Global Robotic Cardiology Surgery Market

Market Size in USD Million

USD

665.09 Million

USD

1,793.30 Million

2024

2032

USD

665.09 Million

USD

1,793.30 Million

2024

2032

| 2025 - 2032 | |

| USD 665.09 Million | |

| USD 1,793.30 Million | |

| % | |

|

Robotic Cardiology Surgery Market Size

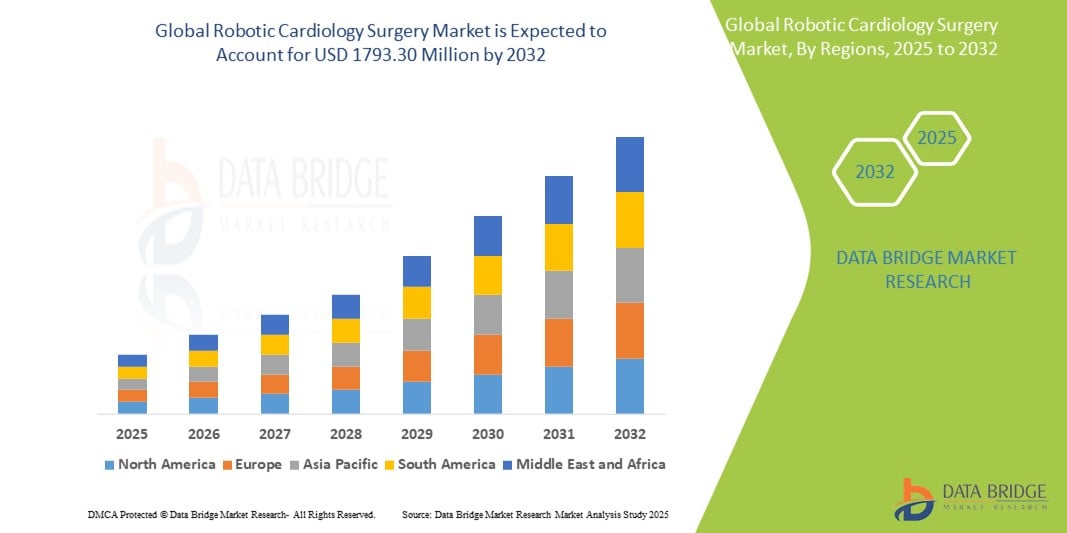

- The global robotic cardiology surgery market size was valued at USD 665.09 Million in 2024 and is expected to reach USD 1,793.30 Million by 2032, at a CAGR of 13.20% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive procedures and technological advancements in robotic-assisted surgical systems, particularly in cardiology. These innovations are enhancing precision, reducing surgical trauma, and shortening patient recovery times, leading to broader acceptance of robotic solutions across both public and private healthcare settings

- Furthermore, rising demand for accurate, user-friendly, and outcome-optimized cardiac procedures is establishing robotic cardiology surgery as a preferred option among surgeons and hospitals. These converging factors are accelerating the uptake of robotic cardiology surgery systems, thereby significantly boosting the industry's growth and transforming the landscape of cardiac care worldwide

Robotic Cardiology Surgery Market Analysis

- Robotic cardiology surgery systems, offering high-precision, minimally invasive interventions for complex heart procedures, are becoming increasingly vital components of modern cardiovascular care. These technologies improve surgical accuracy, reduce blood loss, shorten hospital stays, and minimize post-operative complications, making them indispensable in both advanced cardiac centers and high-volume hospitals

- The escalating demand for robotic cardiology surgery is primarily fueled by the rising prevalence of cardiovascular diseases (CVDs), an aging population, increasing preference for minimally invasive procedures, and significant technological advancements in robotic platforms

- North America dominated the robotic cardiology surgery market, with the largest revenue share of 40.9% in 2024, due to early adoption of robotic technologies, high per capita healthcare expenditure, and the presence of leading robotic system manufacturers

