurgery market size was valued at USD 232.23 million in 2025 and is expected to reach USD 542.94 million by 2033, at a CAGR of 11.2% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological disorders such as stroke and brain tumors, along with continuous advancements in neurosurgical technologies and imaging systems across the region

- Furthermore, rising healthcare investments, improving hospital infrastructure, and growing demand for minimally invasive and precision-based neurosurgical procedures are establishing advanced neurosurgery solutions as a critical component of modern healthcare systems. These converging factors are accelerating the adoption of neurosurgical devices and procedures, thereby significantly boosting the market growth in the region

Middle East and Africa Neurosurgery Market Analysis

- Neurosurgery, encompassing surgical interventions for disorders of the brain, spine, and nervous system, is becoming an increasingly critical component of advanced healthcare systems across the Middle East and Africa due to the rising burden of neurological conditions and the need for specialized surgical care

- The escalating demand for neurosurgical procedures is primarily fueled by the growing incidence of stroke, traumatic brain injuries, and brain tumors, along with increasing awareness, improving diagnostic capabilities, and a rising preference for minimally invasive surgical techniques

- Saudi Arabia dominated the Middle East and Africa neurosurgery market with the largest revenue share of 30.4% in 2025, characterized by strong healthcare infrastructure, high healthcare expenditure, and rapid adoption of advanced surgical technologies, with the country witnessing significant growth driven by government investments and expanding specialized hospitals

- South Africa is expected to be the fastest growing country in the market during the forecast period, due to improving healthcare access, increasing investments in hospital infrastructure, and a gradual rise in the availability of skilled neurosurgeons and advanced treatment facilities

- Neurosurgery Devices segment dominated the market with the largest share of 38.7% in 2025, driven by their essential role in both traditional and minimally invasive procedures, along with continuous technological advancements enhancing surgical precision and patient outcomes

Report Scope and Middle East and Africa Neurosurgery Market Segmentation

|

Attributes |

Middle East and Africa Neurosurgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Neurosurgery Market Trends

“Rising Adoption of Minimally Invasive and Robotic-Assisted Neurosurgery”

- A significant and accelerating trend in the Middle East and Africa neurosurgery market is the increasing adoption of minimally invasive techniques and robotic-assisted surgical systems across advanced healthcare facilities. This integration of technologies is significantly enhancing surgical precision and patient recovery outcomes

- For instance, robotic-assisted neurosurgical platforms and image-guided navigation systems are being increasingly utilized in countries such as Saudi Arabia and the UAE, enabling surgeons to perform complex brain and spine procedures with higher accuracy and reduced complications. Similarly, advanced intraoperative imaging solutions are improving real-time decision-making during surgeries

- The adoption of advanced technologies in neurosurgery enables features such as enhanced visualization, improved targeting of affected areas, and reduced surgical trauma. For instance, neuronavigation systems assist surgeons in accurately locating tumors, while intraoperative MRI allows real-time imaging to ensure complete removal of abnormal tissues. Furthermore, minimally invasive procedures offer patients shorter hospital stays and faster recovery times

- The integration of neurosurgical technologies with digital healthcare infrastructure facilitates better surgical planning and patient management across healthcare systems. Through centralized data platforms, clinicians can access imaging, patient history, and surgical plans, creating a more coordinated and efficient treatment approach

- This trend towards more precise, technology-driven, and patient-centric neurosurgical care is fundamentally transforming treatment standards in the region. Consequently, companies are developing advanced neurosurgical instruments and robotic systems with features such as real-time imaging integration and enhanced surgical accuracy

- The demand for advanced neurosurgical solutions with integrated imaging and robotic assistance is growing rapidly across major healthcare centers, as providers increasingly prioritize improved patient outcomes and operational efficiency

- The rising focus on training programs and skill development for neurosurgeons is supporting the adoption of advanced surgical techniques, further strengthening the region’s neurosurgical ecosystem

Middle East and Africa Neurosurgery Market Dynamics

Driver

“Growing Demand Driven by Rising Neurological Disorders and Healthcare Investments”

- The increasing prevalence of neurological disorders among patients, coupled with rising healthcare investments across the Middle East and Africa, is a significant driver for the heightened demand for neurosurgical procedures

- For instance, in recent years, several governments in the region have increased funding for specialized healthcare services, focusing on expanding neurology and neurosurgery departments in major hospitals. Such strategies by public and private stakeholders are expected to drive the neurosurgery market growth in the forecast period

- As healthcare systems strengthen and awareness of neurological conditions increases, neurosurgical interventions are becoming more accessible, offering advanced treatment options for conditions such as brain tumors, epilepsy, and spinal disorders

