North America Neurosurgery Market

Размер рынка в млрд долларов США

CAGR :

%

USD

5.46 Billion

USD

15.90 Billion

2025

2033

USD

5.46 Billion

USD

15.90 Billion

2025

2033

| 2026 –2033 | |

| USD 5.46 Billion | |

| USD 15.90 Billion | |

| % | |

|

North America Neurosurgery Market Segmentation, By Product Type (Neurosurgery Devices, Neurosurgery Software, and Consumables), Application (Aneurysms, Arteriovenous Malformation (AVM), Brain Tumors, Carotid Artery Blockage/Stenosis, Cerebrovascular Surgery, Cortical Mapping, Epilepsy, Functional Neurosurgery, Intraoperative Angiography, Parkinson's Disease and Tremors, Peripheral Nerve Surgery, Pituitary Tumors, Radiosurgery, Skull Base Surgery, Spine Surgery, Stereotactic Neurosurgery, Trauma Surgery, Trigeminal Neuralgia, and Others), Age Group (Pediatric, Adult, and Geriatric), End User (Hospitals, Neurosurgery Centers, Research Centers, Ambulatory Surgical Centers, and Others), Distribution Channel (Direct Tender, Third Party Distributors, and Others)- Industry Trends and Forecast to 2033

North America Neurosurgery Market Size

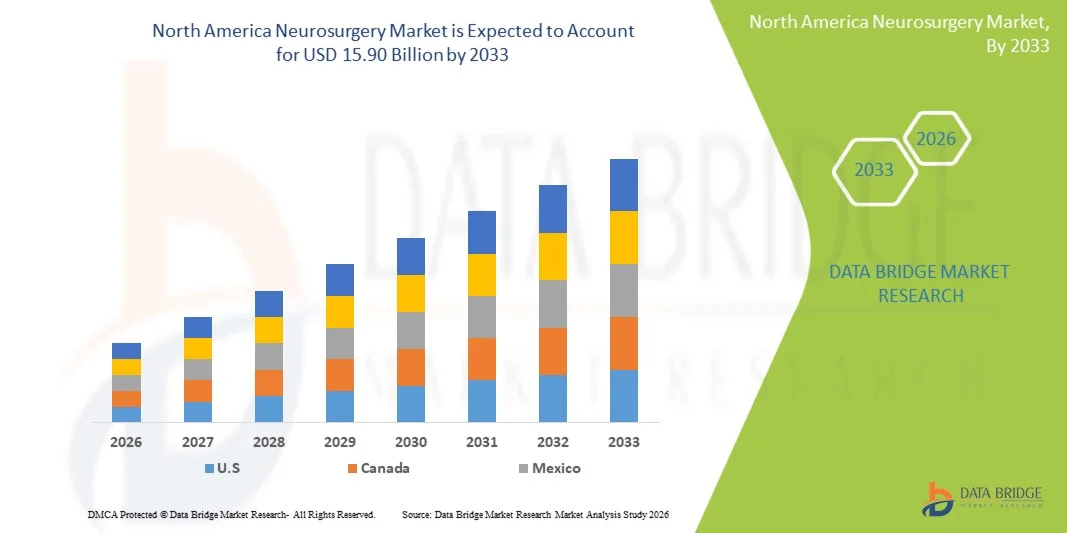

- The North America neurosurgery market size was valued at USD 5.46 billion in 2025 and is expected to reach USD 15.90 billion by 2033, at a CAGR of 14.3% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological disorders, rising demand for minimally invasive brain and spine procedures, and continuous technological advancements in neurosurgical equipment and imaging systems, driving improved clinical outcomes across healthcare facilities

- Furthermore, the expanding geriatric population, growing investments in healthcare infrastructure, and strong presence of leading medical device manufacturers are establishing advanced neurosurgical solutions as a critical component of modern healthcare. These converging factors are accelerating the adoption of neurosurgery technologies, thereby significantly boosting the region’s market growth

