Asia Pacific Optical Fiber Components Market

市场规模(十亿美元)

CAGR :

%

USD

4.89 Billion

USD

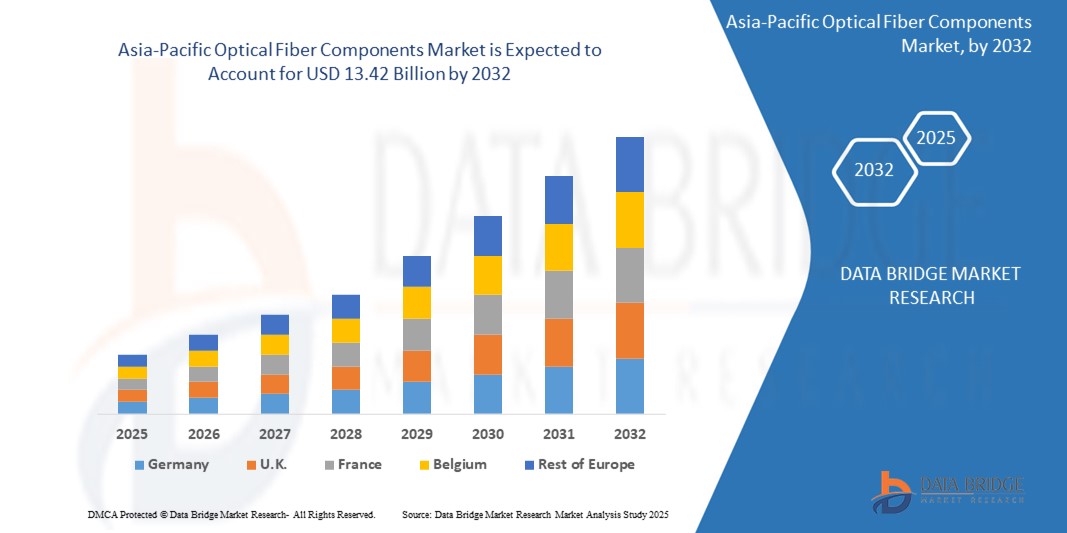

13.42 Billion

2024

2032

USD

4.89 Billion

USD

13.42 Billion

2024

2032

| 2025 –2032 | |

| USD 4.89 Billion | |

| USD 13.42 Billion | |

| % | |

|

亞太地區光纖組件市場正在快速成長,這並非偶然。隨著越來越多的人和企業比以往任何時候都更依賴高速互聯網,該地區正面臨著巨大的數位基礎設施擴展和升級的壓力。中國、印度、日本和韓國等國正引領這股潮流,紛紛推出5G網絡,建置更多資料中心,並大力投資雲端運算和智慧城市計畫。在幕後,連接器、收發器、擴大機和分路器等光纖組件承擔重任。這些元件有助於快速可靠地進行長距離資料傳輸,這對於從串流媒體和遠端辦公室到連網汽車和智慧工廠等各種應用都至關重要。隨著政府和私營部門攜手合作,改善寬頻存取並增強數位化能力,光纖技術正成為亞太地區互聯未來的支柱。

亞太光纖組件市場規模

- 預計到 2024 年亞太光纖組件市場規模將達到 48.9 億美元,到 2032 年預計將成長至 134.2 億美元,預測期內複合年增長率為 15.51%。

- 這一強勁成長反映了人們對高速連接日益增長的需求、5G 網路的部署,以及跨行業無縫通訊日益增長的重要性。隨著數位經濟的擴張,無線基礎設施正成為智慧城市、互聯家居、工業自動化和遠距醫療等所有領域的核心。

亞太光纖組件市場分析

- 光纖技術正在悄悄改變亞太地區的連結、通訊和數位化發展方式。從日常互聯網使用到人工智慧和雲端運算等先進技術,對更快、更可靠數據傳輸的需求正推動該地區各國升級其數位基礎設施。擴大機、連接器和收發器等光纖組件是這項轉變的核心,它們能夠實現長距離的無縫高速通訊。

- 這一成長背後的主要驅動力是 5G 的推出。但這不僅關乎更快的智慧型手機——5G 還為智慧城市、連網汽車、自動化工廠和遠距醫療提供支援。為了應對資料激增,網路需要更強大、更快速的主幹網路——而這正是光纖發揮作用的地方。無論是連接基地台還是支援超低延遲應用,光纖元件對於實現 5G 願景都至關重要。

