世界の大腸がん診断市場規模、株式、動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

4.14 Billion

USD

7.89 Billion

2024

2032

USD

4.14 Billion

USD

7.89 Billion

2024

2032

| 2025 –2032 | |

| USD 4.14 Billion | |

| USD 7.89 Billion | |

| % | |

|

全体的なColorectal癌の診断の市場区分、プロダクト タイプ(器械および消耗品及び付属品)によって、テスト タイプ(腰検査、血テスト、イメージ投射検査、腫瘍マーカー、生検および他の)、癌の段階(点0、段階I、段階II、段階IIIおよび段階IV)、癌のタイプ(Adenocarcinoma、Colorectal Lymphoma、Gastrointestinalの腫瘍、カルチノイドの腫瘍、他)、癌の段階(Stage I、段階II、段階II、段階III、および段階IV)、癌のタイプ(診断および診断センター)、癌および診断センター、診断および診断センター、他

色の癌の診断の市場のサイズ

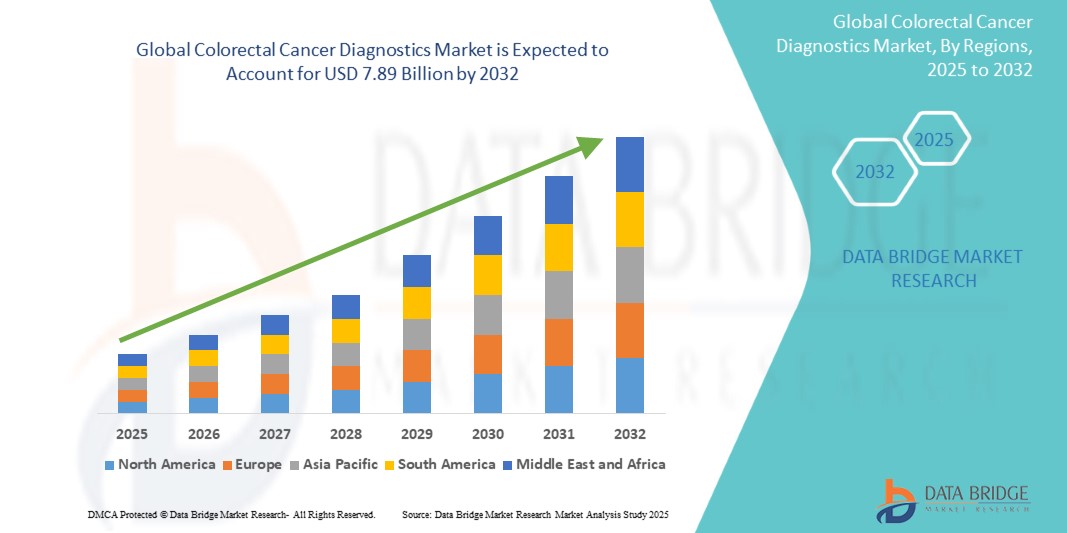

- 世界的なcolorectal癌の診断の市場のサイズはで評価されました2024年のUSD 4.14億そして到達する予定2032年までのUSD 7.89億, お問い合わせ8.40%のCAGR予報期間中

- 市場成長は、大部分は、大腸がんの有病率を高め、早期発見に対する意識を高め、診断ツールの技術的進歩により、臨床および研究設定の精度と納期の短縮につながる

- さらに、最小限の侵襲的処置、精密医学および個人化された処置の作戦のための成長した要求は高度のcolorectal癌診断解決の採用を、それによって企業の成長を著しく高める運転しています

色の癌診断市場分析

- 世界的な大腸がん診断市場は、大腸がんの予防接種による強力な成長を目撃し、早期発見に対する意識を高め、イメージング試験、液体バイオピース、および分子診断などの診断技術の継続的な進歩を目撃しています。 早期診断および改善された忍耐強い結果は世界中でヘルスケア設備を渡る高度のスクリーニングの解決の採用を運転しています

