Global Hydrocolloid Dressing Market

市场规模(十亿美元)

CAGR :

%

USD

1.57 Billion

USD

2.60 Billion

2024

2032

USD

1.57 Billion

USD

2.60 Billion

2024

2032

| 2025 –2032 | |

| USD 1.57 Billion | |

| USD 2.60 Billion | |

| % | |

|

全球水膠體敷料市場,按產品類型(糊狀、粉狀、凝膠/水狀及其他)、材料類型(明膠、果膠、多醣及其他)、應用(急性傷口、慢性傷口和壓瘡)、最終用戶(醫院、診所、美容診所、門診護理中心及其他)細分 - 行業趨勢及預測(至 2032 年)

水膠體敷料市場規模

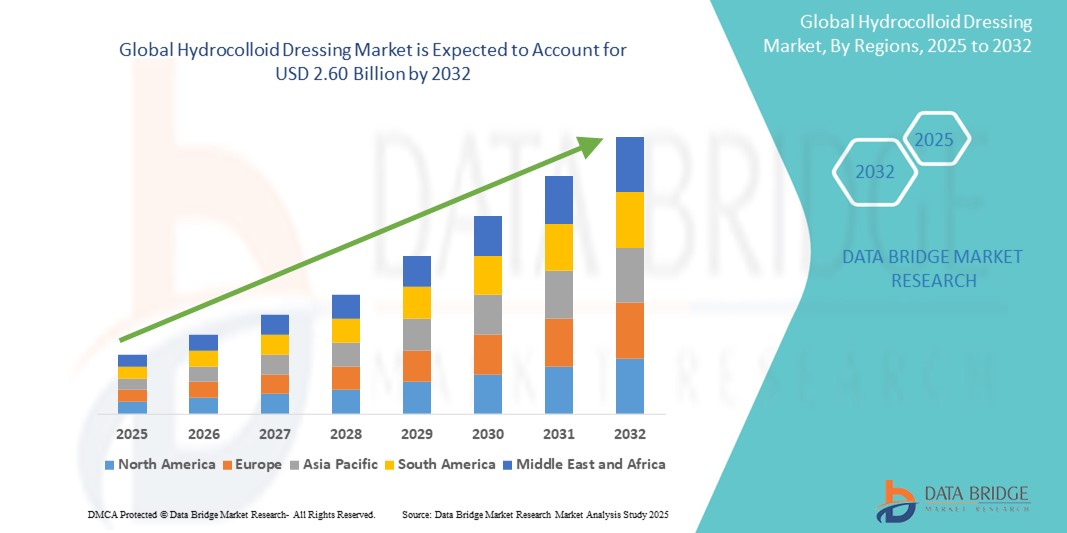

- 2024 年全球水膠體敷料市場規模為15.7 億美元 ,預計 到 2032 年將達到 26 億美元,預測期內 複合年增長率為 6.48%。

- 市場成長主要源於慢性傷口(例如糖尿病足潰瘍、壓瘡和腿部靜脈潰瘍)的日益增多,這些傷口需要先進的傷口護理解決方案來有效癒合和控制感染。水膠體敷料以維持濕潤傷口環境和促進快速恢復而聞名,正成為醫療保健專業人士的首選。

- 此外,醫院和家庭護理機構對微創且經濟高效的傷口護理的需求不斷增長,也加速了水膠體敷料的普及。敷料材料的技術進步,以及人口老化和外科手術的增多,正在顯著推動全球水膠體敷料市場的擴張。

水膠體敷料市場分析

- 水膠體敷料由羧甲基纖維素等凝膠形成劑組成,由於其能夠維持濕潤環境,支持自溶清創,並加速急性和慢性傷口的癒合,越來越被認為是現代傷口護理的重要組成部分

- 水膠體敷料需求的不斷增長,主要由於壓瘡和糖尿病足潰瘍等慢性傷口發病率的上升,以及全球人口老化和外科手術數量的增加

- 北美在水膠體敷料市場佔據主導地位,2024 年其收入份額最大,為 40.6%,這得益於其完善的醫療基礎設施、患者和醫療服務提供者的高度認知以及領先傷口護理公司的強大影響力

- 預計亞太地區將成為預測期內水膠體敷料市場成長最快的地區,2025 年至 2032 年的複合年增長率為 8.7%。這一增長主要得益於醫療保健支出的增加、糖尿病患者的增加以及中國和印度等新興經濟體先進傷口護理服務的普及。