- 在整個亞太地區,政府和私營部門都在加強投資力度。在中國和韓國等國家,重點是擴展和優化下一代網路;而在印度和東南亞等新興市場,則致力於縮小連通性差距,改善農村地區的網路覆蓋範圍。無論數位化發展處於哪個階段,光纖基礎設施都被視為打造互聯互通、面向未來的亞太地區的關鍵。

報告範圍和亞太光纖組件市場細分

|

屬性 |

亞太光纖組件市場關鍵洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

隨著該地區已開發經濟體和新興經濟體加強 5G 部署力度,對高頻寬、低延遲光纖基礎設施的需求激增,以支援密集網路和無縫回程連接。

BFSI、IT 和醫療保健等領域的企業正在升級到基於光纖的 LAN 和資料中心連接,以支援即時操作、雲端遷移和高級分析。

Governments in countries such as China, India, and Singapore are investing heavily in smart city infrastructure, requiring robust fiber connectivity for smart lighting, surveillance, public Wi-Fi, and connected transport systems.

With the rise of IoT devices and demand for localized data processing, fiber optics are becoming crucial for connecting distributed edge data centers and ensuring minimal latency

The boom in digital services is driving large-scale investments in hyperscale and regional data centers, all of which require high-performance optical fiber links for storage, processing, and communication |

|

Value Added Data Infosets |

|

Asia-Pacific Optical Fiber Components Market Trends

“Fiber First: Powering Asia-Pacific’s Digital Shift”

- The demand for high-speed, reliable internet is skyrocketing across Asia-Pacific, and optical fiber is at the heart of this transformation. As more countries roll out 5G networks, expand cloud infrastructure, and adopt smart technologies, the need for faster, more stable data transmission is becoming critical. Optical fiber components like connectors, amplifiers, and transceivers are enabling this shift, acting as the foundation for everything from streaming videos and remote work to real-time medical services and connected vehicles.

- One of the biggest drivers of this market is the massive rollout of 5G. Unlike previous generations, 5G isn’t just about faster phones it supports entire ecosystems of connected devices, from smart traffic systems to industrial automation. But to make 5G work, you need strong fiber backhaul to carry all that data. Countries like China, Japan, South Korea, and India are investing heavily in fiber infrastructure to keep up with the surge in data demand.

- At the same time, fiber deployment isn’t without its challenges. High installation costs, time-consuming regulatory processes, and a shortage of skilled labor in some emerging markets can slow progress. Laying cables through urban landscapes or across remote regions often involves complex logistics and significant expenses. However, innovative approaches like shared fiber networks and public-private partnerships are helping ease the burden and speed up implementation.

- Opportunities are also opening up with the growth of edge computing and IoT. As more devices collect and process data locally, the need for low-latency connections is increasing. Fiber supports this by offering the kind of speed and reliability wireless solutions can’t always guarantee. Whether it’s powering a smart factory or enabling real-time healthcare monitoring, fiber is proving essential in supporting advanced, data-driven applications across the region

Asia-Pacific Optical Fiber Components Market Dynamics

Drive

“Surging Digital Demand and 5G-Driven Fiber Expansion”

- Across Asia-Pacific, the digital landscape is evolving fast driven by a wave of 5G rollouts, smart city initiatives, and skyrocketing data consumption. From high-definition streaming and cloud computing to AI-powered services and IoT ecosystems, the region's hunger for speed and bandwidth is pushing telecom operators to upgrade their networks at scale. And at the core of these upgrades lies optical fiber.

- 5G, in particular, is a major catalyst. Unlike earlier mobile generations, 5G requires ultra-fast, low-latency fiber backhaul to support dense networks of small cells and edge data centers. This is prompting major investments in optical fiber components like transceivers, connectors, and amplifiers across countries such as China, India, South Korea, and Japan.

- Additionally, governments are playing an active role offering incentives, funding broadband expansion plans, and easing regulatory bottlenecks to accelerate fiber deployments. Public-private partnerships are on the rise, especially in rural and semi-urban areas where infrastructure gaps still exist.

- The growing presence of hyperscale data centers and rising demand for FTTH (Fiber-to-the-Home) connections further fuel the need for high-performance optical fiber networks. With more users working from home, gaming online, or accessing cloud-based tools, the importance of reliable, fiber-enabled connectivity has never been clearer.

