アジア・パシフィック・コントラスト・メディア・インジェクター市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

346.00 Million

USD

603.44 Million

2024

2032

USD

346.00 Million

USD

603.44 Million

2024

2032

| 2025 –2032 | |

| USD 346.00 Million | |

| USD 603.44 Million | |

| % | |

|

アジア・パシフィック・コントラスト・メディア・インジェクター・マーケット・セグメンテーション、製品(インジェクター・システムおよび消耗品)、タイプ(シングルヘッド・インジェクター、デュアルヘッド・インジェクター、シンリンジレス・インジェクター)、アプリケーション(放射線学、インターベンショナル・カーディオロジー、インターベンショナル・ラジオロジー)、エンド・ユース(病院、診断センター、およびアンブレータ)- 業界動向と予測 2032

アジア・パシフィック・コントラスト・メディア・インジェクター市場規模

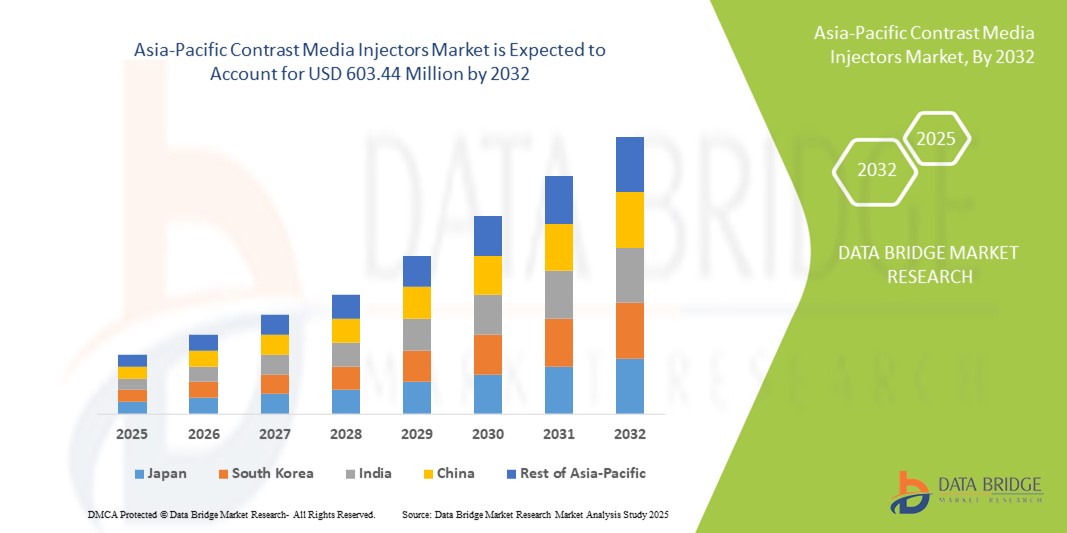

- アジア・パシフィック・コントラスト・メディア・インジェクター市場規模は、2024年のUSD 346.00百万そして到達する予定2032年までに603.44百万米ドル, お問い合わせカリフォルニア 7.2%予報期間中

- 市場成長は、慢性疾患の増加の優先順位、ヘルスケア投資の増加、および診断イメージングにおける技術の進歩によって大幅に燃料を補給し、病院やイメージングセンターのコントラストメディアインジェクタのより大きな採用につながる

- さらに、正確で安全かつ効率的なイメージング手順の需要が高まっています。現代の放射線と診断ワークフローの重要なツールとして、コントラストメディアインジェクタを確立しています。 これらの収束要因は、コントラストメディアインジェクタソリューションの取込みを加速し、その結果、業界の成長を著しく向上しています

アジア・パシフィック・コントラスト・メディア・インジェクター市場分析

- 対照的な媒体の注入器は、画像処理の間に対照の代理店の精密な配達を提供し、高度のイメージング システムとの高められた正確さ、安全および継ぎ目が無い統合による病院およびイメージング センターの現代診断イメージ投射のワークフローのますます重要な部品です

- 対照的な媒体の注入器のためのエスケーラビリティの要求は主に慢性疾患の上昇の prevalence によって、高度のイメージ投射物の採用および有効な、信頼できる、および診断プロシージャの自動化された注入システムのための必要性を燃やします

- 中国は、2024年に42.5%の最大の収益シェアを持つアジア太平洋のコントラストメディアインジェクタ市場を支配し、急速に拡大する医療インフラ、診断イメージングセンターの増加、および医療サービスを改善する強力な政府の取り組みによって主導しました

- 日本は、技術的に先進的なインジェクターシステムを採用し、民間および専門病院の需要が高いため、予測期間中にアジア・パシフィック・コントラスト・メディア・インジェクター市場で最も急速に成長している国であることが期待されています

