Global Flexible Display Market

市场规模(十亿美元)

CAGR :

%

USD

45.30 Billion

USD

252.30 Billion

2024

2032

USD

45.30 Billion

USD

252.30 Billion

2024

2032

| 2025 –2032 | |

| USD 45.30 Billion | |

| USD 252.30 Billion | |

| % | |

|

全球弹性显示市场,按类型(OLED、LCD、LED、EPD)、底板材料(玻璃、可塑、其他底板材料)、应用(智能手机和平板、智能可衣、电视和数字信号系统、个人计算机和笔记本电脑、监视器、车辆和公共交通、智能家用电器)、表单因子(显示器、可弯和可折叠显示器、可滚动显示器)、面板尺寸(上至6个、50个以上)、20-50个、6-20个)。 2032年工业趋势和预测

Flexible Display Market Size

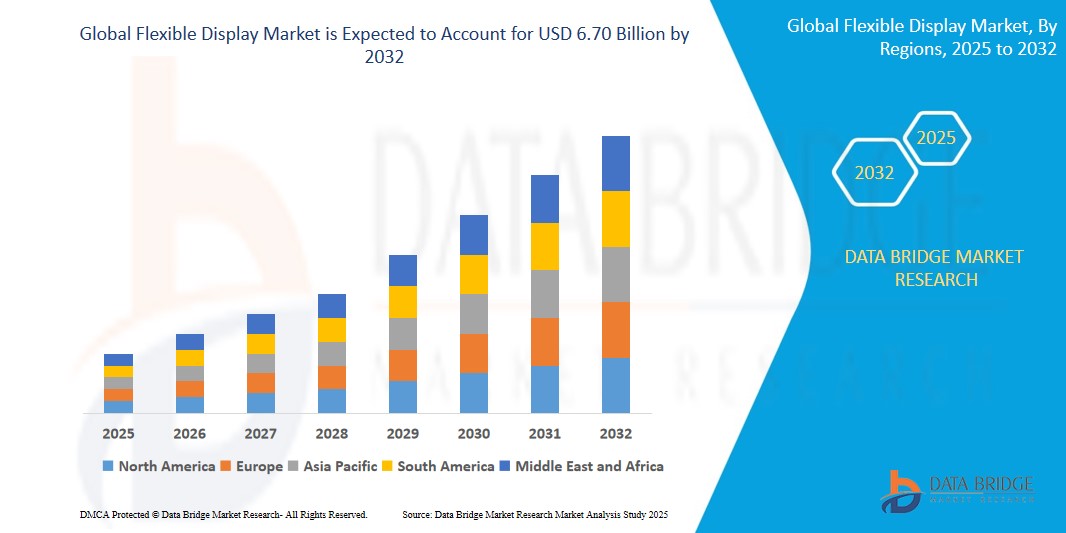

- The global Flexible Display market size was valued atUSD 4.12 billion in 2024 and is expected to reachUSD 6.70 billion by 2032, at aCAGR of 6.4%during the forecast period

- This growth is driven by factors such as rising consumer demand for lightweight, foldable, and portable electronic devices, advancements in OLED, AMOLED, and micro-LED technologies, and the increased adoption of flexible displays in smartphones, automotive infotainment systems, smart home interfaces, and wearable healthcare devices.

Flexible Display Market Analysis

- Flexible displays are flexible in nature, in comparison to the traditional displays that are utilized in most of the electronic devices. These displays are substituting for flat pieces of glass or plastics in the computer monitors, televisions, and mobile phones. They are sturdy in nature in comparison to the traditional displays.

- Major factors that are expected to boost the growth of the flexible display market in the forecast period are the development in the electronic technology and the growing demands of the products. The increase in the demand for connected and automated vehicles which required a display for documentary and navigation services and the increasing acceptance of digital signage system with the initiation of the smart city concept are further anticipated to further propel the growth of the flexible display market.

- Asia Pacific is expected to dominate the Flexible Display market due to the growing demand for compact and light-weight electronic devices. Furthermore, the rise of the smartphones and the growing acceptance of the advanced technologies will further boost the flexible display market in the region during the forecast period.

