Global Podiatry Services Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

406.97 Million

USD

740.26 Million

2024

2032

USD

406.97 Million

USD

740.26 Million

2024

2032

| 2025 –2032 | |

| USD 406.97 Million | |

| USD 740.26 Million | |

| % | |

치료 유형별 글로벌 정형외과 서비스 시장 세분화(보존적 치료 및 수술적 치료), 환자 유형(성인, 노인, 소아), 시술 유형(발 수술, 발목 수술 및 일상적인 정형외과 시술), 최종 용도(병원, 정형외과 클리닉 및 기타) - 2032년까지 산업 동향 및 예측

정형외과 서비스 시장 규모

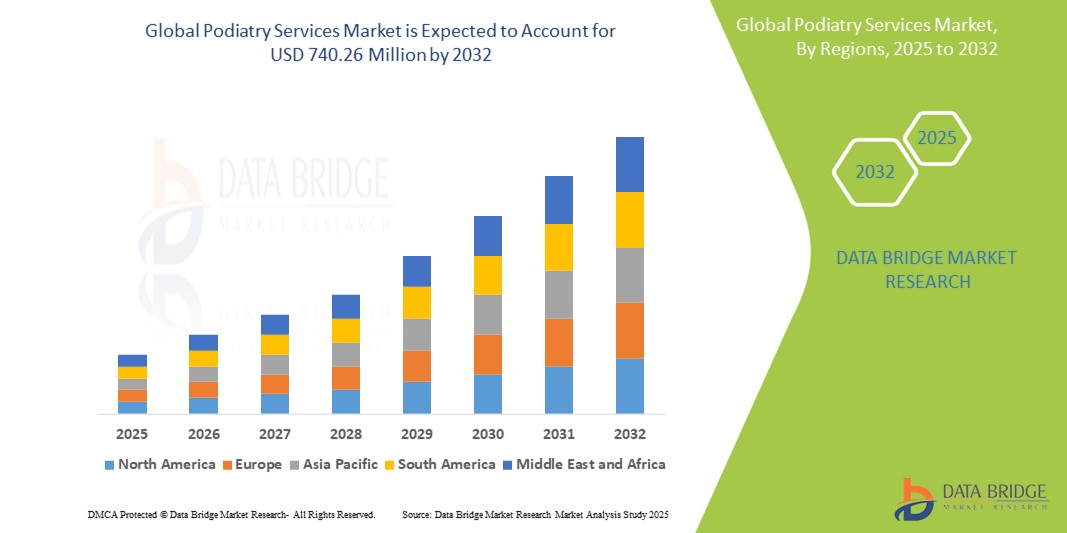

- 글로벌 정형외과 서비스 시장은 2024년에 4억 697만 달러 규모로 평가되었으며 2032년까지 7억 4,026만 달러 에 이를 것으로 예상됩니다 .

- 2025년부터 2032년까지의 예측 기간 동안 시장은 주로 당뇨병 관련 발 질환의 유병률 증가와 발 건강 및 전문 치료에 대한 인식 증가에 따라 연평균 성장률 6.90%로 성장할 것으로 예상됩니다.

- 이러한 성장은 노인 인구 증가, 관절염 및 당뇨병 과 같은 만성 질환의 발병률 증가 , 고급 발 관리 솔루션 및 최소 침습적 시술에 대한 수요 증가와 같은 요인에 의해 촉진됩니다.

정형외과 서비스 시장 분석

- 족부외과 서비스는 발, 발목, 하지 질환의 예방, 진단 및 치료에 중점을 둡니다. 여기에는 족저근막염 , 건막류, 당뇨병성 족부 궤양, 스포츠 부상 등이 포함됩니다. 이러한 서비스는 특히 고령층과 당뇨병 환자의 이동성과 삶의 질을 유지하는 데 필수적입니다.

- 전 세계적으로 당뇨병과 비만의 발병률이 증가하고 발 건강에 대한 인식이 높아짐에 따라 족부 전문의 서비스 수요가 크게 증가하고 있습니다. 당뇨병성 발 관리만으로도 서비스 이용률의 상당 부분을 차지하며, 특히 당뇨병 유병률이 높은 지역에서 더욱 그렇습니다.

