Global Green Roof Market

市场规模(十亿美元)

CAGR :

%

USD

1.93 Billion

USD

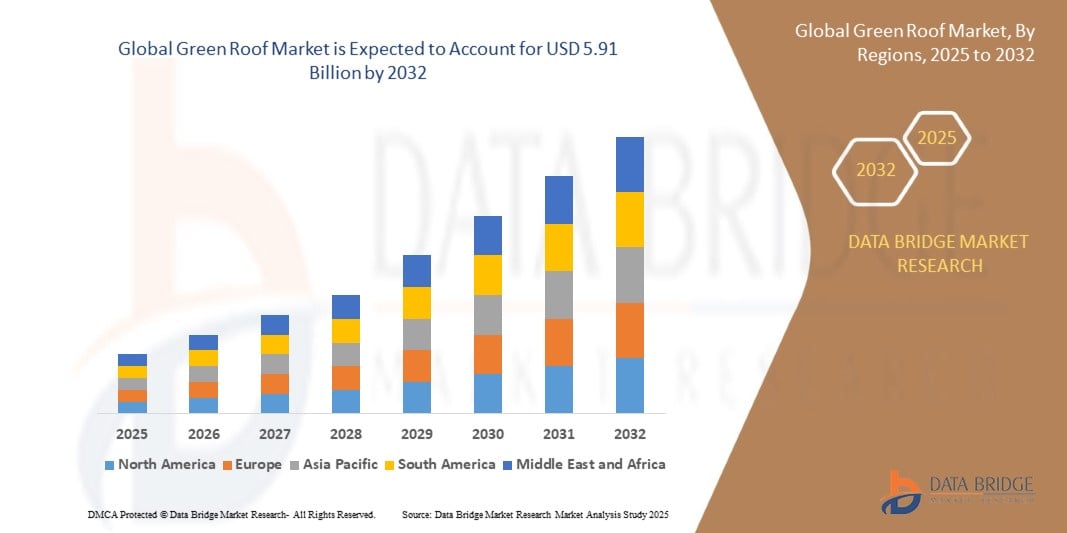

5.91 Billion

2024

2032

USD

1.93 Billion

USD

5.91 Billion

2024

2032

| 2025 –2032 | |

| USD 1.93 Billion | |

| USD 5.91 Billion | |

| % | |

|

全球綠色屋頂市場細分,按類型(粗放型、半集約型和集約型)、應用(住宅、商業和工業)、分銷渠道(零售和批發)、植被類型(景天和多肉植物、本地草類和野花、蔬菜和藥草園) - 行業趨勢和預測至 2032 年

綠屋頂市場規模

- 2024 年全球綠屋頂市場規模為19.3 億美元 ,預計 到 2032 年將達到 59.1 億美元,預測期內 複合年增長率為 15.00%。

- 市場成長主要受到對永續城市發展的日益重視、對氣候變遷日益增長的擔憂以及政府對節能基礎設施的激勵

- 綠建築規範的日益普及,以及人們對綠屋頂的環境和經濟效益的認識不斷提高,例如改善隔熱效果、減少城市熱島效應和加強雨水管理,進一步支持了市場擴張

綠屋頂市場分析

- 在嚴格的環境法規和城市永續發展目標的推動下,歐洲和北美已開發經濟體的市場正在經歷顯著增長

- 此外,亞太地區快速的城市化正在促進綠色屋頂的安裝,尤其是在商業和公共基礎設施項目中

- 歐洲在全球綠色屋頂市場佔據主導地位,2024 年其收入份額最高,為 42.8%,這得益於嚴格的環境法規、日益增長的城市可持續發展計劃以及政府對環保建築實踐的大力激勵

- 受快速城市化、環保意識增強以及中國、印度和日本等國家政府大力推行永續建築實踐的推動,亞太地區預計將成為全球綠色屋頂市場成長率最高的地區。

- 2024年,大面積屋頂綠化佔據了市場主導地位,其市場收入份額最大,這得益於其維護要求低、結構負荷輕和成本效益高。大面積屋頂綠化因其土壤層較薄、安裝成本較低而被廣泛用於現有建築的改造。對於有結構限制的城市環境來說,大面積屋頂綠化是理想之選,能夠提供隔熱和雨水管理優勢,且維護成本極低。

報告範圍和綠色屋頂市場細分

|

屬性 |

綠屋頂關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括進出口分析、生產能力概覽、生產消費分析、價格趨勢分析、氣候變遷情景、供應鏈分析、價值鏈分析、原材料/消耗品概覽、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

綠屋頂市場趨勢

“智慧綠色屋頂系統在城市建設中的應用激增”

