Europe Optical Fiber Components Market

市场规模(十亿美元)

CAGR :

%

USD

5.40 Billion

USD

10.20 Billion

2024

2032

USD

5.40 Billion

USD

10.20 Billion

2024

2032

| 2025 –2032 | |

| USD 5.40 Billion | |

| USD 10.20 Billion | |

| % | |

|

歐洲光纖組件市場正在快速發展,這得益於高速寬頻計畫的不斷擴展、5G 部署的不斷增長以及該地區對數位化永續發展的大力推動。歐盟致力於建立千兆社會並彌合數位鴻溝,而光纖基礎設施對於實現超高速、低延遲連接至關重要。連接器、收發器、放大器和分路器等光學組件正在為 5G 提供穩健的回程,增強 FTTH(光纖到戶)的普及率,並滿足智慧城市、雲端平台和工業自動化日益增長的數據需求。隨著德國、法國、英國和北歐等國家升級傳統銅纜網路並將光纖覆蓋範圍擴展到服務不足的地區,對可靠且可擴展的光纖組件的需求持續增長,使其成為歐洲數位化轉型之旅的重要組成部分。

歐洲光纖組件市場規模

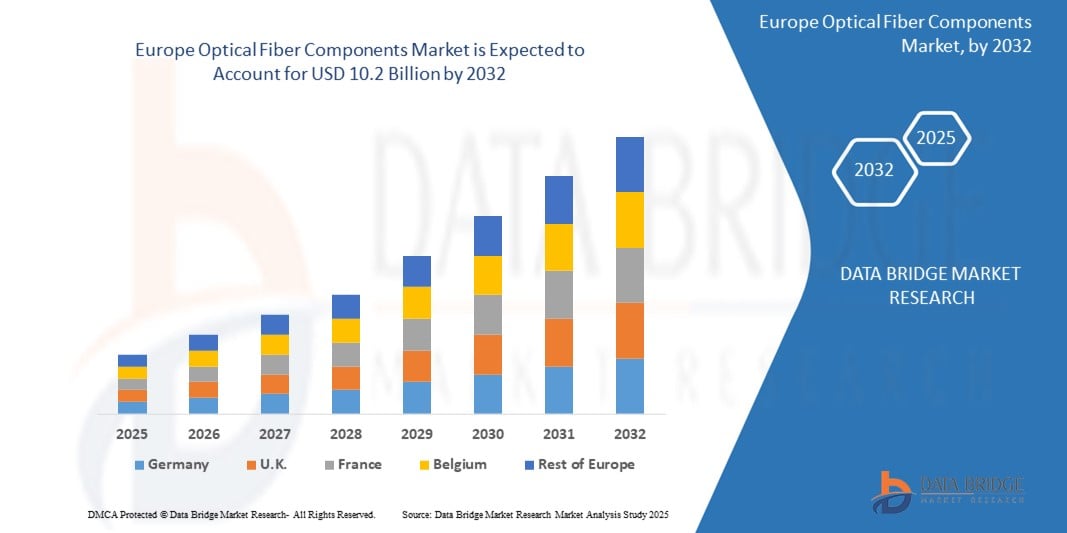

- 預計到 2024 年歐洲光纖組件市場規模將達到 54 億美元,到 2032 年預計將達到 102 億美元,預測期內複合年增長率為 9.51%......

- 這一強勁成長反映了人們對高速連接日益增長的需求、5G 網路的部署,以及跨行業無縫通訊日益增長的重要性。隨著數位經濟的擴張,無線基礎設施正成為智慧城市、互聯家居、工業自動化和遠距醫療等所有領域的核心。

歐洲光纖組件市場分析

- 光纖正在重新定義歐洲的通訊方式,為從日常互聯網使用到關鍵工業運營的方方面面提供支援。隨著對更快、更安全、更可靠連接的需求不斷增長,該地區各國正在加速光纖部署,以支援下一代數位基礎設施。無論是家庭高速寬頻,或是行動網路的穩健光纖回程,光纖組件都是歐洲數位轉型的核心。

- 推動這一勢頭的因素是5G部署、雲端運算和智慧城市計劃的激增。光纖不僅傳輸數據,還能提供人工智慧、物聯網和自主系統等技術蓬勃發展所需的速度和規模。為了實現這一點,網路必須更加密集、反應更快、面向未來。因此,收發器、放大器和連接器等組件至關重要,它們能夠確保在不斷擴展的網路中實現低損耗、高頻寬的性能。

- 為因應這一趨勢,電信業者、政府和企業部門正在加大對光纖基礎設施的投資。西歐的重點是用全光纖網路取代傳統銅線,並增強數位韌性。東歐和南歐則致力於擴大寬頻覆蓋範圍,以彌合農村地區的連接缺口。總體而言,歐洲光纖裝置市場正在不斷發展,以滿足高性能和包容性連接的需求,從而實現速度、可擴展性和永續性。

