Global Ehealth Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

279.20 Billion

USD

1,632.47 Billion

2025

2033

USD

279.20 Billion

USD

1,632.47 Billion

2025

2033

| 2026 –2033 | |

| USD 279.20 Billion | |

| USD 1,632.47 Billion | |

| % | |

|

Global eHealth Market Segmentation, By Offering (Solutions and Services), Deployment (Cloud and On-Premises), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Functionality (Content Management System, Group Messaging, Dashboard, Video Sessions, Social Support, and Others), Technology (Internet of Things (IoT), Chatbots, Artificial Intelligence, Block Chain and Big Data, and Others), End User (Healthcare Providers, Payers, Healthcare Consumers, Pharmacies, and Others)- Industry Trends and Forecast to 2033

eHealth Market Size

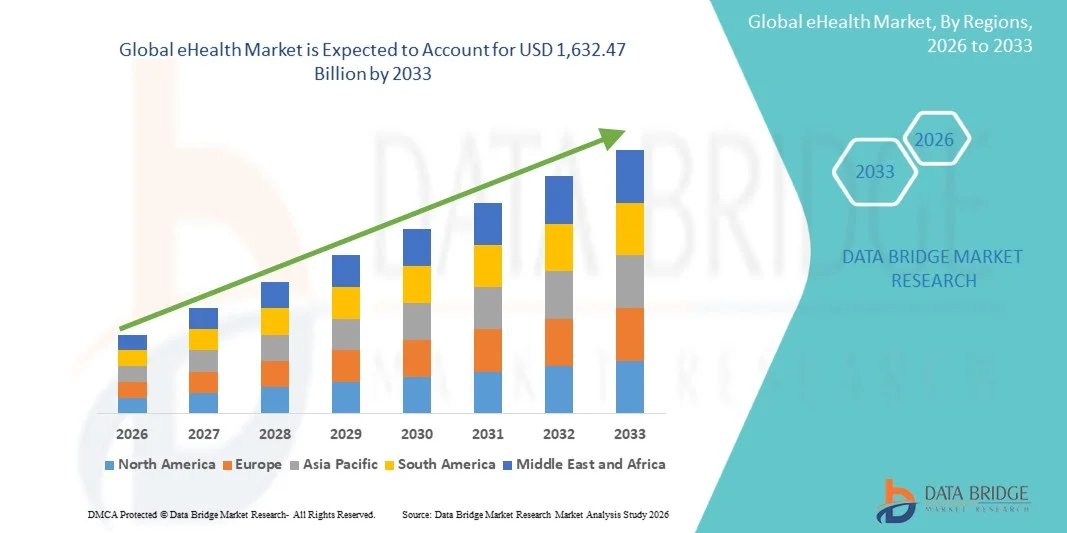

- The global eHealth market size was valued at USD 279.20 billion in 2025 and is expected to reach USD 1,632.47 billion by 2033, at a CAGR of 24.7% during the forecast period

- The market growth is largely fueled by the increasing adoption and technological advancements in digital health solutions, including telemedicine, electronic health records (EHR), mobile health (mHealth), and AI-driven healthcare systems, leading to enhanced healthcare accessibility and efficiency across both developed and emerging regions

- Furthermore, rising demand for cost-effective, patient-centric, and data-driven healthcare solutions, along with growing investments in healthcare IT infrastructure and supportive government initiatives, is establishing eHealth as a critical component of modern healthcare delivery. These converging factors are accelerating the adoption of eHealth solutions, thereby significantly boosting the industry's growth

eHealth Market Analysis

- eHealth, encompassing digital healthcare services such as telemedicine, electronic health records (EHR), mobile health (mHealth), and health information systems, is becoming an integral part of modern healthcare delivery across both clinical and non-clinical settings due to its ability to improve accessibility, efficiency, and patient outcomes

- The escalating demand for eHealth solutions is primarily fueled by the rapid digital transformation of healthcare systems, increasing prevalence of chronic diseases, growing demand for remote patient monitoring, and a rising preference for convenient, cost-effective, and patient-centric care models

- North America dominated the eHealth market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare IT infrastructure, strong regulatory support, and high adoption of digital health technologies, with the U.S. witnessing significant growth in telehealth and EHR implementation driven by major technology providers and healthcare organizations

- Asia-Pacific is expected to be the fastest growing region in the eHealth market during the forecast period due to expanding healthcare infrastructure, increasing internet penetration, and supportive government initiatives promoting digital health adoption