- 心癌診断のエスカレート要求は、主に技術革新、政府のスクリーニングの取り組み、および成長する高齢者の人口によって燃料を供給され、大腸がんの影響を受けやすくなります。 非侵襲的かつ正確な診断ソリューションは、臨床医と患者の両方にますます優先され、市場拡大に貢献します

- 北アメリカは、2024年に42.5%の最大の収益分配で、色素癌診断市場を支配し、確立された医療インフラ、高度なスクリーニング技術の高い採用、および重要な市場プレーヤーによる重要な投資を認めた。 米国は、病院、診断イメージングセンター、および多専門クリニックにおける色素癌診断の実装の実質的な成長を経験しました。人工知能イメージング、液体バイオサイのイノベーション、早期発見プログラム

- アジア・パシフィックは、予報期間中、大腸がん診断市場で最も急速に成長する地域であると予想され、都市化の拡大、使い捨て所得の拡大、医療インフラの拡大、がん検診プログラムの普及に向けた。 中国、インド、日本などの国は、先進的な診断の迅速な採用を目撃し、需要の高まりを期待しています。

- ザ・オブ・ザ・機器セグメントは、2024年に46.5%の最大の市場収益シェアを占めました、病院、癌の研究所および専門医院を渡る高度の診断技術の高められた採用によって運転される

レポート スコープと色素がん診断市場セグメンテーション

| アトリビュート | コロデカルがん診断キーマーケットインサイト |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

色の癌診断市場動向

早期発見と非侵襲試験の進歩

- 世界的な色素癌診断市場での有意で加速傾向は、非侵襲的なスツールベースのテスト、液体バイオピース、およびを含む高度な早期検出技術の採用の増加です。次世代シーケンシング(NGS). これらの革新は診断正確さ、忍耐強い承諾および時機を得た介入を高めます

- 例えば、非侵襲的フェカル免疫化学検査(FIT)とマルチターゲットスツールDNA検査は、人口レベルのスクリーニングにますます好まれ、色素癌や多孔質病変の早期発見を可能にします。 初期段階の診断により、生存率が向上し、治療の複雑性が低下し、医療従事者の強い採用を促進

- 分子診断および精密薬の統合は、さらに増大性癌検出である。 NGSパネルとバイオマーカーベースのアッセイにより、よりパーソナライズされたリスクアセスメント、高リスクで患者を識別し、調整されたスクリーニングスケジュールを推薦する臨床医が許可します

- 政府のスクリーニングプログラムと保険のカバレッジと相まって、大腸がんリスクの上昇意識は市場を拡大しています。 病院、専門医および診断実験室はますます患者の結果を改善するこれらの現代診断解決を組み込んでいます

- また、高精細コロノスプロテクションやAIを用いた内視鏡解析などのイメージング技術の進歩は、病変の検知率を改善し、欠損診断の最小化により、臨床意思決定の自信を強化

- 全体的に、より正確で非侵襲的、および患者に優しい診断に対する傾向は、色素がんスクリーニングおよび管理に対する期待を再構築しています。 早期発見、パーソナライズされたテスト、およびアクセス可能な診断に重点を置き、開発および新興地域の急成長を促進します

測色がん診断市場ダイナミクス

ドライバー

成長の必要性 有利性および色素癌の意識

- 世界的な大腸がんの発生率が高まり、早期発見の重要な重要性についての意識を高め、高度な診断ソリューションの需要を促進しています。 この傾向は、予防ケアと人口の多いスクリーニングプログラムのヘルスケアシステムの成長焦点を反映しています

- 例えば、2024年に、複数の大手診断会社が次世代のスツールDNA検査と高感度分子パネルを導入し、早期の検出精度を向上させ、誤った負を削減しました。 このような技術の進歩は、予測期間中に大腸がん診断市場を著しくブーストすることが期待されます

- 患者とヘルスケアプロバイダーの両方が早期診断、非侵襲的診断オプションの臨床的利点を認識しているため、液体バイオピースやフェカル免疫化学的検査(FIT)など、より高い患者のコンプライアンスと不快な不快感による結腸検査などの従来の侵襲的な手順と比較して、

