North America Microgrid Market

Размер рынка в млрд долларов США

CAGR :

%

USD

35.89 Billion

USD

92.08 Billion

2025

2033

USD

35.89 Billion

USD

92.08 Billion

2025

2033

| 2026 –2033 | |

| USD 35.89 Billion | |

| USD 92.08 Billion | |

| % | |

|

North America Microgrid Market Segmentation, By Grid Type (Alternate Current Microgrid, Direct Current Microgrid, and Hybrid), Connectivity (Grid Connected and Remote/Island), Offering (Hardware, Software and Services), Vertical (Healthcare, Educational Institutions, Industrial, Military and Electric Utility), Power Source (Natural Gas, Combined Heat and Power, Diesel, Solar, Fuel Cells, and Others)- Industry Trends and Forecast to 2033

North America Microgrid Market Size

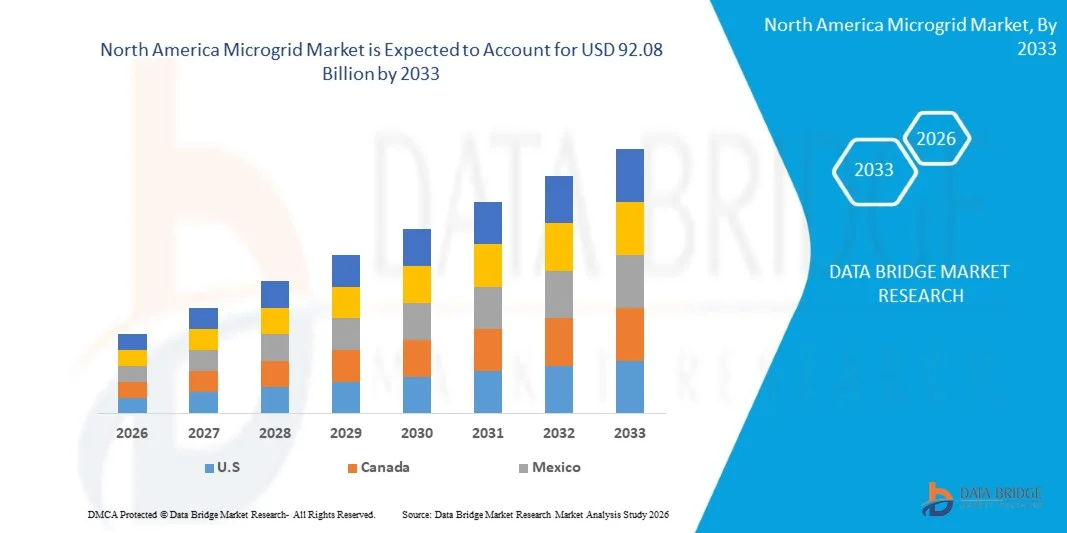

- The North America microgrid market size was valued at USD 35.89 billion in 2025 and is expected to reach USD 92.08 billion by 2033, at a CAGR of 12.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for decentralized energy systems, integration of renewable energy sources, and the need for energy security and reliability

- Rising investments in smart grids, energy storage technologies, and government initiatives to promote sustainable energy infrastructure are also supporting market expansion

North America Microgrid Market Analysis

- Growing adoption of renewable energy sources such as solar, wind, and biomass is driving the demand for microgrid solutions

- Increasing frequency of power outages and rising need for resilient energy infrastructure in industrial, commercial, and remote areas are accelerating market growth

- U.S. microgrid market captured the largest revenue share in 2025 within North America, driven by extensive investments in grid resilience, renewable integration, and critical infrastructure protection. Microgrid deployment continues to expand across military installations, healthcare facilities, universities, and municipal applications to mitigate outage risks and enhance energy security

- Canada is expected to witness the highest compound annual growth rate (CAGR) in the North America microgrid market due to increasing initiatives to replace diesel generation in remote and Indigenous communities with hybrid renewable microgrids. Government support, growing industrial and mining sector demand for reliable energy, and advancements in energy storage and distributed generation technologies are driving rapid market expansion in Canada

