Global Ameloblastic Carcinoma Market

市场规模(十亿美元)

CAGR :

%

USD

305.45 Million

USD

472.34 Million

2024

2032

USD

305.45 Million

USD

472.34 Million

2024

2032

| 2025 –2032 | |

| USD 305.45 Million | |

| USD 472.34 Million | |

| % | |

|

全球成釉細胞癌市場細分,按治療(藥物、放射療法、手術等)、診斷(電腦斷層掃描 (CT) 掃描、磁振造影 (MRI) 等)、給藥途徑(口服、注射等)、最終用戶(醫院、家庭護理、專科診所等)、分銷渠道(醫院藥房、網上藥房、零售藥房等)劃分 - 行業趨勢和預測行業 203 年)

成釉細胞癌市場規模

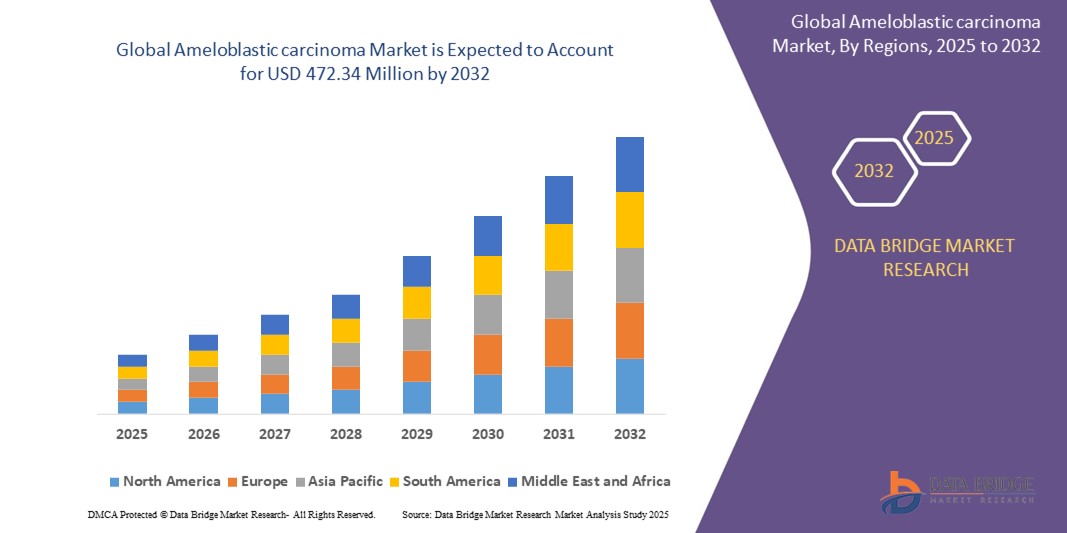

- 2024 年全球成釉細胞癌市場規模為3.0545 億美元 ,預計 到 2032 年將達到 4.7234 億美元,預測期內 複合年增長率為 5.60%。

- 市場成長主要得益於成釉細胞癌盛行率的不斷上升以及診斷和治療技術的進步,從而改善了已開發地區和發展中地區對該疾病的檢測和管理。

- 此外,醫療保健專業人員和患者對有效治療方案的認識不斷提高,以及對腫瘤學研究的投入不斷增加,使得新療法和手術技術成為治療成釉細胞癌的首選方法。這些因素共同加速了先進處理方案的採用,從而顯著促進了產業成長。

成釉細胞癌市場分析

- 牙釉質細胞癌是一種罕見的惡性牙源性腫瘤,由於其侵襲性和在發達和發展中醫療環境中的複雜治療要求,在診斷成像和外科技術的進步的推動下,它正成為口腔腫瘤學中越來越重要的關注焦點。