報告範圍和歐洲光纖組件市場細分

|

屬性 |

歐洲光纖組件市場關鍵洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

歐洲

|

|

主要市場參與者 |

|

|

市場機會 |

德國、法國、英國和北歐等國家大力投資5G基礎設施,對光纖裝置的需求也隨之激增。為了實現超低延遲和高速行動網絡,營運商正在部署密集的光纖回傳和前傳網絡,尤其是在城市地區和工業園區。

歐洲各行各業,包括汽車、航空航太、製藥和能源,正日益採用私有 5G 和光纖網路。這些網路增強了控制力、網路安全和即時資料流,尤其是在工廠和智慧園區等高精度環境中。

隨著歐洲各地邊緣資料中心的增多,以應對日益增長的物聯網工作負載,對快速、安全、低延遲的光纖鏈路的需求也日益增長。光纖組件在連接邊緣站點和雲端基礎設施以及確保無縫的機器間通訊方面發揮著至關重要的作用。

歐洲各城市正在投資智慧基礎設施,例如智慧桿、智慧交通系統和覆蓋全市的公共Wi-Fi。這些舉措依賴高容量光纖網路來處理來自互聯感測器、攝影機和控制系統的資料傳輸。

「連接歐洲基金」(CEF)和「數位歐洲計畫」等項目的公共資金正在加速光纖部署,尤其是在農村和服務欠缺地區。隨著各國致力於實現歐盟範圍內的千兆連接目標,這些措施為光纖組件供應商開闢了新的市場。 |

|

加值資料資訊集 |

|

歐洲光纖組件市場趨勢

“光纖是歐洲數位化未來的核心”

- 光纖正成為歐洲數位革命的靜默支柱。隨著家庭、企業和公共基礎設施對高速網路的需求激增,各國都在加倍投入建設全光纖網路。從德國雄心勃勃的千兆目標到法國農村光纖到戶 (FTTH) 的擴張,收發器、放大器和分路器等光纖組件都是每項部署的核心。這不僅是為了速度,更是為了建立可擴展、面向未來的基礎設施,以處理從 5G 回傳到超高清串流媒體和智慧城市平台等各種業務。

- 重塑市場的一個主要趨勢是光纖在支援邊緣運算和資料中心互連方面發揮著日益重要的作用。隨著法蘭克福、阿姆斯特丹和都柏林等歐洲科技中心的互聯互通日益緊密,對低延遲光纖鏈路的需求也急劇增長。光學組件已不再僅限於電信領域,如今它們已成為整個歐洲大陸雲端服務、人工智慧驅動的工作負載和企業級網路安全的關鍵支撐。光纖的可靠性和容量使其成為歐洲不斷擴張的數位經濟的首選媒體。

- 同時,永續性正成為一項至關重要的優先事項。歐洲網路營運商面臨降低能耗和碳排放的壓力。這推動了對更高效的光學元件、緊湊型設計和可回收佈線系統的需求。供應商正在透過創新來應對挑戰,這些創新不僅提升了效能,還符合歐盟綠色協議和環境、社會和治理 (ESG) 標準。在這個新時代,光纖不僅速度更快,而且比以往任何時候都更聰明、更環保、更不可或缺。

歐洲光纖組件市場動態

司機

“ 5G 加速部署,光纖優先策略興起”

- Europe is witnessing a rapid expansion of 5G networks, and with that comes an urgent demand for robust fiber infrastructure. As mobile operators race to offer high-speed, low-latency services, fiber-optic components are at the heart of enabling seamless backhaul and fronthaul connectivity.

- Countries like Germany, the U.K., and France are prioritizing fiber-first strategies—where optical fiber becomes the baseline for all broadband and mobile services. National programs such as the U.K.’s Project Gigabit and Germany’s Digital Infrastructure Plan are fueling this push with billions in public funding.

- This shift is creating massive opportunities for fiber component manufacturers and system integrators. Transceivers, optical amplifiers, connectors, and fiber cables are being deployed at scale to support not just telecom networks, but also smart cities, data centers, and edge computing hubs across the continent.

- As consumers and businesses demand more bandwidth—for streaming, cloud services, telemedicine, and AI workloads—fiber components are becoming essential to meet these expectations reliably and efficiently.

Restraint/Challenge

“High Deployment Costs and Uneven Rollout in Rural Regions”

Rolling out fiber infrastructure in Europe is capital-intensive, particularly in less densely populated rural and remote areas. While urban centers benefit from existing ductwork and infrastructure, rural deployments often require new trenching, which can drive costs significantly higher.