- 政府および民間スクリーニングのイニシアチブの拡大は、国民の健康戦略にますます積分される大腸がんの診断をしています。 公共の意識キャンペーン、保険のカバレッジ、定期的な病院のスクリーニングプログラムは、都市と半都市地域の採用を強化しています

- さらに、パーソナライズされた治療計画による分子診断の統合により、医師は患者固有のリスクプロファイルに基づいて治療を調整し、これらの高度な診断ツールの臨床関連性を強化

- 予防医療に重点を置き、技術革新と患者の需要増加と相まって、病院、専門医院、診断ラボをグローバルに展開する強力な成長の勢いを築き続けています。

拘束/チャレンジ

新興市場での高コストと限定アクセス

- 次世代シーケンシングパネルやマルチターゲットスツールDNA検査などの高度な診断手順の比較的高いコストは、特に価格に敏感な新興地域に、より広い市場浸透への重要な障壁を維持します

- 専門化された診断実験室の限られた可用性および農村または開発区域の訓練された人員は更にアクセスを制限し、早期の検出および時機を得た処置のdisparitiesを作成します

- これらの課題を克服するには、政府の助成プログラム、ローカル診断センターとのパートナーシップ、およびアクセシビリティを高めるための費用対効果の高いテストソリューションの開発などの戦略的取り組みが必要です

- 都心部に採用が進んでいますが、先進国における市場規模拡大は、ヘルスケアインフラ、認知キャンペーン、手頃な価格のテストソリューションの提供への投資に依存します。

- 家庭用サンプルコレクションキットやポータブルポイントオブケア診断ツールなどのイノベーションは、アクセシビリティの課題に対応し、世界規模のColorectal Cancer Diagnostics市場の持続的な拡大をサポート

色の癌の診断の市場規模

市場は、製品の種類、テストの種類、がんステージ、がんの種類、年齢グループ、エンドユーザーに基づいてセグメント化されます。

製品タイプ別

製品の種類に基づいて、色素癌診断市場は、機器および消耗品および付属品に分けられます。 ザ・オブ・ザ・機器セグメントは、2024年に46.5%の最大の市場収益シェアを占めました、病院、癌の研究所および専門医院を渡る高度の診断技術の高められた採用によって運転される。 高精細コロノスコープ、内視鏡イメージングシステム、自動分析装置、分子診断プラットフォームを含む洗練された機器は、色素癌の正確な検出、ステージング、および継続的な監視において重要な役割を果たします。 これらのツールは、診断精度を高めるだけでなく、タイムリーな臨床意思決定をサポートし、最終的に患者の結果と生存率を改善します。

ザ・オブ・ザ・消耗品及び付属品の区分は2025から2032までの12.3%の最速のCAGRを目撃するために写っています、使い捨て可能なテスト キット、試薬、標本のコレクション装置および他の必要な補助プロダクトのための上昇の要求によって燃料を供給される。 これらの消耗品は、汚染のないサンプル処理を可能にし、ラボのワークフローを合理化し、効率的な大規模な集団スクリーニングプログラムを容易にします。 予防診断に関する意識を成長させ、早期がん検出のための政府および民間の取り組みの増加と組み合わせ、さらに世界中の色素がん診断における消耗品および付属品の採用を加速します。

•テスト タイプによって

検査の種類に基づいて、大腸がん診断市場は、便検査、血液検査、画像検査、腫瘍マーカー、生検などに分けられます。 スツール検査は、主に非侵襲的な性質、使いやすさ、手頃な価格、大規模な人口スクリーニングのための適合性のために、2024年に41.2%の最大の収益シェアを開催しました。 複雑な装置や手順を問わず、色素異常の早期発見を可能にし、都市や農村のヘルスケア設定に非常にアクセス可能です。 より広い採用は、45歳以上の成人向け定期的なスツールベースのスクリーニングを推薦する臨床ガイドラインを確立することにより、さらにサポートされます。