North America Neurosurgery Market Analysis

- Neurosurgery, encompassing surgical procedures for the treatment of disorders affecting the brain, spine, and nervous system, is a critical component of advanced healthcare systems across North America due to its role in managing complex conditions such as brain tumors, traumatic brain injuries, and spinal disorders with high precision and improved patient outcomes

- The escalating demand for neurosurgical procedures is primarily fueled by the rising prevalence of neurological disorders, increasing incidence of traumatic injuries, and growing preference for minimally invasive and image-guided surgical techniques among both patients and healthcare providers

- The United States dominated the neurosurgery market with the largest revenue share of 78.5% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of leading medical device and technology providers, experiencing substantial growth in neurosurgical procedures driven by rapid adoption of robotic-assisted surgery and intraoperative imaging innovations

- Canada is expected to be the fastest growing country in the neurosurgery market during the forecast period driven by increasing healthcare investments, expanding access to advanced neurosurgical care, and rising adoption of minimally invasive and technologically advanced surgical procedures

- Spine surgery segment dominated the neurosurgery market with a market share of 47.3% in 2025, driven by the high prevalence of degenerative spine disorders, growing aging population, and increasing demand for minimally invasive spinal procedures

Report Scope and North America Neurosurgery Market Segmentation

|

Attributes |

North America Neurosurgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Neurosurgery Market Trends

“Rising Adoption of Minimally Invasive and Robotic-Assisted Neurosurgery”

- A significant and accelerating trend in the North America neurosurgery market is the increasing adoption of minimally invasive and robotic-assisted surgical techniques, which are transforming the precision and efficiency of complex brain and spine procedures. This integration of advanced technologies is significantly enhancing surgical outcomes and reducing patient recovery times

- For instance, robotic-assisted platforms and neuronavigation systems are being widely utilized across hospitals in the United States to perform highly precise spinal and cranial procedures with reduced complications. Similarly, intraoperative imaging technologies such as MRI and CT are enabling real-time guidance during surgeries, improving accuracy and safety

- Technological advancements in neurosurgery enable features such as enhanced visualization, real-time data integration, and improved surgical planning. For instance, advanced navigation systems allow surgeons to map critical brain structures and avoid damage to surrounding tissues, while robotic systems enhance dexterity and control during delicate operations. Furthermore, minimally invasive approaches reduce hospital stays and postoperative complications, offering significant benefits to patients

- The seamless integration of neurosurgical technologies with digital healthcare systems facilitates improved workflow and patient management. Through centralized platforms, healthcare providers can access patient data, imaging results, and surgical plans, creating a more coordinated and efficient treatment environment

- This trend towards more precise, efficient, and technology-driven neurosurgical procedures is fundamentally reshaping treatment standards in North America. Consequently, leading companies such as Medtronic plc are developing advanced neurosurgical solutions, including robotic-assisted systems and navigation platforms, to enhance surgical performance and patient outcomes

- The demand for advanced neurosurgical technologies is growing rapidly across hospitals and specialty clinics, as healthcare providers increasingly prioritize precision, safety, and improved patient recovery outcomes

- Increasing focus on outpatient and ambulatory surgical centers is further shaping the market, as healthcare systems aim to reduce hospitalization costs and improve patient throughput while maintaining high standards of neurosurgical care

North America Neurosurgery Market Dynamics

Driver

“Increasing Neurological Disorder Burden and Healthcare Investments”

- The rising prevalence of neurological disorders, coupled with increasing healthcare investments, is a significant driver for the heightened demand for neurosurgical procedures across North America

- For instance, in recent years, companies such as Stryker Corporation have expanded their neurosurgical portfolios through product innovations and acquisitions, aiming to strengthen their presence in cranial and spinal surgery segments. Such strategic initiatives by key players are expected to drive the neurosurgery market growth in the forecast period

- As the incidence of conditions such as brain tumors, epilepsy, and spinal disorders continues to rise, there is a growing need for advanced surgical interventions. Neurosurgery offers critical solutions for managing these conditions, improving survival rates and quality of life for patients

- Furthermore, the increasing adoption of advanced imaging systems, surgical robotics, and navigation technologies is making neurosurgery more effective and accessible, particularly in developed healthcare systems such as the United States and Canada

