Global Robotic Cardiology Surgery Market

市场规模(十亿美元)

CAGR :

%

USD

665.09 Million

USD

1,793.30 Million

2024

2032

USD

665.09 Million

USD

1,793.30 Million

2024

2032

| 2025 –2032 | |

| USD 665.09 Million | |

| USD 1,793.30 Million | |

| % | |

|

全球機器人心臟病手術市場細分,按產品和服務(機器人系統、儀器和配件、維護服務和系統服務)、設備類型(機器人機器、導航系統、規劃器和模擬器等)、最終用戶(醫院和研究中心) - 行業趨勢和預測到 2032 年

機器人心臟病手術市場規模

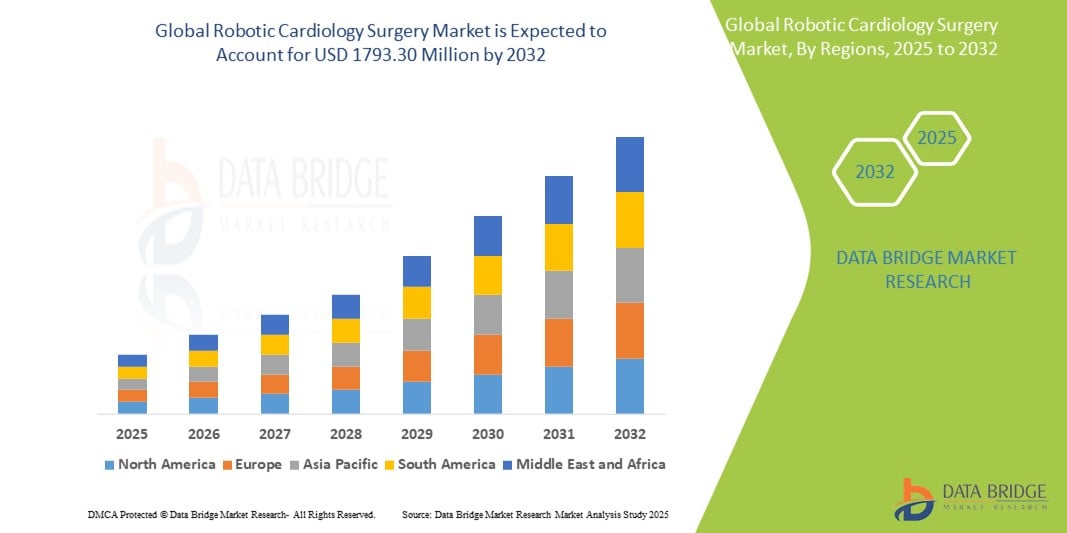

- 2024 年全球機器人心臟病手術市場規模為6.6509 億美元 ,預計 到 2032 年將達到 17.933 億美元,預測期內 複合年增長率為 13.20%。

- 市場成長主要得益於微創手術的日益普及以及機器人輔助手術系統的技術進步,尤其是在心臟病學領域。這些創新提高了手術精準度,減少了手術創傷,並縮短了患者康復時間,從而使得機器人解決方案在公立和私立醫療機構中得到更廣泛的接受。

- 此外,對精準、便利且療效優化的心臟手術的需求日益增長,使得機器人心臟手術成為外科醫生和醫院的首選。這些因素共同加速了機器人心臟手術系統的普及,顯著推動了該行業的成長,並改變了全球心臟護理的模式。

機器人心臟病手術市場分析

- 機器人心臟外科手術系統可為複雜的心臟手術提供高精度、微創的干預,正成為現代心血管護理中日益重要的組成部分。這些技術能夠提高手術精準度,減少失血,縮短住院時間,並最大程度地減少術後併發症,使其成為先進心臟中心和高容量醫院不可或缺的輔助設備。

- 機器人心臟病手術需求的不斷增長,主要原因是心血管疾病(CVD)盛行率的上升、人口老化、對微創手術的偏好增加以及機器人平台的重大技術進步

- 北美在機器人心臟病手術市場佔據主導地位,由於早期採用機器人技術、人均醫療保健支出高以及領先的機器人系統製造商的存在,2024 年其收入份額最大,為 40.9%。

