Europe Dual Emission X

Market Size in USD Billion

CAGR :

%

USD

1.20 Billion

USD

1.71 Billion

2025

2033

USD

1.20 Billion

USD

1.71 Billion

2025

2033

| 2026 –2033 | |

| USD 1.20 Billion | |

| USD 1.71 Billion | |

| % | |

|

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Segmentation, By Product Type (Central Dual Emission X-Ray Absorptiometry (DEXA) and Peripheral Dual Emission X-Ray Absorptiometry (DEXA)), Application (Body Composition Analysis, Fracture Diagnosis, Bone Densitometry and Fracture Risk Assessment), End Users (Hospitals, Clinics, Mobile Health Centres and Others)- Industry Trends and Forecast to 2033

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Size

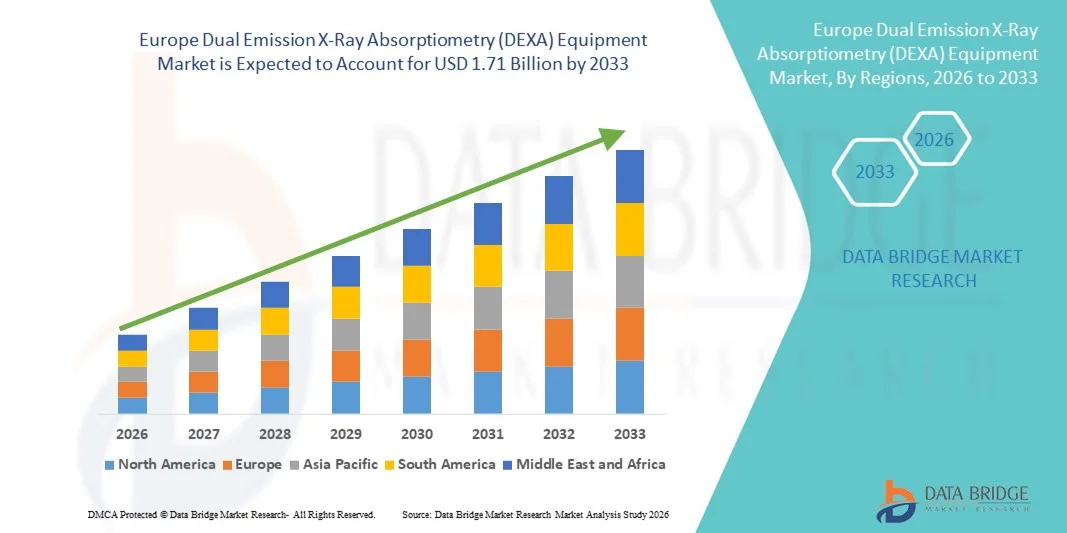

- The Europe Dual Emission X-Ray Absorptiometry (DEXA) equipment market size was valued at USD 1.20 billion in 2025 and is expected to reach USD 1.71 billion by 2033, at a CAGR of 4.60% during the forecast period

- The market growth is largely driven by increasing awareness of osteoporosis and other bone-related disorders, coupled with the expanding geriatric population across Europe. Advances in imaging technology and improved accessibility of diagnostic centers are also contributing to higher adoption rates

- Furthermore, the preference for accurate, low-radiation, and non-invasive bone density assessment solutions is positioning DEXA equipment as the standard choice in hospitals, clinics, and research facilities. These converging factors are accelerating the deployment of DEXA systems, thereby significantly boosting the industry’s growth

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Analysis

- Dual Emission X-Ray Absorptiometry (DEXA) systems, providing accurate bone mineral density measurement and body composition analysis, are increasingly vital components of modern diagnostic healthcare across hospitals, clinics, and mobile health centers due to their precision, low radiation exposure, and non-invasive operation

- The escalating demand for DEXA equipment is primarily fueled by growing awareness of osteoporosis and other bone-related disorders, technological advancements in imaging systems, and the increasing geriatric population in Europe seeking preventive and diagnostic care

- Germany dominated the Europe Dual Emission X-Ray Absorptiometry (DEXA) equipment market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of medical imaging technologies, and a strong presence of key industry players, with hospitals and clinics experiencing substantial growth in central and peripheral DEXA system installations

- Poland is expected to be the fastest-growing country during the forecast period due to expanding healthcare facilities, government initiatives promoting bone health screening, and rising investments in mobile and community-based diagnostic solutions