血液検査セグメントは、液体生検技術、分子診断、および高感度バイオマーカー検出の進歩によって推進される2025から2032までの13.1%の最速のCAGRを登録することが期待されます。 血液ベースの診断は、がんを早期に検出する能力、病気の進行状況をリアルタイムに監視し、パーソナライズされた治療戦略を導きます。 臨床医や患者の意識を高めるとともに、血液検査を定期的に実施するプログラムへの統合とともに、このセグメントの採用を世界的に加速しています。

• がんの段階によって

がんの段階に基づいて、大腸がん診断市場はステージ0、ステージI、ステージII、ステージIII、ステージIVに分けられます。 ステージIIは、2024年に最大38.7%の市場収益シェアを占める大腸がんで、治療がより複雑で生存率低下する先進的な段階に進む前に、がんを特定する臨床的意義を強調しています。 ステージIIの癌を検出すると、手術や補助療法などの効果的な介入を可能にし、患者の結果や生活の質を大幅に向上させます。

ステージIIIは、2025年から2032年にかけて最も速いCAGRを目撃し、全国のスクリーニングの取り組みの実施、早期発見に関する意識キャンペーン、およびイメージングおよび診断ツールの技術的進歩の増加によって燃料を供給する予定です。 段階IIIの癌の早期検出は時機を得た外科プロシージャ、精密な押すことを可能にし、そしてターゲットを絞られた治療計画は、それによって全体的な生存を高めます。 患者の意識を高める, 政府支援がんスクリーニングプログラム, 開発および新興市場での専門診断施設へのアクセスを改善し、このセグメントの急激な成長を促進しています。 世界的な大腸がん診断市場.

• 癌のタイプによって

がんの種類に基づいて、大腸がん診断市場は、アデノカルチノーマ、大腸リンパ腫、消化管腫瘍、がん腫瘍、その他に分けられます。 Adenocarcinoma は、2024 年に 44.3% の収益シェアで市場を支配し、世界規模の大腸がんの最も一般的な組織的サブタイプとして位置を強調した。 その市場優位性は、その高い優先順位、検出のための十分に確立された臨床ガイドラインによって駆動され、ルーチン色素がんスクリーニングプログラムの広範な含有量。 広範囲の研究、標準化された処置の議定書および早期検出の強い重点からの区分の利点は、集団的にadenocarcinomaを目標とする診断解決のための安定した要求を保障します。

2025年から2032年にかけて最も速いCAGRを目撃するためにGastrointestinalのstromal腫瘍はまれな腫瘍のタイプの意識を高め、診断のイメージ投射および分子テストの進歩および専門にされた研究プログラムの上昇の投資を増加させることによって燃料を供給されます。 セグメントの成長は、標的療法および精密薬のアプローチの開発によってさらに支持され、正確な検出、改善された患者結果、および効果的な病気管理を可能にします。 ヘルスケアプロバイダーは、希少がんの早期識別とパーソナライズされた治療に焦点を当てているため、このセグメントの高度な診断ツールの需要は大幅に上昇すると予想されます。

・年齢別グループ

年齢層に基づいて、大腸がん診断市場は、小児科、成人、小児科に分けられます。 大人は、2024年に49.1%の最大の市場収益シェアを保有し、45歳〜65歳の個人で大腸がんの発生率を高め、定期的なスクリーニングおよび予防医療プログラムの積極的な参加を反映しています。 このセグメントは、広範な認知キャンペーン、定期的なチェック、タイムリーな検出を促す高度な診断技術の可用性から恩恵を受けています。

2025年から2032年までの最も速いCATGを目撃するためにgeriatricの区分は、高齢化の人口の増加によって運転され、高齢化の危険因子による色素癌の影響を受けやすくなります。 このセグメントにおける成長は、高齢者の予防医療の重点を置き、年齢別スクリーニングの取り組みの広範囲にわたる実施、都市および半都市地域における診断サービスへのアクセスを改善することによって加速されます。 消化管の患者間の早期検出の上昇焦点は死亡率を減らし、全体的な生活の質を高めるために重要で、全体的な色素癌診断市場でのセグメントの成長の重要性を強調しています。