- 智慧綠色屋頂系統越來越多地與自動灌溉和環境感測器等技術相結合,以優化建築性能

- 這些系統具有降低能耗、增強雨水管理以及即時監測濕度和溫度水平等優勢

- 城市開發商正在採用智慧綠色屋頂來滿足永續發展目標和 LEED 等綠色建築認證

- 城市正在利用這些屋頂來解決城市熱島效應並改善建築物的生態足跡

- 例如,新加坡正在「摩天大樓綠化」激勵計畫下實施智慧綠色屋頂,以增強生物多樣性並調節屋頂溫度

綠屋頂市場動態

司機

“支持永續建築的政府措施和法規”

- 北美、歐洲和亞洲各國政府正在實施政策,鼓勵或強制在新建和現有建築上安裝綠屋頂

- 補貼、退稅和補助等財政激勵措施正在提高建築商和業主的採用率

- Regulations in cities such as Chicago and Stuttgart require green roofs on large flat-roof buildings for environmental compliance

- These initiatives support urban resilience against flooding, reduce air pollution, and contribute to carbon emission reductions

- For instance, Stuttgart (Germany) mandates green roofs on new flat-roof buildings larger than 60 m² to combat stormwater runoff and rising urban temperatures

Restraint/Challenge

“High Installation Costs and Structural Limitations”

- The initial cost of green roof installation is significantly higher than traditional roofs due to additional materials and engineering requirements

- Retrofitting older buildings requires structural reinforcement, increasing complexity and deterring property owners

- The lack of skilled labor and green infrastructure policies in some developing regions further hinders adoption

- Long return on investment discourages cost-conscious developers despite long-term energy savings and ecological benefits

- For instance, In Indonesia, limited funding and insufficient technical expertise make it challenging for developers to adopt green roofs in public infrastructure projects

Green Roof Market Scope

The market is segmented on the basis of type, application, distribution channel, and vegetation type.

• By Type

On the basis of type, the green roof market is segmented into extensive, semi-intensive, and intensive. The extensive segment dominated the market with the largest market revenue share in 2024, driven by its low maintenance requirements, lighter structural load, and cost-effectiveness. Extensive green roofs are widely adopted for retrofitting existing buildings due to their thinner soil layers and lower installation costs. They are ideal for urban environments where structural limitations exist, providing insulation and stormwater management benefits with minimal upkeep.

The intensive segment is expected to witness the fastest growth rate from 2025 to 2032, owing to rising demand for high-performance green spaces that can support a wider range of plant types, including shrubs and trees. These roofs offer recreational and aesthetic advantages, making them popular in commercial complexes and institutional buildings. Their adaptability to design, combined with environmental and social benefits, contributes to their growing preference among developers and architects.

• By Application

On the basis of application, the green roof market is segmented into residential, commercial, and industrial. The commercial segment held the largest market revenue share in 2024 due to increased implementation of sustainable practices across office buildings, shopping malls, and hospitality infrastructure. Businesses are embracing green roofs to meet green building certifications and improve energy efficiency.

The residential segment is expected to witness the fastest growth rate from 2025 to 2032, fuelled by increasing awareness among homeowners regarding the benefits of improved insulation, reduced heat absorption, and enhanced property value. The rise in sustainable housing projects across urban centers further supports segment growth.

• By Distribution Channel

On the basis of distribution channel, the green roof market is segmented into retail and wholesale. The wholesale segment dominated the market in 2024, as bulk procurement by construction companies, landscaping contractors, and green building developers remains the most common purchasing approach. Partnerships with large-scale distributors and government-supported building projects also contribute to wholesale dominance.

The retail segment is expected to witness the fastest growth rate from 2025 to 2032, supported by increasing demand from individual homeowners and small-scale developers. Availability of modular green roofing kits and improved accessibility through e-commerce and gardening stores are accelerating retail sales globally.

• By Vegetation Type

On the basis of vegetation type, the green roof market is segmented into sedum and succulents, native grasses and wildflowers, and vegetable and herb gardens. The sedum and succulents segment held the largest market revenue share in 2024 due to their drought-resistant properties, low maintenance, and strong adaptability to varying climatic conditions.

The vegetable and herb gardens segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the rising trend of urban farming and increasing interest in self-sustained food sources. Consumers, particularly in metropolitan areas, are utilizing rooftop spaces to grow fresh produce, aligning with health-conscious and eco-friendly living preferences.

