Global Bladder Cancer Treatment Market

Taille du marché en milliards USD

TCAC :

%

USD

4.11 Billion

USD

5.93 Billion

2025

2033

USD

4.11 Billion

USD

5.93 Billion

2025

2033

| 2026 –2033 | |

| USD 4.11 Billion | |

| USD 5.93 Billion | |

| % | |

|

Segmentation du marché mondial des traitements du cancer de la vessie, par type (carcinome urothélial, carcinome épidermoïde, adénocarcinome et autres), grade (tumeur de la vessie de bas grade, tumeur de la vessie de haut grade et autres), traitement (chirurgie, chimiothérapie, radiothérapie, immunothérapie et autres), voie d'administration (orale, parentérale et autres), canal de distribution (pharmacie hospitalière, pharmacie de détail et autres) - Tendances du secteur et prévisions jusqu'en 2033

Taille du marché des traitements du cancer de la vessie

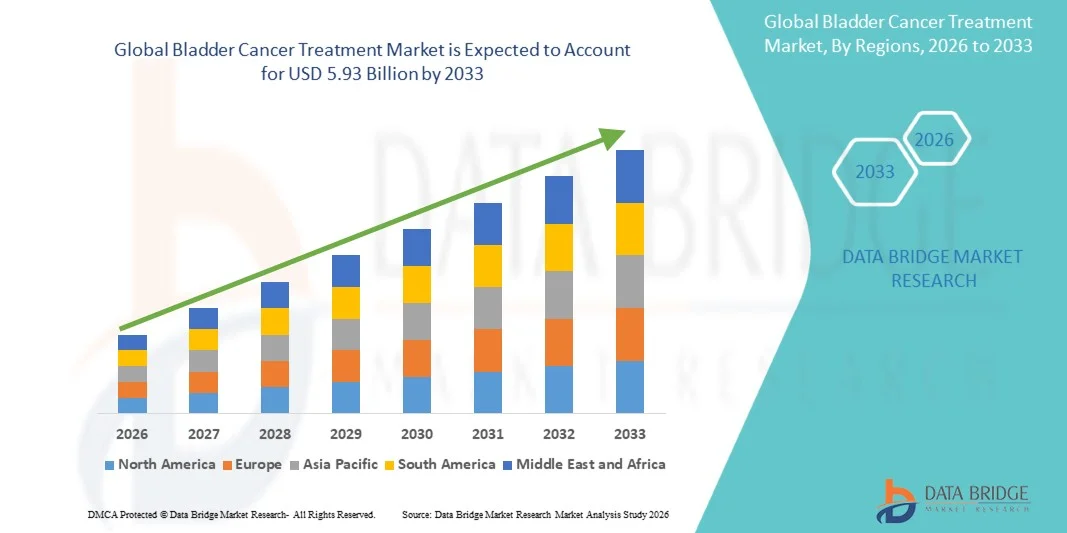

- Le marché mondial des traitements contre le cancer de la vessie était évalué à 4,11 milliards de dollars américains en 2025 et devrait atteindre 5,93 milliards de dollars américains d'ici 2033 , avec un TCAC de 4,7 % au cours de la période de prévision.

- La croissance du marché est largement alimentée par la prévalence croissante du cancer de la vessie dans le monde, la sensibilisation accrue au diagnostic précoce et les progrès constants des traitements, notamment l'immunothérapie , les thérapies ciblées et les interventions chirurgicales mini-invasives.

- Par ailleurs, la hausse des investissements dans la recherche et le développement, conjuguée à l'augmentation des dépenses de santé dans les économies émergentes, favorise l'adoption de traitements innovants et efficaces contre le cancer de la vessie. Ces facteurs convergents accélèrent l'adoption de ces traitements, stimulant ainsi considérablement la croissance du secteur.

Analyse du marché des traitements du cancer de la vessie

- Les traitements du cancer de la vessie, notamment les interventions chirurgicales, l'immunothérapie, la chimiothérapie et les thérapies ciblées, sont des composantes de plus en plus essentielles des soins oncologiques modernes, tant en milieu hospitalier qu'ambulatoire, en raison de leur efficacité accrue, de leurs approches thérapeutiques personnalisées et de leur intégration aux protocoles de médecine de précision.