- The growing emphasis on early diagnosis, improved healthcare infrastructure, and the availability of skilled neurosurgeons are key factors propelling the adoption of neurosurgical procedures across hospitals and specialty centers. The trend towards technologically advanced operating rooms and integrated surgical systems further contributes to market growth

Restraint/Challenge

“High Procedure Costs and Limited Accessibility”

- The high cost associated with neurosurgical procedures and advanced equipment poses a significant challenge to broader market adoption. Neurosurgery often requires expensive technologies such as robotic systems, intraoperative imaging, and specialized surgical instruments, increasing the overall treatment cost

- For instance, the adoption of advanced neurosurgical systems in smaller healthcare facilities can be limited due to budget constraints and high capital investment requirements

- Addressing cost-related challenges and improving accessibility to neurosurgical care is crucial for expanding market reach. Companies such as Johnson & Johnson (through its medical device segment) are focusing on developing cost-effective and scalable surgical solutions to support wider adoption. In addition, disparities in access to specialized neurosurgical care between urban and rural areas can limit timely treatment for patients

- Disparities in access to neurosurgical care between urban and rural areas across the United States and Canada further restrict timely diagnosis and treatment, impacting patient outcomes

- In addition, stringent regulatory requirements and lengthy approval timelines for new neurosurgical devices can delay market entry for innovative technologies, slowing overall adoption rates

- While technological advancements continue to improve surgical outcomes, affordability and accessibility remain key barriers, particularly for underserved populations. Ensuring broader access through healthcare policy support, infrastructure development, and cost optimization strategies will be vital for sustained market growth

North America Neurosurgery Market Scope

The market is segmented on the basis of product type, application, age group, end user, and distribution channel.

- By Product Type

On the basis of product type, the North America neurosurgery market is segmented into neurosurgery devices, neurosurgery software, and consumables. The neurosurgery devices segment dominated the market with the largest market revenue share in 2025, driven by the extensive use of advanced surgical instruments such as neuroendoscopes, surgical microscopes, and stereotactic systems in complex brain and spine procedures. Hospitals heavily rely on these devices to enhance surgical precision and improve patient outcomes. The continuous innovation in robotic-assisted systems and intraoperative imaging technologies further strengthens the dominance of this segment. In addition, the growing number of neurosurgical procedures and increasing investments in advanced operating room infrastructure contribute significantly to segment growth. The demand for high-performance and reliable devices remains strong across major healthcare facilities.

The neurosurgery software segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing adoption of surgical planning, navigation, and data integration platforms. These software solutions enable real-time imaging analysis, improved decision-making, and enhanced workflow efficiency during neurosurgical procedures. The integration of artificial intelligence (AI) and machine learning for predictive analytics and surgical guidance is further accelerating adoption. Healthcare providers are increasingly leveraging software to reduce procedural risks and improve accuracy. The shift toward digital healthcare ecosystems and connected operating rooms is also supporting the rapid expansion of this segment.

- By Application

On the basis of application, the North America neurosurgery market is segmented into aneurysms, arteriovenous malformation (AVM), brain tumors, carotid artery blockage/stenosis, cerebrovascular surgery, cortical mapping, epilepsy, functional neurosurgery, intraoperative angiography, Parkinson's disease and tremors, peripheral nerve surgery, pituitary tumors, radiosurgery, skull base surgery, spine surgery, stereotactic neurosurgery, trauma surgery, trigeminal neuralgia, and others. The spine surgery segment dominated the market in 2025 with a market share of 47.3%, driven by the high prevalence of degenerative spine disorders, spinal injuries, and age-related conditions. Increasing demand for minimally invasive spine procedures and advancements in spinal implants and navigation systems further support segment growth. Hospitals are witnessing a surge in spinal surgeries due to sedentary lifestyles and an aging population. The availability of advanced surgical tools and improved postoperative outcomes also contribute to the dominance of this segment. Continuous innovation in spinal robotics and imaging technologies further strengthens its market position.