- Asia-Pacific is expected to be the fastest-growing region in the robotic cardiology surgery market, with a projected CAGR of 13.4% from 2025 to 2032, fueled by rapid urbanization, improving healthcare infrastructure, rising awareness of minimally invasive surgical benefits, and growing investments in hospital robotics across countries such as China, India, and Japan

- The robotic systems segment dominated the robotic cardiology surgery market, with a market share of 46.5% in 2024, owing to the growing preference for minimally invasive procedures and the increasing deployment of advanced robotic platforms in cardiac surgeries

Report Scope and Robotic Cardiology Surgery Market Segmentation

|

Attributes |

Robotic Cardiology Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Robotic Cardiology Surgery Market Trends

“Enhanced Efficiency and Precision Through Technological Advancements”

- A significant and accelerating trend in the global robotic cardiology surgery market is the continuous advancement in robotic surgical platforms and miniaturized instrumentation, enabling more precise and minimally invasive cardiac procedures. These innovations are enhancing surgeon capabilities, reducing complication rates, and improving patient recovery outcomes

- For instance, modern robotic cardiology systems are now designed to perform highly delicate procedures such as mitral valve repair, coronary artery bypass grafting (CABG), and atrial septal defect closures with enhanced dexterity and control. These systems enable cardiac surgeons to operate with better visualization and greater accuracy through small incisions, reducing trauma and hospital stay duration

- The integration of real-time imaging, motion stabilization, and enhanced robotic articulation allows for greater surgical precision, particularly in complex heart operations. These features are improving procedural success rates and reducing the learning curve for new surgeons through simulation-based training modules

- The demand for robotic-assisted cardiology surgeries is also being driven by hospitals and surgical centers’ efforts to improve patient satisfaction, reduce post-operative complications, and meet the growing expectations for less invasive treatment options in cardiovascular care

- As technology continues to evolve, companies in the field are focusing on developing compact, cost-effective robotic systems that are more accessible to mid-sized hospitals and emerging markets. This expansion is expected to broaden adoption beyond premium cardiac care centers into wider healthcare ecosystems globally

- The market is experiencing strong traction across both developed and developing healthcare systems, as robotic cardiology surgery becomes increasingly recognized for its role in enhancing surgical outcomes and reducing healthcare costs in the long term

Robotic Cardiology Surgery Market Dynamics

Driver

“Increasing Global Burden of Cardiovascular Diseases”

- The increasing global burden of cardiovascular diseases (CVDs), combined with the growing demand for precision-based, minimally invasive cardiac interventions, is a major driver for the robotic cardiology surgery market. Patients and healthcare providers asuch as are turning to robotic solutions for their ability to enhance surgical accuracy, reduce complications, and accelerate recovery times

- For instance, in April 2024, Medtronic plc announced advancements in its robotic-assisted cardiac surgical platform aimed at improving access to coronary artery bypass grafting (CABG) and mitral valve repair procedures. Such innovations from key market players are expected to drive market expansion over the forecast period

- As hospitals aim to reduce length of stay and improve patient outcomes, robotic cardiology systems are being increasingly adopted to replace conventional open-heart surgeries. These systems offer features such as motion stabilization, 3D visualization, and high dexterity in confined spaces, enhancing clinical effectiveness

- Furthermore, growing awareness among patients and physicians about the benefits of robotic cardiac procedures is encouraging broader use in both developed and emerging healthcare settings

- The rising demand for advanced surgical solutions, shortage of skilled cardiac surgeons, and integration of training modules with robotic systems are additional factors accelerating the adoption of robotic cardiology surgery across specialized cardiac centers

Restraint/Challenge

“High Initial Investment and Technical Complexity”

- Despite the clinical advantages, the high capital cost of robotic cardiology systems—often exceeding several million dollars—remains a significant barrier to widespread adoption, particularly in resource-constrained settings