- La demande croissante de traitements contre le cancer de la vessie est principalement alimentée par la prévalence croissante de ce cancer dans le monde, la sensibilisation accrue au diagnostic précoce et l'augmentation des dépenses de santé consacrées aux thérapies de pointe.

- L'Amérique du Nord a dominé le marché du traitement du cancer de la vessie avec la plus grande part de revenus (39,5 %) en 2025, caractérisée par une infrastructure de soins de santé avancée, une forte sensibilisation des patients et une présence importante d'acteurs pharmaceutiques et biotechnologiques clés. Les États-Unis ont connu une croissance substantielle de l'adoption des immunothérapies et des procédures chirurgicales mini-invasives, grâce aux innovations des entreprises établies et des biotechnologies émergentes.

- La région Asie-Pacifique devrait connaître la croissance la plus rapide sur le marché du traitement du cancer de la vessie au cours de la période de prévision, en raison d'un accès accru aux soins de santé, du vieillissement de la population et du développement des initiatives gouvernementales en matière de lutte contre le cancer.

- Immunotherapy segment dominated the bladder cancer treatment market with a market share of 41.7% in 2025, driven by its demonstrated clinical efficacy, fewer side effects compared to conventional chemotherapy, and growing adoption in combination therapy regimens

Report Scope and Bladder Cancer Treatment Market Segmentation

|

Attributes |

Bladder Cancer Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Bladder Cancer Treatment Market Trends

“Advancements in Immunotherapy and Targeted Therapies”

- A significant and accelerating trend in the global bladder cancer treatment market is the increasing adoption of immunotherapy and targeted therapy, offering personalized and more effective treatment options for advanced and recurrent bladder cancer cases

- For instance, immune checkpoint inhibitors such as pembrolizumab and atezolizumab are being integrated into first-line and second-line therapy protocols, improving patient survival and response rates compared to conventional chemotherapy

- Immunotherapy integration enables features such as combination therapy with chemotherapy or targeted agents, leading to optimized treatment regimens and better patient outcomes. For instance, some clinical trials are evaluating antibody-drug conjugates alongside immunotherapy to improve efficacy in metastatic cases

- The seamless integration of novel treatment modalities with existing surgical and chemotherapeutic approaches facilitates more comprehensive patient management, allowing oncologists to tailor therapies based on tumor stage, genetic biomarkers, and patient health status

- This trend towards more precise, personalized, and effective treatment approaches is fundamentally reshaping patient expectations for bladder cancer care. Consequently, companies such as Merck and Pfizer are developing new immunotherapies and combination regimens with targeted therapy and minimal side effects

- The demand for therapies that offer improved efficacy, fewer adverse effects, and better long-term outcomes is growing rapidly across both developed and emerging healthcare markets, as patients and clinicians increasingly prioritize advanced cancer care options

- Increasing collaborations between pharmaceutical companies, research institutes, and hospitals for clinical trials and real-world evidence generation are driving faster innovation and approval of next-generation bladder cancer treatments globally

Bladder Cancer Treatment Market Dynamics

Driver

“Rising Prevalence of Bladder Cancer and Early Diagnosis Awareness”

- The increasing prevalence of bladder cancer globally, coupled with growing awareness for early detection and treatment, is a significant driver for the heightened demand for advanced therapies

- For instance, in April 2025, Bristol Myers Squibb announced expanded access programs for checkpoint inhibitors, targeting high-risk bladder cancer patients and improving early intervention outcomes

- As healthcare providers and patients become more aware of risk factors such as smoking and occupational exposure, bladder cancer treatments offer advanced therapeutic options that can improve survival and reduce recurrence rates

- Furthermore, rising government and private investments in cancer research, along with increasing adoption of guideline-based treatment protocols, are making advanced bladder cancer therapies a central focus in oncology care

- The availability of targeted therapy, minimally invasive surgeries, and immunotherapies alongside conventional treatments offers patients more options and flexibility in therapy planning, driving adoption across hospitals and specialized cancer centers

- Expansion of healthcare infrastructure and oncology centers, particularly in emerging economies, is improving access to modern treatments, supporting market growth

- Growing patient advocacy, awareness campaigns, and early screening initiatives by non-profits and healthcare organizations are facilitating timely diagnosis and therapy initiation, further driving demand for effective bladder cancer treatments

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Markets”

- The high cost of advanced bladder cancer therapies, including immunotherapies and targeted drugs, poses a significant challenge to broader market adoption, particularly in price-sensitive regions