- Bone Densitometry and Fracture Risk Assessment segment dominated the Europe Dual Emission X-Ray Absorptiometry (DEXA) equipment market in 2025 with a market share of 45.3%, driven by the increasing need for early osteoporosis detection, fracture prevention, and comprehensive patient management across hospitals and diagnostic centers

Report Scope and Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Segmentation

|

Attributes |

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Trends

Advancements in Imaging Technology and AI Integration

- A significant and accelerating trend in the Europe DEXA equipment market is the integration of advanced imaging technologies and AI-based analytics, enhancing diagnostic accuracy and workflow efficiency in hospitals, clinics, and mobile health centers

- For instance, central and peripheral DEXA systems now incorporate AI-driven image reconstruction and automated fracture detection, allowing clinicians to assess bone health more accurately and efficiently than conventional systems

- AI integration enables features such as automated body composition analysis, intelligent anomaly detection, and predictive fracture risk assessment, providing clinicians with actionable insights and reducing diagnostic errors. Furthermore, AI-supported software can track patient history over time to improve monitoring and treatment planning

- The seamless incorporation of DEXA systems with hospital information systems (HIS) and electronic medical records (EMR) facilitates centralized patient management, enabling physicians to coordinate diagnosis, treatment, and follow-up from a single interface

- This trend toward more intelligent, precise, and interconnected diagnostic solutions is fundamentally reshaping healthcare expectations in Europe. Consequently, companies such as Hologic and GE Healthcare are developing AI-enabled DEXA systems with enhanced bone health assessment and integration capabilities

- The demand for DEXA equipment offering AI-driven analytics and improved imaging workflow is growing rapidly across hospitals, clinics, and mobile health centers, as healthcare providers increasingly prioritize accuracy, efficiency, and preventive care

- In addition, modular and portable DEXA systems are gaining traction, offering flexibility for mobile health centers and research studies, and enabling on-site patient assessments outside traditional hospital settings

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Dynamics

Driver

Rising Awareness of Bone Health and Preventive Screening

- The increasing prevalence of osteoporosis and other bone-related disorders, coupled with growing preventive healthcare initiatives, is a significant driver for the heightened adoption of DEXA equipment in Europe

- For instance, in April 2025, Hologic announced the launch of its next-generation central DEXA system with advanced AI-based fracture risk assessment, expected to enhance clinical adoption across hospitals and diagnostic centers

- As patients and healthcare providers become more aware of the importance of early detection, DEXA systems offer precise bone densitometry, body composition analysis, and fracture risk prediction, providing compelling clinical value

- Furthermore, government-led bone health awareness programs and insurance coverage for preventive screenings are making DEXA assessments more accessible, integrating these systems as standard tools in hospitals and clinics

- The ability to track patient bone health over time, integrate with hospital information systems, and provide accurate predictive analytics is a key factor propelling DEXA adoption across Europe. The trend towards AI-enabled and portable DEXA solutions further contributes to market growth

- For instance, collaborations between equipment manufacturers and healthcare providers to conduct community-based bone screening camps are increasing market reach and awareness, further driving adoption

- Rising demand for research-grade DEXA systems in universities and medical research centers is also supporting market expansion, particularly for longitudinal studies on osteoporosis and metabolic disorders

Restraint/Challenge

High Equipment Cost and Limited Trained Workforce

- The relatively high cost of DEXA systems and the need for specialized training to operate the equipment pose significant challenges to broader market penetration, particularly for smaller clinics and mobile health providers

- For instance, smaller diagnostic centers in developing European countries may delay adoption due to budget constraints and the requirement for certified technicians to ensure accurate measurements

- Addressing these challenges through cost-effective models, user-friendly interfaces, and training programs is crucial for wider adoption. Companies such as GE Healthcare and Hologic emphasize simplified operation and support services in their marketing to encourage uptake. In addition, the high maintenance and calibration requirements of advanced DEXA systems can act as a barrier

- While the benefits of preventive diagnostics are clear, the perceived premium for sophisticated AI-enabled and high-precision systems can limit adoption, especially in budget-conscious or smaller healthcare facilities

- Overcoming these challenges through financing options, leasing programs, and educational initiatives for clinicians and technicians will be vital for sustained growth of the DEXA equipment market in Europe

- For instance, ongoing workshops and certification programs organized by manufacturers help clinicians operate DEXA systems efficiently, partially mitigating workforce constraints

- Supply chain limitations for high-end components and software upgrades can also delay installations and expansions, particularly in countries with fewer local distributors or service centers

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Scope

The market is segmented on the basis of product type, application, and end users.