- Services segment dominated the eHealth market with a market share of 46.8% in 2025, driven by the growing demand for teleconsultation, remote monitoring, and digital healthcare management services across hospitals and homecare settings

Report Scope and eHealth Market Segmentation

|

Attributes |

eHealth Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

eHealth Market Trends

“Expansion of AI-Driven Digital Health and Virtual Care Integration”

- A significant and accelerating trend in the global eHealth market is the deepening integration of artificial intelligence (AI) with digital health platforms and virtual care ecosystems such as telemedicine platforms, mobile health applications, and cloud-based health systems. This convergence of technologies is significantly enhancing healthcare accessibility, efficiency, and clinical outcomes

- For instance, leading telehealth platforms are increasingly integrating AI-based diagnostic support and virtual assistants to streamline patient consultations and improve decision-making processes. Similarly, remote monitoring platforms now leverage AI to provide real-time health insights and predictive alerts for patients and healthcare providers

- AI integration in eHealth enables features such as predictive analytics for early disease detection, personalized treatment recommendations, and automated clinical workflows. For instance, some digital health platforms utilize AI algorithms to analyze patient data trends and generate intelligent alerts for potential health risks. Furthermore, virtual care capabilities offer patients the convenience of accessing healthcare services remotely, reducing the need for in-person visits and improving care continuity

- The seamless integration of eHealth solutions with healthcare IT infrastructure and connected medical devices facilitates centralized management of patient data and care delivery. Through unified platforms, healthcare providers can monitor patient conditions, manage records, and coordinate treatments efficiently, creating a more connected and data-driven healthcare ecosystem

- This trend towards more intelligent, accessible, and interconnected healthcare systems is fundamentally transforming how healthcare services are delivered and consumed. Consequently, companies such as Philips Healthcare are developing AI-enabled digital health solutions with features such as remote diagnostics, predictive monitoring, and integration with cloud-based healthcare platforms

- • The demand for eHealth solutions that offer seamless AI integration and virtual care capabilities is growing rapidly across hospitals, clinics, and homecare settings, as stakeholders increasingly prioritize efficiency, accessibility, and patient-centric healthcare delivery

- Moreover, increasing utilization of wearable health technologies and Internet of Medical Things (IoMT) devices is driving continuous patient monitoring and real-time data collection, further strengthening the capabilities of eHealth ecosystems

eHealth Market Dynamics

Driver

“Rising Demand Due to Increasing Digitalization and Need for Remote Healthcare Solutions”

- The increasing need for accessible and efficient healthcare services, coupled with the rapid digitalization of healthcare systems, is a significant driver for the growing demand for eHealth solutions

- For instance, in March 2025, Teladoc Health, Inc. announced the expansion of its AI-powered virtual care services to enhance patient engagement and improve care outcomes. Such strategic developments by key companies are expected to drive the eHealth market growth in the forecast period

- As healthcare systems face rising patient loads and resource constraints, eHealth solutions offer advanced capabilities such as remote consultations, digital health records, and automated workflows, providing a scalable alternative to traditional healthcare delivery models

- Furthermore, the increasing adoption of smartphones, internet connectivity, and wearable health devices is enabling broader access to digital health services, making eHealth a critical component of modern healthcare infrastructure

- The convenience of remote access to healthcare professionals, real-time health monitoring, and improved patient engagement through digital platforms are key factors propelling the adoption of eHealth solutions across both developed and emerging markets. The trend towards personalized medicine and preventive healthcare further contributes to market expansion

- In addition, supportive government initiatives and funding programs aimed at digital health transformation are accelerating the deployment of eHealth infrastructure across public and private healthcare systems

- Moreover, the growing demand for value-based care and outcome-driven healthcare models is encouraging healthcare providers to adopt digital solutions that enhance efficiency, reduce costs, and improve patient satisfaction

Restraint/Challenge

“Data Privacy Concerns and Regulatory Compliance Hurdles”

- Concerns regarding data privacy, cybersecurity risks, and stringent regulatory requirements pose significant challenges to the widespread adoption of eHealth solutions. As digital health platforms handle sensitive patient information, they are vulnerable to data breaches and unauthorized access, raising concerns among users and healthcare providers

- For instance, incidents involving healthcare data breaches and cyberattacks on hospital systems have increased scrutiny on digital health platforms, impacting user trust and adoption rates