- For instance, limited insurance coverage and high out-of-pocket expenses make some patients hesitant to pursue these innovative treatments despite clinical efficacy

- Addressing affordability through patient assistance programs, government reimbursement initiatives, and tiered pricing strategies is crucial for increasing accessibility. Companies such as Roche and AstraZeneca emphasize patient support and compassionate use programs to improve uptake

- In addition, limited availability of specialized oncology centers and trained healthcare professionals in emerging economies can restrict timely access to effective therapies, hindering market growth

- While advancements continue in drug development, overcoming cost and access barriers through policy interventions, education, and infrastructure development will be vital for sustained global market expansion

- Regulatory challenges and delays in drug approvals in certain regions can slow the launch of new therapies, affecting market penetration and adoption rates

- Potential side effects, patient intolerance, and variability in response to advanced therapies such as immunotherapy or targeted drugs can limit their widespread use, presenting a clinical challenge for providers and patients alike

Bladder Cancer Treatment Market Scope

The market is segmented on the basis of type, grade type, treatment, route of administration, and distribution channel.

- By Type

On the basis of type, the bladder cancer treatment market is segmented into urothelial carcinoma, squamous cell carcinoma, adenocarcinoma, and others. The urothelial carcinoma segment dominated the market with the largest revenue share in 2025, driven by its high prevalence among bladder cancer patients globally. Most patients diagnosed with bladder cancer have urothelial carcinoma, making therapies such as immunotherapy, chemotherapy, and surgical interventions highly concentrated in this segment. The established clinical protocols, availability of FDA-approved drugs, and extensive research on urothelial carcinoma contribute to its dominant position. Hospitals and oncology centers often prioritize targeted therapies for this type due to its responsiveness to immunotherapy and checkpoint inhibitors. Patient awareness campaigns and routine screenings further reinforce early detection and treatment adoption in this segment.

The squamous cell carcinoma segment is expected to witness the fastest growth during the forecast period due to rising cases linked to chronic infections and environmental factors. Advances in targeted therapies and minimally invasive surgical techniques are expanding treatment options for squamous cell carcinoma. In addition, research into combination immunotherapy regimens is providing promising outcomes, attracting greater clinical adoption. Emerging healthcare markets are seeing increasing diagnostic capabilities, which is contributing to early detection and treatment uptake for this subtype.

- By Grade Type

On the basis of grade type, the market is segmented into low-grade bladder tumor, high-grade bladder tumor, and others. The high-grade bladder tumor segment dominated the market in 2025, owing to the aggressive nature of the disease and the high need for intensive treatment. High-grade tumors require advanced therapeutic interventions such as radical cystectomy, intravesical therapies, and immunotherapy, driving significant market demand. Hospitals and specialized oncology centers often focus on comprehensive treatment protocols for high-grade cases to improve survival rates. The prevalence of recurrent and invasive high-grade bladder tumors ensures continuous demand for innovative therapies. Patient monitoring, early detection, and supportive care programs also contribute to the sustained dominance of this segment.

The low-grade bladder tumor segment is projected to witness the fastest growth during the forecast period due to rising awareness of early diagnosis and minimally invasive treatment options. Advancements in laser therapy, intravesical chemotherapy, and surveillance protocols enable effective management of low-grade tumors with reduced complications. Increasing implementation of screening programs and cystoscopy techniques is supporting the early detection of low-grade tumors. Growing patient preference for conservative and organ-preserving treatments further drives adoption in this segment.

- By Treatment

On the basis of treatment, the market is segmented into surgery, chemotherapy, radiation therapy, immunotherapy, and others. The immunotherapy segment dominated the bladder cancer treatment market with a market share of 41.7% in 2025, driven by its superior efficacy, reduced side effects compared to conventional chemotherapy, and growing adoption in advanced and recurrent bladder cancer cases. Immunotherapy, including immune checkpoint inhibitors such as pembrolizumab and atezolizumab, is increasingly being integrated into first-line and second-line treatment protocols, improving patient survival rates and quality of life. Hospitals and specialized oncology centers favor immunotherapy due to clinical guidelines supporting its use for high-grade and metastatic tumors. In addition, ongoing clinical trials and combination regimens with chemotherapy or targeted therapies are further expanding its applicability. Patient awareness and physician preference for personalized treatment approaches also reinforce the dominance of this segment.

