Global Seborrheic Keratosis Sk Treatment Market

市场规模(十亿美元)

CAGR :

%

USD

2.50 Billion

USD

4.50 Billion

2024

2032

USD

2.50 Billion

USD

4.50 Billion

2024

2032

| 2025 –2032 | |

| USD 2.50 Billion | |

| USD 4.50 Billion | |

| % | |

|

全球脂漏性角化症 (SK) 治療市場細分,按診斷(皮膚活檢、皮膚測試等)、治療(冷凍療法、刮除術或電灼術、燒蝕雷射手術、刮除活檢、局部化學換膚、藥物治療等)、最終用戶(醫院、專科診所、家庭醫療保健等)、分銷管道(直接招標、藥物治療等)、最終用戶(醫院、專科診所、家庭醫療保健等)、分銷管道(直接招標、醫院藥房 20 年 20-20 年)

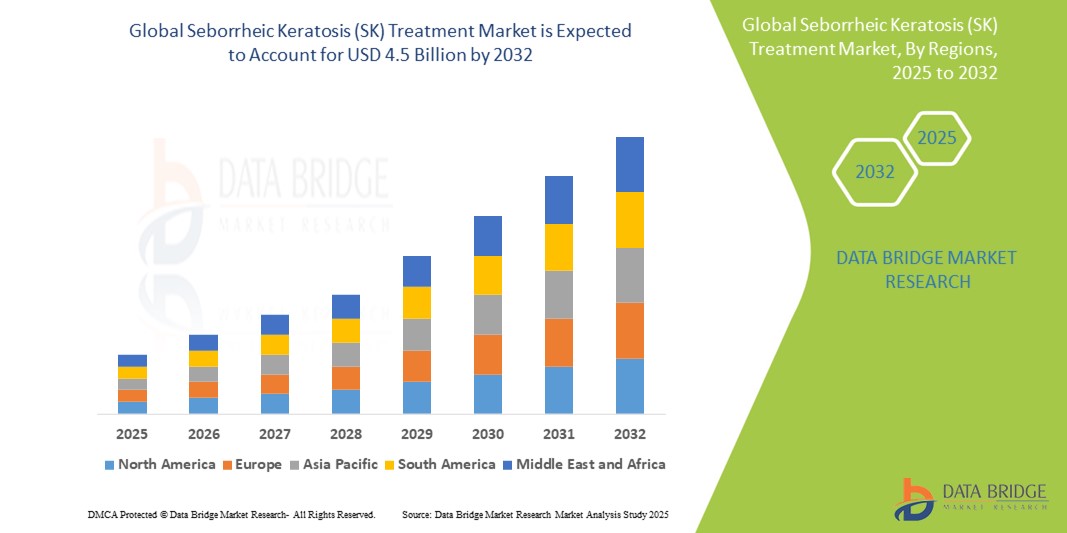

脂漏性角化症(SK)治療市場規模

- 2024 年全球脂漏性角化症 (SK) 治療市場規模為25 億美元 ,預計 到 2032 年將達到 45 億美元,預測期內 複合年增長率為 5.8%。

- 市場成長主要受老齡人口中脂漏性角化病患病率上升以及人們對皮膚健康和早期診斷的認識不斷提高的推動

- 此外,冷凍療法、雷射手術、電燒療法和外用藥物等皮膚病治療方法的進步,正在促進患者治療效果的改善和治療的普及。醫院、專科診所和家庭醫療保健機構對微創美容手術的需求日益增長,進一步推動了市場擴張。這些趨勢的融合預計將在未來幾年推動SK治療產業持續穩定成長。

脂漏性角化症(SK)治療市場分析

- 脂漏性角化症 (SK) 是一種常見的非癌性皮膚病,目前越來越多地採用先進療法進行治療,例如冷凍療法、刮除術或電燒、剝脫性雷射手術、刮除活檢、局部化學剝脫術和外用藥物。這些方法能夠有效去除病灶,最大程度地減少不適感,並改善美容效果,因此在皮膚科診所和醫院中得到越來越廣泛的應用。

- 全球對 SK 治療的需求很大程度上受到老年人口的增長(老年人更容易患 SK)的推動,同時,人們的皮膚健康意識不斷增強,皮膚科服務的日益普及,以及出於美觀原因鼓勵去除良性病變的美容皮膚科趨勢的影響。