- Addressing these concerns through robust data protection measures, compliance with healthcare regulations, and secure system architectures is essential for market growth. Companies such as Cerner Corporation and Allscripts Healthcare Solutions emphasize secure data management and regulatory compliance in their offerings to build trust among users. In addition, the high cost of implementing advanced healthcare IT infrastructure and integrating legacy systems can be a barrier for smaller healthcare providers, particularly in developing regions

- While technological advancements are improving system capabilities, the complexity of integrating eHealth solutions with existing healthcare frameworks can still limit adoption. Variations in regulatory standards across regions further complicate implementation and scalability for global players

- Overcoming these challenges through enhanced cybersecurity frameworks, standardized regulations, and increased investment in healthcare IT infrastructure will be crucial for ensuring sustained growth and broader adoption of eHealth solutions

- In addition, limited digital literacy among certain patient populations and healthcare professionals can hinder effective utilization of eHealth platforms, especially in rural and underserved regions

- Moreover, interoperability issues between different digital health systems and platforms continue to restrict seamless data exchange, creating inefficiencies and limiting the full potential of integrated eHealth ecosystems

eHealth Market Scope

The market is segmented on the basis of offering, deployment, enterprise size, functionality, technology, and end user.

- By Offering

On the basis of offering, the eHealth market is segmented into solutions and services. The services segment dominated the market with the largest market revenue share of 46.8% in 2025, driven by the increasing demand for teleconsultation, remote patient monitoring, and healthcare IT support services. Healthcare providers are increasingly relying on managed and professional services to deploy, maintain, and optimize digital health platforms. The growing need for continuous patient engagement and real-time healthcare delivery further strengthens the demand for service-based models. In addition, services enable seamless integration of various digital health tools, enhancing operational efficiency. The rise in outsourcing of healthcare IT operations is also contributing to segment dominance.

The solutions segment is anticipated to witness the fastest growth rate during the forecast period, fueled by rapid advancements in digital health platforms such as EHR, telemedicine software, and AI-based diagnostic tools. Increasing investments in healthcare IT infrastructure and rising adoption of cloud-based health solutions are accelerating growth. Healthcare organizations are focusing on implementing comprehensive digital systems to improve patient outcomes and streamline workflows. Continuous innovation in software capabilities and interoperability features is further supporting segment expansion.

- By Deployment

On the basis of deployment, the eHealth market is segmented into cloud and on-premises. The cloud segment dominated the market in 2025 driven by its scalability, cost-effectiveness, and ease of access across multiple healthcare settings. Cloud-based platforms allow healthcare providers to store and manage large volumes of patient data securely while enabling remote accessibility. The increasing shift toward digital transformation and telehealth services has significantly boosted cloud adoption. In addition, cloud deployment supports seamless updates, integration, and data sharing across systems. The growing need for flexible and efficient healthcare delivery models continues to drive this segment.

The on-premises segment is expected to witness the fastest growth rate during the forecast period, primarily due to increasing concerns regarding data security and regulatory compliance. Large healthcare institutions often prefer on-premises systems for greater control over sensitive patient data. These systems offer enhanced customization and integration with existing infrastructure. Growing investments in secure IT environments and data protection frameworks are supporting segment growth. The demand from regions with strict healthcare data regulations is also contributing to its expansion.

- By Enterprise Size

On the basis of enterprise size, the market is segmented into large enterprises and small and medium enterprises. The large enterprises segment dominated the market in 2025 due to their strong financial capabilities and early adoption of advanced healthcare IT systems. Large hospitals and healthcare networks invest heavily in digital transformation initiatives to enhance operational efficiency and patient care. They also benefit from the ability to integrate multiple digital health solutions across departments. The presence of dedicated IT teams further supports implementation and maintenance. In addition, large-scale patient data management requirements drive the adoption of comprehensive eHealth platforms.

The small and medium enterprises segment is projected to grow at the fastest rate during the forecast period, driven by increasing accessibility of cost-effective cloud-based solutions. SMEs are rapidly adopting digital health technologies to improve service delivery and remain competitive. Government initiatives supporting digital healthcare adoption among smaller providers are also boosting growth. The availability of scalable and user-friendly platforms is encouraging adoption. Furthermore, rising awareness about digital health benefits is accelerating penetration in this segment.