- The Alternate Current Microgrid segment held the largest market revenue share in 2025 driven by the extensive existing infrastructure built around AC power distribution and its compatibility with conventional electrical systems. AC microgrids are widely adopted as they support a broad range of applications and facilitate easier integration with utility networks. They are also preferred for large-scale deployments in commercial and industrial facilities due to their ability to handle higher loads efficiently. In addition, AC microgrids offer flexibility in maintenance and operational scalability

Report Scope and North America Microgrid Market Segmentation

|

Attributes |

North America Microgrid Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• S&C Electric Company (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Microgrid Market Trends

“Rising Adoption of Renewable Energy and Energy Storage Systems”

• The increasing focus on clean energy integration is significantly shaping the microgrid market, as organizations and utilities seek to improve energy reliability, efficiency, and sustainability. Microgrids are gaining traction due to their ability to provide localized energy generation, backup power during outages, and integration with renewable sources, making them ideal for industrial, commercial, and community applications. This trend is encouraging developers to innovate with hybrid microgrid solutions that combine solar, wind, and storage technologies

• Growing awareness around energy resilience, cost optimization, and environmental responsibility has accelerated the adoption of microgrids across multiple sectors. Corporations, educational institutions, hospitals, and critical infrastructure operators are actively deploying microgrid solutions to ensure uninterrupted power supply and reduce carbon footprint. This has also led to partnerships between technology providers, utility companies, and system integrators to enhance energy management capabilities

• Decentralization trends are influencing energy procurement strategies, with stakeholders emphasizing localized generation, smart controls, and grid independence. These factors are helping organizations optimize operational costs, mitigate risks of grid failure, and improve sustainability credentials. Companies are increasingly using microgrids to demonstrate commitment to ESG objectives and reinforce operational reliability

• For instance, in 2024, Bloom Energy in the U.S. and Schneider Electric launched advanced microgrid solutions for commercial and industrial facilities, integrating renewable generation, energy storage, and intelligent control systems. These deployments were designed to ensure high reliability, reduce energy costs, and support corporate sustainability goals. The solutions were also marketed as future-ready, scalable, and environmentally responsible energy systems

• While demand for microgrids is growing, long-term market expansion depends on continued technological innovation, cost optimization, and policy support. Manufacturers and developers are focusing on improving system efficiency, interoperability with existing infrastructure, and the development of standardized, modular solutions for broader adoption

North America Microgrid Market Dynamics

Driver

“Rising Need for Energy Resilience and Integration of Renewable Energy”

• Increasing demand for reliable and continuous power supply is a major driver for the microgrid market. Organizations are adopting microgrids to ensure uninterrupted electricity, especially in critical facilities and regions prone to grid instability. The trend also encourages investment in distributed energy resources (DERs) and smart grid technologies to enhance energy security

• Expanding applications across industrial, commercial, institutional, and remote community sectors are fueling market growth. Microgrids help optimize energy consumption, reduce costs, and enable the integration of renewable generation, contributing to sustainability objectives and operational efficiency

• Technology providers and energy solution developers are promoting microgrid adoption through innovative offerings such as hybrid microgrids, energy storage integration, and AI-driven energy management platforms. These initiatives improve reliability, predictability, and cost-effectiveness while encouraging collaboration among stakeholders to enhance system performance

• For instance, in 2023, Tesla in the U.S. and Siemens deployed energy storage-backed microgrids for industrial and utility applications, highlighting operational efficiency and renewable integration. These deployments showcased the potential for cost savings, energy independence, and reduced carbon footprint

• Although rising demand supports growth, wider adoption depends on financing, regulatory support, and technological standardization. Investment in scalable, modular solutions, interoperability, and advanced monitoring will be critical to meeting global demand and sustaining competitive advantage

Restraint/Challenge

“High Capital Costs and Complexity of Integration”