- 2024年,北美佔了最大的收入份額,達38.7%。這得歸功於SK發病率高、先進治療技術早期採用、完善的皮膚病學基礎設施以及患者在皮膚相關治療上的支出增加。光是美國一地,2024年SK治療收入就超過6.5億美元。

- 預計亞太地區將成為 2025 年至 2035 年期間成長最快的地區,這得益於大量醫療服務不足的患者群體、城市化進程加快、可支配收入增加以及中國、印度和韓國等國家皮膚病診所和美容中心的擴張。

- 冷凍療法預計將在治療領域佔據主導地位,到 2025 年將佔全球市場份額的約 34.5%,因為它具有高效性、價格實惠以及在門診和家庭護理環境中易於應用的特點

報告範圍和脂漏性角化症(SK)治療市場細分

|

屬性 |

脂漏性角化症(SK)治療關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

脂漏性角化症(SK)治療市場趨勢

“人們對美容皮膚科和非侵入性治療方式的偏好日益增長”

- A significant and accelerating trend in the seborrheic keratosis treatment market is the growing demand for aesthetic dermatological procedures that are minimally invasive, quick, and deliver superior cosmetic outcomes. Patients—especially older adults and professionals—are increasingly seeking removal of benign lesions from visible areas such as the face, neck, and hands for aesthetic purposes.

- For instance, Alma Lasers (Israel) launched the Harmony XL Pro, an advanced multi-technology platform that includes laser-based treatments for benign pigmented lesions like SK. The device is widely used in dermatology clinics across Europe and Asia for fast and scar-minimized removal.

- Similarly, Cutera (U.S.) has expanded the use of its excel V+ laser platform, which is FDA-cleared for treating superficial skin irregularities, including seborrheic keratosis. Dermatologists have reported improved patient outcomes, particularly in patients seeking cosmetic enhancements.

- The market is also witnessing a rise in portable, in-clinic devices that support walk-in procedures, allowing patients to receive treatment without prolonged downtime. Devices like CryoPen X+ are becoming popular among clinics for precise, non-contact cryotherapy for SK lesions.

- Additionally, Aclaris Therapeutics (U.S.) has been developing topical pharmacologic treatments under its AKARI Therapeutics pipeline, aimed at non-invasive, at-home management of non-malignant skin lesions, indicating a shift toward convenience-driven care models.

Seborrheic Keratosis (SK) Treatment Market Dynamics

Driver

“Increasing Prevalence Among Aging Population and Demand for Non-Cancerous Lesion Management”

- A primary driver of the SK treatment market is the growing geriatric population worldwide. As individuals age, the likelihood of developing seborrheic keratosis increases significantly due to cumulative sun exposure and age-related epidermal changes.

- For instance, a study published in the Journal of Clinical and Aesthetic Dermatology (2022) found that over 83% of individuals aged 60+ in the U.S. exhibited at least one SK lesion, many with multiple lesions requiring intervention.

- Furthermore, the American Academy of Dermatology (AAD) has noted a surge in dermatology visits related to benign skin lesions, particularly SK, emphasizing that patients are increasingly seeking removal not only for comfort but for cosmetic satisfaction and peace of mind.

- The wide availability of outpatient treatments such as liquid nitrogen cryotherapy and curettage or shave biopsy in dermatology clinics and specialty hospitals makes it feasible to treat large numbers of patients with minimal infrastructure.

Restraint/Challenge

“Limited Insurance Coverage and Cosmetic Classification of Treatment”

- A key challenge in market expansion is the limited insurance reimbursement for SK procedures. In many countries, treatments for seborrheic keratosis are considered cosmetic rather than medically necessary, especially when the lesions are asymptomatic.

- For instance, in the U.S., Medicare and most private insurers do not cover SK removal unless medically justified, such as in cases of recurrent irritation, bleeding, or diagnostic uncertainty with suspected melanoma. This leads to patients delaying or avoiding treatment due to high out-of-pocket expenses.

- A 2023 survey by the Skin Cancer Foundation found that nearly 48% of U.S. patients with multiple SK lesions opted out of removal procedures due to non-reimbursement and perceived high cost, especially among lower-income or elderly individuals without supplemental insurance.

