欧州の椎体形成術市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

254.64 Million

USD

608.31 Million

2025

2033

USD

254.64 Million

USD

608.31 Million

2025

2033

| 2026 –2033 | |

| USD 254.64 Million | |

| USD 608.31 Million | |

| % | |

|

欧州の椎体形成術市場のセグメンテーション:製品タイプ別(バルーン椎体形成術システム、ニードル椎体形成術システム、X線装置椎体形成術システム)、用途別(失われた椎体の修復および局所的な後弯症の矯正)、エンドユーザー別(病院、クリニック、外来手術センター、その他)-業界動向と2033年までの予測

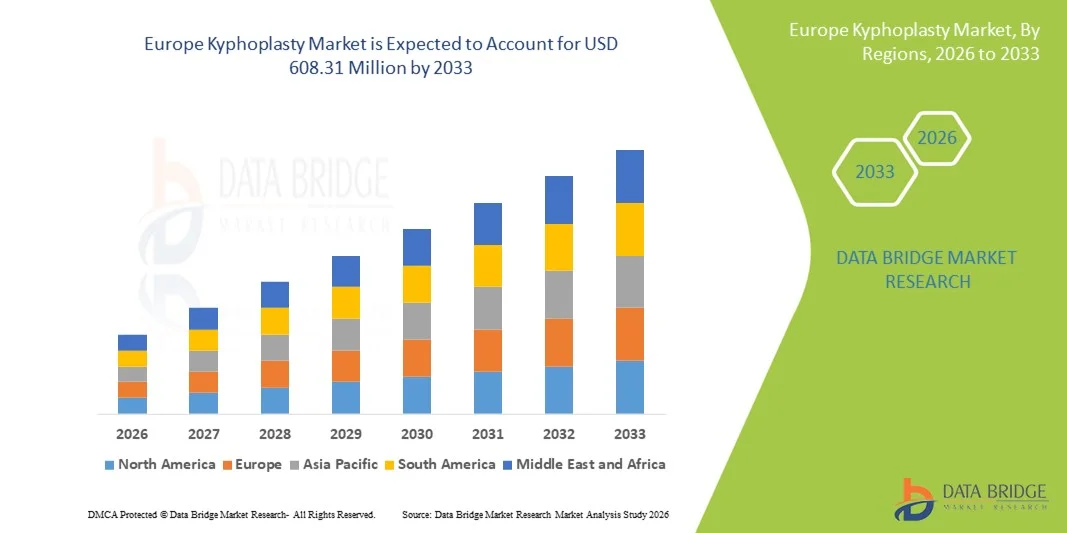

欧州におけるカイフォプラスティ市場規模

- 欧州のカイフォプラスティ市場規模は、2025年には2億5464万米ドルと評価され、予測期間中の年平均成長率(CAGR)11.50%で、2033年には6億831万米ドル に達すると予測されています 。

- 市場の成長は、主に骨粗鬆症性椎体圧迫骨折の有病率の上昇、高齢者人口の増加、そしてヨーロッパ全域における低侵襲脊椎手術に対する意識の高まりによって促進されている。

- さらに、バルーン椎体形成術システムの進歩、主要な欧州諸国における償還制度の改善、そして迅速な疼痛緩和と入院期間の短縮に対する嗜好の高まりにより、椎体形成術は好ましい椎体増強術として確立されつつあります。これらの要因が複合的に作用することで、椎体形成術用機器の普及が加速し、市場の拡大を大きく促進しています。

欧州におけるカイフォプラスティ市場分析

- 椎体形成術は、バルーンタンピング技術と骨セメントを用いて骨折した骨を安定させ、椎体の高さを回復させることで椎体圧迫骨折を治療する低侵襲の椎体増強術であり、迅速な疼痛緩和と可動性の改善をもたらすことから、ヨーロッパの病院や脊椎専門センターにおいて不可欠な介入治療となっている。