- 慢性傷口領域在水膠體敷料市場佔據主導地位,2024 年的市佔率為 44.7%,這主要是由於糖尿病相關傷口和壓瘡的盛行率不斷上升,尤其是在老年人群中,促使醫療保健提供者青睞具有成本效益和治療優勢的水膠體產品

報告範圍和水膠體敷料市場細分

|

屬性 |

水膠體敷料關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

水膠體敷料市場趨勢

“對先進傷口護理解決方案的偏好日益增長”

- A significant and accelerating trend in the global hydrocolloid dressing market is the growing preference for advanced wound care solutions that support moisture-retentive healing and reduce the need for frequent dressing changes. This trend is driven by the increasing prevalence of chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers, especially among the aging population

- For instance, Smith & Nephew’s ALLEVYN hydrocolloid range incorporates a layered design that absorbs exudate while maintaining a moist wound environment conducive to faster healing. These products reduce the pain associated with dressing removal and can be worn for multiple days, enhancing patient comfort and reducing healthcare costs

- The adoption of hydrocolloid dressings is further fueled by their self-adhering, flexible, and transparent nature, which allows for easy application and monitoring without disturbing the wound. This is particularly important in outpatient and home care settings, where ease of use and reduced frequency of intervention are critical

- In addition, the integration of antimicrobial agents into hydrocolloid dressings is gaining traction, offering enhanced infection control capabilities without compromising moisture balance. Companies such as ConvaTec are leading this innovation with dressings such as AQUACEL Ag, which combine hydrocolloid benefits with silver-based antimicrobial protection

- This trend toward multifunctional, patient-friendly wound dressings is reshaping the global wound care landscape, with hydrocolloids becoming a preferred solution in both hospital and home environments. As a result, manufacturers are increasingly investing in product enhancements that align with the demands of both patients and healthcare providers for efficient, cost-effective healing solutions

Hydrocolloid Dressing Market Dynamics

Driver

“Growing Need Due to Rising Chronic Wound Incidences and Demand for Effective Healing Solutions”

- The increasing prevalence of chronic wounds, such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers, is a major driver for the growing demand for hydrocolloid dressings, which offer superior healing benefits compared to traditional wound care methods

- For instance, in 2024, several healthcare providers expanded their adoption of advanced wound care products, highlighting hydrocolloid dressings as a preferred choice due to their ability to maintain a moist wound environment and promote faster healing. This trend is expected to significantly fuel market growth during the forecast period

- As patients and clinicians become more aware of the benefits of non-invasive, pain-free, and infection-preventive treatments, hydrocolloid dressings are gaining preference over conventional options

- Furthermore, the rising focus on outpatient care and home-based treatment solutions is increasing the demand for easy-to-use, long-wear dressings such as hydrocolloids, which reduce the frequency of dressing changes and hospital visits

- The convenience of self-application, combined with the ability to support autolytic debridement and protect wounds from external contaminants, is driving adoption in both clinical and homecare settings worldwide

Restraint/Challenge

“Concerns Over Allergic Reactions and Limited Usage Scope”

- Despite their advantages, hydrocolloid dressings pose challenges related to potential allergic reactions and skin sensitivities in certain patient groups, which can limit their widespread use. Some patients may experience irritation or maceration if dressings are left on for too long or improperly applied

- For instance, reports of adverse skin reactions have made some healthcare practitioners cautious about recommending hydrocolloid dressings for wounds with heavy exudate or infected sites, restricting their application scope

- Moreover, hydrocolloid dressings are generally not suitable for all wound types, such as highly exudative or deep wounds requiring more advanced therapy, which can limit market penetration in specialized care settings

- Educating healthcare providers and patients about proper dressing selection and usage protocols is critical to mitigating these concerns and ensuring optimal outcomes

- In addition, the need for frequent monitoring in complex wounds can increase healthcare costs, which might deter adoption in resource-limited environments. Addressing these challenges through improved product formulations and enhanced clinical guidelines will be essential for sustained growth in the hydrocolloid dressing market

Hydrocolloid Dressing Market Scope

The market is segmented on the basis of product type, material type, application, and end user.

• By Product Type

On the basis of product type, the hydrocolloid dressing market is segmented into paste, powder, gel/water forms, and others. The gel/water forms segment dominates the largest market revenue share of 38.6% in 2024, driven by its superior hydration capabilities, easy application, and higher patient comfort for managing chronic wounds. These dressings are commonly preferred in clinical settings due to their ability to conform to irregular wound surfaces and maintain an optimal healing environment.

