Global Electric Vehicles Adhesives Market

市场规模(十亿美元)

CAGR :

%

USD

4.60 Billion

USD

11.55 Billion

2024

2032

USD

4.60 Billion

USD

11.55 Billion

2024

2032

| 2025 –2032 | |

| USD 4.60 Billion | |

| USD 11.55 Billion | |

| % | |

|

全球電動汽車黏合劑市場細分,按形式(液體、薄膜和膠帶、其他)、樹脂(聚氨酯、環氧樹脂、矽膠、丙烯酸等)、應用(動力傳動系統、外部和內部)、車輛類型(電動汽車、電動公車、電動卡車和電動自行車)、基材(聚合物、複合材料和金屬)- 產業趨勢和預測到 2032 年行業趨勢

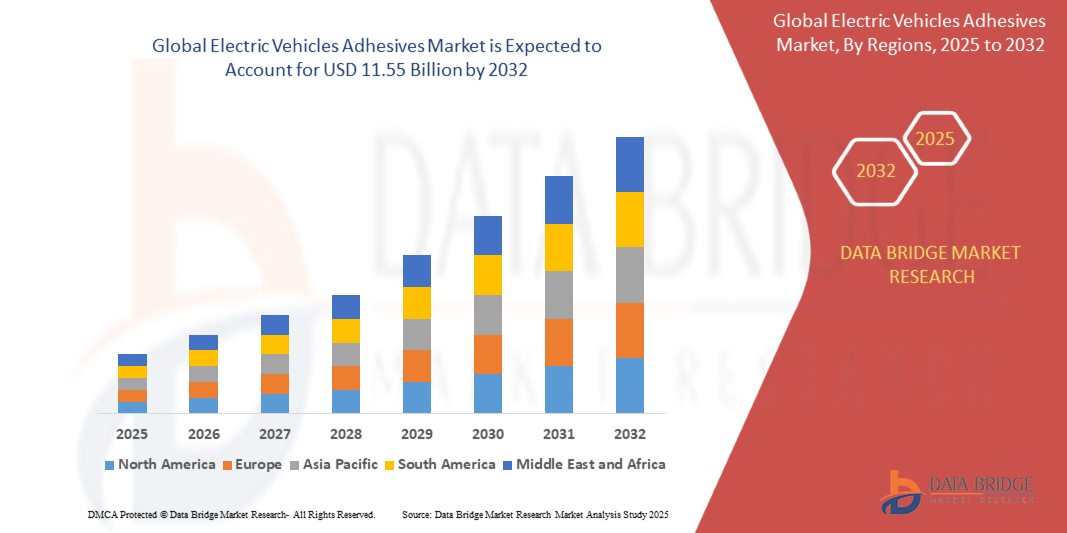

電動汽車黏合劑市場規模

- 2024 年全球電動車黏合劑市場規模為46 億美元 ,預計 到 2032 年將達到 115.5 億美元,預測期內 複合年增長率為 12.20%。

- 市場成長主要得益於電動車(EV)產量和銷量的成長、對輕量化和高性能黏合劑解決方案的需求不斷增長,以及促進減排和汽車效率的嚴格監管政策

電動汽車黏合劑市場分析

- 人們對電動車的日益關注極大地影響了對先進黏合劑技術的需求,這些技術可增強結構完整性、熱管理和電池安全性

- 黏合劑正在取代傳統的機械緊固件,以減輕車輛重量並提高能源效率

- 受電動車普及率上升、對輕量化汽車結構的高度關注以及電池技術進步的推動,北美在電動汽車黏合劑市場佔據主導地位,2024 年其收入份額最高,為 38.6%。

- 預計亞太地區將見證全球電動車黏合劑市場的最高成長率,這得益於電動車產量的成長、政府對電動車普及的激勵措施,以及中國、日本和韓國等國家對電池和汽車製造基礎設施的投資增加

