Asia Pacific Computed Tomography Devices Market

市场规模(十亿美元)

CAGR :

%

USD

3.44 Billion

USD

5.56 Billion

2025

2033

USD

3.44 Billion

USD

5.56 Billion

2025

2033

| 2026 –2033 | |

| USD 3.44 Billion | |

| USD 5.56 Billion | |

| % | |

|

Asia-Pacific Computed Tomography Devices Market Segmentation, By Product Type (Low Slice CT Scanner (64 slices)), Application Type (Cardiovascular Applications, Oncology, Neurovascular Application, Abdomen and Pelvic Application, Pulmonary Angiogram, Spinal Application, and Musculoskeletal Application), End User (Diagnostic Centres, Clinics, Hospitals, and Others)- Industry Trends and Forecast to 2033

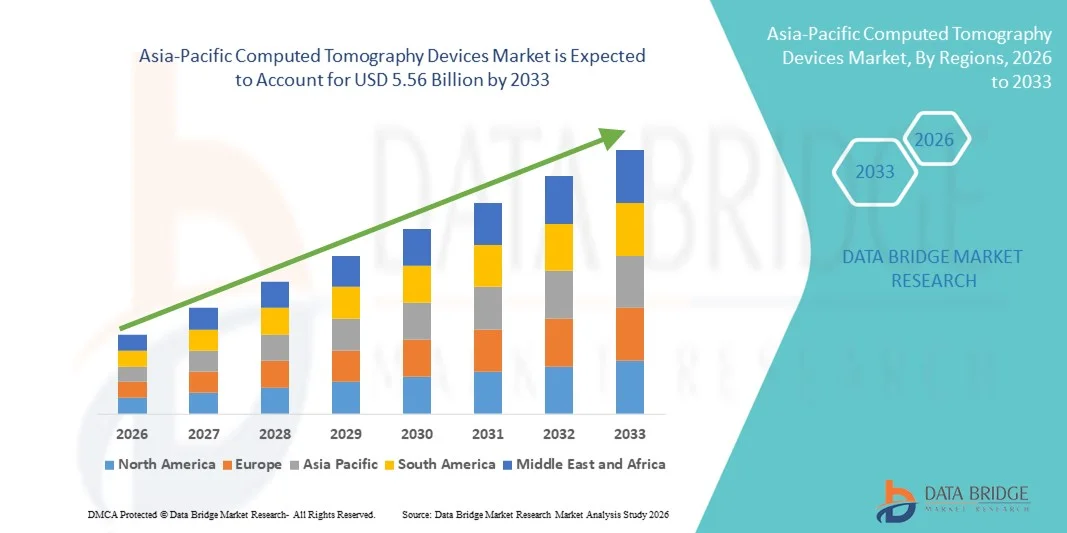

Asia-Pacific Computed Tomography Devices Market Size

- The Asia-Pacific computed tomography devices market size was valued at USD 3.44 billion in 2025 and is expected to reach USD 5.56 billion by 2033, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by the rising burden of chronic diseases, increasing demand for early and accurate diagnostic imaging, and continuous technological advancements in multi-slice and AI-integrated CT systems across the region

- Furthermore, expanding healthcare infrastructure, growing investments in public and private hospitals, and supportive government initiatives to enhance diagnostic capabilities are establishing computed tomography devices as a critical component of modern medical imaging. These converging factors are accelerating the adoption of CT systems, thereby significantly boosting the industry's growth

Asia-Pacific Computed Tomography Devices Market Analysis

- Computed tomography (CT) devices, delivering high-resolution cross-sectional imaging for accurate and rapid diagnosis, are increasingly essential across hospitals and diagnostic centers in the Asia-Pacific region due to their advanced imaging capabilities, faster scan speeds, and integration with AI-based diagnostic software

- The escalating demand for CT systems is primarily driven by the rising incidence of cardiovascular diseases, cancer, and neurological disorders, along with expanding healthcare infrastructure and growing investments in advanced diagnostic technologies across emerging economies

- China dominated the Asia-Pacific computed tomography devices market with the largest revenue share of 38.6% in 2025, supported by large-scale hospital expansion programs, strong government healthcare reforms, and rising installation of high-end CT systems in tier-1 and tier-2 cities

- India is expected to be the fastest growing country in the Asia-Pacific computed tomography devices market during the forecast period due to increasing healthcare expenditure, expanding private diagnostic chains, and rising demand for early and preventive disease diagnosis

- High Slice CT Scanner (>64 slices) segment dominated the Asia-Pacific computed tomography devices market with a market share of 46.8% in 2025, driven by its superior image clarity, faster acquisition times, and extensive use in cardiovascular applications, oncology, and neurovascular application procedures across tertiary care hospitals