The powder segment is anticipated to witness the fastest growth rate of 20.4% from 2025 to 2032, fueled by increasing use in wound exudate absorption and diabetic ulcer management. The powder format’s versatility and ability to be combined with other advanced dressing types contribute to its growing demand.

• By Material Type

On the basis of material type, the hydrocolloid dressing market is segmented into gelatine, pectin, polysaccharides, and others. The pectin segment held the largest market revenue share of 36.9% in 2024, owing to its excellent gelling and moisture retention properties. Pectin-based hydrocolloid dressings offer superior adhesion and wound protection, making them a top choice for both acute and chronic wounds.

The polysaccharides segment is expected to witness the fastest CAGR of 21.1% from 2025 to 2032, due to its bio-compatibility and increasing incorporation into advanced wound care materials. Polysaccharides promote healing and exhibit high moisture-absorbing capabilities, especially in managing pressure sores and diabetic ulcers.

• By Application

On the basis of application, the hydrocolloid dressing market is segmented into acute wounds, chronic wounds, and pressure sores. The chronic wounds segment accounted for the largest market revenue share of 44.7% in 2024, driven by the rising incidence of diabetic foot ulcers, venous ulcers, and pressure injuries worldwide. Hydrocolloid dressings are particularly effective in managing long-term, non-healing wounds by maintaining a moist healing environment and preventing infection.

The acute wounds segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, due to the growing use of hydrocolloid dressings in surgical site care, burn injuries, and post-traumatic wound management.

• By End User

On the basis of end user, the hydrocolloid dressing market is segmented into hospitals, clinics, aesthetics clinics, ambulatory care centres, and others. The hospitals segment dominates the market with the largest revenue share of 45.7% in 2024, attributed to the high volume of wound care procedures, availability of skilled healthcare professionals, and adoption of advanced wound care products.

The ambulatory care centres segment is projected to grow at the fastest CAGR of 22.5% from 2025 to 2032, driven by the increasing shift toward outpatient treatments, rising demand for cost-effective care, and greater patient preference for same-day treatments using convenient dressing solutions such as hydrocolloids

Hydrocolloid Dressing Market Regional Analysis

- North America dominates the hydrocolloid dressing market with the largest revenue share of 40.6% in 2024, driven by the high prevalence of chronic wounds, advanced healthcare infrastructure, and the increasing adoption of advanced wound care products in both hospital and homecare settings

- The region benefits from strong healthcare reimbursement frameworks, rising cases of diabetic foot ulcers and pressure ulcers, and heightened awareness among clinicians and patients regarding the clinical benefits of hydrocolloid dressings

- This dominance is further supported by a growing elderly population, the presence of key market players, and the widespread availability of technologically advanced wound care solutions across the U.S. and Canada

U.S. Hydrocolloid Dressing Market Insight

The U.S. hydrocolloid dressing market captured the largest revenue share of 73.1% in 2024 within North America, driven by the high incidence of chronic wounds, diabetic foot ulcers, and pressure ulcers. The country’s advanced healthcare infrastructure, favorable reimbursement landscape, and growing preference for advanced wound care over traditional dressings are major contributors. In addition, the rise in outpatient and home healthcare services, coupled with increasing awareness of wound management solutions, continues to propel market growth.

Europe Hydrocolloid Dressing Market Insight

The Europe hydrocolloid dressing market is projected to expand at a substantial CAGR during the forecast period, supported by a growing elderly population, a high prevalence of venous leg ulcers and diabetic wounds, and government initiatives promoting advanced wound care. European healthcare systems' focus on reducing hospital stays and preventing infections encourages the use of hydrocolloid dressings in homecare and long-term care facilities. Both Western and Central Europe are witnessing increased demand due to cost-effectiveness and ease of use.

U.K. Hydrocolloid Dressing Market Insight

The U.K. hydrocolloid dressing market is anticipated to grow at a notable CAGR during the forecast period, primarily fueled by the National Health Service’s (NHS) strategic emphasis on advanced wound care management. An aging population, along with high rates of obesity and diabetes, continues to drive the demand for effective, long-lasting wound healing solutions. Moreover, increased clinical trials and product innovations by key players are further enhancing the country’s market potential.

Germany Hydrocolloid Dressing Market Insight

The Germany hydrocolloid dressing market is expected to expand at a steady CAGR over the forecast period, owing to a robust healthcare infrastructure, strong insurance coverage, and growing use of advanced wound care in elderly and post-operative patients. Hospitals and homecare providers increasingly prefer hydrocolloid dressings for their moisture-retentive and infection-reducing properties. Germany’s focus on medical efficiency and innovation is also encouraging product uptake.