- インジェクターシステムセグメントは、2024年に47%の市場シェアを持つアジア太平洋のコントラストメディアインジェクター市場を支配し、高精度、安全機能、CTやMRIなどの複数のイメージングモダリティとの互換性を強化しました。

レポートスコープとアジア太平洋コントラストメディアインジェクタ市場セグメンテーション

| アトリビュート | アジア・パシフィック・コントラスト・メディア・インジェクター・キー・マーケット・インサイト |

| カバーされる区分 |

|

| カバーされた国 | アジアパシフィック

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

アジア・パシフィック・コントラスト・メディア・インジェクター市場動向

自動化・AI対応イメージングシステムとの統合

- アジア・パシフィック・コントラスト・メディア・インジェクター市場における有意で加速的な傾向は、自動イメージング・システムとAIによるイメージング・プロトコルとのインジェクターの統合であり、精度、ワークフローの効率性を高め、患者の安全を実現します。

- 例えば、MEDRAD Stellant FLEXインジェクタはCTとシームレスに統合MRIについて病院および診断中心の手動介入を最小にする間対照配達を自動化するシステム

- AI対応のインジェクタは、患者固有のパラメータに基づいてインジェクション率を最適化し、潜在的なエラーに対する予測アラートを提供し、より一貫性のあるイメージング結果を保証します。 たとえば、BraccoインジェクタモデルはAIを使用してリアルタイムイメージングフィードバックに基づいて注射プロトコルを調整します。

- 病院情報システムとの統合により、複数のイメージング機器の集中制御と監視、診断センター全体の操作を合理化し、スケジューリング効率を向上させることができます。

- 自動化されたインテリジェントで相互接続されたインジェクタシステムに対するこの傾向は、イメージング精度のためのユーザーの期待を再構築し、バイエルやグエルベットなどの企業は、複数のモジュール間でシームレスな運用のためのAI対応インジェクタを開発しています

- 検査部門が効率性、安全性、人的誤りを求めるため、自動およびAIによる統合による対照的なメディアインジェクタに対する需要は、病院や診断センター全体で急速に増加しています。

アジア・パシフィック・コントラスト・メディア・インジェクター・マーケット・ダイナミクス

ドライバー

診断および慢性疾患の増加による上昇の要求

- 慢性疾患の高まりは、患者の体積を増加させ、診断イメージングの手順を増加させることと相まって、アジア・パシフィックにおける対照的な媒体の注入器の要求の主要な運転者です

- 例えば、2024年にSiemens Healthineersは、中国各地の大量のイメージングセンターでインジェクタシステムを拡張する取り組みを開始しました。

- ヘルスケアプロバイダは、画像の精度と運用効率を向上させることを目指し、インジェクタは、精密で自動化されたコントラストの配信を提供し、手続き型エラーを減らし、患者の成果を高めることを目指しています。

- さらに、医療インフラの拡大、診断画像への投資の拡大、民間・専門病院の高まりは、現代のイメージングワークフローに欠かせないコントラストメディアインジェクタを作る

- 自動化インジェクタシステムの効率性、複数のイメージングモダリティとの互換性、および放射性スタッフの操作の容易さは、病院や診断センターの採用を推進する重要な要因です

- 患者の安全、標準化されたイメージングプロトコル、および減らされた手続き性に対する成長の焦点は、アジア・パシフィックの対照的な媒体の注入器のuptakeをさらに運転しています

拘束/チャレンジ

高コストと規制コンプライアンスハルール

- 手動注入方法と比較される高度の対照媒体の注入器および関連の消耗品の比較的高い費用は費用感受性の病院の採用をより広い障壁です

- たとえば、インドと東南アジアの小規模なイメージングセンターは、運用上のメリットにもかかわらず、予算の制約によるプレミアムインジェクタシステムへの投資を躊躇するかもしれません。

- 安全基準や品質基準の承認を含む厳しい地域および国家医療機器規則の遵守、複雑性および市場の参入の遅延を新しいインジェクタモデルに追加

- コストの最適化、柔軟な価格設定モデル、および規制サポートを通じてこれらの課題に対処することは、市場浸透を拡大し、ヘルスケアプロバイダーの信頼を得るための不可欠です

- 一部のメーカーは、低コストでエントリーレベルまたは再生インジェクターモデルを提供していますが、高度な自動化とプレミアムインジェクターツイート統合は高価であり、新興市場での採用を制限します