- Furthermore, the growing adoption of advanced diagnostic imaging and surgical technologies is improving early detection and treatment outcomes, making neurosurgery a critical component of modern healthcare delivery

- The availability of skilled neurosurgeons, improved hospital infrastructure, and increasing collaborations with international medical institutions are key factors propelling the adoption of neurosurgical procedures across the region. The trend towards specialized care centers and technological integration further contributes to market growth

- Increasing government initiatives aimed at strengthening healthcare systems and expanding access to specialized treatments are further accelerating market growth across key countries

- The rising demand for private healthcare services and medical tourism in countries such as the UAE and Saudi Arabia is also contributing significantly to the expansion of neurosurgical services

Restraint/Challenge

“Limited Access to Specialized Care and High Treatment Costs”

- Challenges related to limited access to specialized neurosurgical care and high treatment costs pose a significant barrier to widespread adoption of advanced neurosurgical procedures in the region. Many areas, particularly in parts of Africa, face shortages of trained neurosurgeons and advanced medical facilities

- For instance, disparities in healthcare infrastructure between urban and rural regions have resulted in unequal access to neurosurgical services, leading to delayed diagnosis and treatment for many patients

- Addressing these challenges requires significant investment in healthcare infrastructure, training programs for medical professionals, and expansion of specialized treatment centers. Governments and organizations are increasingly focusing on capacity-building initiatives to improve access to care

- In addition, the high cost of advanced neurosurgical equipment and procedures can limit affordability for many patients, particularly in low- and middle-income countries. While some private hospitals offer cutting-edge treatments, affordability remains a key concern for a large portion of the population

- Overcoming these barriers through increased funding, policy support, and adoption of cost-effective technologies will be essential for ensuring equitable access and sustained growth of the neurosurgery market in the Middle East and Africa

- Limited reimbursement frameworks and insurance coverage for neurosurgical procedures in several countries further restrict patient access to advanced treatments

- Logistical challenges such as inadequate emergency transport systems and delayed referrals can hinder timely neurosurgical interventions, impacting overall patient outcomes

Middle East and Africa Neurosurgery Market Scope

The market is segmented on the basis of product type, application, age group, end user, and distribution channel.

- By Product Type

On the basis of product type, the Middle East and Africa neurosurgery market is segmented into neurosurgery devices, neurosurgery software, and consumables. The neurosurgery devices segment dominated the market with the largest revenue share of 38.7% in 2025, driven by the high demand for advanced surgical instruments, neuronavigation systems, and imaging technologies essential for complex brain and spine procedures. Hospitals across the region are increasingly investing in technologically advanced devices to improve surgical precision and patient outcomes. The growing adoption of minimally invasive procedures further boosts demand for specialized neurosurgical equipment. In addition, the expansion of tertiary care centers and specialty hospitals supports the widespread use of these devices. Continuous technological innovations and product launches are also strengthening the segment’s dominance in the market.

The neurosurgery software segment is anticipated to witness the fastest growth rate during the forecast period, fueled by the rising adoption of digital healthcare solutions and advanced surgical planning tools. Software solutions enable improved preoperative planning, intraoperative guidance, and post-operative analysis, enhancing overall treatment efficiency. Increasing integration of artificial intelligence and data analytics into neurosurgical workflows is further driving demand for such platforms. Healthcare providers are increasingly leveraging software to streamline operations and improve clinical decision-making. The growing focus on precision medicine and personalized treatment approaches also supports segment growth. Furthermore, the shift toward digitization in healthcare systems is accelerating the adoption of neurosurgery software.

- By Application

On the basis of application, the market is segmented into aneurysms, arteriovenous malformation (AVM), brain tumors, carotid artery blockage/stenosis, cerebrovascular surgery, cortical mapping, epilepsy, functional neurosurgery, intraoperative angiography, Parkinson's disease and tremors, peripheral nerve surgery, pituitary tumors, radiosurgery, skull base surgery, spine surgery, stereotactic neurosurgery, trauma surgery, trigeminal neuralgia, and others. The brain tumors segment dominated the market with the largest revenue share in 2025, driven by the increasing incidence of brain cancer cases and the growing need for advanced surgical interventions. The availability of improved diagnostic imaging technologies has enabled early detection and effective treatment planning. Neurosurgical procedures for tumor removal are becoming more precise due to technological advancements. The rising number of specialized oncology and neurology centers further supports this segment’s dominance. In addition, increased awareness and screening programs contribute to higher diagnosis rates. The demand for minimally invasive tumor surgeries is also boosting segment growth.