- 液體黏合劑憑藉其卓越的貼合複雜幾何形狀和確保牢固結構黏合的能力,在2024年佔據了市場主導地位,佔據了最大的市場收入份額。液體黏合劑因其易於使用和高強度的特性,在電池模組、車身面板和內飾組裝中廣受歡迎。其優異的導熱性和減震性能也使其適用於提升電動車的安全性和性能。

報告範圍和電動汽車黏合劑市場細分

|

屬性 |

電動汽車黏合劑關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括進出口分析、生產能力概覽、生產消費分析、價格趨勢分析、氣候變遷情景、供應鏈分析、價值鏈分析、原材料/消耗品概覽、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

電動汽車黏合劑市場趨勢

“熱界面黏合劑在電池性能和安全性方面的應用日益廣泛”

- 熱界面黏合劑在電動車 (EV) 電池系統中變得至關重要,以確保在高負載條件下實現最佳導熱性和穩定的工作溫度

- 這些黏合劑透過在電池單元和冷卻板之間提供更一致的介面來取代傳統的導熱墊和間隙填充物,從而提高耐用性和性能

- 它們在長距離電動車使用的高能量密度電池組中的作用尤其重要,因為管理多餘的熱量對於防止電池性能下降和熱失控至關重要

- 汽車製造商也開始使用這些黏合劑來減少對機械緊固件的依賴,因為機械緊固件會增加車輛重量,並使狹小空間內的設計變得複雜

- 隨著電動車向 800V 架構和超快速充電功能過渡,電池組件的熱負荷增加,推動了這些高性能黏合劑的採用

- For instance, Tesla’s Model Y integrates thermally conductive adhesives in its battery module design to facilitate efficient heat dissipation, reduce component stress, and optimize battery lifespan

Electric Vehicles Adhesives Market Dynamics

Driver

“Surge in EV Production Driving Adhesive Integration in Lightweight Components”

- The surge in global EV production has intensified the need for advanced bonding solutions that reduce vehicle weight and improve structural integrity

- Adhesives are increasingly being used as alternatives to mechanical joints and welds, especially in battery enclosures, body-in-white, and structural frames

- Lightweight bonding directly contributes to extended driving range, improved fuel economy, and enhanced passenger safety, all of which are key selling points in the EV market

- In addition, adhesives provide uniform stress distribution, corrosion resistance, and enable design flexibility for joining dissimilar substrates such as magnesium, composites, and plastics

- OEMs benefit from reduced assembly time and fewer fastener points, streamlining production lines and supporting modular EV architecture designs

- For instance, BYD has adopted high-strength structural adhesives across its battery systems and chassis components to reduce overall vehicle mass and maximize energy efficiency, enabling better vehicle performance at lower cost

Restraint/Challenge

“Stringent Regulatory Approvals and Long Validation Cycles”

- One of the primary challenges in the EV adhesives market is the need for extensive testing and certification to meet stringent automotive safety and regulatory standards

- Adhesives used in critical EV components, particularly battery modules, must demonstrate resistance to flame, chemical exposure, vibration, and prolonged thermal cycling

- Regulatory delays often prolong time-to-market for new adhesive formulations, restricting innovation, especially for startups and mid-tier players with limited R&D budgets

- Compliance protocols vary across regions, with automakers requiring independent validation from global safety organizations such as UL, ISO, and SAE, adding layers of complexity

- The high cost and technical expertise needed for qualification procedures can deter market entry for smaller players and delay product scaling

- For instance, the thermal adhesive deployed in General Motors' Ultium battery system underwent over two years of validation testing to meet stringent UL 94V-0 flame resistance and thermal performance requirements, significantly slowing down implementation despite its potential

Electric Vehicles Adhesives Market Scope

The market is segmented on the basis of form, resin, application, vehicle type, and substrate.

• By Form

On the basis of form, the electric vehicles adhesives market is segmented into liquid, film and tape, and others. The liquid segment dominated the market with the largest market revenue share in 2024, attributed to its superior ability to conform to complex geometries and ensure strong structural bonds. Liquid adhesives are widely preferred in battery modules, body panels, and interior assembly due to their ease of application and high strength. Their excellent thermal conductivity and vibration-damping capabilities also make them suitable for enhancing EV safety and performance.