- 亞太地區預計將成為機器人心臟手術市場成長最快的地區,預計 2025 年至 2032 年的複合年增長率為 13.4%,這得益於快速的城市化、醫療基礎設施的改善、人們對微創手術益處的認識不斷提高,以及中國、印度和日本等國家對醫院機器人技術的投資不斷增加

- 機器人系統領域在機器人心臟病手術市場佔據主導地位,2024 年的市場份額為 46.5%,這得益於人們對微創手術的日益偏好以及先進機器人平台在心臟手術中的日益普及

報告範圍與機器人心臟病手術市場細分

|

屬性 |

機器人心臟病手術關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

機器人心臟病手術市場趨勢

“透過技術進步提高效率和精度”

- 全球機器人心臟病手術市場的一個重要且加速發展的趨勢是機器人手術平台和微型儀器的不斷進步,從而實現了更精準、更微創的心臟手術。這些創新正在提升外科醫生的手術能力,降低併發症發生率,並改善患者的復原效果。

- For instance, modern robotic cardiology systems are now designed to perform highly delicate procedures such as mitral valve repair, coronary artery bypass grafting (CABG), and atrial septal defect closures with enhanced dexterity and control. These systems enable cardiac surgeons to operate with better visualization and greater accuracy through small incisions, reducing trauma and hospital stay duration

- The integration of real-time imaging, motion stabilization, and enhanced robotic articulation allows for greater surgical precision, particularly in complex heart operations. These features are improving procedural success rates and reducing the learning curve for new surgeons through simulation-based training modules

- The demand for robotic-assisted cardiology surgeries is also being driven by hospitals and surgical centers’ efforts to improve patient satisfaction, reduce post-operative complications, and meet the growing expectations for less invasive treatment options in cardiovascular care

- As technology continues to evolve, companies in the field are focusing on developing compact, cost-effective robotic systems that are more accessible to mid-sized hospitals and emerging markets. This expansion is expected to broaden adoption beyond premium cardiac care centers into wider healthcare ecosystems globally

- The market is experiencing strong traction across both developed and developing healthcare systems, as robotic cardiology surgery becomes increasingly recognized for its role in enhancing surgical outcomes and reducing healthcare costs in the long term

Robotic Cardiology Surgery Market Dynamics

Driver

“Increasing Global Burden of Cardiovascular Diseases”

- The increasing global burden of cardiovascular diseases (CVDs), combined with the growing demand for precision-based, minimally invasive cardiac interventions, is a major driver for the robotic cardiology surgery market. Patients and healthcare providers asuch as are turning to robotic solutions for their ability to enhance surgical accuracy, reduce complications, and accelerate recovery times

- For instance, in April 2024, Medtronic plc announced advancements in its robotic-assisted cardiac surgical platform aimed at improving access to coronary artery bypass grafting (CABG) and mitral valve repair procedures. Such innovations from key market players are expected to drive market expansion over the forecast period

- As hospitals aim to reduce length of stay and improve patient outcomes, robotic cardiology systems are being increasingly adopted to replace conventional open-heart surgeries. These systems offer features such as motion stabilization, 3D visualization, and high dexterity in confined spaces, enhancing clinical effectiveness

- Furthermore, growing awareness among patients and physicians about the benefits of robotic cardiac procedures is encouraging broader use in both developed and emerging healthcare settings

- The rising demand for advanced surgical solutions, shortage of skilled cardiac surgeons, and integration of training modules with robotic systems are additional factors accelerating the adoption of robotic cardiology surgery across specialized cardiac centers

Restraint/Challenge

“High Initial Investment and Technical Complexity”

- Despite the clinical advantages, the high capital cost of robotic cardiology systems—often exceeding several million dollars—remains a significant barrier to widespread adoption, particularly in resource-constrained settings