- 椎体形成術の需要増加の主な要因は、骨粗鬆症関連骨折の罹患率の上昇、ヨーロッパ全域における高齢者人口の増加、低侵襲脊椎治療への認識の高まり、そして入院期間を短縮し機能回復を早める手術に対する臨床医の嗜好である。

- ドイツは、2025年に欧州の椎体形成術市場を29.4%の収益シェアで支配した。これは、高度な医療インフラ、有利な償還制度、高い施術普及率、一流の整形外科および脊椎ケアセンターの存在、そして高齢化に伴う椎体圧迫骨折治療の増加といった特徴によるものである。

- フランスは、骨粗鬆症の罹患率の上昇、低侵襲脊椎手術へのアクセス拡大、および高度な介入技術への医療投資の増加を背景に、予測期間中に欧州の椎体形成術市場で最も急速に成長する国になると予想されている。

- バルーン椎体形成術セグメントは、椎体高回復における確立された臨床効果、迅速な疼痛緩和、および脊椎外科医による低侵襲骨折治療技術への強い嗜好を背景に、2025年には市場シェア61.3%で欧州椎体形成術市場を席巻した。

レポートの範囲と欧州カイフォプラスティ市場のセグメンテーション

|

属性 |

欧州におけるカイフォプラスティの主要市場に関する洞察 |

|

対象分野 |

|

|

対象国 |

ヨーロッパ

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成した市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業などの市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みも含まれています。 |

欧州における椎体形成術市場の動向

低侵襲性椎体増強術への嗜好の高まり

- 欧州の脊椎形成術市場における顕著かつ加速的な傾向として、先進的なバルーンカテーテルシステムと高粘度骨セメント技術に支えられた低侵襲脊椎手術への嗜好の高まりが挙げられます。こうした介入技術の進化は、手術の精度、患者の安全性、そして術後の回復結果を大幅に向上させています。

- 例えば、大手医療機器メーカーは、椎体高の回復を促進し、セメント注入の制御を最適化することで、漏出や隣接椎体骨折のリスクを低減するように設計された次世代バルーン椎体形成術システムを導入しています。同様に、ドイツとイタリアの病院では、手技の精度を向上させるために、画像誘導ナビゲーションシステムの導入が進んでいます。

- Technological advancements in kyphoplasty devices enable improved cement viscosity management, better fracture stabilization, and shorter procedure times. For instance, some systems incorporate controlled cement injection mechanisms to minimize extravasation risks and enhance structural support. Furthermore, integration with advanced imaging modalities allows clinicians to achieve precise balloon placement and improved clinical outcomes

- The growing integration of kyphoplasty procedures within comprehensive osteoporosis management programs facilitates coordinated care pathways involving orthopedic surgeons, radiologists, and geriatric specialists. Through multidisciplinary treatment models, healthcare providers can ensure timely diagnosis, intervention, and long-term fracture prevention strategies, creating a more structured care continuum

- This trend toward safer, more efficient, and patient-centric vertebral fracture management is fundamentally reshaping treatment standards across Europe. Consequently, several device manufacturers are investing in R&D to develop bioactive bone cements and expandable implant technologies aimed at improving long-term spinal stability and reducing complication rates

- The demand for advanced kyphoplasty systems is growing steadily across European healthcare facilities, as providers increasingly prioritize minimally invasive solutions that reduce hospitalization time, enable faster mobilization, and improve quality of life for elderly patients

- In addition, the rising establishment of dedicated spine and interventional radiology centers across major European countries is improving patient access to kyphoplasty procedures and supporting overall market penetration

Europe Kyphoplasty Market Dynamics

Driver

Growing Need Due to Rising Osteoporosis Prevalence and Aging Population

- The increasing prevalence of osteoporosis and vertebral compression fractures, coupled with Europe’s rapidly expanding geriatric population, is a significant driver for the heightened demand for kyphoplasty procedures

- For instance, in 2024, several European healthcare systems expanded funding allocations for osteoporosis screening and fracture management programs to address the rising clinical and economic burden associated with fragility fractures. Such strategic healthcare initiatives are expected to drive the kyphoplasty market growth during the forecast period

