Middle East And Africa Healthcare It Integration Market

Taille du marché en milliards USD

TCAC :

%

USD

128.86 Million

USD

290.60 Million

2025

2033

USD

128.86 Million

USD

290.60 Million

2025

2033

| 2026 –2033 | |

| USD 128.86 Million | |

| USD 290.60 Million | |

| % | |

Middle East & Africa Healthcare Information Technology (IT) Integration Market, By Product & Services (Product, and Services), Application (Medical Device Integration, Internal Integration, Hospital Integration, Lab Integration, Clinics Integration, and Radiology Integration), Facility Size (Large, Medium, and Small), Purchase Mode (Group Purchase Organization, and Individual), End User (Hospitals, Laboratory, Diagnostic Centers, Radiology Centers, and Clinics), Industry Trends and Forecast to 2029.

Middle East and Africa Healthcare Information Technology (IT) Integration Market Analysis and Size

Healthcare IT integration enables it for healthcare systems to gather data, exchange it with the cloud, and communicate with one another, allowing for the rapid and correct analysis of that data. The Internet of Things (IoT) combines sensor output with communications to provide tasks that were until recently thought of as notional, from monitoring and diagnosis to delivery methods. The sensors can be incorporated into a device, cloud-based, or wearable. With the developments of such sensors and ICT, the healthcare sector now possesses a dynamic collection of patient data that can be used to support diagnostics and preventive care and to assess the likely success of preventive treatment.

In addition, Integration initiatives are often limited in scope. They integrate only a small portion of patient data available because it is difficult to move information among disparate clinical and business software applications within and beyond healthcare enterprise borders. It requires a thorough understanding of data governance, expert knowledge of health messaging standards, access to sophisticated technology, and expertise in systems integration, including service-oriented architecture (SOA) and enterprise architecture management (EAM). CGI’s HIIF defines and describes all the parameters necessary to achieve the integration that healthcare organizations require.

However, the higher costs associated with integrated IT solutions and issues associated with interoperability are anticipated to restrain the market growth.

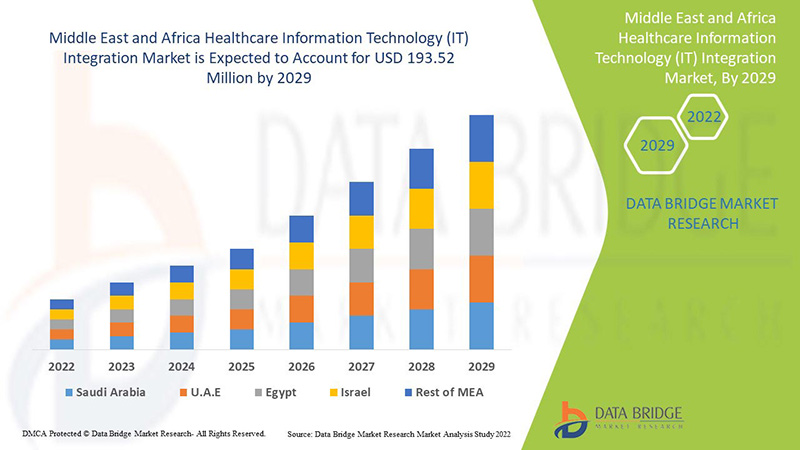

Data Bridge Market Research analyzes that the Middle East & Africa healthcare information technology (IT) integration market is expected to reach the value of USD 193.52 million by 2029, at a CAGR of 10.7% during the forecast period. Product and services account for the largest type segment in the market due to the rapid demand for IT solutions and services in the Middle East & Africa. This market report also covers pricing analysis, patent analysis, and technological advancements in depth.

|

Report Metric |

Details |

|

Forecast Period |

2022 to 2029 |

|

Base Year |

2021 |

|

Historic Years |

2020 (Customizable to 2019 - 2014) |

|

Quantitative Units |

Revenue in USD Million, Volumes in Units, Pricing in USD |

|

Segments Covered |

By Product & Services (Product, and Services), Application (Medical Device Integration, Internal Integration, Hospital Integration, Lab Integration, Clinics Integration, and Radiology Integration), Facility Size (Large, Medium, and Small), Purchase Mode (Group Purchase Organization, and Individual), End User (Hospitals, Laboratory, Diagnostic Centers, Radiology Centers, and Clinics). |

|

Countries Covered |

UAE, Israel, South Africa, Saudi Arabia, Egypt, and Rest of the Middle East and Africa. |

|

Market Players Covered |

Lyniate, Redox, Inc., carepoint health, Nextgen Healthcare Inc., Interfaceware, Inc. Koninklijke Philips, Oracle, AVI-SPL, INC., Allscripts Healthcare solutions, Inc, Epic systems corporation, Qualcomm life Inc., Capsule technologies Inc. Orion health, Quality syetems, Inc., Cerner corporation, Intersystems corporation, Infor Inc., GE Healthcare, MCKESSON Corporation, and Meditech, among others. |

Middle East & Africa Healthcare Information Technology (IT) Integration Market Definition