- By Product Type

On the basis of product type, the Europe DEXA equipment market is segmented into Central DEXA and Peripheral DEXA systems. Central DEXA dominated the market with the largest revenue share in 2025, driven by its high precision, comprehensive scanning capabilities, and suitability for hospitals and large diagnostic centers. These systems are often prioritized in well-established healthcare facilities due to their ability to perform full-body scans and advanced fracture risk assessments. Hospitals and research institutions prefer central DEXA systems for their robust imaging quality, faster scanning time, and integration with hospital information systems. The demand is further supported by technological advancements such as AI-assisted image reconstruction and automated bone analysis, which enhance diagnostic accuracy. In addition, central DEXA systems are widely used for clinical trials and longitudinal bone health studies, adding to their dominance in the market.

Peripheral DEXA is expected to witness the fastest growth during the forecast period, as it is more compact, portable, and cost-effective compared to central systems. These devices are increasingly adopted in mobile health centers, smaller clinics, and community screening programs, enabling on-site bone densitometry and fracture risk assessment. Peripheral DEXA systems are ideal for targeted measurements, such as wrist or heel scans, making them convenient for rapid diagnostics. The growing focus on preventive healthcare and remote patient monitoring is fueling the adoption of portable devices. Furthermore, ease of use, lower operational costs, and minimal space requirements are accelerating the growth of peripheral DEXA systems across Europe.

- By Application

On the basis of application, the Europe DEXA equipment market is segmented into body composition analysis, fracture diagnosis, bone densitometry, and fracture risk assessment. Bone Densitometry and Fracture Risk Assessment dominated the market in 2025, with the largest revenue share of 45.3, driven by the rising prevalence of osteoporosis, fractures, and metabolic bone disorders. These applications are critical in hospitals and diagnostic centers for early detection and preventive treatment planning. Bone densitometry allows clinicians to assess bone mineral density accurately, while fracture risk assessment tools help predict future fractures, improving patient management. The dominance is further strengthened by integration with AI algorithms that enhance prediction accuracy and streamline reporting. Patients undergoing longitudinal monitoring benefit from repeated assessments, which reinforce the need for these applications. In addition, government health initiatives promoting bone health awareness and preventive screening programs support the high adoption of bone densitometry and fracture risk assessment applications.

Body Composition Analysis is expected to witness the fastest growth during the forecast period, driven by its increasing adoption in wellness centers, fitness facilities, and research studies. This application provides insights into fat mass, lean mass, and overall body composition, which are essential for nutrition planning, obesity management, and sports science research. The rise of preventive healthcare trends and growing demand for non-invasive monitoring solutions contribute to the uptake of this application. Portable and peripheral DEXA devices are particularly suitable for body composition analysis, as they allow quick assessments in various settings. Furthermore, increasing awareness among consumers and healthcare providers about the importance of overall health and metabolic monitoring supports rapid growth in this segment.

- By End Users

On the basis of end users, the Europe DEXA equipment market is segmented into hospitals, clinics, mobile health centres, and others. Hospitals dominated the market with the largest revenue share in 2025, due to their established infrastructure, high patient throughput, and preference for advanced imaging solutions. Hospitals require DEXA systems for comprehensive patient management, including diagnosis, treatment planning, and monitoring of bone health in high-risk populations. Central DEXA systems are primarily deployed in hospital settings because of their precision, robustness, and integration with electronic medical records. In addition, hospitals often lead research studies, clinical trials, and longitudinal assessments, further reinforcing their dominance as end users. The demand is strengthened by government and insurance initiatives promoting preventive screenings in hospital-based programs.

Mobile Health Centres are expected to witness the fastest growth during the forecast period, as they enable preventive screenings in rural and underserved areas. These mobile units leverage portable peripheral DEXA systems to perform bone densitometry and fracture risk assessments on-site, increasing healthcare accessibility. The rising focus on community-based health initiatives and government-sponsored screening programs is fueling adoption. Mobile health centers also benefit from the flexibility, lower costs, and ease of deployment offered by portable systems. Furthermore, the trend toward preventive care and early diagnosis is accelerating the integration of DEXA services in mobile healthcare solutions.