- 革新的な資金調達、規制ガイダンス、および手頃な価格の製品提供を通じて、コストとコンプライアンスの課題を克服することは、アジア・パシフィック・コントラスト・メディア・インジェクター市場における持続的な成長にとって不可欠です。

アジア・パシフィック・コントラスト・メディア・インジェクター市場スコープ

市場は、製品、タイプ、アプリケーション、エンドの使用に基づいてセグメント化されます。

- 製品情報

製品のベースでは、アジア・パシフィック・コントラスト・メディア・インジェクター市場は、インジェクター・システムと消耗品に分けられます。 Injector Systemsは、2024年に47%の最大の収益シェアで市場を支配し、CT、MRI、およびその他の画像処理のための精密で自動化されたコントラスト注射を提供することで重要な役割を果たしました。 病院および診断センターは、複数の画像モジュールとの精度、信頼性、互換性のために注入器システムを優先します。 セグメントは、プログラム可能なインジェクションプロトコル、安全アラート、およびイメージングソフトウェアとの統合などの高度な機能から恩恵を受けます。 手動のエラーを減らし、ワークフローの効率を改善するためのラジオロジストのバリューインジェクタシステム。 AI の主張された注入および二重ヘッド システムを含む技術の革新を、更に高めます注入器のシステムを採用します。 セグメントの優位性は、ヘルスケアプロバイダーの意欲によって強化され、高品質で耐久性のある機器に投資し、患者の成果を改善します。

消耗品は、2025年から2032年までの最も速い成長率を目撃するために予想され、イメージング手順の上昇数と注射器、チューブセット、および対照的なメディアカートリッジの要求を回復することによって燃料を供給されます。 注射中に衛生を維持し、交差汚染を防ぐための消耗品は不可欠です。 病院や診断センターは、消耗品を頻繁に交換し、メーカーの安定した成長した収益ストリームを作成します。 新興アジア・太平洋諸国の患者様が高消費率を加速 セグメントは、事前充填された既製の消耗品の革新から、手続き効率を向上させる利点もあります。 感染制御や患者の安全に対する意識の拡大により、医療施設における高品質の消耗品の採用をさらに加速します。

- タイプ別

タイプに基づいて、市場は単一ヘッド注入器、二重ヘッド注入器および注射器に分けられます。 シングルヘッドインジェクタは、2024年にアジア・パシフィック市場を支配し、そのシンプルさ、信頼性、およびマルチヘッドシステムと比較してコストを削減しました。 単一ヘッド注入器は標準的なCTおよびMRIのイメージ投射のプロシージャのために、特に適当なイメージ投射量が付いている病院で広く利用されています。 操作の容易さは、放射性スタッフが一貫した結果を維持しながら、コントラストメディアを効率的に管理できるようにします。 セグメントは、幅広いイメージングプロトコルと高い互換性から恩恵を受けています。 単一ヘッド注入器は低い維持の条件による診断中心および小さい病院で特に好まれます。 製造業者は安全センサーおよびプログラム可能な制御とこれらの注入器を改良し、市場の優位性を更に凝固し続けます。

デュアルヘッドインジェクタは、2025から2032までの最速の成長率を目撃し、マルチコントラストプロトコルの需要の増加と異なるエージェントの同時管理によって駆動されます。 デュアルヘッドインジェクタは、大量の病院や介入放射線学部門のワークフロー効率性を向上させます。 それらは精密な対照の混合を可能にしましたり、複雑なイメージ投射のプロシージャを支え、繰り返された注入の必要性を減らします。 セグメントは、時間効率と患者の快適性を優先する高度な医療センターで牽引しています。 AIによるフロー規制や遠隔監視などの継続的な技術改善、採用の強化 介入手順への投資を成長させ、緊急時のイメージングの高速化の必要性は、さらに、デュアルヘッドインジェクタの成長を促進します。

- 用途別

用途に応じて、市場は放射線学、介入心、および介入放射線学に分けられます。 ラジオロジーは、2024年に市場を支配し、CTやMRIスキャンなどの定期的なイメージング手順の高量による最大の収益シェアを占めています。 ラジオロジー部門は、正確で再現可能な結果を得るために、対照的なメディアインジェクタに大きく依存しています。 セグメントは、画像の品質を向上させるAI支援注射プロトコルを含む継続的な技術アップグレードの恩恵を受けています。 病院および診断センターは患者の安全を保障し、対照の無駄を最小にし、ワークフローを合理化する注入器を優先順位付けします。 ラジオロジーアプリケーションは、民間および公共医療施設の双方の需要を促進します。 新興国におけるイメージングインフラの拡大により、このセグメントの優位性が強化されます。