- 북미는 잘 확립된 의료 시스템, 보상 체계, 정기적인 발 관리를 원하는 노인 인구의 증가로 인해 정형외과 서비스의 주요 지역 중 하나로 돋보입니다.

- 예를 들어, 미국에서는 정형외과 진료와 당뇨병성 발 치료가 꾸준히 증가하고 있으며, 정형외과 진료소와 다학제 당뇨병 치료 센터가 외래 진료 제공에 핵심적인 역할을 하고 있습니다.

- 전 세계적으로 발병의학 서비스는 예방 건강 관리의 중요한 구성 요소로 인식되고 있으며, 특히 당뇨병과 같은 만성 질환 관리, 조기 개입을 통한 입원 감소, 장기적인 환자 결과 개선에 중요한 역할을 합니다.

보고서 범위 및 정형외과 서비스 시장 세분화

|

속성 |

정형외과 서비스 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 업체 등 시장 시나리오에 대한 통찰력 외에도 수입 수출 분석, 생산 능력 개요, 생산 소비 분석, 가격 추세 분석, 기후 변화 시나리오, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선택 기준, PESTLE 분석, Porter 분석 및 규제 프레임워크가 포함됩니다. |

정형외과 서비스 시장 동향

"고급 진단 도구와 원격 진료의 통합 확대"

- 글로벌 정형외과 서비스 시장의 두드러진 추세는 고급 진단 도구와 원격 정형외과 솔루션의 통합이 증가하고 있다는 것입니다.

- 이러한 기술은 진단 정확도를 높이고 발 관리 접근성을 확대하며, 특히 외딴 지역과 의료 서비스가 부족한 지역에서 더욱 효과적입니다. 디지털 보행 분석 시스템, 압력 매핑, 스마트 깔창과 같은 도구는 발 생체역학 및 압력 분포에 대한 실시간 통찰력을 제공합니다.

- 예를 들어, 디지털 보행 분석은 비정상적인 보행 패턴을 조기에 감지하는 데 도움이 되어 평발이나 당뇨병 신경병증과 같은 상태에 대한 시기적절한 개입을 가능하게 하여 치료 결과와 환자 이동성을 개선합니다.

- Telepodiatry enables virtual consultations, follow-ups, and monitoring of chronic foot conditions, reducing the need for in-person visits and improving care continuity, especially for elderly and mobility-challenged patients

- This trend is transforming traditional podiatric care by making it more accessible, personalized, and technology-driven, thereby boosting patient engagement and driving growth in the podiatry services market

Podiatry Services Market Dynamics

Driver

“Rising Prevalence of Diabetes and Foot-Related Complications”

- The increasing global prevalence of diabetes is a major driver of the podiatry services market, as diabetic patients are at high risk of developing foot complications such as ulcers, infections, and neuropathy

- These complications often lead to reduced mobility and, in severe cases, amputations if not managed promptly—necessitating regular foot examinations and specialized care from podiatrists

- As populations age and lifestyle-related diseases such as obesity and type 2 diabetes become more common, the need for podiatric services continues to grow, especially in countries with high diabetes burdens

- The Preventive care, including diabetic foot screenings and education on proper foot hygiene, has become a focal point in healthcare strategies, driving demand for podiatry services in both hospital settings and outpatient clinics

For instance,

- In November 2022, the International Diabetes Federation reported that approximately 537 million adults globally were living with diabetes, with numbers expected to rise to 643 million by 2030—many of whom will require foot care services.

- In March 2023, the American Podiatric Medical Association highlighted that early intervention by podiatrists can reduce diabetes-related lower-limb amputations by up to 85%, emphasizing the crucial role of podiatry in chronic disease management

- Consequently, the growing diabetic population and the associated risk of foot complications continue to drive the expansion and necessity of podiatry services across global healthcare systems

Opportunity

“Enhancing Podiatric Care Through AI and Smart Health Technologies”

- The integration of artificial intelligence (AI) and smart health technologies presents a significant opportunity in the podiatry services market by transforming how foot-related conditions are diagnosed, monitored, and managed.