- North America is expected to be the fastest growing region in the Flexible Display market during the forecast period due to the increase in the demand for energy-effective devices. Moreover, the substantial demand for adaptable displays is further anticipated to further propel the growth of the flexible display market in the region in the coming years.

- The OLED segment is expected to dominate the Flexible Display market, with a market share of 37.23% during the forecast period. This leadership is attributed to the soaring demand for lightweight, foldable, and energy-efficient display devices, increasing adoption in smartphones, wearables, and televisions, and continuous technological advancements in display quality and durability

Report Scope and Flexible Display Market Segmentation

|

Attributes |

Flexible DisplayKey Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Flexible Display Market Trends

“Integration of Foldable, Rollable, and Stretchable Display Technologies”

- Flexible display technologies are rapidly evolving beyond foldable smartphones, now incorporating rollable and stretchable screen designs that enhance device portability, user interactivity, and visual appeal across consumer electronics and automotive dashboards.

- Advancements in OLED materials, thin-film encapsulation, and substrate engineering are enabling manufacturers to create ultra-thin, lightweight, and durable displays with high brightness and superior flexibility..

- For instance, in March 2025, LG Display unveiled its next-generation 20-inch stretchable display prototype, capable of being extended by 20% without distortion. This innovation is expected to fuel applications in wearables, healthcare devices, and smart mobility interfaces.

- The trend is driven by increasing consumer demand for futuristic device form factors, space-saving solutions, and immersive user experiences in smartphones, tablets, automotive infotainment systems, and smart home devices

Flexible Display Market Dynamics

Driver

“Rising Demand for Foldable and Lightweight Smart Devices”

- Consumers are increasingly drawn to sleek, foldable, and ultra-light devices that offer enhanced portability without compromising display quality or functionality—especially in smartphones, tablets, and wearables.

- Major tech brands are rapidly investing in foldable OLEDs and plastic substrate displays to cater to the modern consumer's desire for futuristic design, flexibility, and compactness.

- Enhanced durability, drop resistance, and energy efficiency in foldable devices are accelerating their adoption across premium electronics.

- For instance, In February 2025, Samsung announced record sales of its Galaxy Z Fold5 and Z Flip5, attributing their success to durable ultra-thin glass, improved hinge design, and vibrant AMOLED panels. These models drove a 24% YoY growth in Samsung’s foldable lineup.

- The rise of hybrid working, gaming-on-the-go, and multi-screen functionality makes foldable displays a key growth driver in consumer and enterprise segments.

Opportunity

“Automotive Integration of Flexible Displays in Smart Cockpits”

- The automotive sector is embracing flexible and curved displays for smart dashboards, infotainment systems, and heads-up displays, transforming vehicle interiors into immersive digital spaces.

- Automakers are replacing conventional control panels with OLED touchscreens and wraparound displays that offer real-time feedback, personalized controls, and a seamless digital interface.

- Flexible display panels are also enhancing design freedom, enabling slimmer and more ergonomic cabin layouts.

- For instance, In March 2025, BMW revealed its concept iVision Dee at CES 2025, featuring a full-width curved flexible display integrated into the dashboard. The display spans the windscreen base, merging real-time driving data, navigation, and infotainment on a single screen.

- As EVs and connected vehicles rise, this trend opens new revenue streams for display manufacturers targeting next-gen automotive design and UX innovation.

Restraint/Challenge

“High Manufacturing Costs & Material Limitations of Flexible Displays”

- The production of flexible displays, particularly OLED and plastic-based variants, involves complex processes, precision engineering, and high-cost materials, making end products expensive for mainstream consumers.

- Yield issues during manufacturing—like pixel uniformity, substrate stress, and lamination failures—lead to wastage and further drive-up costs.

- Dependency on a limited number of suppliers for flexible substrates and encapsulation materials creates supply chain bottlenecks and reduces scalability

- For instance, In January 2024, Japan Display Inc. (JDI) delayed mass production of its flexible OLED panels due to low yield rates and high defect percentages, impacting its supply agreements with major smartphone manufacturers.

- Additionally, repairability and recyclability remain major concerns, as flexible screens are more vulnerable to scratches, creases, and structural fatigue over time—raising questions about long-term durability and sustainability.