- In addition, these systems require specialized infrastructure, trained personnel, and extended setup times, which can be challenging for mid-sized or rural hospitals to accommodate

- For instance, healthcare institutions in developing regions often hesitate to invest in robotic surgical platforms due to concerns over return on investment, system maintenance costs, and the limited volume of eligible procedures

- The learning curve associated with robotic-assisted cardiac procedures is another hurdle, as surgeons must undergo extensive training to operate the systems proficiently and safely

- Moreover, ongoing costs such as maintenance, disposable instruments, and software upgrades can increase the total cost of ownership, affecting adoption rates in price-sensitive markets

Robotic Cardiology Surgery Market Scope

The market is segmented on the basis of product and service, equipment type, and end user.

• By Product and Service

On the basis of product and service, the robotic cardiology surgery market is segmented into robotic systems, instruments and accessories, maintenance services, and system services. The robotic systems segment dominated the market with the largest revenue share of 46.5% in 2024, driven by the rising demand for precision surgical interventions in complex cardiac procedures. These systems offer high-definition visualization, tremor reduction, and enhanced dexterity—key features in minimally invasive surgeries.

The instruments and accessories segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, due to the recurring demand for tools such as end effectors, graspers, and cutters that are essential for each procedure. As the number of robotic surgeries rises globally, this segment experiences consistent growth.

• By Equipment Type

On the basis of equipment type, the market is segmented into robot machines, navigation systems, planners and simulators, and others. The robot machines segment held the largest market revenue share of 49.7% in 2024, attributed to their core role in performing surgical tasks and the increasing installation of robotic platforms in cardiac care centers.

The planners and simulators segment is anticipated to register the fastest CAGR of 20.5% from 2025 to 2032, driven by their growing use in surgeon training and pre-operative planning. Simulation-based learning is becoming essential for mastering complex robotic procedures, particularly in cardiac surgery.

• By End User

On the basis of end user, the robotic cardiology surgery market is segmented into hospitals and research centers. The hospitals segment dominated the market in 2024 with a market share of 84.3%, due to the higher volume of cardiovascular procedures, well-established surgical infrastructure, and the presence of skilled professionals in hospital settings.

The research centers segment is projected to witness the fastest growth rate of 19.1% from 2025 to 2032, fueled by increasing investments in clinical research, technology trials, and the development of next-generation cardiac robotic systems.

Robotic Cardiology Surgery Market Regional Analysis

- North America dominated the robotic cardiology surgery market, holding the largest revenue share of 40.9% in 2024, driven by the early adoption of robotic-assisted surgical technologies and a high prevalence of cardiovascular diseases in the region

- The region benefits from strong healthcare infrastructure, high healthcare expenditure, and widespread access to advanced medical technologies. Hospitals and surgical centers are increasingly integrating robotic systems for precision and minimally invasive cardiology procedures

- Furthermore, the U.S. leads the regional market due to the presence of leading robotic surgery companies, growing acceptance of AI-powered systems in cardiology, and favorable reimbursement frameworks

U.S. Robotic Cardiology Surgery Market Insight

The U.S. robotic cardiology surgery market captured the largest revenue share of 79.8% in 2024 within North America, driven by the country’s strong leadership in medical innovation and clinical research. The widespread adoption of robotic systems in large hospital networks for minimally invasive cardiac procedures has significantly contributed to this dominance. The increasing patient preference for less invasive surgeries with shorter recovery times, along with the presence of top-tier medtech manufacturers, continues to propel the market forward.

Europe Robotic Cardiology Surgery Market Insight

The Europe robotic cardiology surgery market is projected to expand at a substantial CAGR throughout the forecast period, reflecting the continent’s growing emphasis on precision medicine and surgical innovation. The demand is particularly strong in countries such as Germany, the U.K., and France, where hospitals are actively investing in advanced robotic platforms to enhance cardiac surgery outcomes. The combination of rising cardiovascular disease prevalence, favorable regulatory environments, and healthcare digitalization efforts is driving consistent market growth.