- AI-powered tools can analyze gait patterns, foot pressure distributions, and patient history to detect early signs of conditions such as diabetic foot ulcers, plantar fasciitis, or neuropathy, enabling timely and personalized intervention

- Smart insoles and wearable sensors, connected to AI-driven platforms, allow for continuous remote monitoring of patients at risk, providing alerts for pressure anomalies or changes in mobility patterns, thereby reducing the risk of complications

For instance,

- In August 2023, a study published in the Journal of Foot and Ankle Research highlighted the effectiveness of AI-based gait analysis in early detection of diabetic foot complications, significantly reducing the need for emergency interventions and hospitalizations

- In October 2024, the British Journal of Sports Medicine reported that wearable tech integrated with AI algorithms successfully predicted and prevented sports-related foot injuries in athletes through real-time biomechanical monitoring

- The application of AI in podiatry is also enhancing patient engagement and clinical decision-making, with platforms offering visual feedback, treatment tracking, and predictive analytics—ultimately improving patient outcomes and streamlining podiatric workflows

- As healthcare moves toward preventive, data-driven models, the adoption of AI and smart health technologies in podiatry services offers immense potential to reduce long-term healthcare costs and expand access to high-quality foot care

Restraint/Challenge

“Limited Access and Affordability of Specialized Podiatric Care”

- One of the major challenges in the global podiatry services market is the limited access to specialized foot care services, particularly in low-income and rural areas where healthcare infrastructure is underdeveloped

- The cost of podiatric treatments, including advanced diagnostics, orthotic devices, and surgical procedures, can be prohibitive for patients without adequate insurance coverage, leading to delayed or forgone care.

- In addition, the shortage of trained podiatrists in many regions further restricts access to timely and quality foot care, contributing to the progression of preventable conditions and increased risk of complications, especially among diabetic patients

For instance,

- In September 2023, the World Health Organization highlighted that many developing countries face a critical shortage of foot care professionals, which significantly limits their capacity to manage diabetic foot complications and prevent amputations

- In April 2024, a report by the Global Health Access Initiative emphasized that out-of-pocket expenses for custom orthotics and regular podiatric checkups often discourage patients from seeking continuous care, particularly in underserved communities

- Consequently, these challenges create disparities in the availability and quality of podiatry services, ultimately hindering the growth of the market and underscoring the need for policy reforms, insurance support, and workforce development to bridge the care gap

Podiatry Services Market Scope

The market is segmented on the basis of treatment type, patient type, procedure type and end use.

|

Segmentation |

Sub-Segmentation |

|

By Treatment Type |

|

|

By Patient Type |

|

|

By Procedure Type |

|

|

By End Use |

|

정형외과 서비스 시장 지역 분석

“ 북미는 정형외과 서비스 시장에서 가장 큰 비중을 차지하는 지역입니다 .”

- 북미는 강력한 의료 인프라, 발 건강에 대한 높은 인식, 당뇨병 및 비만과 같은 만성 질환의 유병률 증가에 힘입어 글로벌 발병학 서비스 시장을 선도하고 있습니다.

- 미국은 발병원 진료소의 높은 집중도, 유리한 보상 구조, 그리고 첨단 진단 및 치료 발병원 진료에 대한 광범위한 접근성으로 인해 시장 점유율이 높습니다.

- 관절염, 신경병증, 운동 장애 등 발 관련 합병증에 더 취약한 고령 인구 증가로 인해 예방 및 수술적 정형외과 서비스에 대한 수요가 계속해서 증가하고 있습니다.

- APMA(American Podiatric Medical Association)와 같은 전문 조직의 존재와 정형외과 교육 및 연구에 대한 지속적인 투자는 이 지역의 시장 지배력에 크게 기여합니다.

“ 아시아 태평양 지역이 가장 높은 성장률을 기록할 것으로 예상됩니다 .”