Flexible Display Market Scope

The market is segmented on the basis type, substrate material, application, form factor, panel size.

|

Segmentation |

Sub-Segmentation |

|

By type |

|

|

By substrate material |

|

|

By Application |

|

|

By form factor |

|

|

By panel size |

|

In 2025, the OLED is projected to dominate the market with a largest share inbytype segment

The OLED segment is expected to dominate the Flexible Display market, with a market share of 37.23% during the forecast period. This leadership is attributed to the soaring demand for lightweight, foldable, and energy-efficient display devices, increasing adoption in smartphones, wearables, and televisions, and continuous technological advancements in display quality and durability

TheLCDis expected to account for the largest share during the forecast period inFlexible Display market

In 2025, the LCD segment in the Flexible Display Market is projected to hold the largest share of approximately 35.87%. This dominance is driven by the widespread availability, cost-effectiveness, and mature production technology of LCD panels, along with their extensive use in applications such as signage, monitors, and consumer electronics across both consumer and commercial sectors..

Flexible Display Market Regional Analysis

“Asia-Pacific Holds the Largest Share in theFlexible Display Market”

- Asia-Pacific dominates the Flexible Display Market, driven by the presence of major display panel manufacturers, increasing demand for flexible and foldable smartphones, and technological advancements in countries such as China, South Korea, and Japan.

- China and South Korea are major contributors due to their massive electronics manufacturing ecosystems, strong R&D focus, and aggressive expansion into next-gen OLED and AMOLED technologies.

- Japan, with its advanced infrastructure and legacy in display technology, plays a key role in supplying high-quality flexible components for wearables, automotive dashboards, and digital signage.

- The region’s dominance is further reinforced by government-backed initiatives promoting smart manufacturing, smart cities, and digital transformation across public and private sectors.

“North America is Projected to Register the Highest CAGR in theFlexible Display Market”

- North America is expected to witness the fastest growth in the Flexible Display Market, driven by rising adoption of advanced consumer electronics, smart home technologies, and automotive infotainment systems.

- The U.S. leads the region due to the presence of major tech companies like Apple, Corning, and Universal Display Corporation that are investing heavily in foldable devices, wearable tech, and AR/VR applications powered by flexible displays.

- The integration of flexible displays into smart vehicles, next-gen laptops, and innovative commercial displays is accelerating regional demand.

- Additionally, growing consumer preference for sleek, high-performance, and space-saving devices and a strong ecosystem of startups and R&D labs support long-term growth prospects in the region.

Flexible Display Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- LG Display Co., Ltd. (South Korea)

- BOE Technology Group Co., Ltd. (China)

- Japan Display Inc. (Japan)

- Koninklijke Philips N.V. (Netherlands)

- SAMSUNG (South Korea)

- Apple Inc. (U.S.)

- Corning Incorporated (U.S.)

- DuPont (U.S.)

- ASUSTeK Computer Inc. (Taiwan)

- BenQ Materials Corporation (Taiwan)

- AU Optronics Corp. (Taiwan)

- Bolymin Inc. (Taiwan)

- CASIO COMPUTER CO., LTD. (Japan)

- Chunghwa Picture Tubes, LTD. (Taiwan)

- Planar Systems, Inc. (U.S.)

- Toshiba Corporation (Japan)

- Sony Corporation (Japan)

- Atmel Corporation (U.S.)

- Universal Display Corporation (U.S.)

- Novaled AG (Germany)

Latest Developments in Global Flexible Display Market

- On March 10, 2025, flexible displays and wearable technology emerged as transformative forces in the consumer electronics landscape, breaking traditional boundaries and redefining how users interact with devices. These innovations are driven by advancements in materials science, miniaturization, and next-gen manufacturing techniques.

- On November 11, 2024, LG unveiled the world’s first stretchable display, capable of expanding from 12 to 18 inches without image loss. Built on microLED tech, it endures 10,000 stretch cycles and supports touch gestures. This ultra-thin, wearable-ready innovation challenges Samsung's foldables and sets a new benchmark in flexible display technology across smartphones, tablets, and wearables.

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。