The film and tape segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the demand for clean, efficient, and automated bonding processes. Film adhesives offer consistent thickness, minimal waste, and faster curing times, making them ideal for mass production in automotive manufacturing lines. They are particularly gaining traction in applications such as battery cell-to-pack bonding and EV electronics assembly.

• By Resin

On the basis of resin, the electric vehicles adhesives market is segmented into polyurethane, epoxy, silicone, acrylic, and others. The polyurethane segment accounted for the largest market share in 2024 owing to its excellent flexibility, bonding strength, and durability. These adhesives are commonly used in bonding glass, composite, and metal surfaces across EV body parts and interiors.

The silicone segment is expected to witness the fastest growth rate from 2025 to 2032, due to its superior thermal stability and resistance to harsh environmental conditions. Silicone-based adhesives are increasingly favored in battery packs and power electronics, offering reliable performance under wide temperature ranges, which is essential in electric mobility systems.

• By Application

On the basis of application, the electric vehicles adhesives market is segmented into powertrain system, exterior, and interior. The powertrain system segment held the largest revenue share in 2024, as adhesives are critical in assembling and thermally managing EV batteries and electric motors. Their role in ensuring strong bonds and managing thermal expansion is essential for the durability and efficiency of EV powertrains.

The exterior segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the adoption of lightweight body materials and the shift toward seamless, aerodynamic designs. Adhesives in exteriors replace traditional mechanical fasteners, improving aesthetics while reducing noise and vibration.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into electric car, electric bus, electric truck, and electric bike. The electric car segment led the market in 2024 with the largest revenue share due to the rising global sales of passenger EVs and increasing investments by automakers in electric mobility.

預計電動卡車領域將在 2025 年至 2032 年間見證最快的成長率,這得益於電子商務物流的興起、嚴格的排放標準以及大型電池組和重型結構對高性能黏合劑解決方案的需求不斷增加。

• 按基材

根據基材,市場細分為聚合物、複合材料和金屬。金屬材料因其在電動車底盤、電池外殼和動力總成部件的廣泛應用,在2024年佔據了最大的市場收入份額。黏合劑在黏合金屬表面時具有耐腐蝕性、應力分佈和耐用性。

受汽車產業輕量化材料推動,複合材料領域預計在2025年至2032年期間實現最快成長。黏合劑能夠實現複合材料零件的牢固、靈活的黏合,從而支持更輕量化、更節能的電動車的發展。

電動汽車黏合劑市場區域分析

- 受電動車普及率上升、對輕量化汽車結構的高度關注以及電池技術進步的推動,北美在電動汽車黏合劑市場佔據主導地位,2024 年其收入份額最高,為 38.6%。

- 該地區的特點是擁有完善的電動車基礎設施、對永續交通的投資不斷增加,以及政府為電動車提供稅收優惠的舉措

- 美國和加拿大的主要汽車製造商正在積極整合高性能黏合劑,以取代傳統的焊接和機械緊固件,從而優化電動車的續航里程和結構完整性

美國電動汽車黏合劑市場洞察

由於採用電動車產能的擴張和強大的汽車研發現狀系統,美國電動汽車黏合劑市場在2024年佔據了北美80%以上的市場份額。特斯拉和通用汽車等製造商正在電池組中廣泛使用黏合劑來減輕重量並實現熱管理。政府對電動車創新的資助,以及車隊和商業運輸日益向電氣化轉型,持續推動對先進黏合解決方案的需求。

歐洲電動汽車黏合劑市場洞察

受嚴格的排放法規和雄心勃勃的碳中和目標的推動,歐洲電動汽車膠粘劑市場預計將在預測期內實現顯著的複合年增長率。德國、法國和荷蘭等國的電動車註冊量正在不斷增長,這促使汽車製造商探索用於降低噪音、提高碰撞性能和電池安全性的膠合劑解決方案。在該地區競爭激烈且注重環保的市場中,電動車組裝中的輕量化黏合正變得越來越普遍。