Report Scope and Asia-Pacific Computed Tomography Devices Market Segmentation

|

Attributes |

Asia-Pacific Computed Tomography Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Computed Tomography Devices Market Trends

AI-Integrated High-Slice Imaging and Workflow Automation

- A significant and accelerating trend in the Asia-Pacific computed tomography devices market is the rapid integration of artificial intelligence (AI) with high-slice CT systems to enhance diagnostic precision, automate workflow, and reduce scan time across high-volume hospitals and diagnostic centres

- For instance, leading manufacturers such as GE HealthCare and Siemens Healthineers are incorporating AI-powered reconstruction algorithms and dose optimization software into advanced CT platforms to improve image clarity while minimizing radiation exposure. Similarly, Canon Medical Systems Corporation is focusing on deep-learning reconstruction technologies to enhance low-dose imaging performance

- AI integration in CT devices enables automated lesion detection, smart workflow triaging, and advanced cardiovascular and neurovascular imaging analysis, improving diagnostic confidence and operational efficiency. Furthermore, automated dose modulation technologies help optimize radiation levels based on patient size and clinical indication, ensuring safer imaging procedures

- The seamless integration of CT systems with hospital information systems (HIS), radiology information systems (RIS), and picture archiving and communication systems (PACS) facilitates centralized data management and faster reporting workflows across healthcare networks in the region

- This trend towards more intelligent, faster, and lower-dose imaging systems is reshaping clinical expectations for diagnostic imaging accuracy and patient throughput. Consequently, companies such as United Imaging Healthcare are expanding AI-enabled CT portfolios tailored to large tertiary hospitals and expanding urban healthcare facilities

- The demand for AI-enhanced and high-slice CT systems is growing rapidly across both public and private healthcare sectors, as providers increasingly prioritize precision diagnostics, workflow optimization, and improved patient safety standards

- The integration of cloud-based image sharing and teleradiology solutions is further strengthening regional collaboration among radiologists, enabling faster second opinions and improved clinical decision-making across geographically dispersed facilities

Asia-Pacific Computed Tomography Devices Market Dynamics

Driver

Rising Chronic Disease Burden and Expanding Healthcare Infrastructure

- The increasing prevalence of chronic conditions such as cardiovascular diseases, cancer, and neurological disorders, coupled with expanding healthcare infrastructure investments across Asia-Pacific countries, is a significant driver for the heightened demand for computed tomography devices

- For instance, in March 2025, Philips Healthcare announced expansion of its advanced CT imaging portfolio in emerging Asian markets, aiming to strengthen diagnostic capabilities in secondary and tertiary hospitals. Such strategic expansions by key players are expected to drive the CT devices market growth in the forecast period

- As governments prioritize early disease detection and universal healthcare access, CT systems offer rapid and accurate imaging solutions essential for trauma care, oncology staging, and cardiovascular risk assessment

- Furthermore, the growing establishment of multi-specialty hospitals and independent diagnostic centres across China, India, and Southeast Asia is increasing procurement of medium and high slice CT scanners to meet rising patient volumes

- The demand for advanced CT imaging in emergency departments, cancer screening programs, and interventional radiology applications is accelerating procurement decisions, while public–private partnerships and favorable reimbursement frameworks further support adoption

- Increasing health insurance penetration across developing Asia-Pacific economies is improving patient affordability for advanced imaging procedures, thereby boosting CT scan volumes

- Government-led initiatives to modernize public hospitals and expand diagnostic infrastructure in rural and semi-urban regions are further strengthening long-term market growth prospects

Restraint/Challenge

High Capital Investment and Radiation Exposure Concerns

- The high capital investment required for purchasing, installing, and maintaining advanced CT systems presents a significant challenge to broader adoption, particularly for small and mid-sized healthcare facilities in developing Asia-Pacific economies

- For instance, budget constraints in rural hospitals often limit procurement of high-slice CT scanners, leading facilities to rely on lower-slice or refurbished systems, thereby slowing modernization of diagnostic infrastructure

- In addition, concerns regarding cumulative radiation exposure from repeated CT scans create hesitation among patients and regulatory bodies, especially for pediatric and preventive screening applications

- Addressing these challenges requires continuous innovation in low-dose imaging technologies, flexible financing models, and government-backed funding programs to support equipment upgrades

- While technological advancements are gradually reducing radiation dose and improving affordability through localized manufacturing, the substantial upfront investment and regulatory compliance requirements remain key barriers to widespread CT system penetration across the region

- The shortage of skilled radiologists and trained imaging technicians in certain emerging markets can limit optimal utilization of advanced CT systems and delay diagnostic reporting timelines

- Lengthy regulatory approval processes and varying compliance standards across Asia-Pacific countries can slow product launches and increase operational complexity for global manufacturers

Asia-Pacific Computed Tomography Devices Market Scope

The market is segmented on the basis of product type, application type, and end user.