•エンドユーザーによる

エンドユーザーに基づいて、大腸がん診断市場は、病院、診断センター、がん研究センター、血管外科センター、学術研究所などに分かれています。 病院は、2024年に51.4%の収益シェアで市場を支配し、十分に確立された診断インフラ、高度なイメージング技術とラボ技術へのアクセス、熟練した腫瘍学の専門家の存在を主導しました。 病院は、初期スクリーニング、確認診断、治療計画、治療管理、および進行中のフォローアップを含むエンドツーエンドの患者ケアを提供することができます。これらは、大腸がん管理のための中央ハブです。

診断センターのセグメントは、2025年から2032年までの13.4%の最速のCAGRを目撃すると予想され、アクセス可能な外来ベースの診断サービスのための成長している患者の好みによって推進されます。 予防医療への取り組みの拡大、早期発見の重要性の認識を高め、都市部・半都市部のスクリーニングプログラムの普及が診断センターの到達を促進しています。 これらのセンターは、より短い待ち時間と柔軟な任命オプションで、しばしば、迅速かつ効率的な診断を求める患者の間でますます人気を上げる、タイムリーで、便利で専門性のある心癌検査サービスを提供しています。

色の癌の診断の市場地域の分析

- 北アメリカは、2024年に42.5%の最大の収益分配で色素癌診断市場を支配し、確立された医療インフラ、高度なスクリーニング技術の高い採用、および重要な市場プレーヤーによる重要な投資に優れました

- 市場は、AI-assistedイメージング、液体バイオプシー技術、早期検出プログラムなどの革新によって駆動され、病院、診断イメージングセンター、および多専門クリニック全体で大幅な成長を経験しました

- 高い医療費の増大と予防ケアに対する意識の向上により、地域における市場拡大に貢献

米国のColorectal癌診断市場の洞察

米国の大腸がん診断市場は、2024年に北米で最大45%の収益率を占め、堅牢な医療インフラ、高度なスクリーニング技術の高い採用、および主要な市場プレーヤーによる実質的な投資を率いています。 病院、診断イメージングセンター、およびAIアシストイメージング、液体バイオサイのイノベーション、早期検出プログラムがサポートする多専門クリニックにおける色素がん診断の迅速な実施を目撃しました。 また、最小限の侵襲試験、分子診断の統合、および外来および専門ケアセンターの拡大のための増加の需要は市場成長を後押ししています

ヨーロッパのColorectal癌の診断市場の洞察

予測期間中、欧州の測色がん診断市場は注目すべきCAGRで展開し、堅牢な医療システムでサポートし、早期がんの検出に関する意識を高め、スクリーニングプログラムを推進する政府の取り組みを推進しています。 ドイツ、イギリス、フランスなどの国々は、最小限の侵襲的な診断と分子検査ソリューションの採用を目撃しています。 ヘルスケアプロバイダーと診断会社間の外来診断センターおよびコラボレーションの拡大も、住宅や臨床設定の市場成長を促進しています。

U.K. 測色がん診断市場インサイト

U.K.カラークタールがん診断市場は、国家スクリーニングイニシアチブによって駆動される重要なCAGRで成長し、大腸がんの発生率が上昇し、早期検出の優先順位が高まっています。 先進的なイメージング技術の診断技術と統合における成長投資と組み合わせた国の強力な医療インフラは、病院、診断センター、および研究機関における革新的な色素癌検査ソリューションの採用を促進しています。

ドイツColorectal癌診断市場の洞察

ドイツの大腸がん診断市場は、高い医療費の着実に拡大し、大腸がんの罹患率を高め、精密診断の採用を増加させることが期待されています。 AIベースのイメージングおよび分子診断プラットフォームへの投資とともに、非侵襲的検査方法に関する意識を高め、病院ベースの診断施設とスタンドアローン診断施設の両方で成長を促進しています。