- By Functionality

On the basis of functionality, the market is segmented into content management system, group messaging, dashboard, video sessions, social support, and others. The video sessions segment dominated the market in 2025, driven by the widespread adoption of telemedicine and virtual consultations. The need for remote healthcare services, especially post-pandemic, has significantly increased reliance on video-based interactions. Healthcare providers use video sessions for diagnosis, follow-ups, and patient engagement. This functionality enhances accessibility for patients in remote and underserved areas. Continuous improvements in video technology and connectivity are further strengthening this segment.

The dashboard segment is expected to witness the fastest growth rate during the forecast period, fueled by the growing need for real-time data visualization and clinical decision support. Dashboards enable healthcare professionals to monitor patient data, track performance metrics, and make informed decisions efficiently. Increasing integration of AI and analytics tools is enhancing dashboard capabilities. The demand for data-driven healthcare systems is driving rapid adoption. In addition, dashboards support improved workflow management and operational efficiency.

- By Technology

On the basis of technology, the market is segmented into Internet of Things (IoT), chatbots, artificial intelligence, blockchain and big data, and others. The artificial intelligence segment dominated the market in 2025, driven by its widespread application in diagnostics, predictive analytics, and personalized treatment planning. AI technologies enable faster and more accurate clinical decision-making, improving patient outcomes. Healthcare providers are increasingly integrating AI into digital platforms to enhance efficiency and reduce costs. The growing volume of healthcare data is further supporting AI adoption. Continuous advancements in machine learning and deep learning are strengthening segment dominance.

The Internet of Things (IoT) segment is expected to witness the fastest growth rate during the forecast period, fueled by the increasing adoption of connected medical devices and remote monitoring solutions. IoT enables real-time health tracking and data collection, improving patient management. The rise of wearable health devices is significantly contributing to segment growth. Healthcare providers are leveraging IoT for proactive and preventive care. Expanding use of smart sensors and connected ecosystems is further accelerating adoption.

- By End User

On the basis of end user, the market is segmented into healthcare providers, payers, healthcare consumers, pharmacies, and others. The healthcare providers segment dominated the market in 2025 due to the extensive use of digital health solutions in hospitals, clinics, and diagnostic centers. Providers rely on eHealth platforms for patient management, clinical workflows, and data integration. The increasing patient load and need for efficient healthcare delivery are driving adoption. Investments in digital infrastructure by hospitals are further supporting growth. In addition, the shift toward value-based care is boosting demand among providers.

The healthcare consumers segment is expected to witness the fastest growth rate during the forecast period, driven by increasing awareness and adoption of digital health applications. Consumers are actively using mobile health apps, wearable devices, and telehealth platforms for self-monitoring and preventive care. The demand for personalized and convenient healthcare services is accelerating segment growth. Rising internet penetration and smartphone usage are further enabling adoption. The trend toward patient-centric healthcare is significantly contributing to expansion.

eHealth Market Regional Analysis

- North America dominated the eHealth market with the largest revenue share of 38.5% in 2025, characterized by advanced healthcare IT infrastructure, strong regulatory support, and high adoption of digital health technologies

- Healthcare providers and patients in the region highly value the accessibility, efficiency, and advanced capabilities offered by eHealth solutions such as telemedicine platforms, electronic health records, and remote monitoring systems

- This widespread adoption is further supported by favorable government initiatives, high healthcare expenditure, and a technologically advanced population, along with the growing preference for digital and patient-centric care, establishing eHealth as a key component of modern healthcare delivery across both clinical and homecare settings

U.S. eHealth Market Insight

The U.S. eHealth market captured the largest revenue share of 80% in 2025 within North America, fueled by the rapid adoption of digital healthcare technologies and the expanding trend of telehealth services. Healthcare providers and patients are increasingly prioritizing improved care delivery through virtual consultations, electronic health records, and remote monitoring systems. The growing preference for digital healthcare platforms, combined with strong demand for AI-driven diagnostics and mobile health applications, further propels the eHealth market. Moreover, the increasing integration of advanced technologies such as artificial intelligence, cloud computing, and data analytics is significantly contributing to the market's expansion.

Europe eHealth Market Insight

The Europe eHealth market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations and the rising need for efficient healthcare delivery systems. The increase in aging population, coupled with the demand for digital health solutions, is fostering the adoption of eHealth. European healthcare providers are also drawn to the efficiency and cost-effectiveness these solutions offer. The region is experiencing significant growth across hospitals, clinics, and homecare settings, with eHealth solutions being incorporated into both existing healthcare systems and new digital infrastructure projects.