- In addition, these systems require specialized infrastructure, trained personnel, and extended setup times, which can be challenging for mid-sized or rural hospitals to accommodate

- For instance, healthcare institutions in developing regions often hesitate to invest in robotic surgical platforms due to concerns over return on investment, system maintenance costs, and the limited volume of eligible procedures

- The learning curve associated with robotic-assisted cardiac procedures is another hurdle, as surgeons must undergo extensive training to operate the systems proficiently and safely

- Moreover, ongoing costs such as maintenance, disposable instruments, and software upgrades can increase the total cost of ownership, affecting adoption rates in price-sensitive markets

Robotic Cardiology Surgery Market Scope

The market is segmented on the basis of product and service, equipment type, and end user.

• By Product and Service

On the basis of product and service, the robotic cardiology surgery market is segmented into robotic systems, instruments and accessories, maintenance services, and system services. The robotic systems segment dominated the market with the largest revenue share of 46.5% in 2024, driven by the rising demand for precision surgical interventions in complex cardiac procedures. These systems offer high-definition visualization, tremor reduction, and enhanced dexterity—key features in minimally invasive surgeries.

The instruments and accessories segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, due to the recurring demand for tools such as end effectors, graspers, and cutters that are essential for each procedure. As the number of robotic surgeries rises globally, this segment experiences consistent growth.

• By Equipment Type

On the basis of equipment type, the market is segmented into robot machines, navigation systems, planners and simulators, and others. The robot machines segment held the largest market revenue share of 49.7% in 2024, attributed to their core role in performing surgical tasks and the increasing installation of robotic platforms in cardiac care centers.

The planners and simulators segment is anticipated to register the fastest CAGR of 20.5% from 2025 to 2032, driven by their growing use in surgeon training and pre-operative planning. Simulation-based learning is becoming essential for mastering complex robotic procedures, particularly in cardiac surgery.

• By End User

On the basis of end user, the robotic cardiology surgery market is segmented into hospitals and research centers. The hospitals segment dominated the market in 2024 with a market share of 84.3%, due to the higher volume of cardiovascular procedures, well-established surgical infrastructure, and the presence of skilled professionals in hospital settings.

The research centers segment is projected to witness the fastest growth rate of 19.1% from 2025 to 2032, fueled by increasing investments in clinical research, technology trials, and the development of next-generation cardiac robotic systems.

Robotic Cardiology Surgery Market Regional Analysis

- North America dominated the robotic cardiology surgery market, holding the largest revenue share of 40.9% in 2024, driven by the early adoption of robotic-assisted surgical technologies and a high prevalence of cardiovascular diseases in the region

- The region benefits from strong healthcare infrastructure, high healthcare expenditure, and widespread access to advanced medical technologies. Hospitals and surgical centers are increasingly integrating robotic systems for precision and minimally invasive cardiology procedures

- Furthermore, the U.S. leads the regional market due to the presence of leading robotic surgery companies, growing acceptance of AI-powered systems in cardiology, and favorable reimbursement frameworks

U.S. Robotic Cardiology Surgery Market Insight

The U.S. robotic cardiology surgery market captured the largest revenue share of 79.8% in 2024 within North America, driven by the country’s strong leadership in medical innovation and clinical research. The widespread adoption of robotic systems in large hospital networks for minimally invasive cardiac procedures has significantly contributed to this dominance. The increasing patient preference for less invasive surgeries with shorter recovery times, along with the presence of top-tier medtech manufacturers, continues to propel the market forward.

Europe Robotic Cardiology Surgery Market Insight

The Europe robotic cardiology surgery market is projected to expand at a substantial CAGR throughout the forecast period, reflecting the continent’s growing emphasis on precision medicine and surgical innovation. The demand is particularly strong in countries such as Germany, the U.K., and France, where hospitals are actively investing in advanced robotic platforms to enhance cardiac surgery outcomes. The combination of rising cardiovascular disease prevalence, favorable regulatory environments, and healthcare digitalization efforts is driving consistent market growth.