Health IT integration (health information technology) is the area of IT involving the design, development, creation, use, and maintenance of information systems for the healthcare industry. Automated and interoperable healthcare information systems will continue to improve medical care and public health, lower costs, increase efficiency, reduce errors and improve patient satisfaction, and optimize reimbursement for ambulatory and inpatient healthcare providers. The importance of health IT results from the combination of evolving technology and changing government policies that influence the quality of patient care. Some of the healthcare information technology (IT) integration products are interface/integration engines, medical device integration software, and media integration solutions, and services are implementation & integration, support & maintenance, training & education, and consulting. Health IT makes it possible for health care providers to better manage patient care through the secure use and sharing of health information. By developing secure and private electronic health records for most Americans and making health information available electronically when and where it is needed, health IT can improve the quality of care, even as it makes health care more cost-effective. With the help of health IT, health care providers will have: Accurate and complete information about a patient's health. That way, providers can give the best possible care, whether during a routine visit or a medical emergency, The ability to better coordinate the care given. This is especially important if a patient has a serious medical condition, a way to securely share information with patients and their family caregivers over the Internet, for patients who opt for this convenience.

In addition, the rapid adoption of electronic health records and other healthcare IT solutions is one of the high-impact rendering drivers of the market. Moreover, the urgent need to integrate patient data into healthcare systems and favorable government policies, funding programs, and initiatives to deploy healthcare IT integration solutions are the major drivers for the market growth.

Middle East & Africa Healthcare Information Technology (IT) Integration Market Dynamics

This section deals with understanding the market drivers , opportunities, restraints, and challenges. All of this is discussed in detail as below:

Drivers

- Rapid Adoption of Electronic Health Records and Other Healthcare IT Solutions

Patient data is complex, confidential, and often unstructured. Incorporating this information into the healthcare delivery process is a challenge that must be met in order to realize the opportunity to improve patient care. Although Electronic Health Record (HER) has been in use for over a decade, the market has recently accelerated due to government initiatives in different countries to improve patient data security.

Regulatory requirements imposed by HITECH have spurred the adoption of EHR and EMR. Another important factor, which is fueling the growth of the market is the increasing number of Responsible Care Organizations (ACOs), increasing the demand for EHRs and EMRs.

Government initiatives in other countries, such as Denmark, Sweden, France, and Canada, are also encouraging the adoption of EHRs and mandating their meaningful use to control healthcare costs.

In addition, IT services help to integrate various end-users throughout the healthcare system, including hospitals, nursing units, pharmacies, and health insurance companies. However, integrating this data and its availability in real-time is essential for healthcare professionals to ensure effective decision-making. Therefore, with the anticipated growth of the EHR systems in the coming years, hospitals will focus strongly on enhancing their capacity by integrating different hospital systems with EHR, thereby creating development opportunities for the healthcare information technology (IT) integration market.

- Growing Demand For Telehealth Services and Remote Patient Monitoring Solutions

Currently, telehealth services are being requested for monitoring and consulting purposes. Advances in healthcare solutions have helped to deliver educational content and ensure uninterrupted communication between patients and healthcare providers. The successful operation of remote patient monitoring solutions depends on the successful integration of medical and Information and Communications Technology (ICT) devices that enable the delivery of medical services over long distances.

Since doctors and nurses spend most of their time working without computers in hospitals, it is difficult for them to carry patient records with them on the go. As a result, many market players have started offering mobile platforms, such as mobile apps, for healthcare IT solutions.

Advances in computing have provided an ever-expanding array of options such as advanced broadband, mobile and networking, remote patient monitoring, high-definition video conferencing, and EHR. This has created significant opportunities for solution providers to integrate healthcare information technology. Through an IoT healthcare network consisting of connected medical devices, patients sitting at home can be remotely monitored for their vital signs, such as blood pressure levels, weight, blood glucose level, electrocardiogram, and body temperature, as patient data is automatically sent to the nurse or a doctor.

A connected healthcare environment allows doctors to remotely monitor and adjust a patient's condition. Connected health technologies involve smart sensor technology, advanced connectivity, interface enhancements, and data analytics. These advances help reduce healthcare costs by improving patient acceptance and reducing clinic visits. Additionally, while implementation costs can be high, these technologies are helping to speed up operations for many businesses.

With advancements in technology, these solutions play an important role in improving remote monitoring and patient compliance, and subsequently, their quality of life. Therefore, the growing demand for remote monitoring solutions and remote devices is expected to drive the growth of the Middle East & Africa healthcare information technology (IT) integration solution providers in the coming years.

Restraint

- Issues Associated With Interoperability

The heterogeneity of health information systems possesses major challenges for the successful implementation and use of health informatics solutions. Many countries do not have specific IT standards for storing and exchanging data, which leads to interoperability issues. While there are many different data storage, transport, and security standards, implementing and integrating these interoperability standards presents a major challenge for care providers, and health and medical IT solution providers. Due to the lack of a single health information system to meet all the administrative, clinical, technical, and laboratory requirements of major healthcare providers, interoperability requirements and interoperability standards have become important. Vendors also follow different data formats and standards due to poor knowledge or lack of technical knowledge of the defined standards, which makes it difficult to share real-time data with partner systems, which increases the cost of healthcare IT integration. Issues with data quality and integrity, non-compliance with established standards, lack of qualified professionals, and variation in uptime between healthcare providers are among the issues acting as major obstacles to implementing a fully interoperable healthcare IT infrastructure. These factors are expected to restrain the growth of the market.