- 아시아 태평양 지역은 당뇨병 인구 증가, 발 관리에 대한 인식 증가, 전문 의료 서비스 접근성 확대로 인해 발병의학 서비스 시장에서 가장 빠른 성장을 보일 것으로 예상됩니다.

- 중국, 인도, 호주 등의 국가들은 당뇨병과 당뇨병성 족부궤양, 말초신경병증 등 관련 합병증의 증가율로 인해 주요 시장으로 부상하고 있습니다.

- 선진 의료 시스템과 고령화 사회를 갖춘 일본과 한국도 특히 노인 발 관리 및 재활 분야에서 정형외과 서비스에 대한 수요를 늘리고 있습니다.

- 당뇨병 치료를 장려하는 정부 이니셔티브와 도시 지역에서 발병학 교육 프로그램 및 클리닉의 존재감이 증가함에 따라 시장 개발이 가속화되고 있습니다.

- 또한, 지역 의료 서비스 제공자와 국제 정형외과 전문의 간의 협력으로 서비스 품질과 인지도가 향상되어 아시아 태평양 지역이 글로벌 시장의 중요한 성장 동력이 되고 있습니다.

정형외과 서비스 시장 점유율

시장 경쟁 구도는 경쟁사별 세부 정보를 제공합니다. 여기에는 회사 개요, 회사 재무 상태, 매출 창출, 시장 잠재력, 연구 개발 투자, 신규 시장 진출, 글로벌 입지, 생산 시설 및 설비, 생산 능력, 회사의 강점과 약점, 제품 출시, 제품 종류 및 범위, 응용 분야별 우위 등이 포함됩니다. 위에 제공된 데이터는 해당 회사의 시장 집중도와 관련된 데이터입니다.

시장에서 활동하는 주요 시장 리더는 다음과 같습니다.

- 종합병원협회 (미국)

- Kaiser Foundation Health Plan, Inc. (미국)

- 런던 포디아트리 센터 (영국)

- Royal Free Hospital NHS Foundation Trust (영국)

- 포티스 헬스케어 (인도)

- 베이징푸화국제병원(중국)

- 숀 클리니크 SE(독일)

- 어센션(미국)

- 메이요 의학 교육 및 연구 재단(MFMER)(미국)

- 맥스 헬스케어(인도)

- 너필드 헬스(영국)

- 램지 헬스케어(호주)

- HCA 관리 서비스, LP(미국)

- TH 메디컬(미국)

- 유니버설 헬스 서비스(US)

- 클리블랜드 클리닉(미국)

- 가이스 앤 세인트 토마스 NHS 재단 신탁(영국)

- 뉴욕 풋 센터(미국)

- Mid-Atlantic, LLC(미국)의 발 및 발목 전문의

- Capron Co Inc. (미국)

글로벌 정형외과 서비스 시장의 최신 동향

- 2023년 9월, 족부 전문 병원들은 3D 프린팅 기술을 접목하여 환자 개개인의 생체 역학에 맞춘 맞춤형 보조 깔창을 제작하기 시작했습니다. 이러한 맞춤형 보조 깔창은 환자의 편안함과 치료 결과를 개선하는 동시에 생산 비용과 처리 시간을 단축하고 있습니다.

- 2023년 9월, 족부 전문 클리닉에서 스위프트 마이크로파 치료(Swift Microwave Therapy)와 비디오 보행 분석(Video Gait Analysis) 도입률이 눈에 띄게 증가했습니다. 스위프트 마이크로파 치료는 발바닥 사마귀 치료에 비침습적 방법을 제공하며, 비디오 보행 분석은 생체역학적 평가의 진단 정확도를 향상시킵니다.

- 2023년 7월, Premier Podiatry Group은 Lake Ridge Podiatry와의 전략적 합병을 발표하며 미국 북동부 지역으로 사업 영역을 확장하고 서비스 제공 범위를 확대했습니다. 이는 족부 치료 서비스 부문의 지속적인 통합 추세를 반영합니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.