アジア太平洋色素癌診断市場インサイト

アジア・パシフィック・カラークタールのがん診断市場は、予測期間中に7.8%の最速のCAGRで成長し、都市化の拡大、使い捨ての収入の増加、医療インフラの拡大、がんスクリーニングプログラムの認知度の向上に取り組みます。 中国、インド、日本などの国々は、分子検査、液体バイオピース、イメージングソリューションなどの先進的な診断の迅速な採用を目撃し、早期発見とパーソナライズされた治療戦略の需要が高まっています。 がん検診プログラムや医療モダナイゼーションをサポートする政府の取り組みは、市場拡大を加速しています。

日本大腸がん診断市場動向

日本大腸がん診断市場は、国の老化人口、強固な医療システムによる勢いを増大させ、予防的腫瘍に焦点を合わせています。 高精度イメージング、内視鏡技術、および分子診断プラットフォームの採用は、病院、専門クリニック、研究センターにおける成長を促進しています。 全国スクリーニングプログラムおよび患者意識の向上は、持続的な市場開発を支援しています。

中国大腸がん診断市場インサイト

2024年にアジア・パシフィックで最大の市場収益シェアを占める中国大腸がん診断市場は、急速な都市化、ヘルスケアインフラの拡大、中級人口の上昇、早期がん検知に関する意識の高まりに至りました。 非侵襲的なスツールテスト、イメージングモダリティ、液体バイオピースなどの先進的な診断の採用が高まっています。 費用効果が大きい解決を提供する国内製造業者の存在と結合される強い政府サポートは病院、診断中心および専門医院の市場成長を促進します。

色の癌診断市場シェア

色の癌診断の企業は主に下記のものを含んでいる十分に確立された会社によって、導きます:

- F.ホフマン・ラ・ロチェ株式会社(スイス)

- アボット(米国)

- Illumina(アメリカ)

- QIAGEN(オランダ)

- サーモフィッシャーサイエンス株式会社(米国)

- クエスト診断株式会社(米国)

- メルク・カーガ(ドイツ)

- 株式会社ホロジック(米国)

- Siemens Healthineers AG(ドイツ)

- BD(アメリカ)

- Myriad Genetics, Inc.(米国)

- PlexBio株式会社(韓国)

- フジフイルム株式会社(日本)

- キャノンメディカルシステムズ株式会社(日本)

- メドニカ株式会社(韓国)

- MinFoundの医療機器Co.、株式会社(中国)

- バイオロード研究所(米国)

- ノイソフト株式会社(中国)

- バイオファイア診断(米国)

- アジレントテクノロジーズ株式会社(米国)

国際色素癌診断市場の最新動向

- 2024年7月、ガードラント・ヘルスは、シールド・血液検査が45歳以上の成人における色素癌の第一次スクリーニングオプションとしてFDA承認を受けたことを発表しました。 この承認は、ECLIPSE研究の結果に基づいていました, 20,000 + 患者登録試験のパフォーマンスを評価する研究. シールドテストは、色素癌に関連したDNA変異と流行の変化を検出し、従来のスクリーニング方法に非侵襲的代替を提供

- 2024年4月、Freenomeは、PreEMPTのCRC研究のトップライン結果を発表しました。この試験は、早期発色性癌検出のための血液ベースの試験の最初のバージョンを検証しました。 この研究では、非先進的な色素形成神経症に対する色素癌および91.5%の特異性に対する79.2%の感受性を含む、すべての第一次エンドポイントに会いました。 プレムプトCRCは、米国における平均リスクの成人の実質的な多様性を反映した48,995人の参加者に登録された、色素癌の血液ベースのテストの最大の研究です。

- 2023年10月、国立がん研究所は、大腸内視鏡検査におけるコンピュータ断線検出(CAD)の統合に関する研究発表を行いました。 この研究では、CADシステムは、コロノスコピエの間により多くのポリープを識別し、色素癌の検出率を潜在的に改善する臨床医を助けることができることを強調した。 しかしながら、CADシステムががんに進行する可能性が高いポリープとがんに進行する可能性が高いものと、そうでないものと必ずしも異なる可能性があると指摘した。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。