Restraint/Challenge

“High Installation Costs and Infrastructure Complexities”

- Deploying fiber networks isn’t as simple as flipping a switch it involves significant capital investments, time, and logistical planning. In densely populated urban areas, challenges include right-of-way permissions, road excavation, and coordinating with multiple municipal agencies. Meanwhile, rural and remote regions face issues like difficult terrain, lack of existing infrastructure, and lower population density making returns on investment less attractive.

- Moreover, inconsistent regulatory environments across Asia-Pacific can delay projects. While some countries have streamlined their fiber deployment policies, others still struggle with fragmented permitting processes, import restrictions on components, or lack of clarity in infrastructure-sharing norms. For many operators, these factors not only increase deployment time and cost but also slow down the pace of digital inclusion in underserved areas.

• By Infrastructure Type

- Core Network: The backbone of all data transmission, core fiber networks connect regional and national hubs, ensuring high-speed communication over long distances. These are crucial for managing large-scale internet traffic, cloud connectivity, and intercontinental data flow.

- Access Network: These networks bring fiber directly to homes and businesses (FTTH/B). In Asia-Pacific, access networks are rapidly expanding due to rising broadband demand, especially in metro and suburban areas..

- Metro Network: These serve densely populated city centre’s and commercial zones. Metro fiber networks bridge the gap between core and access layers, supporting everything from 5G small cells to data-intensive urban applications.

- Data Center Interconnect: With the rise of hyperscale and edge data centers in APAC, there’s growing need for fast, reliable fiber links between them. This infrastructure type is key for cloud services, streaming platforms, and real-time analytics

• By Component

- Hardware: Hardware remains the dominant segment, driven by strong demand for transceivers, connectors, amplifiers, optical cables, and splitters. These components are vital for building out physical fiber networks supporting 5G, FTTx, and enterprise connectivity.

- Software: As networks get smarter and more complex, software is playing a growing role in monitoring, managing, and optimizing fiber performance. AI-based tools are helping operators reduce downtime, predict failures, and ensure efficiency.

- Services: Planning, deployment, and ongoing maintenance services are essential especially in large, multi-country rollouts. Skilled services help ensure quality control, faster installations, and long-term performance of fiber networks.

• By Network Technology

- 4G LTE: Still a major driver in several developing markets across Asia-Pacific, 4G networks heavily rely on fiber for backhaul and expansion, especially in semi-urban and rural zones.

- 5G: The fastest-growing segment, 5G demands dense, low-latency fiber backhaul to connect small cells, edge nodes, and data centers. Countries like China, South Korea, and India are heavily investing in fiber to support national 5G coverage.

- Wi-Fi 6/6E: Rising adoption in enterprise campuses, education, and healthcare environments is boosting the need for robust fiber links that support higher bandwidth and more devices simultaneously.

- 未來技術(6G、Edge、LEO 衛星):雖然這些技術仍處於早期開發階段,但最終將需要光纖來支援地面基礎設施並以超低延遲互連全球數據網路。

- 未來技術(6G、低地球軌道衛星)正處於早期發展階段,具有實現超高速連結的巨大長期潛力。

• 依所有權類型

- 電信業者:在大多數亞太市場中光纖擁有量領先。從5G回傳到最後一哩的FTTH網絡,Reliance Jio、中國行動和NTT等業者正積極擴張光纖覆蓋範圍。

- 雲端和內容供應商:Google、亞馬遜和騰訊等主要超大規模公司正在投資私有光纖網路來支援資料中心和區域雲區域。

- 私人網路供應商:製造、採礦和物流行業的企業正在部署自己的基於光纖的私人網絡,以實現安全、高效能的連接。

- 政府機構:政府在寬頻基礎建設中發揮重要作用,尤其是在農村和服務不足的地區。印度的BharatNet等項目以及東南亞的數位包容措施正在推動光纖部署。

按最終用戶

- 電信:在最大的消費領域,營運商正在建立和升級網路以應對不斷增長的數據需求並為未來的技術做好準備。

- 資料中心:隨著亞太地區成為資料中心,超大規模和邊緣資料中心依靠光纖實現快速、安全和可擴展的互連。

- 企業(BFSI、醫療保健、零售):這些行業需要可靠的高速連接,以實現數位化營運、遠端監控、AI 工具和基於雲端的應用程式。

- 政府和智慧城市:光纖為智慧基礎設施提供支援——從監視攝影機和交通感測器到公共 Wi-Fi 和電子政府平台。

- 運輸和物流:光纖支援鐵路、航空和航運領域的即時追蹤、自動化物流系統和互聯基礎設施。

- 住宅:智慧家庭、串流媒體、線上遊戲和物聯網設備的使用正在推動對光纖寬頻的需求,尤其是在城市和二線城市。

亞太光纖組件市場—區域發展分析

- 中國

中國在光纖部署方面引領該地區乃至全球。在大規模5G部署、智慧城市計畫以及對資料中心基礎設施的大規模投資的支持下,中國也擁有長飛光纖光纜和中天科技等主要製造商。政府對「新基建」和數位經濟擴張的重視,確保了電信、企業和工業領域對光纖組件的持續需求。