Opportunity/ Challenges

- Data Integration Related Challenges

Information related to patients have created from different departments. At all points of treatment within the healthcare organization, making it a more highly information-intensive industry and reliable patient records, however, it is essential to give reliable information by combining huge amounts of data in order to produce comprehensive and trustworthy patient records because a variety of medical equipment and diagnostic instruments are used in healthcare systems and is a growing need to connect all of these systems to assist healthcare practitioners in responding quickly at various care delivery points.

Several information management applications, including asset management systems, imaging systems, email management systems, forms management systems, clinical information systems, workforce management systems, database management systems, content management systems, revenue cycle management systems, clinical and non-clinical workflow systems, and customer relations management systems that, have been invested in by numerous healthcare organizations. As healthcare organizations are increasingly adopting various healthcare IT systems, there is a greater need to integrate different types of IT systems into the IT architecture of the organization to ensure the optimum utilization of these systems and aid in accurate decision-making. The successful combination of healthcare IT systems with other systems is a focus of IT infrastructure development projects in healthcare organizations.

Thus, each organization in healthcare uses different systems, and there is a high chance of misdiagnosis and improper examination of the report due to the data integration that demolishes the usage of healthcare information technology, which can act as a challenge to the market growth.

Post-COVID-19 Impact On Middle East & Africa Healthcare Information Technology (IT) Integration Market

The COVID-19 outbreak had a drastic effects on the Middle East & Africa healthcare, with the UK amongst the countries most severely impacted. Due to the COVID-19 outbreak, all healthcare clinics are under immense pressure, and healthcare facilities worldwide have been overcrowded by the daily visits of numerous patients. The rising prevalence of coronavirus disease has driven the demand for accurate diagnosis and treatment devices in several countries worldwide. In this regard, connected care technologies have proven to be very helpful. They allow healthcare providers to monitor patients using digitally connected noninvasive devices such as home blood pressure monitors and pulse oximeters. Moreover, the rapid spread of this disease in the Middle East & Africa has led to a shortage of hospital beds and healthcare workers. As a result, connected medical devices were increasingly adopted to monitor vital signs, and a similar trend is likely to be observed in the coming years

Manufacturers are making various strategic decisions to bounce back post-COVID-19. The players are conducting multiple R&D activities and product launches, and strategic partnerships to improve the technology and test results involved in the pharmacogenetics testing market.

Recent Developments

- In August 2022, Cognizant announced that it has been selected by AXA UK & Ireland as a technology partner to help consolidate, modernize and manage part of its IT operations. AXA UK & Ireland is transforming its technology ecosystem to create a more digitally-enabled, modern, and agile IT environment that is data-rich, secure, and sustainable with lower overall cost. Cognizant will provide integrated IT services spanning service desk support and maintenance, end-user computing, application development and maintenance, cloud operations, and IT infrastructure management. This has helped the company to expand its business.

- In July 2022, NXGN Management, LLC, have demonstrated its award-winning NextGen Office, the only Electronic Health Record (EHR) integrated into the American Podiatric Medical Association (APMA) Registry, at the group’s annual conference held on July 28 to 31 in Orlando. NextGen Healthcare is a founding partner of the APMA Registry, which provided clinically relevant insights to NextGen Healthcare clients. This has helped the company to show its products in APMA and get recognition.

Middle East & Africa Healthcare Information Technology (IT) Integration Market Scope

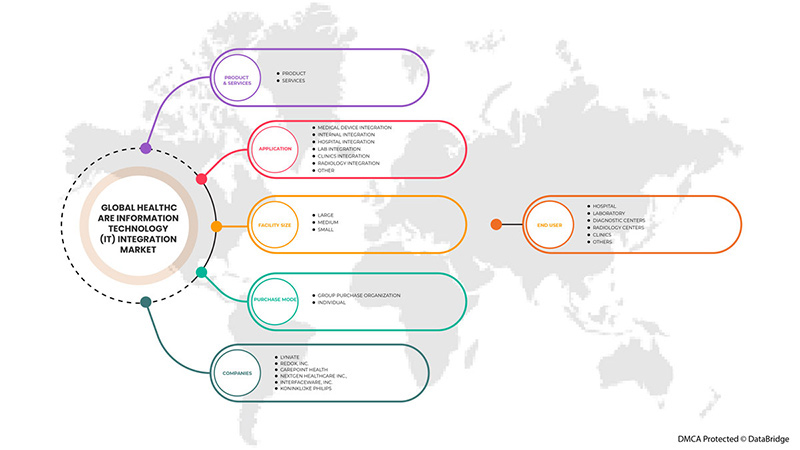

Middle East & Africa healthcare information technology (IT) integration market is segmented into product & services, application, facility size, purchase mode, and end user. The growth among segments helps you analyze niche pockets of growth and strategies to approach the market and determine your core application areas and the difference in your target markets.

By Product & Services

- Product

- Services

On the basis of product & services, the Middle East & Africa healthcare information technology (IT) integration market is segmented into products, and services.

By Applications

- Medical Device Integration

- Internal Integration

- Hospital Integration

- Lab Integration

- Clinics Integration

- Radiology Integration

- Other

On the basis of application, the Middle East & Africa healthcare information technology (IT) integration market is segmented into medical device integration, internal integration, hospital integration, lab integration, clinics integration, radiology integration and others.