Green Roof Market Regional Analysis

• Europe dominated the global green roof market with the largest revenue share of 42.8% in 2024, driven by strict environmental regulations, growing urban sustainability initiatives, and strong government incentives for eco-friendly construction practices

• Consumers and developers across the region are increasingly adopting green roofs due to their benefits in stormwater management, thermal insulation, and urban biodiversity enhancement

• The widespread implementation of green building standards, along with active participation by municipalities in promoting vegetative roofing through subsidies and policy frameworks, continues to support market expansion across both new developments and retrofit projects

Germany Green Roof Market Insight

2024年,德國綠色屋頂市場佔據歐洲最大份額,達到68%,這得益於積極的環境政策和推廣綠色基礎設施的廣泛市政法規。柏林和斯圖加特等城市已將綠色屋頂要求納入城市規劃規範,加速了住宅和商業建築的綠色屋頂應用。德國在永續建築領域的領先地位,加上公眾意識的提升和資金支持,正在持續增強其市場競爭力。

英國綠屋頂市場洞察

英國綠色屋頂市場預計將在2025年至2032年間實現最快成長,這得益於城市發展的加速、更嚴格的規劃政策以及永續建築的推動。 「倫敦規劃」等倡議旨在推廣綠色基礎設施,鼓勵開發商將綠屋頂納入建築設計。英國對減少碳排放和改善城市空氣品質的重視預計將進一步推動市場擴張。

北美綠屋頂市場洞察

預計北美綠屋頂市場將在2025年至2032年間實現最快增長,這得益於人們對城市熱島效應日益增長的擔憂、對雨水控制的日益重視以及LEED等綠色建築認證的不斷擴展。美國和加拿大各地城市正在推出稅收減免和激勵計劃,以鼓勵綠色屋頂的建設,尤其是在人口密集的大都市地區。將綠屋頂納入永續城市規劃框架,將進一步提升其應用。

美國綠屋頂市場洞察

受環保意識的增強、城市發展規模的擴大以及傳統製冷方式成本的上升等因素推動,美國綠色屋頂市場預計將在北美佔據主導地位。綠屋頂在學校、商業建築和政府設施的應用日益廣泛,紐約、芝加哥和華盛頓特區等城市已強製或鼓勵安裝綠屋頂。公私合作模式以及聯邦政府撥款的到位也推動了市場的發展。

亞太綠屋頂市場洞察

受快速城鎮化、環境問題以及對節能建築解決方案日益增長的需求的推動,亞太地區綠色屋頂市場預計將在2025年至2032年間實現最快增長。日本、中國和韓國等國家正大力投資智慧城市計畫和永續基礎建設。此外,政府不斷增加的激勵措施和宣傳活動也支持綠屋頂在城市規劃中的應用。

日本綠屋頂市場洞察

日本綠色屋頂市場預計將在2025年至2032年間實現最快的成長,因為該國優先考慮永續城市發展和氣候適應基礎設施。由於傳統綠地空間有限,綠色屋頂正廣泛應用於商業、公共和住宅建築,以應對城市熱島效應。日本注重將綠色技術與創新和美學相結合,這將繼續支撐對先進綠色屋頂解決方案的需求。

中國綠屋頂市場洞察

2024年,中國佔據了亞太地區最大的市場收入份額,這得益於政府主導的、旨在發展綠建築的廣泛舉措。碳中和和永續城市擴張的推動,使得各大城市的綠屋頂安裝量增加。受環境政策、空氣品質問題以及有效管理雨水徑流需求的推動,公共建築、學校和商業開發項目越來越多地採用綠色屋頂。

綠屋頂市場份額

綠色屋頂產業主要由知名公司主導,其中包括:

- Optigrün International AG(德國)

- 綠色屋頂砌塊(英國)

- Axter有限公司(英國)

- 森博格林(荷蘭)

- 鮑德有限公司(英國)

- ZinCo GmbH(德國)

- 索普瑞瑪(法國)

- XeroFlor(德國)

- 本德爾(德國)

- 約爾格·布羅伊寧(德國)

- American Hydrotech, Inc.(美國)

- 巴雷特公司(美國)

- 哥倫比亞綠色科技公司(美國)

- ArchiGreen(美國)

- Pashek+MTR(美國)

- 伯克利集團(英國)

- 可口可樂系統(美國)

- Gambit Nash Limited(英國)

- 哈羅登草坪(英國)

- GreenBlue Urban Limited(美國)

全球綠色屋頂市場的最新發展

- 2022年,巴雷特公司被基恩家族收購。此次策略性收購將基恩家族的產品組合拓展至新市場,並增強了其營運能力。此次交易為巴雷特公司提供了更多資源和更廣闊的網絡,促進了其成長和創新。此次收購旨在利用兩家公司之間的綜效,實現長期成功。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。