2025年から2032年までの最も速い成長率を目撃するInterventional Radiologyは、最小限の侵襲的な手順と複雑なイメージングガイドによる介入の採用の増加によって燃料を供給する予定です。 慣習的な放射状学はプロシージャの成功および忍耐強い安全を保障するために高度の正確で、制御された対照配達を要求します。 セグメントは、複数のコントラストエージェントをサポートするデュアルヘッドとプログラム可能なインジェクタシステムから恩恵を受けます。 心臓血管疾患、腫瘍学の手順、血管介入の有利な発生は、成長する需要に貢献します。 病院および専門センターは高度の注入器システムに手続き上の条件を満たすためにますます投資しています。 インターベンショナルスタッフの継続的なトレーニングと啓発プログラムも、この分野におけるインジェクタの迅速な採用をサポートしています。

- エンド使用

末端の使用に基づいて、市場は病院、診断中心および血管の外科中心に分けられます。 病院は高度の忍耐強い容積、多数のイメージ投射部および高度の診断機能の必要性による最大の収入のシェアと2024年に市場を、支配しました。 病院は効率、正確さおよびワークフロー管理のための自動化され、二重ヘッド注入器システムを好む。 大規模イメージングインフラへの投資と、日常や緊急画像処理の採用に対する高い要求。 病院の区分は注入器の製造業者によって提供される長期維持の契約およびサービス サポートからの寄与します。 高い信頼性および安全規格はキーのエンド ユーザーとして病院を更に凝固させます。 高度の病院はまた改善された手続き上の結果、忍耐強い満足を高めるためにAIアシスト注入器を利用します。

診断センターは、2025年から2032年までの最も速い成長率を目撃し、外来イメージング施設の急速な拡大によって燃料を供給し、便利で費用効果が大きい診断サービスのための成長の要求を増加することを期待しています。 診断センターは、自動インジェクターシステムを採用し、より高い患者のスループットを処理し、一貫したイメージング品質を保証します。 ヘルスケアの認知度を高め、医療ツーリズム、診断手順の保険増大によるセグメントメリット 慢性疾患の予防と早期診断の必要性は、先進的なインジェクタでの投資を促進しています。 製造業者は密集した、使いやすいおよび費用効果が大きい注入器解決の診断中心を目標としています。 インジェクターが提供する利便性、効率性、安全性は、アジア太平洋地域の診断センターに優先する選択肢となっています。

アジア・パシフィック・コントラスト・メディア・インジェクター市場地域分析

- 中国は、2024年に42.5%の最大の収益シェアを持つアジア太平洋のコントラストメディアインジェクタ市場を支配し、急速に拡大する医療インフラ、診断イメージングセンターの増加、および医療サービスを改善する強力な政府の取り組みによって主導しました

- イメージング手順の精度、安全性、および自動化を優先する領域のヘルスケアプロバイダは、CT、MRI、および介入放射線装置と統合する高度な注入器システムの高い採用につながる

- この広範囲にわたる採用は、患者のボリュームを増加させ、早期診断の意識を高め、公共および民間病院の両方で投資を成長させ、現代の診断ワークフローの重要なツールとして対照的なメディアインジェクタを確立することにより、さらにサポートされます

中国コントラストメディアインジェクタ市場インサイト

中国の対照的なメディアインジェクター市場は、医療インフラの急速な拡大と診断イメージングセンターの増加によって駆動され、2024年にアジア太平洋で最大の収益シェアを獲得しました。 病院や専門クリニックは、画像処理の精度、安全性、自動化を優先しています。 健康を近代化し、早期診断を促進するための政府の取り組みは、さらなる採用を促進しています。 患者の体積を上げ、公立病院と私立病院の双方の投資を成長させ、需要を高めます。 また、先進的なCT、MRI、および慣習的な放射線システムとの統合は成長を促進しています。 製造拠点としての中国の位置は、インジェクタシステムの手頃な価格とアクセシビリティも向上します。

ジャパン・コントラスト・メディア・インジェクター・マーケット・インサイト

ハイテク医療施設、急速な都市化、精密な診断イメージングの需要により、日本のコントラストメディアインジェクター市場が勢いを増しています。 病院や専門センターは、ワークフローの効率化と患者の安全を高めるために、自動化されたAI支援インジェクタシステムを採用しています。 CT、MRI、および慣習的な放射状装置との統合は広範な採用を支えます。 日本は、イノベーション、高品質基準、技術的に先進的な医療インフラに重点を置き、最先端のインジェクターソリューションの使用を保証します。 成長する高齢者人口は、使いやすく、正確で安全な注入器システムに対する需要を燃料化しています。