By Facility Size

- Large

- Medium

- Small

On the basis of facility size, the Middle East & Africa healthcare information technology (IT) integration market is segmented into large, medium, and small.

By Purchase Mode

- Group Purchase Organization

- Individual

On the basis of purchase mode, the Middle East & Africa healthcare information technology (IT) integration market is segmented into group purchases, and individual.

By End User

- Hospital

- Laboratory

- Diagnostic Centers

- Radiology Centers

- Clinics

- Others

On the basis of end users, the Middle East & Africa healthcare information technology (IT) integration market is segmented into hospitals, laboratories, diagnostic centers, radiology centers, clinics, and others.

Middle East & Africa Healthcare Information Technology (IT) Integration Market Regional Analysis/Insights

The Middle East & Africa healthcare information technology (IT) integration market is analyzed. Market size information is provided by product & services, application, facility size, purchase mode, and end user.

The countries covered in this market report are South Africa, Saudi Arabia, Egypt, and rest of the Middle East and Africa.

In 2022, Middle East & Africa is dominating due to the rise in government initiatives and R&D. South Africa is expected to grow due to the rise in technological advancement in healthcare IT.

The country section of the report also provides individual market-impacting factors and changes in regulation in the market domestically that impact the current and future trends of the market. Data points such as new sales, replacement sales, country demographics, regulatory acts, and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Middle East & Africa brands and their challenges faced due to large or scarce competition from local and domestic brands, and the impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Middle East & Africa Healthcare Information Technology (IT) Integration Market Share Analysis

Middle East & Africa healthcare information technology (IT) integration market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product trials pipelines, product approvals, patents, product width and breath, application dominance, technology lifeline curve. The above data points are only related to the company’s focus on the Middle East & Africa healthcare information technology (IT) integration market.

Some of the major players operating in the Middle East & Africa healthcare information technology (IT) integration market are Lyniate, Redox, Inc., carepoint health, Nextgen Healthcare Inc., Interfaceware, Inc., Koninklijke Philips, Oracle, AVI-SPL, INC., Allscripts Healthcare solutions, Inc, Epic systems corporation, Qualcomm life Inc., Capsule technologies Inc., Orion health, Quality syetems, Inc., Cerner corporation, Intersystems corporation, Infor Inc., GE Healthcare, MCKESSON Corporation, and Meditech, among others.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