U.K. eHealth Market Insight

The U.K. eHealth market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing adoption of telemedicine and a strong focus on improving healthcare accessibility and efficiency. In addition, pressure on healthcare systems and rising patient demand are encouraging both providers and patients to adopt digital health solutions. The UK’s strong digital infrastructure, alongside its supportive regulatory environment, is expected to continue to stimulate market growth.

Germany eHealth Market Insight

The Germany eHealth market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of digital healthcare solutions and the demand for technologically advanced, secure, and efficient systems. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and data security, promotes the adoption of eHealth, particularly in hospitals and outpatient care settings. The integration of eHealth platforms with existing healthcare systems is also becoming increasingly prevalent, with a strong preference for privacy-focused solutions aligning with local regulatory standards.

Asia-Pacific eHealth Market Insight

The Asia-Pacific eHealth market is poised to grow at the fastest CAGR of 24.7% during the forecast period of 2026 to 2033, driven by increasing healthcare digitization, rising internet penetration, and growing investments in healthcare infrastructure in countries such as China, Japan, and India. The region's growing focus on improving healthcare accessibility, supported by government initiatives promoting digital health, is driving the adoption of eHealth solutions. Furthermore, as APAC emerges as a hub for digital innovation and healthcare technology development, the affordability and scalability of eHealth solutions are expanding to a wider population base.

Japan eHealth Market Insight

The Japan eHealth market is gaining momentum due to the country’s advanced technological landscape, aging population, and strong demand for efficient healthcare delivery. The Japanese market places significant emphasis on quality care, and the adoption of eHealth is driven by the increasing need for remote monitoring and digital health management. The integration of eHealth solutions with IoT devices, such as wearable health monitors and connected medical systems, is fueling growth. Moreover, Japan's aging population is likely to spur demand for accessible and reliable digital healthcare solutions in both clinical and homecare settings.

India eHealth Market Insight

The India eHealth market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding population, rapid digital transformation, and increasing adoption of mobile health technologies. India stands as one of the fastest-growing markets for digital healthcare solutions, and eHealth platforms are becoming increasingly popular across hospitals, clinics, and rural healthcare settings. The push towards digital health initiatives and the availability of cost-effective solutions, alongside strong government support, are key factors propelling the market in India.

eHealth Market Share

The eHealth industry is primarily led by well-established companies, including:

- Teladoc Health, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Medtronic (Ireland)

- McKesson Corporation (U.S.)

- Epic Systems Corporation (U.S.)

- athenahealth, Inc. (U.S.)

- eClinicalWorks, LLC (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- Greenway Health, LLC (U.S.)

- MEDITECH (U.S.)

- DrChrono Inc. (U.S.)

- CareCloud, Inc. (U.S.)

- Health Catalyst, Inc. (U.S.)

- Doximity, Inc. (U.S.)

- Amwell (U.S.)

- Babylon Holdings Limited (U.K.)

- Practo Technologies Pvt. Ltd. (India)

- SHL Telemedicine Ltd. (Israel)

What are the Recent Developments in Global eHealth Market?

- In November 2025, eHealth, Inc., a leading digital health insurance marketplace, announced the expansion of its AI-powered voice agent capabilities to support both enrollment and post-enrollment services. This development enhances customer interaction efficiency and reflects the growing adoption of AI-driven automation in digital healthcare platforms

- In October 2025, Heidi Health secured USD 65 million in Series B funding to further develop its AI-driven clinical documentation and care coordination platform, aiming to improve healthcare efficiency and reduce clinician workload globally

- In July 2025, Samsung Electronics announced the acquisition of Xealth, a U.S.-based digital health platform, to expand its connected healthcare ecosystem by integrating wearable devices with digital health services across hospitals and patient networks. This move highlights the convergence of consumer technology and eHealth platforms

- In June 2025, Hims & Hers Health announced its acquisition of UK-based telehealth provider Zava to expand its presence across Europe, including Germany, France, and Ireland, strengthening its global telehealth footprint and digital care delivery capabilities

- In June 2025, Ant Group launched its AI-powered healthcare application “AQ,” connecting users with over 5,000 hospitals and 1 million doctors, significantly advancing digital healthcare accessibility and large-scale integration of AI in medical services

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.