- 對改善成釉細胞癌管理的需求不斷增加,主要是由於牙源性腫瘤發病率的上升、醫療保健專業人員意識的增強以及患者對更有效、侵入性更小的治療方案的偏好日益增長。

- 北美在成釉細胞癌市場佔據主導地位,2025 年其收入份額最大,為 40.01%,其特點是醫療基礎設施先進、醫療支出高、領先的研究機構和製藥公司眾多,而美國的診斷和治療方案大幅增長,得益於外科手術和標靶治療的創新。

- 由於醫療保健投資的增加、對口腔癌的認識的提高以及先進醫療技術的普及,預計亞太地區將成為預測期內成釉細胞癌市場成長最快的地區。

- Surgical resection segment is expected to dominate the ameloblastic carcinoma market with a market share of 43.2% in 2025, driven by its established efficacy as the primary treatment modality and widespread adoption by oral and maxillofacial surgeons.

Report Scope and Ameloblastic carcinoma Market Segmentation

|

Attributes |

Ameloblastic carcinoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Advancements in Diagnostic Technologies and Treatment Modalities |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ameloblastic carcinoma Market Trends

“Advancements in Diagnostic and Treatment Technologies”

- A significant and accelerating trend in the global ameloblastic carcinoma market is the integration of advanced diagnostic technologies such as molecular profiling, next-generation sequencing, and AI-assisted imaging analysis. This fusion of technologies is significantly improving early detection, accurate diagnosis, and personalized treatment planning.

- For instance, advanced imaging techniques like PET-CT scans and AI-based histopathological analysis enable clinicians to better distinguish ameloblastic carcinoma from benign odontogenic tumors, facilitating more effective surgical and therapeutic decisions. Similarly, targeted therapies developed using molecular insights are providing new treatment options with improved outcomes.

- AI integration in diagnostics enables features such as analyzing complex datasets to identify tumor markers and predict treatment response, while AI-powered imaging tools enhance detection accuracy. For example, some emerging platforms use AI algorithms to analyze biopsy slides and identify malignant features with high precision. Furthermore, personalized medicine approaches based on genetic profiling allow oncologists to tailor therapies specific to patient tumor characteristics.

- The seamless integration of diagnostics with treatment platforms facilitates a comprehensive approach to patient management. Through coordinated care, clinicians can monitor tumor progression, adjust treatment regimens, and improve prognostic outcomes in real time.

- This trend towards more precise, personalized, and integrated diagnostic and therapeutic systems is fundamentally reshaping patient care standards. Consequently, companies such as Xcess Biosciences and Eli Lilly are advancing AI-enabled diagnostic tools and targeted therapies for ameloblastic carcinoma.

- The demand for innovative diagnostic and treatment solutions that leverage AI and molecular technologies is growing rapidly across both developed and emerging markets, as healthcare providers and patients increasingly prioritize effective and personalized cancer care.

Ameloblastic carcinoma Market Dynamics

Driver

“Growing Need Due to Rising Incidence and Advancements in Treatment Technologies”

- The increasing prevalence of ameloblastic carcinoma worldwide, coupled with advancements in diagnostic and therapeutic technologies, is a significant driver for the heightened demand for effective treatment solutions.

- For instance, in early 2025, Xcess Biosciences announced progress in molecular-targeted therapies for rare odontogenic tumors, aiming to improve patient outcomes through precision medicine. Such innovations by key companies are expected to drive the ameloblastic carcinoma market growth in the forecast period.

- As awareness among healthcare providers and patients about the aggressive nature of ameloblastic carcinoma grows, demand for advanced treatments such as surgical resection combined with adjunct therapies is increasing, providing a compelling upgrade over traditional methods.

- Furthermore, the rising emphasis on early diagnosis through imaging and biopsy techniques is making comprehensive treatment planning more effective, offering improved prognosis and survival rates.

- The integration of personalized medicine approaches, including genetic profiling and targeted therapies, and the increasing availability of specialized oncology centers are key factors propelling the adoption of advanced treatment solutions in both developed and emerging markets. The trend towards multidisciplinary care and expanding healthcare infrastructure further contributes to market growth.