The functional neurosurgery segment is expected to witness the fastest growth rate during the forecast period, driven by the rising prevalence of neurological disorders such as Parkinson’s disease and epilepsy. Advancements in techniques such as deep brain stimulation are improving patient outcomes and expanding treatment possibilities. Increasing awareness about these procedures is encouraging more patients to opt for surgical interventions. Healthcare providers are investing in advanced technologies to support functional neurosurgery procedures. The growing geriatric population, which is more susceptible to neurological conditions, further fuels demand. In addition, ongoing research and innovation in this field are accelerating segment expansion.

- By Age Group

On the basis of age group, the market is segmented into pediatric, adult, and geriatric. The adult segment dominated the market with the largest revenue share in 2025, driven by the high prevalence of neurological disorders such as brain tumors, trauma injuries, and spinal conditions among the adult population. Adults are more likely to undergo neurosurgical procedures due to lifestyle-related risk factors and occupational hazards. The availability of advanced treatment options and improved healthcare access further supports this segment’s dominance. In addition, increasing awareness about neurological health encourages early diagnosis and treatment. Hospitals are focusing on expanding neurosurgical services tailored to adult patients. The rising incidence of road accidents and injuries in the region also contributes to higher demand.

The geriatric segment is expected to witness the fastest growth rate during the forecast period, driven by the increasing aging population and higher susceptibility to neurodegenerative diseases. Conditions such as Alzheimer’s disease, Parkinson’s disease, and stroke are more prevalent among elderly individuals, increasing the need for neurosurgical interventions. Improvements in healthcare infrastructure are enabling better treatment options for older patients. The growing focus on elderly care and specialized treatment facilities is also supporting segment growth. In addition, advancements in minimally invasive procedures make surgeries safer for geriatric patients. Rising life expectancy across the region further contributes to the expansion of this segment.

- By End User

On the basis of end user, the market is segmented into hospitals, neurosurgery centers, research centers, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by the availability of advanced infrastructure, skilled professionals, and comprehensive care facilities. Hospitals are the primary centers for performing complex neurosurgical procedures, offering access to advanced imaging and surgical technologies. The increasing number of hospital admissions for neurological disorders further supports this segment’s dominance. Government investments in healthcare infrastructure are also boosting hospital capabilities. In addition, the presence of multidisciplinary teams enhances treatment outcomes. The expansion of private hospitals in the region further strengthens this segment.

The ambulatory surgical centers segment is expected to witness the fastest growth rate during the forecast period, driven by the increasing preference for cost-effective and minimally invasive procedures. These centers offer shorter hospital stays and faster recovery times, making them an attractive option for patients. Advancements in surgical techniques are enabling more procedures to be performed in outpatient settings. Healthcare providers are increasingly establishing ambulatory centers to reduce the burden on hospitals. The growing focus on efficiency and patient convenience is also contributing to segment growth. In addition, rising healthcare costs are encouraging the adoption of these centers.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third party distributors, and others. The direct tender segment dominated the market with the largest revenue share in 2025, driven by large-scale procurement by government and private hospitals. Direct purchasing ensures cost efficiency and access to high-quality neurosurgical equipment from manufacturers. Healthcare institutions prefer direct tenders for bulk procurement and long-term contracts. The involvement of government bodies in healthcare spending further strengthens this segment. In addition, direct procurement helps maintain product authenticity and service support. The increasing number of large hospital networks also contributes to this segment’s dominance.

The third party distributors segment is expected to witness the fastest growth rate during the forecast period, driven by their ability to expand market reach and provide localized support. Distributors play a crucial role in supplying neurosurgical products to smaller hospitals and clinics across remote areas. They help manufacturers penetrate untapped markets and improve product accessibility. The growing demand for neurosurgical devices in developing regions further supports this segment’s growth. In addition, distributors offer value-added services such as training and maintenance support. The increasing collaboration between manufacturers and distributors is also accelerating segment expansion.

Middle East and Africa Neurosurgery Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa neurosurgery market with the largest revenue share of 30.4% in 2025, characterized by strong healthcare infrastructure, high healthcare expenditure, and rapid adoption of advanced surgical technologies, with the country witnessing significant growth driven by government investments and expanding specialized hospitals

- Healthcare providers in the country highly prioritize advanced surgical technologies, precision-based treatment, and improved patient outcomes, supported by the adoption of minimally invasive techniques and modern imaging systems

- This strong growth is further supported by government healthcare initiatives, rising medical tourism, and the presence of well-equipped hospitals and skilled professionals, establishing Saudi Arabia as a key hub for neurosurgical care in the region

Saudi Arabia Neurosurgery Market Insight

The Saudi Arabia neurosurgery market captured the largest revenue share in 2025 within the Middle East and Africa, fueled by substantial government investments in healthcare infrastructure and the growing demand for advanced neurosurgical procedures. The country is actively expanding specialized hospitals and neurology centers under national healthcare transformation programs. Healthcare providers are increasingly prioritizing the adoption of cutting-edge surgical technologies such as neuronavigation and robotic-assisted systems to enhance patient outcomes. The growing prevalence of neurological disorders, including stroke and brain tumors, is further driving demand. Moreover, the integration of advanced imaging systems and minimally invasive techniques is significantly contributing to the market's expansion, alongside rising medical tourism.