The brain tumors segment is expected to witness the fastest growth rate during the forecast period, driven by the increasing incidence of brain cancer and advancements in tumor resection technologies. The adoption of precision-based surgical techniques and intraoperative imaging is improving treatment success rates. Growing awareness regarding early diagnosis and treatment options is also contributing to increased surgical volumes. In addition, the integration of targeted therapies and radiosurgery is enhancing treatment effectiveness. The need for specialized neurosurgical interventions in oncology is expected to significantly boost this segment’s growth.

- By Age Group

On the basis of age group, the market is segmented into pediatric, adult, and geriatric. The adult segment dominated the market with the largest revenue share in 2025, driven by the high incidence of neurological conditions such as brain tumors, spinal disorders, and traumatic injuries among the adult population. Adults represent the largest patient pool undergoing neurosurgical procedures due to lifestyle-related factors and occupational hazards. The availability of advanced treatment options and improved healthcare access further supports segment dominance. In addition, increasing awareness and early diagnosis contribute to higher surgical intervention rates in this group. The demand for neurosurgical care remains consistently high among adults across North America.

The geriatric segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rapidly aging population and increasing prevalence of age-related neurological disorders such as Parkinson’s disease and degenerative spine conditions. Older adults often require complex neurosurgical interventions, leading to rising demand for specialized care. Advancements in minimally invasive procedures are making surgeries safer for elderly patients. Healthcare systems are increasingly focusing on geriatric care, further supporting segment growth. The rising life expectancy and improved access to healthcare services are key factors driving this segment.

- By End User

On the basis of end user, the market is segmented into hospitals, neurosurgery centers, research centers, ambulatory surgical centers, and others. The hospitals segment dominated the market in 2025, driven by the availability of advanced infrastructure, skilled neurosurgeons, and comprehensive patient care facilities. Hospitals handle a high volume of complex neurosurgical procedures, including emergency and trauma cases. The presence of integrated operating rooms and advanced imaging systems further supports their dominance. In addition, favorable reimbursement policies and government funding contribute to higher patient inflow. Hospitals remain the primary point of care for neurosurgical treatments across the region.

The ambulatory surgical centers segment is anticipated to witness the fastest growth rate during the forecast period, fueled by the increasing shift toward outpatient procedures and cost-effective treatment options. These centers offer reduced hospital stays, faster recovery times, and lower overall treatment costs. Advancements in minimally invasive techniques are enabling more procedures to be performed in outpatient settings. Patients are increasingly preferring ambulatory centers for convenience and efficiency. The growing focus on value-based healthcare is further accelerating the adoption of these facilities.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third party distributors, and others. The direct tender segment dominated the market with the largest revenue share in 2025, driven by bulk procurement by hospitals and large healthcare institutions. Direct purchasing allows healthcare providers to negotiate better pricing and ensure consistent supply of critical neurosurgical equipment and consumables. This channel is widely preferred for high-value medical devices and long-term procurement contracts. Strong relationships between manufacturers and healthcare providers further support this segment’s dominance. The need for reliable and timely delivery of advanced surgical tools is a key contributing factor.

The third party distributors segment is expected to witness the fastest growth rate from 2026 to 2033, driven by their ability to expand market reach and provide efficient distribution networks across diverse healthcare settings. These distributors play a crucial role in supplying products to smaller hospitals and clinics. They offer logistical support, inventory management, and faster delivery services, enhancing accessibility. Increasing demand from remote and underserved areas is further boosting this segment. The growing complexity of supply chains and need for streamlined distribution channels are key factors driving its growth.