Restraint/Challenge

“Concerns Regarding High Treatment Costs and Limited Awareness”

- Concerns surrounding the high cost of treatment procedures for ameloblastic carcinoma pose a significant challenge to broader market penetration. As treatments often involve complex surgeries and adjunct therapies, they can be expensive and inaccessible to many patients, especially in developing regions.

- For instance, limited insurance coverage and reimbursement policies in several countries make it difficult for patients to afford the full course of treatment, leading to hesitation in seeking timely care.

- Addressing these financial concerns through improved healthcare policies, increased insurance support, and patient assistance programs is crucial for improving treatment accessibility. Companies such as Eli Lilly and Pfizer emphasize patient support initiatives and cost-effective therapy development in their strategies to make treatments more affordable. Additionally, the lack of widespread awareness about ameloblastic carcinoma among the general population and even some healthcare providers can delay diagnosis and treatment initiation.

- While treatment costs are gradually being optimized, the perception of expensive and complex care can still hinder early diagnosis and management, especially in resource-limited settings.

- Overcoming these challenges through enhanced patient education, healthcare infrastructure improvements, and the development of affordable and effective treatment options will be vital for sustained market growth.

Ameloblastic carcinoma Market Scope

The market is segmented on the basis of treatment, diagnosis, route of administration, end-users, and distribution channel

By Treatment

On the basis of treatment, the ameloblastic carcinoma market is segmented into medication, radiation therapy, surgery, and others. The surgery segment dominates the largest market revenue share of 43.2% in 2025, driven by its established efficacy as the primary treatment approach for managing malignant odontogenic tumors. Healthcare providers often prioritize surgical resection due to its ability to achieve clear margins and reduce recurrence risk. The market also sees strong demand for surgery due to advancements in maxillofacial surgical techniques and the increasing availability of skilled professionals across major healthcare centers.

The medication segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, fueled by increasing research in targeted therapies and chemotherapeutic options. Medications offer non-invasive or adjunctive solutions, making them suitable for patients ineligible for surgery or those requiring postoperative treatment. The development of precision oncology drugs and supportive therapies also contributes to the growing popularity of pharmacological interventions in the management of ameloblastic carcinoma.

By Diagnosis

On the basis of diagnosis, the ameloblastic carcinoma market is segmented into computerized tomography (CT) scanning, magnetic resonance imaging (MRI), and others. The CT scanning segment dominates the largest market revenue share of 48.5% in 2025, driven by its widespread availability, rapid imaging capability, and effectiveness in assessing bone involvement in mandibular and maxillary lesions. Clinicians often rely on CT scans for initial evaluation due to their ability to provide detailed cross-sectional images that guide surgical planning. The market also sees strong demand for CT scanning due to its cost-efficiency and its role in monitoring recurrence post-treatment.

The MRI segment is anticipated to witness the fastest growth rate of 19.6% from 2025 to 2032, fueled by its superior soft-tissue contrast resolution and non-ionizing radiation benefits. MRI is increasingly adopted in advanced diagnostic centers for differentiating ameloblastic carcinoma from other soft tissue or odontogenic lesions. The precision of MRI in identifying neural or soft tissue invasion and its role in comprehensive tumor mapping contribute to its growing preference among oncologists and oral surgeons.

By Route of Administration

On the basis of route of administration, the ameloblastic carcinoma market is segmented into oral, injectable, and others. The injectable segment dominates the largest market revenue share of 55.3% in 2025, driven by its effectiveness in delivering chemotherapeutic and targeted agents directly into the bloodstream for faster systemic action. Oncologists often prefer injectable administration for its precision in dosing and suitability for hospital-based treatment settings. The market also sees strong demand for injectable options due to the development of biologics and the increasing availability of intravenous cancer therapies across oncology centers.