インド コントラスト メディア インジェクター マーケット インサイト

インドのコントラストメディアインジェクター市場は、急速な都市化、ヘルスケアインフラの拡大、およびイメージングセンターの増加によって推進され、2024年に重要な収益シェアのために考慮しました。 予防医療や早期診断の意識を高めることで、自動インジェクタシステムの導入が進んでいます。 費用効果が大きい注入器解決、強い国内製造業と結合されて、首都および層2都市を渡るサポート成長。 病院および診断センターはプロシージャの正確さ、効率および忍耐強い安全を改善する注入器システムをますます導入しています。 スマートな病院のインフラを促進し、市場浸透を加速する政府の取り組み。

韓国コントラストメディアインジェクター市場インサイト

韓国のコントラストメディアインジェクター市場は、先進的な医療施設によって燃料を供給し、最小限の侵襲的なイメージング手順の需要増加を着実に成長することが期待されます。 病院および専門イメージングセンターは、ワークフローの効率と精度を向上させるために、AI対応およびデュアルヘッド注入器システムを採用しています。 ヘルスケア投資と技術革新のライジングは、先進インジェクタソリューションの採用に貢献します。 CTやMRIなどの近代的な画像のモダリティとの統合により、正確で安全なコントラスト配信を実現します。 ヘルスケアのモダナイゼーションをサポートし、患者の意識を高め、市場成長を促進します。

アジア・パシフィック・コントラスト・メディア・インジェクター市場シェア

アジア・パシフィック・コントラスト・メディア・インジェクター業界は、主に以下の分野を含む、老舗の企業によって導かれています。

- 株式会社アポロRT(香港)

- バイエルAG(ドイツ)

- Bracco Imaging S.p.A.(イタリア)

- GE HealthCare(アメリカ)

- グエルベット(フランス)

- MEDTRON AG(ドイツ)

- 株式会社根本協林堂(日本)

- シンセンAnkeのハイテクなCo.、株式会社(中国)

- Sinoの医療機器の技術Co.、株式会社(中国)

- Ulrich GmbH & Co. KG (ドイツ)

- ヴィーゴングループ(フランス)

- Leriva(インド)

- スペクトラムメディカルテクノロジーズ LLP(英国)

- AngioDynamics(アメリカ)

- ビビッドイメージングソリューション(オーストラリア)

- IVDテクノロジー(インド)

- シンセンMindrayの生物医学の電子工学Co.、株式会社(中国)

- Siemens Healthineers AG(ドイツ)

- 日立メディカル株式会社(日本)

アジア・パシフィック・コントラスト・メディア・インジェクター市場における最近の発展とは?

- 2024年8月、バイエルがMEDRAD Stellant FLEX Computed Tomography Injection Systemを立ち上げました。 この製品発売は、コントラストの無駄や自動化された文書のより小さなシリンジサイズなど、グローバルな戦略とその特徴の一部であり、アジア太平洋市場での効率性と持続可能性のための成長した需要に直接関連しています

- 2024年12月、Braccoの診断Inc.はMRIのための最高の3TMシリンジレス注入器がFDAの整理を受けたことを発表しました。 この革新的で、シリンジレスなデザインは、プラスチック廃棄物を削減し、放射線学部門のワークフローの効率性を向上させるため、重要な開発です。 初期のクリアランスは米国市場ではありますが、この技術は、アジア・パシフィックを含む他の主要市場に影響する主要なブレークスルーであり、持続可能な効率的な医療ソリューションの需要が高まっています。

- 2024年4月、Braccoグループでは、Bracco Japan社、Bracco Japan社、Bracco Japan社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、Bracco社、B この戦略的動きは、Braccoの日本市場での直接的な存在を強化し、現地の医師や患者に「診断イメージングのための最先端コントラストエージェント、技術とサービス」を提供し、インジェクターや他の製品の提供を強化する

- 2022年12月、GE HealthCareは、米国におけるGE HealthCareブランドのマルチデュースコントラストメディアインジェクタを提供するulrich Medicalとの合意を発表しました。 シンリンジレス技術である「CTモーション」インジェクターのためのこのコラボレーションは、市場への革新的でワークフロー効率の高いソリューションを提供する主要なプレーヤーの傾向を強調します。 このタイプのコラボレーションと技術導入は、アジア・パシフィックを含む他のグローバル地域に優先されることが多い

- 2022年11月、サニーブルック・ヘルス・サイエンス・センターとバイエルは、カナダのMEDRAD Centargo CT噴射システムの導入を発表しました。 北米で初となるこの打ち上げは、バイエルなどの主要企業による高度なワークフロー最適化インジェクタシステムのロールアウトを強調し、アジア太平洋市場へのトレンドを直接影響し、設定します

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。