- Moreover, the recurrence of lesions post-treatment and the need for multiple sessions—especially in patients with extensive skin involvement—can cause dissatisfaction and increase treatment costs, further discouraging uptake in certain markets.

- Addressing these challenges involves educating healthcare providers on the psychosocial burden of SK, developing cost-effective treatment devices, and pushing for reimbursement reforms, particularly in markets with aging populations and high SK prevalence.

Seborrheic Keratosis (SK) Treatment Market Scope

The market is segmented on the basis of diagnosis, treatment, end-users, and distribution channel.

- By Diagnosis

On the basis of diagnosis, the seborrheic keratosis treatment market is segmented into skin biopsy, skin test, and others. The skin biopsy segment held the largest market revenue share of 56.3% in 2024, driven by its widespread use in confirming diagnosis and ruling out malignancies such as melanoma or basal cell carcinoma. Dermatologists often rely on biopsy to differentiate SK from similar-looking lesions. The increasing availability of dermatoscopic tools and trained professionals in clinical settings further supports this segment’s dominance.

The skin test segment is projected to witness the fastest CAGR of 7.9% from 2025 to 2032, as non-invasive diagnostic techniques gain traction. Technological advancements in digital dermoscopy and AI-driven image analysis are making in-clinic skin assessments more accessible, helping to minimize the need for invasive biopsies in routine cases.

By Treatment

On the basis of treatment, the market is segmented into cryotherapy, curettage or electrocautery, ablative laser surgery, shave biopsy, focal chemical peel, medication, and others. Cryotherapy held the largest market revenue share in 2024, accounting for approximately 34.5% of the global market. This dominance is attributed to its cost-effectiveness, ease of application, and suitability for outpatient or homecare settings. For instance, devices like CryoPen X+ are widely used in dermatology practices for precise lesion removal with minimal discomfort.

The ablative laser surgery segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing demand for high-precision, cosmetic-focused treatments. Devices such as the Harmony XL Pro by Alma Lasers (Israel) and excel V+ by Cutera (U.S.) are gaining popularity due to their ability to target SK lesions with minimal scarring and downtime.

• By End-User

On the basis of end-users, the market is segmented into hospitals, specialty clinics, home healthcare, and others. Hospitals accounted for the largest market share in 2024, driven by the availability of advanced equipment, multidisciplinary teams, and insurance-covered treatment pathways in medically justified cases. Hospitals are often the first point of diagnosis for elderly patients presenting with multiple skin lesions.

The home healthcare segment is projected to grow at the fastest CAGR from 2025 to 2032, fueled by the rise in at-home treatment devices, teledermatology consultations, and elderly care services. Increasing availability of user-friendly cryotherapy pens and topical treatments enhances treatment access for immobile or elderly patients.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, hospital pharmacy, retail pharmacy, online pharmacy, and others. Hospital pharmacies held the dominant market revenue share in 2024, primarily due to the high volume of dermatological prescriptions and in-hospital procurement of SK treatment devices and topical medications.

The online pharmacy segment is anticipated to witness the fastest CAGR from 2025 to 2032. This is driven by growing e-commerce penetration in healthcare, increasing consumer preference for convenience, and the availability of prescription and OTC topical medications via digital platforms. Leading players like Netmeds and CVS Health have expanded their dermatology portfolios to include SK-focused therapies.

Seborrheic Keratosis (SK) Treatment Market Regional Analysis

- North America dominates the global seborrheic keratosis treatment market with the largest revenue share of 38.7% in 2024, driven by a high prevalence of SK among the aging population and strong access to dermatological care.

- Consumers in the region are highly proactive about skin health and aesthetics, often opting for SK treatment not just for medical necessity but also for cosmetic reasons. The presence of advanced healthcare infrastructure and a wide network of dermatologists further facilitates early diagnosis and effective treatment.

- This widespread treatment adoption is further supported by higher disposable incomes, greater awareness of non-cancerous skin conditions, and a well-established reimbursement landscape for dermatological evaluations in select cases. The region’s focus on aesthetic dermatology also fuels demand for laser-based and minimally invasive treatment modalities, positioning North America as the leading market for SK care across both medical and cosmetic segments.