The surgery segment is expected to witness the fastest growth during the forecast period due to continuous advancements in minimally invasive and robotic-assisted procedures. Surgical interventions, including radical and partial cystectomy, remain critical for localized tumors, and improved surgical techniques are reducing recovery time and complications. Rising investments in hospital infrastructure, availability of skilled surgeons, and patient preference for definitive treatment contribute to the rapid growth of this segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The parenteral segment dominated the market in 2025, as most chemotherapeutic agents, immunotherapies, and targeted therapies are administered intravenously in hospitals or specialized clinics. Parenteral administration ensures precise dosing, rapid bioavailability, and direct therapeutic efficacy, which is crucial for aggressive or high-grade tumors. Oncology centers and hospital pharmacies focus on parenteral therapies due to clinical guidelines and standardized treatment protocols. The availability of advanced infusion systems and patient monitoring capabilities further supports the dominance of this segment.

The oral segment is projected to witness the fastest growth during the forecast period due to the development of oral targeted therapies and small-molecule drugs. Oral medications provide the convenience of at-home administration and improved patient adherence, which is particularly beneficial for long-term maintenance therapy. Pharmaceutical companies are investing in oral formulations of existing drugs to expand treatment accessibility. Increasing patient preference for non-invasive administration and telemedicine-enabled monitoring also contributes to the rapid adoption of oral therapies.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated the market in 2025, as most bladder cancer treatments, including immunotherapy, chemotherapy, and parenteral therapies, are administered under medical supervision. Hospitals and oncology centers provide specialized care, infusion facilities, and patient monitoring, making hospital pharmacies the primary point of distribution. Clinical guidelines, insurance coverage, and reimbursement policies favor hospital-based treatment, reinforcing the dominance of this channel. Hospitals also act as hubs for clinical trials and expanded access programs, further supporting this segment’s market share.

The retail pharmacy segment is expected to witness the fastest growth during the forecast period due to the increasing availability of oral medications and supportive care drugs for bladder cancer patients. Retail pharmacies offer convenient access to maintenance therapy, symptom management, and post-discharge medications. Rising awareness, patient education programs, and e-pharmacy platforms are accelerating adoption in both developed and emerging markets. In addition, government initiatives to improve access to essential cancer medications are further strengthening the growth of this segment.

Bladder Cancer Treatment Market Regional Analysis

- North America dominated the bladder cancer treatment market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key pharmaceutical and biotech players

- Patients and healthcare providers in the region highly value early diagnosis, personalized treatment approaches, and access to state-of-the-art therapies such as immune checkpoint inhibitors and minimally invasive surgical techniques

- This widespread adoption is further supported by well-established oncology centers, robust clinical research programs, and favorable reimbursement policies, establishing North America as the leading market for bladder cancer treatments in both hospital and outpatient settings.

U.S. Bladder Cancer Treatment Market Insight

The U.S. bladder cancer treatment market captured the largest revenue share of 80% in 2025 within North America, fueled by advanced healthcare infrastructure, high patient awareness, and the rapid adoption of immunotherapies and targeted therapies. Patients are increasingly prioritizing early diagnosis and personalized treatment approaches. The growing preference for minimally invasive surgical techniques, combination therapies, and outpatient treatment programs further propels the market. Moreover, the integration of biomarker testing and precision medicine in oncology practices is significantly contributing to the market's expansion.

Europe Bladder Cancer Treatment Market Insight

The Europe bladder cancer treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising prevalence of bladder cancer and the availability of advanced therapeutic options. Increasing urbanization, healthcare investments, and government-backed cancer awareness initiatives are fostering the adoption of bladder cancer treatments. European patients and oncologists are also drawn to therapies offering improved efficacy and reduced side effects. The region is experiencing significant growth across hospital, outpatient, and specialized oncology applications, with treatments being incorporated into both early-stage and advanced cancer care protocols.

U.K. Bladder Cancer Treatment Market Insight

The U.K. bladder cancer treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of early detection and a growing preference for personalized therapy. Concerns regarding recurrence and invasive disease are encouraging both patients and healthcare providers to choose advanced treatment options such as immunotherapy and minimally invasive surgery. The U.K.’s well-established oncology infrastructure, alongside strong government and private healthcare support, is expected to continue to stimulate market growth.