- 印度

印度的光纖部署正在快速成長,這得益於全國 5G 的部署、BharatNet 等農村寬頻專案以及資料中心的擴張。 Jio 和 Airtel 等電信業者正在大力投資 FTTH(光纖到府)和光纖回程,以支援日益增長的數據流量。政府的支持和公私合作正在幫助彌合二線城市和農村地區的連接缺口。

- 日本

日本擁有成熟且高度先進的光纖網路格局,FTTH 服務滲透率高,5G 部署也較早。該國正在投資升級其城域網路和核心網,以支援機器人、自動駕駛和智慧製造等新興應用——這些應用都需要高速、低延遲的光纖連接。

- 韓國

韓國是全球光纖普及率最高的國家之一。該國正在投資6G、邊緣運算和人工智慧等下一代技術,將進一步增強對光纖組件的需求。韓國持續升級其超密集網路基礎設施,正使其成為該地區數位轉型的典範。

- 東南亞

受智慧城市計畫、5G 部署和數位服務興起的推動,新加坡、馬來西亞、越南和泰國等國的光纖部署正在顯著成長。城市地區的基礎設施建設正在蓬勃發展,而農村地區仍在迎頭趕上,這為公共投資和私人創新創造了機會。

亞太光纖組件市場洞察

亞太光纖組件市場競爭激烈,既有全球光纖製造商,也有區域主導的供應商。

康寧公司、藤倉株式會社和住友電工等公司以端到端光纖解決方案引領全球市場。這些供應商提供從光纜、連接器到電信和資料中心應用的高密度光纖系統等各種產品。長飛光纖光纜(YOFC)、中天集團和亨通集團在中國市場佔據主導地位,並透過大規模5G和寬頻專案在區域內擴張。 Sterlite Technologies憑藉其一體化光纖網路解決方案以及在南亞和東南亞地區不斷增長的影響力,正在擴大市場份額。其他值得關注的參與者包括普睿司曼集團、康普、古河電工和灝訊,它們正在光纖到戶 (FTTH)、高速互連和無源光裝置等領域進行創新。

以下公司被公認為全球無線基礎設施市場的主要參與者:

- 康寧公司(美國)

- 住友電氣工業株式會社(日本)

- 普睿司曼集團(義大利)

- 長飛光纖光纜股份有限公司 (中國)

- 藤倉株式會社(日本)

- 萊尼(德國)

- LS Cable & System Ltd.(韓國)

- 亨通集團有限公司 (中國)

- 古河電氣工業株式會社(日本)

- 光纜公司(美國)

- LS Cable & System Ltd.(韓國)

- Proterial Cable America Inc.,(美國)

- Coherent Corporation (US)

- Finolex Cables Ltd. (India)

- CommScope Holding Company, Inc. (US)

- FiberHome Telecommunication Technologies Co., Ltd. (China)

- Aksh Optifibre (India)

- Art Photonics GmbH (Germany)

- RPG Cables (India)

- Nestor Cables (Finland)

- Orbis Oy (Finland)

- Birla Cable Ltd. (India)

- Belden Inc. (US)

- Fiber Mountain (US)

Latest Developments in Asia-Pacific Optical Fiber Components Market

- May 2025: Corning Incorporated announced the expansion of its optical fiber manufacturing facility in India to support growing regional demand driven by 5G and FTTH deployments.

- April 2025: YOFC launched a new ultra-low loss fiber product line optimized for long-haul 5G backhaul and metro network applications across Asia-Pacific..

- February 2025: Sterlite Technologies (STL) introduced AI-enabled fiber network design and monitoring tools to accelerate deployment and reduce downtime in dense urban areas.

- January 2025: Sumitomo Electric Industries unveiled its next-generation optical connectors designed for ultra-high-density data center interconnects and edge cloud environments...

- November 2024: ZTT Group partnered with a Southeast Asian telecom operator to deploy high-capacity submarine fiber cables aimed at boosting regional internet connectivity and cross-border data transmission.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。