Operators and local authorities also face logistical challenges like terrain complexity, labor shortages, and long permitting processes. In countries like Poland, Romania, and parts of Southern Europe, bureaucratic red tape can delay project timelines by months.

Moreover, while EU funds are available, smaller municipalities and local ISPs often struggle with upfront financing or co-investment requirements. This limits the pace at which fiber can reach the “last mile” in underserved communities

Although government subsidies and public-private partnerships are helping bridge the gap, many regions still lag behind, creating a digital divide that component providers and policymakers alike are working hard to close

• By Infrastructure Type

Access Network (FTTH/FTTB): The largest deployment area across Europe, especially in France, Spain, and the U.K., where governments and telecoms are accelerating fiber-to-the-home/building coverage. Key components used include optical splitters, connectors, and termination boxes..

Metro Network: Supports connectivity between local exchanges and data aggregation points. Countries like Germany and the Netherlands are investing in metro fiber networks for enterprise and 5G support. Common components include optical amplifiers, WDM systems, and enclosures.

Core/Long-Haul Network: Used to connect major cities, countries, and internet exchanges. Deployed across pan-European routes, especially in central and northern Europe. High-capacity transceivers, DWDM modules, and optical switches dominate in this segment

Backhaul and Fronthaul (5G Mobile Transport): Growing significantly with 5G rollouts across the EU. Fiber is critical for connecting cell sites to core networks, particularly in urban areas. Fiber cables, ruggedized connectors, and mux/demux units are widely deployed.

Data Center Interconnect (DCI): With the expansion of hyperscale and colocation data centers in cities like Frankfurt, Paris, and Amsterdam, demand for high-density fiber links is rising. Optical transceivers, patch panels, and cable assemblies are key components in this space.

• By Component

Hardware leads the segment, driven by strong demand for optical cables, transceivers, amplifiers, and splitters. As FTTH and 5G rollouts intensify, hardware components form the foundation of Europe’s next-gen connectivity landscape.

Software adoption is picking up across the region as telecom operators increasingly deploy SDN (Software Defined Networking) and AI-driven network management. Countries like Germany and the Netherlands are pioneering the shift to intelligent fiber networks.

Services are essential for supporting deployment and maintenance. With multiple EU-backed programs in motion, service providers offering installation, project management, and post-deployment support are seeing high demand across Europe’s fiber expansion projects..

• By Network Technology

4G LTE remains significant in Eastern and parts of Southern Europe, where it still forms the primary connectivity layer. However, operators are steadily transitioning toward 5G-ready infrastructure.

5G is growing fastest, particularly in the U.K., France, and Nordic countries, where full-scale rollouts are underway. The fiber components market is benefiting directly from the high backhaul capacity required for 5G.

Wi-Fi 6/6E adoption is accelerating in enterprise, education, and healthcare sectors across Europe, particularly in Germany, the Netherlands, and Finland.

2G/3G networks are being phased out in much of Western Europe, though they remain active in parts of Central and Eastern Europe for legacy services.

Future Technologies (6G, LEO Satellites) are in early trial phases, with the EU investing in research to ensure Europe’s leadership in ultra-high-speed and low-orbit satellite connectivity by the next decade..

• By Ownership Type

Mobile Network Operators (MNOs) like Orange, Deutsche Telekom, and Vodafone are the primary owners of core optical infrastructure across Europe, especially for nationwide 5G backbones.

Tower Companies such as Cellnex and Vantage Towers are expanding fiber-linked passive infrastructure, enabling cost-efficient shared use by multiple telecom providers.

私人網路供應商正在汽車(德國)、製造業(義大利)和物流(比利時)等領域湧現,部署閉環光纖網路以實現更好的控制和安全性。

政府機構積極參與在服務欠缺地區部署光纖,特別是透過歐盟資助計劃和愛爾蘭、葡萄牙和希臘等國的農村寬頻計劃

按最終用戶

電信仍然是主要的終端用戶,營運商正在擴大基礎設施以滿足行動、寬頻和資料中心網路日益增長的頻寬需求。

歐洲各地的企業,尤其是金融、醫療保健和先進製造等領域的企業,正在整合高速光纖,以實現低延遲營運和私有 5G 用例。

政府和公共安全依靠光纖網路進行監控、緊急通訊和數位公共服務,尤其是在城市現代化計畫中。

運輸和物流行業正在鐵路、港口和公路網路上部署光纖連接,以實現即時追蹤、自動化系統和智慧基礎設施。

隨著光纖到府 (FTTH) 計畫在歐盟範圍內的擴展,住宅需求正在蓬勃發展。隨著遠距辦公、智慧家庭和線上學習的興起,光纖連接已成為歐洲家庭的必需品。

歐洲光纖元件市場-區域發展分析

- 西歐:

德國、法國和英國等國家在西歐光纖組件市場領先。這些國家受益於完善的電信基礎設施、高城市化率以及積極的5G部署計畫。對光收發器、分路器和WDM系統的需求正在快速成長,尤其是在城域網路和核心網路部署中。英國的「千兆計畫」和德國的「千兆戰略2025」等政府措施正在加速光纖到府(FTTH)的普及,從而推動對高性能光纖組件的需求。

- 南歐:

受FTTH強勁滲透率和歐盟數位基礎設施資金支持的推動,西班牙、義大利和葡萄牙的光纖部署正在穩步成長。尤其是西班牙,其FTTH覆蓋率位居歐洲前列,這推動了對連接器和外殼等被動光元件的持續投資。該地區還在投資資料中心基礎設施,這增加了對高速光模組和互連的需求。

- 北歐:

包括瑞典、芬蘭和丹麥在內的北歐國家在寬頻普及和光纖主導的連接方面處於領先地位。這些市場專注於可持續且節能的光纖基礎設施,並得到政府強有力的激勵措施和技術驅動的部署模式的支持。基於人工智慧的網路監控和SDN的採用也推動了對智慧光學組件的需求不斷增長。

- 東歐:

波蘭、羅馬尼亞和匈牙利等國家正透過加速農村寬頻計畫和公私合作迎頭趕上。儘管部分地區基礎設施仍欠發達,但歐盟支持的措施和國家光纖戰略正在提升網路覆蓋率和品質。這導致光纜、熔接套件和 ODF(光纖配線架)等基本光纖組件的使用率不斷提高,尤其是在接取網路和回程網路中。

- 中歐:

奧地利、捷克共和國和瑞士等市場呈現溫和成長態勢,城市和半城市地區持續部署光纖。這些國家專注於網路現代化和數位包容性,導致對光放大器和高密度配線架等組件的需求不斷增長。瑞士率先採用10G PON技術也影響先進組件的消費。

歐洲光纖組件市場洞察

歐洲光纖裝置市場正在快速擴張,這得益於 FTTH 的廣泛部署、5G 的加速部署以及各行各業數位轉型的蓬勃發展。德國、法國、英國和西班牙等主要經濟體正在大力投資光纖基礎設施,以滿足對高速、低延遲連接日益增長的需求。

電信業者和寬頻業者正在增加對主動和被動光元件(包括收發器、光纖、連接器、分路器和波分複用系統)的投資,以支援不斷擴展的存取網、城域網路和骨幹網路。德國的千兆戰略和英國的千兆項目等政府支持的舉措正在為城鄉光纖鋪設創造強勁勢頭。

此外,資料中心互連、雲端運算和智慧城市基礎設施的興起,正在推動企業和公共部門對高效能、可擴展光纖元件的需求。永續性也影響著採購決策,人們對節能耐用的光纖系統的興趣日益濃厚。

隨著老牌廠商和新進業者爭奪市場份額,競爭日益激烈。本地製造、成本優化和組件創新(例如更小尺寸的收發器和整合AI的監控系統)正成為關鍵的差異化因素。隨著歐洲邁向千兆社會,光纖組件市場有望實現強勁且持續的成長…

以下公司被公認為全球無線基礎設施市場的主要參與者:

- 康寧公司

- 普睿司曼集團(義大利)

- 耐克森公司(法國)

- 藤倉株式會社(透過歐洲子公司)

- Huber+Suhner AG(瑞士)

- 康普公司

- Adtran(德國/美國)

- Hexatronic Group AB(瑞典)

- 羅格朗(法國)

- Telefonica Tech / Open Fiber(透過合作)

歐洲光纖元件市場最新發展

- May 2025 – Corning Incorporated announced the expansion of its optical fiber manufacturing capacity in Poland to support rising demand for FTTH deployments across Central and Eastern Europe. The investment aims to strengthen local supply chains and reduce lead times for passive optical components..

- March 2025 – Prysmian Group unveiled its new high-density optical cable portfolio designed specifically for urban FTTH rollouts. These cables, featuring reduced diameter and enhanced flexibility, are being piloted in Italy and the Netherlands to accelerate city-wide fiber access..

- January 2025 – HUBER+SUHNER launched a range of eco-friendly fiber management systems made from recycled materials. The product line, introduced at a European telecom conference in Geneva, aligns with sustainability goals and green infrastructure trends..

- December 2024 – Adtran (formerly ADVA Optical Networking) completed the deployment of an open optical transport solution for a pan-European research network. The project spans multiple countries and aims to boost capacity and scalability for academic and scientific data exchanges.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。