The oral segment is anticipated to witness the fastest growth rate of 22.1% from 2025 to 2032, fueled by growing patient preference for non-invasive treatment options and the increasing approval of oral anticancer medications. Oral therapies offer the convenience of at-home administration, making them ideal for long-term management or maintenance therapy. Additionally, advancements in drug formulations that enhance bioavailability and reduce side effects are contributing to the rising adoption of oral treatments in ameloblastic carcinoma care plans.

By End User

On the basis of end-users, the ameloblastic carcinoma market is segmented into hospitals, homecare, specialty clinics, and others. The hospital segment dominates the largest market revenue share of 61.8% in 2025, driven by the concentration of advanced diagnostic tools, surgical infrastructure, and multidisciplinary care teams required for treating complex oral malignancies. Hospitals remain the primary setting for both diagnosis and comprehensive treatment, including surgery, radiation therapy, and inpatient medication. The market also sees strong demand for hospital-based care due to the availability of experienced oral and maxillofacial surgeons and oncology specialists.

The specialty clinics segment is anticipated to witness the fastest growth rate of 20.4% from 2025 to 2032, fueled by the increasing number of oncology-focused clinics and dental care centers offering advanced diagnostic and surgical services. Specialty clinics provide targeted expertise and shorter wait times, making them a preferred option for patients seeking specialized treatment. Additionally, the expansion of private healthcare infrastructure and investments in outpatient surgical capabilities contribute to the rising popularity of specialty clinics in managing ameloblastic carcinoma.

Ameloblastic carcinoma Market Regional Analysis

- North America dominates the ameloblastic carcinoma market with the largest revenue share of 40.01% in 2024, driven by a growing demand for advanced cancer diagnostics and treatment, as well as increased awareness of rare oral malignancies.

- Patients and healthcare providers in the region highly value the precision, accessibility, and multidisciplinary approach offered by integrated cancer care systems, including the use of advanced imaging, surgical interventions, and emerging targeted therapies.

- This widespread adoption is further supported by high healthcare expenditure, a well-established medical infrastructure, and the growing emphasis on early detection and personalized treatment, establishing North America as a leading region for both clinical research and patient care in ameloblastic carcinoma.

U.S. Ameloblastic carcinoma Market Insight

The U.S. ameloblastic carcinoma market captured the largest revenue share of 81% within North America in 2025, fueled by the swift uptake of advanced diagnostic technologies and the expanding trend of personalized oncology care. Healthcare providers are increasingly prioritizing the early detection and comprehensive treatment of rare oral cancers through multidisciplinary approaches. The growing preference for minimally invasive surgical techniques, combined with robust demand for targeted therapies and AI-assisted diagnostic tools, further propels the ameloblastic carcinoma treatment landscape. Moreover, the increasing integration of precision medicine strategies, such as molecular profiling and genomics, is significantly contributing to the market's expansion.

Europe Ameloblastic carcinoma Market Insight

The European ameloblastic carcinoma market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations and the escalating need for early diagnosis and advanced treatment options. The increase in urbanization, coupled with growing awareness of rare oral cancers, is fostering the adoption of innovative diagnostic and therapeutic technologies. European healthcare providers and patients are also drawn to the improved outcomes and personalized care these advancements offer. The region is experiencing significant growth across hospital, specialty clinic, and outpatient settings, with ameloblastic carcinoma treatments being incorporated into both newly established oncology centers and upgraded healthcare facilities.

U.K. Ameloblastic carcinoma Market Insight

The U.K. ameloblastic carcinoma market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating emphasis on early diagnosis and the adoption of advanced treatment protocols. Additionally, increasing awareness about oral cancers and the availability of specialized oncology centers are encouraging both patients and healthcare providers to seek timely and effective care. The U.K.’s robust healthcare infrastructure, alongside its focus on research and clinical trials, is expected to continue to stimulate market growth.