1 INTRODUCTION

1.1 OBJECTIFS DE L'ÉTUDE

1.2 DÉFINITION DU MARCHÉ

1.3 APERÇU DU MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE

1.4 MONNAIE ET TARIFS

1.5 LIMITATIONS

1.6 MARCHÉS COUVERTS

2 SEGMENTATION DU MARCHÉ

2.1 MARCHÉS COUVERTS

2.2 PORTÉE GÉOGRAPHIQUE

2,3 ANS CONSIDÉRÉS POUR L'ÉTUDE

2.4 MODÈLE DE VALIDATION DES DONNÉES DU TRÉPIED DBMR

2.5 ENTRETIENS PRIMAIRES AVEC DES LEADERS D'OPINION CLÉS

2.6 MODÉLISATION MULTIVARIÉE

2.7 GRILLE DE COUVERTURE DES APPLICATIONS DU MARCHÉ

2.8 COURBE DE VIE DES PRODUITS ET SERVICES

2.9 GRILLE DE POSITIONNEMENT DU MARCHÉ DBMR

2.1 ANALYSE DE LA PART DES FOURNISSEURS

2.11 SOURCES SECONDAIRES

2.12 HYPOTHÈSES

3 RÉSUMÉ EXÉCUTIF

4 PREMIUM INSIGHT

4.1 TECHNOLOGIES INFORMATIQUES POTENTIELLES DANS LE DOMAINE DE LA SANTÉ

4.1.1 DSE

4.1.2 DME

4.1.3 INTELLIGENCE ARTIFICIELLE

4.1.4 TÉLÉMÉDECINE

5 ANALYSE DES PARTS DE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE-

6 RÈGLEMENTS

7 APERÇU DU MARCHÉ

7.1 PILOTES

7.1.1 ADOPTION RAPIDE DES DOSSIERS DE SANTÉ ÉLECTRONIQUES ET D'AUTRES SOLUTIONS INFORMATIQUES DE SANTÉ

7.1.2 DEMANDE CROISSANTE DE SERVICES DE TÉLÉSANTÉ ET DE SOLUTIONS DE SURVEILLANCE À DISTANCE DES PATIENTS

7.1.3 BESOIN CROISSANT DE SERVICES DE TÉLÉSANTÉ DANS L'ENSEMBLE DU SECTEUR DE LA SANTÉ

7.2 RESTRICTIONS

7.2.1 PROBLÈMES LIÉS À L'INTEROPÉRABILITÉ

7.2.2 COÛTS ÉLEVÉS ASSOCIÉS AUX SOLUTIONS INFORMATIQUES INTÉGRÉES

7.3 OPPORTUNITÉS

7.3.1 DÉCISIONS MÉDICALES PRÉCOCES ET SOUTIEN À LA DÉCISION CLINIQUE

7.3.2 UNIFORMITÉ DES DONNÉES ET ÉCHANGE DE DONNÉES STANDARDISÉ

7.3.3 SENSIBILISATION ACCRUE DES GENS

7.4 DÉFIS

7.4.1 DÉFIS LIÉS À L'INTÉGRATION DES DONNÉES

7.4.2 AUGMENTATION DES FRAUDES DANS LE DOMAINE DE LA SANTÉ

8 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR PRODUITS ET SERVICES

8.1 APERÇU

8.2 SERVICES

8.2.1 SUPPORT ET MAINTENANCE

8.2.2 MISE EN ŒUVRE ET INTÉGRATION

8.2.3 FORMATION ET ÉDUCATION

8.2.4 CONSEIL

8.3 PRODUIT

8.3.1 MOTEURS D'INTERFACE/D'INTÉGRATION

8.3.1.1 ORGANISATION D'ACHAT GROUPÉ

8.3.1.2 INDIVIDUEL

8.3.2 LOGICIEL D'INTÉGRATION DE DISPOSITIFS MÉDICAUX

8.3.2.1 ORGANISATION D'ACHAT GROUPÉ

8.3.2.2 INDIVIDUEL

8.3.3 SOLUTIONS D'INTÉGRATION MÉDIA

8.3.3.1 ORGANISATION D'ACHAT GROUPÉ

8.3.3.2 INDIVIDUEL

8.3.4 AUTRES OUTILS D'INTÉGRATION

9 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR APPLICATION

9.1 APERÇU

9.2 INTÉGRATION DES DISPOSITIFS MÉDICAUX

9.3 INTÉGRATION HOSPITALIÈRE

9.4 INTÉGRATION INTERNE

9.5 INTÉGRATION DE LA RADIOLOGIE

9.6 INTÉGRATION DU LABORATOIRE

9.7 INTÉGRATION DES CLINIQUES

9.8 AUTRES

10 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR TAILLE D'ÉTABLISSEMENT

10.1 APERÇU

10.2 GRAND

10.3 MOYEN

10.4 PETIT

11 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR MODE D'ACHAT

11.1 APERÇU

11.2 ORGANISATION D'ACHAT GROUPÉ

11.3 INDIVIDUEL

12 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR UTILISATEUR FINAL

12.1 APERÇU

12.2 HÔPITAL

12.3 CENTRES DE DIAGNOSTIC

12.4 CENTRES DE RADIOLOGIE

12.5 LABORATOIRE

12.6 CLINIQUES

12.7 AUTRES

13 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR RÉGION

13.1 MOYEN-ORIENT ET AFRIQUE

13.1.1 AFRIQUE DU SUD

13.1.2 ARABIE SAOUDITE

13.1.3 Émirats arabes unis

13.1.4 ÉGYPTE

13.1.5 ISRAËL

13.1.6 RESTE DU MOYEN-ORIENT ET DE L'AFRIQUE

14 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAYSAGE DES ENTREPRISES

14.1 ANALYSE DES ACTIONS DE L'ENTREPRISE : MOYEN-ORIENT ET AFRIQUE

15 ANALYSE SWOT

16 PROFIL DE L'ENTREPRISE

16.1 FOURNISSEURS DE DME

16.2 ALLSCRIPTS HEALTHCARE, LLC ET/OU SES FILIALES.

16.2.1 INSTANTANÉ DE L'ENTREPRISE

16.2.2 ANALYSE DES REVENUS

16.2.3 PORTEFEUILLE DE PRODUITS

16.2.4 ÉVOLUTIONS RÉCENTES

16.3 NXGN MANAGEMENT, LLC

16.3.1 INSTANTANÉ DE L'ENTREPRISE

16.3.2 ANALYSE DES REVENUS

16.3.3 PORTEFEUILLE DE PRODUITS

16.3.4 ÉVOLUTIONS RÉCENTES

16.4 EPIC SYSTEMS CORPORATION

16.4.1 INSTANTANÉ DE L'ENTREPRISE

16.4.2 ANALYSE DES ACTIONS DE L'ENTREPRISE

16.4.3 PORTEFEUILLE DE PRODUITS

16.4.4 ÉVOLUTION RÉCENTE

16.5 TECHNOLOGIE DE L'INFORMATION MÉDICALE, INC.

16.5.1 INSTANTANÉ DE L'ENTREPRISE

16.5.2 PORTEFEUILLE DE PRODUITS

16.5.3 ÉVOLUTIONS RÉCENTES

16.6 FOURNISSEURS D'INTÉGRATION

16.7 INFOR.

16.7.1 INSTANTANÉ DE L'ENTREPRISE

16.7.2 PORTEFEUILLE DE PRODUITS

16.7.3 ÉVOLUTION RÉCENTE

16.8 LYNIATE

16.8.1 INSTANTANÉ DE L'ENTREPRISE

16.8.2 PORTEFEUILLE DE PRODUITS

16.8.3 ÉVOLUTIONS RÉCENTES

16,9 QVERA

16.9.1 INSTANTANÉ DE L'ENTREPRISE