- By Product Type

On the basis of product type, the Asia-Pacific computed tomography devices market is segmented into Low Slice CT Scanner (<64 slices), Medium Slice CT Scanner (64 slices), and High Slice CT Scanner (>64 slices). The High Slice CT Scanner (>64 slices) segment dominated the market with the largest market revenue share of 46.8% in 2025, driven by its superior image resolution, faster scan times, and advanced cardiac and neurovascular imaging capabilities. These systems are widely adopted in tertiary care hospitals and large diagnostic centers where complex cases require detailed anatomical visualization. High slice CT scanners are particularly preferred for cardiovascular applications, oncology staging, and trauma imaging due to their ability to capture high-quality images in shorter acquisition times. The growing burden of chronic diseases and increasing demand for precision diagnostics across China, Japan, and South Korea further support segment dominance. In addition, integration with AI-based reconstruction and dose optimization technologies enhances clinical efficiency and patient safety.

The Medium Slice CT Scanner (64 slices) segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its cost-effectiveness and balanced imaging performance suitable for mid-sized hospitals and diagnostic centres. These systems offer adequate imaging quality for routine cardiovascular, abdominal, and musculoskeletal examinations while maintaining relatively lower capital investment compared to high-slice systems. Expanding healthcare infrastructure in emerging economies such as India and Southeast Asian countries is accelerating procurement of 64-slice CT scanners. Government initiatives to upgrade district hospitals and improve diagnostic access are further supporting adoption. Moreover, medium slice scanners provide an optimal combination of affordability and performance, making them attractive for expanding private diagnostic chains.

- By Application Type

On the basis of application type, the Asia-Pacific computed tomography devices market is segmented into cardiovascular applications, oncology, neurovascular application, abdomen and pelvic application, pulmonary angiogram, spinal application, and musculoskeletal application. The Oncology segment dominated the market with the largest revenue share in 2025, driven by the rising incidence of cancer across Asia-Pacific countries and the increasing importance of early tumor detection and staging. CT imaging plays a crucial role in identifying tumor size, location, and metastasis, making it indispensable in oncology diagnostics and treatment planning. Growing government-led cancer screening programs and expansion of oncology centres are further boosting segment growth. High-slice CT systems are extensively utilized for accurate and rapid cancer evaluation. In addition, improved reimbursement frameworks in developed markets such as Japan and Australia support higher imaging volumes.

The Cardiovascular Applications segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing prevalence of heart diseases and demand for non-invasive coronary imaging solutions. CT angiography is increasingly preferred for rapid cardiac assessment due to its speed and high diagnostic accuracy. Rising lifestyle-related risk factors and aging populations across China and India are contributing to higher cardiac imaging demand. Technological advancements enabling low-dose cardiac scans and faster image reconstruction are further accelerating adoption. Expansion of specialized cardiac care centers across the region is also strengthening segment growth prospects.

- By End User

On the basis of end user, the Asia-Pacific computed tomography devices market is segmented into diagnostic centres, clinics, hospitals, and others. The Hospitals segment dominated the market with the largest revenue share in 2025, primarily due to the high patient inflow, availability of advanced imaging infrastructure, and capacity to invest in high-slice CT systems. Large public and private hospitals perform a broad range of imaging procedures including trauma, oncology, and cardiovascular scans. Government funding for hospital modernization programs in countries such as China and South Korea further supports equipment upgrades. Hospitals also benefit from integrated IT systems that streamline imaging workflows and reporting. In addition, the presence of skilled radiologists and multidisciplinary teams enhances CT utilization rates.

The Diagnostic Centres segment is projected to witness the fastest growth rate from 2026 to 2033, driven by the rapid expansion of private imaging chains and increasing preference for outpatient diagnostic services. Diagnostic centres often provide cost-effective and quicker imaging services compared to hospitals, attracting a growing patient base. Rising urbanization and increasing health awareness are contributing to higher imaging volumes in metropolitan and tier-2 cities. Many centres are investing in medium-slice CT scanners to balance affordability with performance. Furthermore, partnerships with hospitals and insurance providers are strengthening their role in the regional diagnostic ecosystem.