U.K. Robotic Cardiology Surgery Market Insight

英國機器人心臟病手術市場預計在預測期內將實現顯著的複合年增長率,這得益於機器人輔助手術在NHS(英國國家醫療服務體系)和私立醫院環境中日益整合的趨勢。國家醫療數位化策略以及減少手術積壓的努力是機器人系統日益普及的關鍵因素,尤其是在診療量大的心臟護理中心。

德國機器人心臟病手術市場洞察

預計在預測期內,德國機器人心臟外科手術市場將以可觀的複合年增長率擴張,這得益於該國強大的醫療基礎設施和對技術進步的重視。德國醫院率先採用機器人系統進行心胸外科手術,旨在提高手術精準度、縮短恢復時間並減少術後併發症。高技能外科醫生的湧現和醫院資金的充裕也進一步支持了市場擴張。

亞太地區機器人心臟病手術市場洞察

預計2025年至2032年期間,亞太地區機器人心臟手術市場將以13.4%的複合年增長率高速成長。快速的城鎮化、不斷擴大的醫療保健投資以及人們對微創手術日益增長的認識,正在推動中國、日本和印度等國家的需求。政府推動醫療體系現代化的措施以及智慧醫院的興起,正在促進市場強勁成長。

中國機器人心臟病手術市場洞察

2024年,中國機器人心臟手術市場以44.3%的市場份額佔據亞太地區主導地位,這得益於其龐大的患者群體、心血管疾病患病率的上升以及政府對人工智慧智慧醫院的大力支持。本土製造能力,加上對高科技精準心臟手術日益增長的需求,使中國成為該區域市場的領導者。

印度機器人心臟病手術市場洞察

預計印度機器人心臟外科手術市場在預測期內將以可觀的複合年增長率擴張。這一快速增長的驅動力包括心臟病負擔的增加、私人醫療基礎設施的擴張以及機器人技術的普及。不斷增加的投資、優惠的政策以及醫療旅遊中心的興起,正在加速一二線城市的市場滲透。

機器人心臟病手術市場份額

機器人心臟病手術產業主要由知名公司主導,包括:

- 強生服務公司(美國)

- Intuitive Surgical, Inc.(美國)

- 美敦力公司(愛爾蘭)

- Stereotaxis, Inc.(美國)

- CMR Surgical Ltd.(英國)

- Auris Health, Inc.(美國)

- Zimmer Biomet(美國)

- Smith + Nephew(英國)

- Asensus Surgical, Inc.(美國)

全球機器人心臟病手術市場的最新發展

- 2024年4月,美敦力在北美和歐洲的部分醫院推出了下一代機器人輔助心臟手術平台。該系統專為微創心臟手術而設計,有望實現更高的精度、更短的手術時間和更強大的即時成像功能,從而鞏固美敦力在智慧手術自動化領域的領先地位。

- 2024年3月,Intuitive宣布與德國大學醫院達成策略合作,試行其最新達文西5機器人手術平台的AI整合版本,用於心臟手術。該軟體透過機器學習和預測分析來增強手術規劃,從而優化心臟病幹預措施。

- 2024年2月,史賽克為亞太地區的訓練機構推出了導航式機器人心胸外科手術模擬器。該系統利用機器人的精準度,模擬二尖瓣修復和冠狀動脈繞道手術,展現了史賽克對創新和外科教育的投入。

- 2024年1月,Zimmer Biomet公司的VersaCardio機器人系統獲得FDA 510(k)批准,該系統旨在用於微創心臟瓣膜手術。該平台融合了機器人技術、即時成像和觸覺回饋,使Zimmer Biomet公司成為機器人心臟病學領域的新興競爭者。預計於2024年第三季進行臨床部署。

- 2023年12月,西門子醫療擴建了位於印度班加羅爾的心臟機器人研發中心,投資約360億印度盧比(約4,500萬美元)。該中心將專注於開發用於介入性心臟病學和導管介入手術的機器人系統,以服務亞太新興市場。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。