16.9.2 PORTEFEUILLE DE PRODUITS

16.9.3 ÉVOLUTIONS RÉCENTES

16.1 INTERSYSTEM CORPORATION

16.10.1 INSTANTANÉ DE L'ENTREPRISE

16.10.2 PORTEFEUILLE DE PRODUITS

16.10.3 ÉVOLUTIONS RÉCENTES

16.11 SOINS DE SANTÉ ÉLECTRIQUES GÉNÉRAUX

16.11.1 INSTANTANÉ DE L'ENTREPRISE

16.11.2 ANALYSE DES REVENUS

16.11.3 ANALYSE DES ACTIONS DE LA SOCIÉTÉ

16.11.4 PORTEFEUILLE DE PRODUITS

16.11.5 ÉVOLUTIONS RÉCENTES

16.12 INTERFACEWARE INC.

16.12.1 INSTANTANÉ DE L'ENTREPRISE

16.12.2 PORTEFEUILLE DE PRODUITS

16.12.3 ÉVOLUTIONS RÉCENTES

16.13 GROUPE DE SANTÉ ORION

16.13.1 INSTANTANÉ DE L'ENTREPRISE

16.13.2 ANALYSE DES REVENUS

16.13.3 PORTEFEUILLE DE PRODUITS

16.13.4 ÉVOLUTIONS RÉCENTES

16.14 IBM (2021)

16.14.1 INSTANTANÉ DE L'ENTREPRISE

16.14.2 ANALYSE DES REVENUS

16.14.3 ANALYSE DES ACTIONS DE LA SOCIÉTÉ

16.14.4 PORTEFEUILLE DE PRODUITS

16.14.5 ÉVOLUTIONS RÉCENTES

16.15 SUMMIT HEALTHCARE SERVICES, INC.

16.15.1 INSTANTANÉ DE L'ENTREPRISE

16.15.2 PORTEFEUILLE DE PRODUITS

16.15.3 ÉVOLUTIONS RÉCENTES

16.16 MASIMO (2021)

16.16.1 INSTANTANÉ DE L'ENTREPRISE

16.16.2 ANALYSE DES REVENUS

16.16.3 PORTEFEUILLE DE PRODUITS

16.16.4 ÉVOLUTION RÉCENTE

16.17 SOLUTIONS MDI

16.17.1 INSTANTANÉ DE L'ENTREPRISE

16.17.2 PORTEFEUILLE DE PRODUITS

16.17.3 ÉVOLUTIONS RÉCENTES

16.18 CONSCIENT

16.18.1 INSTANTANÉ DE L'ENTREPRISE

16.18.2 ANALYSE DES REVENUS

16.18.3 PORTEFEUILLE DE PRODUITS

16.18.4 ÉVOLUTIONS RÉCENTES

16.19 SIEMENS HEALTHCARE GMBH

16.19.1 INSTANTANÉ DE L'ENTREPRISE

16.19.2 ANALYSE DES REVENUS

16.19.3 ANALYSE DES ACTIONS DE LA SOCIÉTÉ

16.19.4 PORTEFEUILLE DE PRODUITS

16.19.5 ÉVOLUTIONS RÉCENTES

16.2 REDOX, INC.

16.20.1 INSTANTANÉ DE L'ENTREPRISE

16.20.2 PORTEFEUILLE DE PRODUITS

16.20.3 ÉVOLUTIONS RÉCENTES

16.21 LES DEUX FOURNISSEURS

16.22 ORACLE (2021)

16.22.1 INSTANTANÉ DE L'ENTREPRISE

16.22.2 ANALYSE DES REVENUS

16.22.3 ANALYSE DES ACTIONS DE LA SOCIÉTÉ

16.22.4 PORTEFEUILLE DE PRODUITS

16.22.5 ÉVOLUTIONS RÉCENTES

16.23 KONNKLIJKE PHILIPS NV (2021)

16.23.1 INSTANTANÉ DE L'ENTREPRISE

16.23.2 ANALYSE DES REVENUS

16.23.3 PORTEFEUILLE DE PRODUITS

16.23.4 ÉVOLUTIONS RÉCENTES

17 QUESTIONNAIRE

18 RAPPORTS CONNEXES

Liste des tableaux

TABLEAU 1 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 2 SERVICES DU MOYEN-ORIENT ET DE L'AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) EN MATIÈRE DE SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 3 SERVICES DU MOYEN-ORIENT ET DE L'AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) EN SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 4 PRODUITS DU MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 5 PRODUITS DU MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 6 MOTEURS D'INTERFACE/D'INTÉGRATION AU MOYEN-ORIENT ET EN AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) EN SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 7 MOYEN-ORIENT ET AFRIQUE LOGICIELS D'INTÉGRATION DE DISPOSITIFS MÉDICAUX SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) EN SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 8 SOLUTIONS D'INTÉGRATION DES MÉDIAS AU MOYEN-ORIENT ET EN AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 9 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR APPLICATION, 2020-2029 (EN MILLIONS USD)

TABLEAU 10 MOYEN-ORIENT ET AFRIQUE INTÉGRATION DES DISPOSITIFS MÉDICAUX DANS LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DES SOINS DE SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 11 INTÉGRATION DES HÔPITAUX AU MOYEN-ORIENT ET EN AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LES SOINS DE SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 12 INTÉGRATION INTERNE AU MOYEN-ORIENT ET EN AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 13 INTÉGRATION DE LA RADIOLOGIE DANS LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DES SOINS DE SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 14 INTÉGRATION DES LABORATOIRES AU MOYEN-ORIENT ET EN AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 15 INTÉGRATION DES CLINIQUES DU MOYEN-ORIENT ET DE L'AFRIQUE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LES SOINS DE SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 16 MOYEN-ORIENT ET AFRIQUE AUTRES INTÉGRATION DANS LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LES SOINS DE SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 17 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE, PAR TAILLE D'ÉTABLISSEMENT, 2020-2029 (EN MILLIONS USD)