Asia-Pacific Computed Tomography Devices Market Regional Analysis

- China dominated the Asia-Pacific computed tomography devices market with the largest revenue share of 38.6% in 2025, supported by large-scale hospital expansion programs, strong government healthcare reforms, and rising installation of high-end CT systems in tier-1 and tier-2 cities

- Healthcare providers in the region highly prioritize early and accurate disease diagnosis, advanced imaging capabilities, and integration of AI-powered reconstruction software to improve clinical outcomes and operational efficiency

- This widespread adoption is further supported by rising chronic disease prevalence, expanding public and private hospital networks, improving reimbursement frameworks, and the growing focus on precision diagnostics, establishing computed tomography devices as a critical component of modern healthcare delivery across the region

The China Computed Tomography Devices Market Insight

The China computed tomography devices market captured the largest revenue share in 2025 within Asia-Pacific, fueled by rapid healthcare infrastructure modernization and strong government investment in advanced diagnostic imaging technologies. Hospitals are increasingly prioritizing high-slice CT systems to improve early detection of cancer, cardiovascular, and neurological disorders. The growing expansion of tertiary hospitals and public health reforms aimed at enhancing diagnostic capacity further propel the CT devices industry. Moreover, the increasing integration of AI-based image reconstruction and dose optimization technologies is significantly contributing to the market’s expansion.

Japan Computed Tomography Devices Market Insight

The Japan computed tomography devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by its aging population and strong demand for early disease detection. The country’s advanced healthcare infrastructure and high diagnostic imaging penetration support steady equipment upgrades. Japanese healthcare providers emphasize precision diagnostics and low-dose imaging technologies to enhance patient safety. The integration of AI-enabled CT systems and continuous technological innovation are further strengthening market growth across hospitals and specialty clinics.

India Computed Tomography Devices Market Insight

The India computed tomography devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rapid expansion of private hospitals and diagnostic chains. Increasing healthcare expenditure, rising chronic disease burden, and expanding medical tourism are encouraging investments in advanced imaging systems. Government initiatives to upgrade district hospitals and improve rural diagnostic access are further stimulating demand. The growing adoption of medium-slice CT scanners due to their affordability and performance balance is expected to continue to stimulate market growth.

South Korea Computed Tomography Devices Market Insight

The South Korea computed tomography devices market is expected to expand at a considerable CAGR during the forecast period, fueled by strong technological capabilities and high healthcare standards. The country’s well-developed hospital infrastructure and emphasis on innovation promote adoption of advanced high-slice CT systems. South Korea’s focus on precision medicine and early screening programs is increasing CT scan volumes. Integration of digital health platforms and AI-powered imaging analytics further supports sustained market expansion.

Asia-Pacific Computed Tomography Devices Market Share

The Asia-Pacific Computed Tomography Devices industry is primarily led by well-established companies, including:

- General Electric Company (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM Holdings Corporation (Japan)

- United Imaging Healthcare Co., Ltd. (China)

- Neusoft Medical Systems Co., Ltd. (China)

- Hitachi, Ltd. (Japan)

- Samsung Medison Co., Ltd. (South Korea)

- Mindray Medical International Limited (China)

- Carestream Health, Inc. (U.S.)

- Shimadzu Corporation (Japan)

- Allengers Medical Systems Limited (India)

- NeuroLogica Corp. (U.S.)

- Shenzhen Anke High Tech Co., Ltd. (China)

- Analogic Corporation (U.S.)

- Carestream Health Asia Pacific (U.S.)

- Planmeca Oy (Finland)

- Allengers OEM Private Limited (India)

- Apollo Radiance Technologies (India)

What are the Recent Developments in Asia-Pacific Computed Tomography Devices Market?

- In April 2025, Sengkang General Hospital in Singapore launched a Siemens Healthineers photon-counting CT scanner (NAEOTOM Alpha), which delivers sub-millimetre image detail with lower radiation exposure compared to conventional CT systems, enhancing diagnostic precision across clinical applications such as cardiology, oncology, and neurovascular imaging

- In January 2025, Royal Philips launched the AI-enabled CT 5300 system at the 23rd Asian Oceanian Congress of Radiology (AOCR) 2025 in Chennai, featuring advanced AI tools for diagnostics, interventional procedures and screening, aimed at improving workflow efficiency and imaging confidence across Asia-Pacific healthcare settings

- In December 2024, Philips unveiled the AI-powered CT 5300 system at the RSNA 2024 conference, featuring CT Smart Workflow with AI-driven tools that significantly reduce radiation dosing and patient positioning time across clinical imaging environments, positioning the device as a next-generation CT solution

- In September 2024, Philips Korea introduced the AI-powered CT 5300 scanner in the South Korean market, designed to enhance radiologist productivity and streamline diagnostic workflows through integrated artificial intelligence and advanced imaging features

- In May 2021, Siemens Healthineers unveiled the Somatom X.ceed high-resolution CT scanner, a new system designed for precise diagnostics and rapid scanning in demanding clinical settings, marking an early Asia-Pacific innovation push in multi-slice CT technologies

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。