- As awareness of the debilitating impact of untreated vertebral fractures increases, kyphoplasty offers rapid pain relief, vertebral stabilization, and improved mobility, providing a compelling alternative to prolonged conservative treatments such as bracing and analgesic therapy

- Furthermore, favorable reimbursement policies in countries such as Germany and France, along with strong hospital infrastructure and access to trained spine specialists, are making kyphoplasty a preferred interventional treatment option for eligible patients

- The clinical benefits of shorter hospital stays, reduced dependency on opioid-based pain management, and quicker return to daily activities are key factors propelling the adoption of kyphoplasty across public and private healthcare institutions. The expansion of specialized spine centers further contributes to procedural volume growth

- Increasing early diagnosis rates through improved bone density screening programs are enabling timely clinical intervention, thereby supporting higher treatment adoption rates across at-risk populations

- In addition, growing collaboration between orthopedic societies and public health agencies to promote vertebral fracture awareness campaigns is strengthening referral networks and driving patient inflow for kyphoplasty procedures

Restraint/Challenge

High Procedure Costs and Risk of Cement Leakage Complications

- Concerns surrounding procedure-related complications, including bone cement leakage and adjacent vertebral fractures, pose a significant challenge to broader adoption of kyphoplasty across certain European healthcare settings. As the procedure involves percutaneous cement injection, clinical precision is critical to avoid adverse outcomes

- For instance, reported cases of cement extravasation in vertebral augmentation procedures have led some clinicians to exercise caution when selecting patients, particularly those with complex fracture patterns or severe comorbidities

- Addressing these concerns through enhanced device design, improved cement viscosity control, and physician training programs is crucial for strengthening clinical confidence. Manufacturers are emphasizing safety-enhancing features and controlled delivery systems to mitigate complication risks and reassure healthcare providers

- In addition, the relatively high procedural cost of kyphoplasty compared to conservative management can be a barrier in cost-sensitive healthcare systems, particularly in parts of Southern and Eastern Europe where reimbursement coverage may be limited

- While healthcare investments are increasing, budget constraints and varying reimbursement frameworks across European countries can still limit widespread procedural adoption, especially in facilities with restricted capital expenditure capacity

- Lengthy regulatory approval timelines for new vertebral augmentation devices within the European medical device framework may delay product launches and slow technological diffusion across the region

- Overcoming these challenges through technological refinement, expanded reimbursement support, broader clinical evidence demonstrating long-term cost-effectiveness, and streamlined regulatory pathways will be vital for sustained market expansion across Europe

Europe Kyphoplasty Market Scope

The market is segmented on the basis of product type, application, and end user.

- By Product Type

On the basis of product type, the Europe kyphoplasty market is segmented into balloon kyphoplasty systems, needle kyphoplasty systems, and X-Ray device kyphoplasty systems. The Balloon Kyphoplasty Systems segment dominated the market with the largest revenue share of 61.3% in 2025, driven by its strong clinical evidence base and widespread physician preference for controlled vertebral height restoration. Balloon systems allow cavity creation prior to cement injection, which reduces cement leakage risk and improves structural stabilization. Hospitals across Germany, France, and Italy increasingly favor balloon systems due to better patient outcomes and shorter recovery periods. The ability to restore spinal alignment and correct deformity more effectively than conventional vertebroplasty further strengthens adoption. In addition, reimbursement support in major European countries supports procedural uptake. Continuous technological improvements in balloon catheter design and cement delivery mechanisms also contribute to sustained segment leadership.

The Needle Kyphoplasty Systems segment is anticipated to witness the fastest growth rate during the forecast period, fueled by demand for cost-effective and simplified vertebral augmentation solutions. Needle-based systems often involve fewer device components, potentially lowering procedural costs in budget-sensitive healthcare settings. Increasing adoption in ambulatory surgical centres and mid-sized hospitals supports segment expansion. Physicians in emerging European markets are exploring needle systems for selected patient populations where full balloon deployment may not be necessary. Growing awareness of minimally invasive spine procedures and expanding training programs are improving procedural confidence. Furthermore, technological refinement in cement viscosity control is enhancing the safety profile of needle-based systems, supporting future growth.