UAE Neurosurgery Market Insight

The UAE neurosurgery market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare expenditure and the rising demand for high-quality specialized treatments. The country’s strong focus on becoming a global medical tourism hub is attracting patients seeking advanced neurosurgical care. The rapid growth of private hospitals and internationally accredited healthcare facilities is fostering the adoption of innovative neurosurgical procedures. Patients are also drawn to the availability of world-class infrastructure and highly trained specialists. In addition, continuous investments in AI-based diagnostics and minimally invasive surgical techniques are further accelerating market growth.

South Africa Neurosurgery Market Insight

The South Africa neurosurgery market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improving healthcare access and a rising burden of neurological disorders. The country is witnessing increasing investments in both public and private healthcare infrastructure to enhance neurosurgical capabilities. In addition, ongoing training programs and partnerships with international institutions are improving the availability of skilled neurosurgeons. The expansion of urban hospitals and specialty clinics is supporting the adoption of advanced procedures. The growing awareness regarding early diagnosis and treatment of neurological conditions further strengthens market demand.

Egypt Neurosurgery Market Insight

The Egypt neurosurgery market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing healthcare reforms and rising demand for specialized surgical care. Government initiatives aimed at improving healthcare accessibility and affordability are encouraging the development of neurosurgical services. The country is also witnessing growth in private healthcare providers offering advanced treatment options. Egypt’s improving medical infrastructure, combined with rising investments in diagnostic imaging and surgical technologies, supports market expansion. In addition, the growing population and increasing incidence of neurological disorders are key contributors to demand.

Middle East and Africa Neurosurgery Market Share

The Middle East and Africa Neurosurgery industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- B. Braun SE (Germany)

- Elekta AB (Sweden)

- Integra LifeSciences Holdings Corporation (U.S.)

- Zimmer Biomet (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Brainlab SE (Germany)

- Renishaw plc (U.K.)

- Natus Medical Incorporated (U.S.)

- Synaptive Medical Inc. (Canada)

- Penumbra, Inc. (U.S.)

- Abbott (U.S.)

- Terumo Corporation (Japan)

- Smith & Nephew (U.K.)

- Olympus Corporation (Japan)

- Richard Wolf GmbH (Germany)

- Leica Microsystems GmbH (Germany)

- Carl Zeiss AG (Germany)

What are the Recent Developments in Middle East and Africa Neurosurgery Market?

- In November 2025, Dubai hosted the 19th World Federation of Neurosurgical Societies Congress, marking the first time this global event was held in the region. The congress attracted over 2,500 international experts, fostering knowledge exchange, innovation, and global collaboration in neurosurgery. This milestone positions the UAE as an emerging global hub for neurosurgical advancement and scientific research

- In October 2025, King Faisal Specialist Hospital and Research Centre in Riyadh performed the world’s first fully robotic intracranial tumor removal surgery, marking a major breakthrough in neurosurgical innovation. The procedure utilized advanced robotic arms and 3D image-guided navigation to precisely remove a brain tumor while minimizing risks to surrounding tissues

- In August 2025, Cleveland Clinic Abu Dhabi became the first hospital in the Middle East and North Africa to deploy the Artisse Intrasaccular Flow Modulator, an advanced device designed for minimally invasive treatment of complex brain aneurysms. This innovation enhances patient safety and treatment effectiveness while reducing the need for traditional open brain surgery. The development highlights the region’s growing adoption of cutting-edge neurosurgical technologies and strengthens Abu Dhabi’s position as a leader in advanced neurological care

- In January 2024, Burjeel Medical City in Abu Dhabi partnered with Northwell Health to establish a state-of-the-art Neuroscience Institute. This collaboration focuses on delivering advanced care for brain, spine, and neurovascular conditions while introducing international expertise into the region. The initiative significantly enhances access to specialized neurosurgical services and strengthens the UAE’s healthcare ecosystem

- In January 2023, American Hospital Dubai announced the acquisition of the Medtronic Mazor X Stealth™ Edition robotic guidance system, becoming the first private healthcare provider in the Middle East to adopt this advanced spinal surgery technology. The system combines robotics and navigation to improve surgical precision and outcomes. This development reflects the region’s rapid adoption of robotic-assisted neurosurgery and advanced surgical innovations

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.