TABLEAU 18 LE MOYEN-ORIENT ET L'AFRIQUE : GRANDS MARCHÉS DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 19 MOYEN-ORIENT ET AFRIQUE MARCHÉ MOYEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLEAU 20 LE MOYEN-ORIENT ET L'AFRIQUE : PETITS MARCHÉS DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR RÉGION, 2020-2029 (EN MILLIONS USD)

TABLE 21 MIDDLE EAST & AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE, 2020-2029 (USD MILLION)

TABLE 22 MIDDLE EAST & AFRICA GROUP PURCHASE IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 23 MIDDLE EAST & AFRICA INDIVIDUAL IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 24 MIDDLE EAST & AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 25 MIDDLE EAST & AFRICA HOSPITAL IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 26 MIDDLE EAST & AFRICA DIAGNOSTIC CENTRES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 27 MIDDLE EAST & AFRICA RADIOLOGY CENTRES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 28 MIDDLE EAST & AFRICA LABORATORY IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 29 MIDDLE EAST & AFRICA CLINICS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 30 MIDDLE EAST & AFRICA OTHERS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 31 MIDDLE EAST AND AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 32 MIDDLE EAST AND AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 33 MIDDLE EAST AND AFRICA SERVICES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 34 MIDDLE EAST AND AFRICA PRODUCT IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 35 MIDDLE EAST AND AFRICA INTERFACE/INTEGRATION ENGINES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 36 MIDDLE EAST AND AFRICA MEDICAL DEVICE INTEGRATION SOFTWARE IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 37 MIDDLE EAST AND AFRICA MEDIA INTEGRATION SOLUTIONS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 38 MIDDLE EAST AND AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 39 MIDDLE EAST AND AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE, 2020-2029 (USD MILLION)

TABLE 40 MIDDLE EAST AND AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE, 2020-2029 (USD MILLION)

TABLE 41 MIDDLE EAST AND AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 42 SOUTH AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 43 SOUTH AFRICA SERVICES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 44 SOUTH AFRICA PRODUCT IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 45 SOUTH AFRICA INTERFACE/INTEGRATION ENGINES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 46 SOUTH AFRICA MEDICAL DEVICE INTEGRATION SOFTWARE IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 47 SOUTH AFRICA MEDIA INTEGRATION SOLUTIONS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 48 SOUTH AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 49 SOUTH AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE, 2020-2029 (USD MILLION)

TABLE 50 SOUTH AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE, 2020-2029 (USD MILLION)

TABLE 51 SOUTH AFRICA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 52 SAUDI ARABIA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 53 SAUDI ARABIA SERVICES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 54 SAUDI ARABIA PRODUCT IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 55 SAUDI ARABIA INTERFACE/INTEGRATION ENGINES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 56 SAUDI ARABIA MEDICAL DEVICE INTEGRATION SOFTWARE IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 57 SAUDI ARABIA MEDIA INTEGRATION SOLUTIONS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 58 SAUDI ARABIA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 59 SAUDI ARABIA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE, 2020-2029 (USD MILLION)

TABLE 60 SAUDI ARABIA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE, 2020-2029 (USD MILLION)

TABLE 61 SAUDI ARABIA HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLEAU 62 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AUX ÉMIRATS ARABES UNIS, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 63 SERVICES DES EAU SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 64 PRODUITS DES EAU SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 65 MOTEURS D'INTERFACE/D'INTÉGRATION DES EAU SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 66 LOGICIELS D'INTÉGRATION DE DISPOSITIFS MÉDICAUX SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) EN SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 67 SOLUTIONS D'INTÉGRATION DES MÉDIAS AUX ÉMIRATS ARABES UNIS SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 68 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2020-2029 (EN MILLIONS USD)

TABLEAU 69 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AUX ÉMIRATS ARABES UNIS, PAR TAILLE D'ÉTABLISSEMENT, 2020-2029 (EN MILLIONS USD)

TABLEAU 70 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AUX ÉMIRATS ARABES UNIS, PAR MODE D'ACHAT, 2020-2029 (EN MILLIONS USD)

TABLEAU 71 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AUX ÉMIRATS ARABES UNIS, PAR UTILISATEUR FINAL, 2020-2029 (EN MILLIONS USD)

TABLEAU 72 MARCHÉ ÉGYPTIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 73 SERVICES ÉGYPTIENS SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 74 PRODUITS ÉGYPTIENS SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 75 MOTEURS D'INTERFACE/D'INTÉGRATION ÉGYPTIENS SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 76 LOGICIELS D'INTÉGRATION DE DISPOSITIFS MÉDICAUX EN ÉGYPTE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 77 SOLUTIONS D'INTÉGRATION DES MÉDIAS EN ÉGYPTE SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 78 MARCHÉ ÉGYPTIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR APPLICATION, 2020-2029 (EN MILLIONS USD)

TABLEAU 79 MARCHÉ ÉGYPTIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR TAILLE D'ÉTABLISSEMENT, 2020-2029 (EN MILLIONS USD)

TABLEAU 80 MARCHÉ ÉGYPTIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR MODE D'ACHAT, 2020-2029 (EN MILLIONS USD)