- By Application

On the basis of application, the Europe kyphoplasty market is segmented into restoring lost vertebral body and correction of the local kyphosis. The Restoring Lost Vertebral Body segment held the largest market revenue share in 2025, driven by the high prevalence of osteoporotic vertebral compression fractures among the elderly population. Restoration of vertebral height is a primary clinical objective in kyphoplasty procedures, as it directly contributes to pain reduction and improved spinal biomechanics. European clinicians prioritize height restoration to prevent progressive spinal deformity and pulmonary compromise. The increasing diagnosis rate of fragility fractures further strengthens procedural volumes within this segment. In addition, strong clinical evidence demonstrating functional mobility improvement supports physician preference. As aging demographics continue to expand across Europe, demand for vertebral body restoration procedures remains consistently high.

The Correction of the Local Kyphosis segment is expected to witness the fastest CAGR during the forecast period, driven by growing awareness of spinal alignment correction and long-term postural outcomes. Physicians are increasingly focusing not only on pain relief but also on restoring sagittal balance to improve quality of life. Technological advancements in balloon expansion systems enable better kyphotic angle correction. Rising clinical emphasis on comprehensive spinal deformity management is encouraging broader use of kyphoplasty in selected cases. Rehabilitation-focused healthcare models in Western Europe further support alignment-based treatment goals. Expanding research on the long-term benefits of kyphosis correction is anticipated to accelerate adoption in the coming years.

- By End User

On the basis of end user, the Europe kyphoplasty market is segmented into hospitals, clinics, ambulatory surgical centres, and others. The Hospitals segment dominated the market in 2025 due to the availability of advanced imaging infrastructure, multidisciplinary spine care teams, and higher procedural capacity. Most kyphoplasty procedures in Europe are performed in tertiary and specialized hospitals where complex fracture cases can be managed effectively. Favorable reimbursement frameworks in major countries further strengthen hospital-based procedural volumes. Hospitals also have greater access to skilled orthopedic surgeons and interventional radiologists trained in vertebral augmentation techniques. The presence of post-operative monitoring facilities enhances patient safety, supporting hospital dominance. Continuous investment in surgical innovation within large healthcare institutions further consolidates their leading position.

The Ambulatory Surgical Centres segment is projected to experience the fastest growth during the forecast period, supported by the increasing shift toward outpatient minimally invasive procedures. ASCs offer cost advantages and reduced hospital stay durations, making them attractive in cost-conscious healthcare systems. Improvements in anesthesia techniques and procedural efficiency enable safe same-day discharge for selected patients. Several European healthcare systems are encouraging outpatient spine interventions to optimize hospital resource utilization. Growing patient preference for shorter recovery timelines further accelerates ASC adoption. As minimally invasive technologies advance, the feasibility of performing kyphoplasty in outpatient settings is expected to expand significantly.

Europe Kyphoplasty Market Regional Analysis

- Germany dominated the Europe kyphoplasty market with the largest revenue share of 29.4% in 2025, characterized by advanced healthcare infrastructure, favorable reimbursement framework, high procedural adoption rates, and the presence of leading orthopedic and spine care centers, with increasing volumes of vertebral compression fracture treatments among the aging population

- Healthcare providers in the country highly value the clinical benefits of minimally invasive vertebral augmentation procedures, including rapid pain relief, vertebral height restoration, and reduced hospital stays compared to conservative treatment approaches

- This widespread adoption is further supported by a rapidly aging population, well-established orthopedic and interventional radiology networks, and continuous investment in advanced medical technologies, establishing kyphoplasty as a preferred treatment solution across major hospitals and specialized spine centers

The Germany Kyphoplasty Market Insight

The Germany kyphoplasty market captured the largest revenue share in 2025 within Europe, fueled by a high incidence of osteoporotic vertebral compression fractures and strong reimbursement support for minimally invasive spine procedures. Physicians increasingly prioritize vertebral augmentation techniques that provide rapid pain relief and improved mobility for elderly patients. The growing aging population, combined with well-established orthopedic and interventional radiology infrastructure, further propels procedural volumes. Moreover, the presence of advanced medical device technologies and continuous innovation in balloon kyphoplasty systems significantly contributes to market expansion across tertiary care hospitals.