• The relatively high upfront cost of microgrid systems, including generation, storage, and control infrastructure, remains a key challenge, limiting adoption among cost-sensitive organizations. Complex design, installation, and operational requirements further contribute to capital and operational expenditures

• Limited awareness and technical expertise restrict adoption across certain sectors, particularly for small and medium enterprises and remote communities. Knowledge gaps in energy management, regulatory compliance, and financial incentives can slow deployment

• Integration with existing power infrastructure and compliance with grid codes adds complexity and cost. Advanced monitoring, intelligent controls, and interconnection requirements necessitate skilled labor, specialized software, and long-term maintenance plans

• For instance, in 2024, microgrid deployments in educational campuses and healthcare facilities by ABB and Schneider Electric faced delayed implementation due to high installation costs, regulatory approvals, and system integration challenges. These factors affected project timelines and required additional investment in training and support

• Overcoming these challenges will require cost-effective design, standardized solutions, and supportive policies. Collaboration with utilities, technology providers, and regulatory bodies can unlock the full potential of microgrids, while developing financing options, turnkey solutions, and educational initiatives will accelerate market adoption

North America Microgrid Market Scope

The market is segmented on the basis of grid type, connectivity, offering, vertical, and power source.

• By Grid Type

On the basis of grid type, the North America microgrid market is segmented into Alternate Current Microgrid, Direct Current Microgrid, and Hybrid. The Alternate Current Microgrid segment held the largest market revenue share in 2025 driven by the extensive existing infrastructure built around AC power distribution and its compatibility with conventional electrical systems. AC microgrids are widely adopted as they support a broad range of applications and facilitate easier integration with utility networks. They are also preferred for large-scale deployments in commercial and industrial facilities due to their ability to handle higher loads efficiently. In addition, AC microgrids offer flexibility in maintenance and operational scalability.

The Direct Current Microgrid segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its higher energy efficiency and reduced conversion losses, making it ideal for renewable energy sources and modern DC‑native loads. DC microgrids are increasingly preferred for their simplified architecture, faster response times, and easier integration with solar PV and battery storage. They are especially suitable for residential complexes, campuses, and remote industrial installations. Growing adoption of DC appliances and electronics further strengthens this segment’s expansion.

• By Connectivity

On the basis of connectivity, the North America microgrid market is segmented into Grid Connected and Remote/Island. The Grid Connected segment held the largest market revenue share in 2025 driven by the widespread implementation of interconnected systems that enhance grid reliability and support energy exchange with traditional utility networks. Grid-connected microgrids allow for optimized energy management and cost savings through demand response programs. They also help utilities balance peak loads and reduce energy wastage. Seamless integration with renewable sources such as solar and wind further boosts their deployment across urban and semi-urban areas.

The Remote/Island segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for off-grid solutions in areas with limited or no access to centralized power. Remote/Island microgrids provide dependable power for isolated communities, military bases, and critical infrastructure. They also help reduce dependency on diesel generators and fossil fuels, promoting sustainable energy use. Technological advancements in energy storage and hybrid systems make these microgrids more reliable and cost-effective.

• By Offering

On the basis of offering, the North America microgrid market is segmented into Hardware, Software and Services. The Hardware segment held the largest market revenue share in 2025 driven by significant investments in core components such as inverters, controllers, and energy storage systems that form the fundamental physical layer of microgrid installations. Hardware reliability directly impacts microgrid performance, efficiency, and longevity. The growth of large-scale industrial and institutional microgrids has further bolstered demand for advanced hardware solutions. In addition, integration with renewable energy systems has made robust hardware offerings critical for long-term energy stability.

The Software segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing adoption of advanced energy management platforms and analytics tools that enhance operational efficiency. Software solutions enable real-time monitoring, predictive maintenance, and intelligent load balancing. They also facilitate seamless integration with IoT devices, cloud platforms, and smart grids. Growing emphasis on digitalization and remote management of microgrids further accelerates software adoption.