TABLEAU 81 MARCHÉ ÉGYPTIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR UTILISATEUR FINAL, 2020-2029 (EN MILLIONS USD)

TABLEAU 82 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ EN ISRAËL, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 83 SERVICES ISRAÉLIENS SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 84 PRODUITS ISRAÉLIENS SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 85 MOTEURS D'INTERFACE/D'INTÉGRATION ISRAÉLIENNES SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 86 LOGICIELS D'INTÉGRATION DE DISPOSITIFS MÉDICAUX EN ISRAËL SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 87 SOLUTIONS D'INTÉGRATION DES MÉDIAS EN ISRAËL SUR LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

TABLEAU 88 MARCHÉ ISRAÉLIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR APPLICATION, 2020-2029 (EN MILLIONS USD)

TABLEAU 89 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ EN ISRAËL, PAR TAILLE D'ÉTABLISSEMENT, 2020-2029 (EN MILLIONS USD)

TABLEAU 90 MARCHÉ ISRAÉLIEN DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR MODE D'ACHAT, 2020-2029 (EN MILLIONS USD)

TABLEAU 91 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ EN ISRAËL, PAR UTILISATEUR FINAL, 2020-2029 (EN MILLIONS USD)

TABLEAU 92 RESTE DU MOYEN-ORIENT ET DE L'AFRIQUE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ, PAR PRODUIT ET SERVICES, 2020-2029 (EN MILLIONS USD)

Liste des figures

FIGURE 1 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : SEGMENTATION

FIGURE 2 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : TRIANGULATION DES DONNÉES

FIGURE 3 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : ANALYSE DROC

FIGURE 4 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : ANALYSE DU MARCHÉ RÉGIONAL ET NATIONAL

FIGURE 5 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : ANALYSE DE LA RECHERCHE DES ENTREPRISES

FIGURE 6 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : DONNÉES DÉMOGRAPHIQUES DES ENTRETIENS

FIGURE 7 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : GRILLE DE COUVERTURE DES APPLICATIONS DU MARCHÉ

FIGURE 8 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : GRILLE DE POSITIONNEMENT DU MARCHÉ DBMR

FIGURE 9 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : ANALYSE DE LA PART DES FOURNISSEURS

FIGURE 10 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : SEGMENTATION

FIGURE 11 LA DEMANDE CROISSANTE DE SOLUTIONS INFORMATIQUES DE SANTÉ, DE SERVICES DE TÉLÉSANTÉ ET DE SOLUTIONS DE SURVEILLANCE À DISTANCE DES PATIENTS DEVRAIT DYNAMISER LE MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DE SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE AU COURS DE LA PÉRIODE DE PRÉVISION DE 2022 À 2029

FIGURE 12 LE SEGMENT DES SERVICES DEVRAIT REPRÉSENTER LA PLUS GRANDE PART DU MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE EN 2022 ET 2029

FIGURE 13 MOTEURS, CONTRAINTES, OPPORTUNITÉS ET DÉFIS DU MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE

FIGURE 14 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PRODUIT ET SERVICES, 2021

FIGURE 15 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PRODUIT ET SERVICES, 2022-2029 (EN MILLIONS USD)

FIGURE 16 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PRODUIT ET SERVICES, TCAC (2022-2029)

FIGURE 17 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PRODUIT ET SERVICES, COURBE DE VIE

FIGURE 18 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR APPLICATION, 2021

FIGURE 19 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR APPLICATION, 2022-2029 (EN MILLIONS USD)

FIGURE 20 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR APPLICATION, TCAC (2022-2029)

FIGURE 21 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR APPLICATION, COURBE DE VIE

FIGURE 22 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR TAILLE D'ÉTABLISSEMENT, 2021

FIGURE 23 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR TAILLE D'ÉTABLISSEMENT, 2022-2029 (EN MILLIONS USD)

FIGURE 24 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR TAILLE D'ÉTABLISSEMENT, TCAC (2022-2029)

FIGURE 25 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR TAILLE D'ÉTABLISSEMENT, COURBE DE VIE

FIGURE 26 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR MODE D'ACHAT, 2021

FIGURE 27 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR MODE D'ACHAT, 2022-2029 (EN MILLIONS USD)

FIGURE 28 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR MODE D'ACHAT, TCAC (2022-2029)

FIGURE 29 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR MODE D'ACHAT, COURBE DE LIGNE DE VIE

FIGURE 30 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR UTILISATEUR FINAL, 2021

FIGURE 31 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR UTILISATEUR FINAL, 2022-2029 (EN MILLIONS USD)

FIGURE 32 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR UTILISATEUR FINAL, TCAC (2022-2029)

FIGURE 33 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR UTILISATEUR FINAL, COURBE DE VIE

FIGURE 34 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : APERÇU (2021)

FIGURE 35 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PAYS (2021)

FIGURE 36 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PAYS (2022 ET 2029)

FIGURE 37 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PAYS (2021 ET 2029)

FIGURE 38 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PAR PRODUIT ET SERVICES (2022-2029)

FIGURE 39 MARCHÉ DE L'INTÉGRATION DES TECHNOLOGIES DE L'INFORMATION (TI) DANS LE DOMAINE DE LA SANTÉ AU MOYEN-ORIENT ET EN AFRIQUE : PART DES ENTREPRISES EN 2021 (%)

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.