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Regional Analysis

- Germany dominated the Europe Dual Emission X-Ray Absorptiometry (DEXA) equipment market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of medical imaging technologies, and a strong presence of key industry players, with hospitals and clinics experiencing substantial growth in central and peripheral DEXA system installations

- Hospitals and diagnostic centers in Germany highly value the accuracy, low radiation exposure, and integration capabilities of DEXA systems, which enable precise bone densitometry, fracture risk assessment, and body composition analysis

- This widespread adoption is further supported by government initiatives promoting preventive healthcare, well-established reimbursement policies for bone health screenings, and increasing awareness of osteoporosis and related disorders, establishing DEXA as the preferred diagnostic solution across hospitals, clinics, and research institutions

The Germany Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The Germany DEXA equipment market is expected to expand at a considerable CAGR during the forecast period, fueled by well-developed healthcare infrastructure, high adoption of advanced imaging technologies, and strong presence of key industry players. Hospitals and research institutions prioritize central and peripheral DEXA systems for bone densitometry, fracture risk assessment, and body composition analysis. Germany’s emphasis on preventive healthcare, combined with government-supported osteoporosis screening initiatives, is driving market growth. The integration of DEXA systems with hospital information systems and AI-assisted analytics is also increasingly prevalent, improving diagnostic workflow and patient management.

U.K. Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The U.K. DEXA equipment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of bone health, increasing demand for preventive diagnostics, and the adoption of mobile screening units in rural areas. Healthcare facilities are prioritizing key applications such as bone densitometry and fracture risk assessment. The presence of advanced clinical research centers and high standards of patient care supports the uptake of AI-enabled DEXA systems. In addition, government initiatives for early detection of osteoporosis and bone-related disorders further stimulate market expansion.

Poland Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The Poland DEXA equipment market is expected to witness the fastest growth during the forecast period, owing to expanding healthcare infrastructure, government-sponsored community screening programs, and rising investments in portable DEXA systems for mobile health centers. Increasing focus on preventive care and early diagnosis is driving adoption in smaller clinics and rural healthcare units. Peripheral DEXA devices, which are cost-effective and easy to deploy, are particularly contributing to growth. The growing awareness of bone health among the general population is also fueling demand across hospitals and clinics.

France Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The France DEXA equipment market is projected to grow steadily, supported by well-established healthcare systems, strong insurance coverage for preventive screenings, and growing awareness of osteoporosis management. Hospitals and private diagnostic centers are the primary end users, with central DEXA systems preferred for comprehensive bone densitometry. The adoption of AI-assisted analytics and integration with electronic health records enhances workflow efficiency. Increasing focus on research and clinical studies on bone health is further stimulating the market.

Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Share

The Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment industry is primarily led by well-established companies, including:

- Hologic, Inc. (U.S.)

- GE HealthCare (U.S.)

- Swissray International, Inc. (U.S.)

- Mindways Software, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Konica Minolta Healthcare Americas, Inc. (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM Healthcare (Japan)

- Analogic Corporation (U.S.)

- Carestream Health (U.S.)

- Ziehm Imaging (Germany)

- Mindray Medical International (China)

- Medtronic (Ireland)

- Orthoscan, Inc. (U.S.)

- Positron Corporation (U.S.)

- ICRco, LLC (U.S.)

- Whale Imaging, Inc. (U.S.)

- Norland at Swissray (U.S.)

What are the Recent Developments in Europe Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market?

- In March 2026, England announced the rollout of 20 new DEXA bone scanners to help prevent fractures and cut waiting times Patients across England are set to benefit from additional and replacement DEXA scanners that will enable earlier diagnosis of osteoporosis and other bone conditions, cutting wait times and improving access to bone health assessments in clinical practice

- In March 2026, the Society of Radiographers highlighted the importance of DXA scanner investment across England for improved osteoporosis diagnosis. The article discusses funding for 20 new DEXA scanners and emphasizes the need for workforce support to ensure faster and more accurate detection of bone conditions

- In July 2025, Medimaps Group launched the TBS Osteo Advanced software in Europe for enhanced bone microarchitecture assessment This next‑generation software, cleared under EU Medical Device Regulation, delivers refined trabecular bone score analysis integrated with clinical DXA workflows, advancing fracture‑risk evaluation beyond standard bone density tests

- In May 2025, Hologic launched a next‑generation DEXA system featuring enhanced image resolution and AI‑assisted bone density analysis. This launch represents an advancement in diagnostic accuracy and imaging capabilities for bone health assessments, underlining continued innovation in DEXA equipment technology across Europe and globally

- In January 2025, Siemens Healthineers entered a strategic partnership with Mindray to integrate DEXA data management and interoperability into hospital information systems.

- This partnership aims to improve clinical workflows and data connectivity for DEXA imaging in hospital settings, enhancing diagnostic continuity and care coordination

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。