Germany Bladder Cancer Treatment Market Insight

The Germany bladder cancer treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by rising patient awareness, advanced clinical facilities, and the demand for precision medicine. Germany’s robust healthcare system, combined with its emphasis on innovation and research, promotes the adoption of novel therapies, particularly immunotherapy and targeted therapy. Integration of advanced diagnostics with treatment planning is also becoming increasingly prevalent, with a strong preference for effective, evidence-based solutions aligning with local healthcare standards.

Asia-Pacific Bladder Cancer Treatment Market Insight

The Asia-Pacific bladder cancer treatment market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing prevalence of bladder cancer, rising healthcare expenditure, and improving medical infrastructure in countries such as China, Japan, and India. The region's growing inclination toward early diagnosis, supported by government initiatives promoting cancer awareness, is driving the adoption of advanced therapies. Furthermore, as APAC emerges as a hub for clinical research and healthcare innovation, the accessibility and affordability of bladder cancer treatments are expanding to a wider patient population.

Japan Bladder Cancer Treatment Market Insight

The Japan bladder cancer treatment market is gaining momentum due to the country’s aging population, high-tech healthcare infrastructure, and demand for advanced oncology therapies. The Japanese market places significant emphasis on early detection and personalized care, and the adoption of immunotherapy and minimally invasive surgical interventions is increasing rapidly. Integration of diagnostic technologies, such as biomarker-based testing, with treatment planning is fueling growth. Moreover, Japan’s focus on patient safety and quality of care is likely to spur demand for effective and less toxic therapies in both hospital and outpatient settings.

India Bladder Cancer Treatment Market Insight

The India bladder cancer treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, increasing awareness of cancer care, and rapid improvements in healthcare infrastructure. India is emerging as a key market for advanced oncology therapies, and bladder cancer treatments are becoming increasingly accessible across hospitals, specialty clinics, and urban centers. Government initiatives promoting cancer screening, the growing prevalence of private healthcare facilities, and increasing affordability of advanced therapies are key factors propelling market growth in India.

Bladder Cancer Treatment Market Share

The Bladder Cancer Treatment industry is primarily led by well-established companies, including:

- AstraZeneca (U.K.)

- Bristol Myers Squibb Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- F. Hoffmann La Roche Ltd. (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Ferring Pharmaceuticals (Switzerland)

- Seagen Inc. (U.S.)

- UroGen Pharma Ltd. (Israel)

- ImmunityBio, Inc. (U.S.)

- CG Oncology, Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Ipsen S.A. (France)

- Amgen Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

What are the Recent Developments in Global Bladder Cancer Treatment Market?

- In November 2025, the U.S. Food and Drug Administration approved pembrolizumab (Keytruda) or pembrolizumab QLEX in combination with enfortumab vedotin‑ejfv (Padcev) as a neoadjuvant and adjuvant treatment for adults with muscle‑invasive bladder cancer (MIBC) who are ineligible for cisplatin‑based chemotherapy, marking a new perioperative regimen and potential standard of care that significantly improves survival outcomes

- In June 2025, the U.S. Food and Drug Administration approved UroGen Pharma’s gel‑based chemotherapy drug Zusduri for non‑muscle invasive bladder cancer (NMIBC), offering a non‑surgical alternative that showed 78% complete response rates in late‑stage clinical trials and expanding treatment options for recurrent disease

- In April 2025, the U.S. National Health Service (NHS) in England began offering an enfortumab vedotin and pembrolizumab combination therapy that clinical evidence showed could nearly double survival for patients with advanced bladder cancer, representing a significant therapeutic advancement available to more than 1,000 patients annually

- In April 2024, the U.S. FDA approved Anktiva (nogapendekin alfa inbakicept), a first‑in‑class IL‑15 receptor agonist, for use with Bacillus Calmette‑Guérin (BCG) in BCG‑unresponsive non‑muscle invasive bladder cancer, introducing a novel immune‑stimulating approach tailored to a high‑risk patient subset

- In December 2023, the U.S. FDA approved the combination of enfortumab vedotin (Padcev) and pembrolizumab (Keytruda) for the treatment of locally advanced or metastatic urothelial bladder cancer, demonstrating statistically significant improvements in overall survival and progression‑free survival compared with platinum‑based chemotherapy and expanding first‑line treatment options

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.