U.K. Robotic Cardiology Surgery Market Insight

The U.K. robotic cardiology surgery market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing integration of robotic-assisted surgery across NHS and private hospital settings. National healthcare digitization strategies and efforts to reduce surgical backlogs are key contributors to the growing adoption of robotic systems, particularly in high-volume cardiac care centers.

Germany Robotic Cardiology Surgery Market Insight

The Germany robotic cardiology surgery market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s robust healthcare infrastructure and focus on technological advancement. German hospitals are early adopters of robotic systems for cardiothoracic surgeries, aiming to improve precision, minimize recovery times, and reduce post-operative complications. The presence of highly skilled surgeons and favorable hospital funding further support market expansion.

Asia-Pacific Robotic Cardiology Surgery Market Insight

The Asia-Pacific robotic cardiology surgery market is projected to grow at the fastest CAGR of 13.4% from 2025 to 2032. Rapid urbanization, expanding healthcare investments, and increasing awareness of minimally invasive procedures are driving demand across countries like China, Japan, and India. Government initiatives to modernize healthcare systems and the rise of smart hospitals are fostering robust market growth.

China Robotic Cardiology Surgery Market Insight

The China robotic cardiology surgery market dominated Asia-Pacific with a 44.3% share in 2024, propelled by its large patient base, rising prevalence of cardiovascular conditions, and aggressive government backing for AI-enabled smart hospitals. Local manufacturing capabilities, coupled with growing demand for high-tech, precision-based cardiac procedures, position China as a leader in the regional market.

India Robotic Cardiology Surgery Market Insight

The India robotic cardiology surgery market is expected to expand at a considerable CAGR during the forecast period. This rapid growth is driven by a rising burden of heart disease, expanding private healthcare infrastructure, and greater accessibility to robotic technologies. Increasing investments, favorable policies, and the emergence of medical tourism hubs are accelerating market penetration across Tier 1 and Tier 2 cities.

Robotic Cardiology Surgery Market Share

The robotic cardiology surgery industry is primarily led by well-established companies, including:

- Johnson & Johnson Services, Inc. (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Medtronic plc (Ireland)

- Stereotaxis, Inc. (U.S.)

- CMR Surgical Ltd. (U.K.)

- Auris Health, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- Smith + Nephew (U.K.)

- Asensus Surgical, Inc. (U.S.)

Latest Developments in Global Robotic Cardiology Surgery Market

- In April 2024, Medtronic launched its next-generation robot‑assisted cardiac surgery platform in select North American and European hospitals. Designed for minimally invasive heart procedures, the system promises greater precision, shorter operating times, and improved real‑time imaging—reinforcing Medtronic’s leadership in intelligent surgical automation

- In March 2024, Intuitive announced a strategic collaboration with university hospitals in Germany to pilot an AI‑integrated version of its latest da Vinci 5 robotic surgery platform for cardiac use. The software enhances surgery planning through machine learning and predictive analytics to optimize cardiology interventions

- In Feb 2024, Stryker introduced a navigation‑enabled robotic cardiothoracic surgery simulator for training institutions in the Asia‑Pacific region. This system provides simulation for mitral valve repair and coronary artery bypass procedures using robotic precision, showcasing Stryker’s commitment to innovation and surgical education

- In January 2024, Zimmer Biomet received FDA 510(k) clearance for its VersaCardio Robotic System, intended for minimally invasive heart valve surgeries. The platform combines robotics, real‑time imaging, and haptic feedback, positioning Zimmer Biomet as an emerging contender in robotic cardiology. Clinical deployment is expected in Q3 2024

- In December 2023, Siemens Healthineers expanded its cardiac robotics R&D hub in Bangalore, India, investing approximately INR 3,600 crore (~USD 45 million). The facility will focus on developing robotic systems for interventional cardiology and catheter-based procedures to serve emerging APAC markets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.