France Kyphoplasty Market Insight

The France kyphoplasty market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising osteoporosis prevalence and increasing awareness regarding minimally invasive spinal treatments. The expansion of geriatric healthcare services, coupled with structured reimbursement policies, is fostering higher procedural adoption. Hospitals in France are emphasizing early fracture intervention to reduce long-term disability. In addition, growing investments in advanced imaging-guided spine procedures are supporting market growth.

U.K. Kyphoplasty Market Insight

The U.K. kyphoplasty market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing vertebral fracture incidence among the aging population and supportive public healthcare initiatives. National focus on osteoporosis screening and early diagnosis is encouraging timely intervention. The presence of skilled spine specialists and improved access to minimally invasive technologies further strengthens adoption. Emphasis on reducing hospital stay duration and improving patient recovery outcomes continues to stimulate market demand.

Italy Kyphoplasty Market Insight

The Italy kyphoplasty market is expected to expand at a considerable CAGR during the forecast period, fueled by rising geriatric demographics and growing awareness of vertebral compression fracture management. Italy’s expanding orthopedic care infrastructure and increasing adoption of interventional radiology techniques promote procedural growth. Hospitals are gradually integrating balloon kyphoplasty into standard fracture treatment pathways. The focus on enhancing quality of life for elderly patients further supports sustained market expansion.

Europe Kyphoplasty Market Share

The Europe Kyphoplasty industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Globus Medical, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Alphatec Holdings, Inc. (U.S.)

- Osseon LLC (U.S.)

- G-21 S.r.l. (Italy)

- SOMATEX Medical Technologies GmbH (Germany)

- joimax GmbH (Germany)

- Joline GmbH & Co. KG (Germany)

- IZI Medical Products, LLC (U.S.)

- Seawon Meditech Co., Ltd. (South Korea)

- Smith & Nephew plc (U.K.)

- MicroPort Scientific Corporation (China)

- Cook (U.S.)

- SPINUS (France)

- Tecres S.p.A. (Italy)

- Medacta International SA (Switzerland)

What are the Recent Developments in Europe Kyphoplasty Market?

- In June 2025, Amber Implants announced successful one-year follow-up data from its first-in-human VCFix® Spinal System clinical trial, reporting significant improvements in key clinical performance outcomes and demonstrating a strong safety profile for the treatment of vertebral compression fractures in The Netherlands

- In May 2025, Amber Implants reported that all patients in its first-in-human clinical study of the VCFix® Spinal System completed their one-year follow-up without any device-related adverse events, reinforcing clinical confidence in the novel spinal augmentation approach

- In June 2024, Amber Implants completed the enrolment of its first-in-human clinical trial for the VCFix® Spinal System, marking a significant clinical research advancement in spinal fracture treatment that may influence future kyphoplasty strategies across European healthcare settings

- In June 2024, Medtronic announced a strategic partnership with Merit Medical Systems to offer the Kyphon™ KyphoFlex™ unipedicular balloon catheter for treating vertebral compression fractures, expanding clinical options for minimally invasive spinal augmentation procedures across markets that include European distribution networks

- In October 2023, Amber Implants announced the start of its first-in-human clinical trial for the VCFix® Spinal System, a next-generation implant for vertebral compression fractures aiming to offer an alternative to traditional bone-cement-based kyphoplasty procedures. This milestone highlighted innovation in vertebral augmentation treatment modalities emerging in Europe

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。