North America Seborrheic Keratosis (SK) Treatment Market Insight

The North America seborrheic keratosis treatment market captured the largest revenue share of 38.7% in 2024, driven by a high prevalence of SK among the aging population and an advanced healthcare infrastructure. The region benefits from widespread dermatological awareness, early diagnosis, and access to both medical and cosmetic treatment options. Increasing demand for minimally invasive aesthetic procedures and the growing popularity of outpatient dermatology clinics further support market growth.

U.S. Seborrheic Keratosis (SK) Treatment Market Insight

The U.S. market accounted for over 81% of North America’s SK treatment revenue in 2024, fueled by a large aging demographic, a high rate of dermatology consultations, and strong consumer inclination toward aesthetic skin improvements. The presence of leading players such as Aclaris Therapeutics, Becton Dickinson, and Cutera supports innovation in cryotherapy, laser-based procedures, and pharmacological treatment options. Additionally, favorable reimbursement frameworks for medically indicated cases and the rise of teledermatology contribute to increased patient engagement.

Europe Seborrheic Keratosis (SK) Treatment Market Insight

The European SK treatment market is projected to grow at a significant CAGR throughout the forecast period, driven by rising awareness of skin health, a growing elderly population, and the expansion of dermatology services. Countries like Germany, France, and Italy are seeing increased demand for laser and cryo-based lesion removal procedures. Moreover, stringent healthcare quality regulations and access to public dermatology services in several EU countries ensure timely diagnosis and treatment.

U.K. Seborrheic Keratosis (SK) Treatment Market Insight

The U.K. SK treatment market is anticipated to grow at a healthy CAGR, supported by a combination of public healthcare accessibility through the NHS and rising private-sector dermatology services. A growing awareness of non-malignant skin conditions and their aesthetic impact is encouraging more patients to seek treatment. The availability of advanced diagnostic tools and increasing cosmetic dermatology procedures in private clinics also contribute to the market’s expansion.

Germany Seborrheic Keratosis (SK) Treatment Market Insight

The German SK treatment market is expected to expand at a considerable CAGR, underpinned by the country’s well-established healthcare infrastructure, aging population, and high demand for innovative dermatological procedures. The presence of technologically advanced treatment devices—such as laser systems from Alma Lasers and Quanta Systems—and a cultural emphasis on personal care and early diagnosis support sustained market growth across both clinical and aesthetic segments.

Asia-Pacific Seborrheic Keratosis (SK) Treatment Market Insight

受中國、日本、印度和韓國等國家中產階級的崛起、預期壽命的延長以及皮膚病治療可及性的不斷擴大的推動,亞太地區皮膚性皮膚炎治療市場預計將在2025年以超過7.2%的複合年增長率高速增長。該地區快速的城市化進程和人們對皮膚美容日益增長的興趣,正在推動對經濟高效、微創的皮膚性皮膚炎治療的需求。此外,醫療基礎設施和數位皮膚病學平台的投資不斷增加,也正在擴大患者覆蓋率。

日本脂漏性角化症(SK)治療市場洞察

由於日本人口老化以及對皮膚健康和外觀的強烈文化重視,日本市場正在蓬勃發展。日本越來越多地採用雷射和非侵入性SK治療,尤其是在城市皮膚科診所。 SK護理與更廣泛的抗衰老和美容皮膚解決方案的整合正在推動需求,而人工智慧驅動的皮膚科工具的進步也支持早期診斷和精準治療。

中國脂漏性角化症(SK)治療市場洞察

2025年,中國SK治療市場佔據亞太地區最大收入份額,這得益於人口老化加速、皮膚健康意識增強以及私人皮膚診所數量的激增。中國不斷壯大的中產階級正在尋求改善容貌,這導致對冷凍療法和雷射消融手術的需求激增。此外,本土製造商正在推出價格實惠的治療設備,使SK治療在二、三線城市更加普及。

脂漏性角化症(SK)治療市佔率

脂漏性角化症(SK)治療產業主要由知名公司主導,包括:

- Aclaris Therapeutics, Inc.(美國)

- Coherent, Inc.(美國)

- Quanta Systems SpA(義大利)

- BioLight Technologies LLC.(美國)

- Alma Lasers(以色列)

- AngioDynamics, Inc.(美國)

- 碧迪公司(美國)

- Cutera(美國)

- Erchonia公司(美國)

- IRIDEX公司(美國)

- Lumenis(以色列)

- Biolase Inc.(美國)

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。