Asia-Pacific Hydrocolloid Dressing Market Insight

The Asia-Pacific hydrocolloid dressing market is poised to grow at the fastest CAGR of 8.7% from 2025 to 2032, propelled by the growing prevalence of diabetes, increased healthcare access, and rising awareness of modern wound care. Urbanization, expanding health insurance coverage, and increased investment in hospital infrastructure across countries such as China, India, and Japan are driving regional growth. The shift from traditional remedies to clinical-grade wound dressings is gaining momentum across both urban and rural healthcare settings.

India Hydrocolloid Dressing Market Insight

受糖尿病病例增加、慢性傷口管理意識增強以及醫院和診所網路擴張的推動,印度水膠體敷料市場預計將在預測期內保持強勁的複合年增長率。政府主導的醫療改革以及「印度醫療援助」(Ayushman Bharat)等項目正在提升公共和私營部門獲得先進傷口護理的可及性。此外,生產經濟實惠的水膠體敷料的本土製造商的湧現,也擴大了二、三線城市的水膠體敷料的供應。

中國水膠體敷料市場洞察

受快速城鎮化、老齡化人口增長以及健康意識增強的推動,中國水膠體敷料市場在2024年佔據亞太地區最大的收入份額。中國在高性價比醫療產品製造領域的領先地位以及社區醫療中心的興起極大地促進了市場需求。公立和私立醫院的擴張,以及政府對先進傷口護理實踐的推廣,將支持市場的長期成長。

水膠體敷料市場份額

水膠體敷料產業主要由知名公司主導,包括:

- 雅培(美國)

- 美敦力(愛爾蘭)

- 3M(美國)

- 康德樂(美國)

- 史賽克(美國)

- Smith+Nephew(英國)

- BD(美國)

- 康維特公司(英國)

- PAUL HARTMANN AG(德國)

- 麥克森公司(美國)

- 強生服務公司(美國)

- B. Braun SE(美國)

- DermaRite Industries, LLC.(美國)

- 康樂保公司(美國)

- Lohmann & Rauscher GmbH & Co. KG(奧地利)

- HELM AG(德國)

- Essity Aktiebolag(出版)。 (瑞典)

- Hollister Incorporated(美國)

- Medline Industries, LP.(美國)

全球水膠體敷料市場的最新發展

- 2023年4月,全球領先的先進傷口管理公司施樂輝(Smith & Nephew)宣佈在部分歐洲市場推出其全新ALLEVYN LIFE水膠體敷料。此敷料專為慢性傷口患者設計,採用多層結構,在優化液體處理的同時保持皮膚完整性。此次推出體現了施樂輝致力於提供以患者為中心的解決方案,並滿足老齡化人群對有效慢性傷口護理日益增長的需求。

- 2023年3月,康維德集團 (ConvaTec Group Plc) 擴展了其 AQUACEL 水膠體敷料產品組合,增強了抗菌性能,旨在降低壓瘡和糖尿病足潰瘍的感染風險。新配方添加了銀離子,可提供持續的抗菌活性,從而增強傷口癒合效果。此項研發彰顯了康維德在感染預防和慢性傷口管理領域創新的策略重點。

- 2023年3月,PAUL HARTMANN AG宣布與一家領先的生物技術公司合作,將智慧感測器技術融入其水膠體敷料中。這些感測器可監測傷口環境中的濕度和pH值平衡,為臨床醫生提供即時回饋。這項試點計畫已在德國和奧地利啟動,彰顯了該公司引領數位化傷口護理創新的雄心壯志。

- 2023年2月,3M健康照護宣布投資1億美元,擴大其位於美國的傷口照護生產設施,以擴大其Tegaderm水膠體敷料的生產。此次擴建旨在滿足全球日益增長的需求,尤其是在北美和亞太地區,這主要源於外科手術和慢性傷口病例的增加。此舉符合3M在先進醫療解決方案領域的長期成長策略。

- 2023年1月,康樂保公司(Coloplast Corp.)推出了專為造口患者設計的Brava水膠體密封條,旨在為造口器具周圍提供更安全、更親膚的密封。這款產品提升了使用者的舒適度,並最大限度地減少了滲漏,支持了康樂保致力於改善私密照護需求人群生活品質的理念。這項創新體現了公司以患者為導向的研發理念和市場反應能力。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。