• By Vertical

On the basis of vertical, the North America microgrid market is segmented into Healthcare, Educational Institutions, Industrial, Military and Electric Utility. The Industrial segment held the largest market revenue share in 2025 driven by strong demand for resilient and cost-effective power supply in manufacturing units and heavy industries. Industrial microgrids ensure uninterrupted operations, reduce energy costs, and enhance productivity. They are also crucial for facilities with critical processes that cannot tolerate power interruptions. Integration of renewables in industrial microgrids supports sustainability initiatives and regulatory compliance.

The Healthcare segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the critical need for uninterrupted power in hospitals and medical facilities. Healthcare microgrids ensure continuous operation of life-saving equipment and critical IT systems. Rising awareness of energy resilience and disaster preparedness is driving hospitals to adopt hybrid and backup microgrid solutions. In addition, regulatory support and incentives for renewable integration in healthcare facilities support segment growth. Remote monitoring and smart energy management systems further enhance operational reliability.

• By Power Source

On the basis of power source, the North America microgrid market is segmented into Natural Gas, Combined Heat and Power, Diesel, Solar, Fuel Cells, and Others. The Natural Gas segment held the largest market revenue share in 2025 driven by its reliability, established use in distributed generation, and ability to deliver stable power output. Natural gas microgrids are cost-effective, scalable, and suitable for industrial and commercial applications. They offer lower emissions compared to conventional diesel-based systems. The segment benefits from mature infrastructure, widespread availability, and high operational efficiency.

The Solar segment is expected to witness the fastest growth rate from 2026 to 2033, driven by falling solar photovoltaic costs, supportive renewable energy policies, and increased integration with battery storage systems. Solar-powered microgrids provide clean, sustainable energy solutions while reducing reliance on fossil fuels. They are particularly suitable for remote areas, campuses, and residential communities. Advances in storage technologies and smart controllers further enhance solar microgrid efficiency and reliability. Growing environmental awareness and net-zero energy goals are accelerating solar adoption in microgrid deployments.

North America Microgrid Market Regional Analysis

- U.S. microgrid market captured the largest revenue share in 2025 within North America, driven by extensive investments in grid resilience, renewable integration, and critical infrastructure protection. Microgrid deployment continues to expand across military installations, healthcare facilities, universities, and municipal applications to mitigate outage risks and enhance energy security

- Federal and state resilience programs, coupled with utility‑led initiatives, support advanced energy management systems, large‑scale battery storage, and distributed generation projects

- The increasing frequency of extreme weather events and aging grid infrastructure further accelerates adoption of microgrids as reliable, decentralized energy solutions

Canada Microgrid Market Insight

The Canada microgrid market is the fastest growing in North America, propelled by initiatives to replace diesel generation in remote and Indigenous communities with hybrid renewable microgrids. Provincial programs in Ontario, British Columbia, and Quebec support remote electrification and sustainability goals, increasing demand for off‑grid and hybrid systems. Industrial sectors and mining operations are also embracing microgrid technologies to improve energy reliability and reduce operational costs. In addition, advancements in energy storage integration and supportive policy measures strengthen Canada’s growth trajectory within the regional microgrid landscape.

North America Microgrid Market Share

The North America microgrid industry is primarily led by well-established companies, including:

• S&C Electric Company (U.S.)

• General Electric Company (U.S.)

• Honeywell International Inc. (U.S.)

• PowerSecure Inc. (U.S.)

• Ameresco Inc. (U.S.)

• Blue Planet Energy (U.S.)

• Enchanted Rock (U.S.)

• Bloom Energy Corporation (U.S.)

• CleanSpark, Inc. (U.S.)

• Cummins Inc. (U.S.)

• Exergonix, Inc. (U.S.)

• BoxPower Inc. (U.S.)

• Spirae LLC (U.S.)

• One Power Company (U.S.)

• Tigo Energy, Inc. (U.S.)

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.