North America Neurosurgery Market Regional Analysis

- The United States dominated the neurosurgery market with the largest revenue share of 78.5% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of leading medical device and technology providers, experiencing substantial growth in neurosurgical procedures driven by rapid adoption of robotic-assisted surgery and intraoperative imaging innovations

- Healthcare providers in the country highly prioritize precision, advanced surgical technologies, and improved patient outcomes, leading to widespread adoption of robotic-assisted systems, intraoperative imaging, and minimally invasive neurosurgical techniques

- This strong adoption is further supported by high healthcare expenditure, the presence of leading industry players, and a technologically advanced medical ecosystem, establishing neurosurgical solutions as a critical component of modern healthcare systems for both complex and routine neurological procedures

U.S. Neurosurgery Market Insight

The United States neurosurgery market captured the largest revenue share of 78.5% in 2025 within North America, fueled by the high prevalence of neurological disorders and the strong adoption of advanced surgical technologies. Healthcare providers are increasingly prioritizing precision-driven procedures such as minimally invasive and robotic-assisted neurosurgeries. The growing demand for improved patient outcomes, coupled with robust investments in healthcare infrastructure and R&D, further propels the market. Moreover, the increasing integration of advanced imaging systems, navigation platforms, and AI-based surgical planning tools is significantly contributing to the market's expansion.

Canada Neurosurgery Market Insight

The Canada neurosurgery market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare investments and improving access to advanced neurosurgical care. The rise in neurological disorders and aging population is fostering the demand for specialized surgical procedures. Canadian healthcare providers are also adopting minimally invasive and image-guided neurosurgical techniques to enhance patient outcomes. The country is witnessing steady growth across hospitals and specialty centers, supported by government funding and advancements in medical technologies.

Mexico Neurosurgery Market Insight

The Mexico neurosurgery market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improving healthcare infrastructure and rising awareness regarding neurological treatments. In addition, increasing investments in hospital facilities and the adoption of advanced surgical equipment are encouraging the use of neurosurgical procedures. The growing burden of neurological conditions and trauma cases is further supporting market demand. Mexico’s expanding private healthcare sector and focus on accessible treatment solutions are expected to continue stimulating market growth.

North America Neurosurgery Market Share

The North America Neurosurgery industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- B. Braun SE (Germany)

- Elekta AB (Sweden)

- Integra LifeSciences Holdings Corporation (U.S.)

- Zimmer Biomet (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Brainlab SE (Germany)

- Renishaw plc (U.K.)

- Natus Medical Incorporated (U.S.)

- Synaptive Medical Inc. (Canada)

- Penumbra, Inc. (U.S.)

- Abbott (U.S.)

- Terumo Corporation (Japan)

- Smith & Nephew (U.K.)

- Olympus Corporation (Japan)

- Richard Wolf GmbH (Germany)

- Leica Microsystems GmbH (Germany)

- Carl Zeiss AG (Germany)

What are the Recent Developments in North America Neurosurgery Market?

- In March 2026, Medtronic plc announced that the U.S. FDA cleared its Stealth AXiS surgical system for cranial and ENT procedures, expanding its application beyond spine surgery. The system integrates surgical navigation, imaging, robotics, and AI-based brain mapping to enhance precision and visualization during complex neurosurgeries. This development highlights the growing role of AI-enabled platforms in improving surgical planning and intraoperative accuracy in North America

- In March 2026, Medtronic plc entered into an agreement to acquire Scientia Vascular for approximately USD 550 million, strengthening its neurovascular portfolio. The acquisition is aimed at enhancing capabilities in treating stroke and other neurovascular conditions, reflecting ongoing consolidation and innovation within the neurosurgery ecosystem

- In January 2026, Medtronic plc partnered with Precision Neuroscience to integrate a brain-computer interface (BCI) with its StealthStation surgical navigation system. This collaboration focuses on combining high-resolution cortical mapping with existing surgical platforms, accelerating the development of next-generation neurosurgical technologies

- In June 2025, Stryker Corporation launched the AXS Lift Intracranial Base Catheter, designed to improve neurovascular access and streamline complex procedures. The device enhances stability and reduces the need for multiple catheter exchanges, supporting more efficient and safer neurosurgical interventions

- In September 2024, Medtronic plc expanded its AiBLE™ spine surgery ecosystem with new technologies and a partnership with Siemens Healthineers. The updated Mazor robotic system integrates AI, advanced imaging, and surgical planning tools, enabling comprehensive intraoperative guidance and improving outcomes in spinal neurosurgery

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.