英國電動汽車黏合劑市場洞察

受政府支持的電動車普及計畫和不斷提升的電池製造能力的推動,英國電動汽車黏合劑市場預計將穩定成長。英國積極的碳排放目標以及2035年內燃機汽車銷售禁令,促使汽車製造商採用高效能黏合劑來支持電動車的大規模生產。無論是本地新創公司還是全球汽車製造商,都在利用黏合劑來提升各類車輛的結構性能和耐腐蝕性能。

德國電動汽車黏合劑市場洞察

德國電動汽車膠黏劑市場蓬勃發展,得益於其全球汽車創新中心的地位。領先的電動車製造商的入駐,加上對電池超級工廠和輕量化建築材料的投資,正在加速膠合劑的整合。先進的膠合劑正被用於下一代電動車的模組封裝、碰撞保護和密封性能提升,這有力地支持了德國對低碳交通解決方案的承諾。

亞太地區電動汽車黏合劑市場洞察

由於快速城鎮化、政府激勵措施以及中國、日本和韓國電動車產量的不斷擴大,亞太地區在2025年至2032年間的複合年增長率預計將達到13.7%,位居全球最快。該地區擁有經濟高效的製造和供應鏈,以及精通技術的消費者群體。黏合劑在電動車大批量生產中被廣泛採用,以確保電池的效率、安全性和輕量化。

日本電動汽車黏合劑市場洞察

日本專注於混合動力和純電動車的發展,其電動車黏合劑市場正在穩步發展。國內汽車製造商正在將黏合劑整合到電池外殼、熱界面和耐碰撞結構中,以滿足性能和安全標準。日本人口老化和城市密度的上升也增加了對採用輕量化黏合解決方案的高效緊湊型電動車的需求。

中國電動汽車膠黏劑市場洞察

2024年,中國佔據亞太地區最大的電動車收入份額,這得益於其在全球電動車生產和電池製造領域的主導地位。政府對電動車的嚴格監管,加上電動車消費者群體的不斷增長,推動了結構膠和熱熔膠的廣泛應用。比亞迪和蔚來等本土電動車巨頭正在利用創新的膠合劑技術來提升車輛的耐用性、乘客安全性和電池性能。

電動汽車黏合劑市場份額

電動汽車黏合劑產業主要由知名公司主導,包括:

- 杜邦(美國)

- 索爾維(比利時)

- 陶氏(美國)

- 漢高股份公司(德國)

- 3M(美國)

- 波斯膠(法國)

- 西卡股份公司(瑞士)

- HB Fuller(美國)

- 巴斯夫公司(德國)

- DAP Global Inc.(美國)

- 歐文斯科寧(美國)

- 科慕公司(美國)

- 帕羅克集團(芬蘭)

- Kingspan集團(愛爾蘭)

- DAIKIN (Japan)

- GAF (U.S.)

- Saint-Gobain S.A. (France)

- Franklin International (U.S.)

- Illinois Tool Works Inc. (U.S.)

- AVERY DENNISON CORPORATION (U.S.)

- ThreeBond Holdings Co., Ltd. (Japan)

- Dymax (U.S.)

- Ashland (U.S.)

- Shell plc (U.K.)

Latest Developments in Global Electric Vehicles Adhesives Market

- In January 2022, H.B. Fuller Company announced that it completed the acquisition of Apollo, the largest independent manufacturer of liquid adhesives,coatings and primers for the roofing, industrial and construction markets in U.K.

- In September 2022, Henkel AG & Co.KGaA has completed the acquisition of Nanoramic Laboratories Thermal Management Management Materials business.Henkel used this acquisition to strengthen its Adhesive Technologies business unit’s position in the growing markets for Thermal Interface Materials (TIM) by expanding its capabilities in high-performance segments

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。