Germany Ameloblastic carcinoma Market Insight

The German ameloblastic carcinoma market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of early cancer detection and the demand for technologically advanced, patient-centric treatment solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on medical innovation and research, promotes the adoption of advanced diagnostic tools and personalized therapies, particularly in specialized oncology centers. The integration of multidisciplinary treatment approaches is also becoming increasingly prevalent, with a strong preference for comprehensive care models aligning with local healthcare standards and patient expectations.

Asia-Pacific Ameloblastic carcinoma Market Insight

Asia-Pacific ameloblastic carcinoma market is poised to grow at the fastest CAGR of over 24% in 2025, driven by increasing urbanization, rising healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards advanced cancer diagnostics and treatment, supported by government initiatives promoting healthcare infrastructure development, is driving the adoption of innovative therapeutic solutions. Furthermore, as APAC emerges as a hub for medical research and pharmaceutical manufacturing, the affordability and accessibility of ameloblastic carcinoma treatments are expanding to a wider patient base.

Japan Ameloblastic carcinoma Market Insight

The Japan ameloblastic carcinoma market is gaining momentum due to the country’s advanced healthcare infrastructure, rapid urbanization, and increasing demand for convenient and effective cancer treatments. The Japanese market places significant emphasis on early diagnosis and personalized care, and the adoption of advanced diagnostic tools and targeted therapies is driven by the rising number of cancer cases and growing awareness. Moreover, Japan’s aging population is likely to spur demand for easier-to-administer and more secure treatment options in both residential and clinical settings.

China Ameloblastic carcinoma Market Insight

The China ameloblastic carcinoma market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's expanding healthcare infrastructure, rapid urbanization, and high rates of technological adoption. China stands as one of the largest markets for advanced cancer diagnostics and treatments, and ameloblastic carcinoma therapies are becoming increasingly accessible in hospitals, specialty clinics, and research centers. The government’s focus on healthcare modernization and the availability of cost-effective treatment options, alongside strong domestic pharmaceutical and biotech manufacturers, are key factors propelling the market in China.

Ameloblastic carcinoma Market Share

The Ameloblastic carcinoma industry is primarily led by well-established companies, including:

• Midwest Dental (U.S.)

• Burkhart Dental Supply (U.S.)

• Patterson Dental Supply, Inc. (U.S.)

• DeCare Dental (U.S.)

• Oratec Corp (U.S.)

• Amerident Dental (U.S.)

• AstraZeneca (U.K.)

• Eli Lilly and Company (U.S.)

• F. Hoffmann-La Roche Ltd (Switzerland)

• Pfizer Inc. (U.S.)

• Nichi-Iko Pharmaceutical Co., Ltd. (Japan)

• LC Laboratories (U.S.)

• CELGENE CORPORATION (U.S.)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Pierre Fabre Group (France)

• Santa Cruz Biotechnology, Inc. (U.S.)

• ApexBio Technology (U.S.)

• Tocris Bioscience (U.K.)

• Sun Pharmaceutical Industries Ltd. (India)

• Bristol-Myers Squibb (U.S.)

• Johnson & Johnson (U.S.)

• Merck & Co., Inc. (U.S.)

Latest Developments in Global Ameloblastic carcinoma Market

- In March 2024, Eli Lilly and Company announced the successful completion of a Phase II clinical trial for a novel targeted therapy aimed at improving survival rates in patients with ameloblastic carcinoma. The therapy showed promising tumor reduction with minimal side effects, highlighting a breakthrough in treatment options.

- In January 2024, Pfizer Inc. disclosed positive interim results from their ongoing study evaluating the efficacy of a BRAF inhibitor in ameloblastic carcinoma patients harboring the BRAF V600E mutation. Early data indicated significant tumor shrinkage and manageable safety profiles.

- In November 2023, AstraZeneca initiated a multi-center Phase I/II clinical trial exploring a new immunotherapy agent targeting PD-1/PD-L1 pathways in ameloblastic carcinoma. This trial aims to enhance the immune response and improve patient outcomes in advanced-stage cases.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。