Asia Pacific Ehealth Market

Размер рынка в млрд долларов США

CAGR :

%

USD

12.50 Billion

USD

82.48 Billion

2025

2033

USD

12.50 Billion

USD

82.48 Billion

2025

2033

| 2026 –2033 | |

| USD 12.50 Billion | |

| USD 82.48 Billion | |

| % | |

|

Asia-Pacific eHealth Market Segmentation, By Offering (Solutions and Services), Deployment (Cloud and On-Premises), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Functionality (Content Management System, Group Messaging, Dashboard, Video Sessions, Social Support, and Others), Technology (Internet of Things (IoT), Chatbots, Artificial Intelligence, Block Chain and Big Data, and Others), End User (Healthcare Providers, Payers, Healthcare Consumers, Pharmacies, and Others)- Industry Trends and Forecast to 2033

Asia-Pacific eHealth Market Size

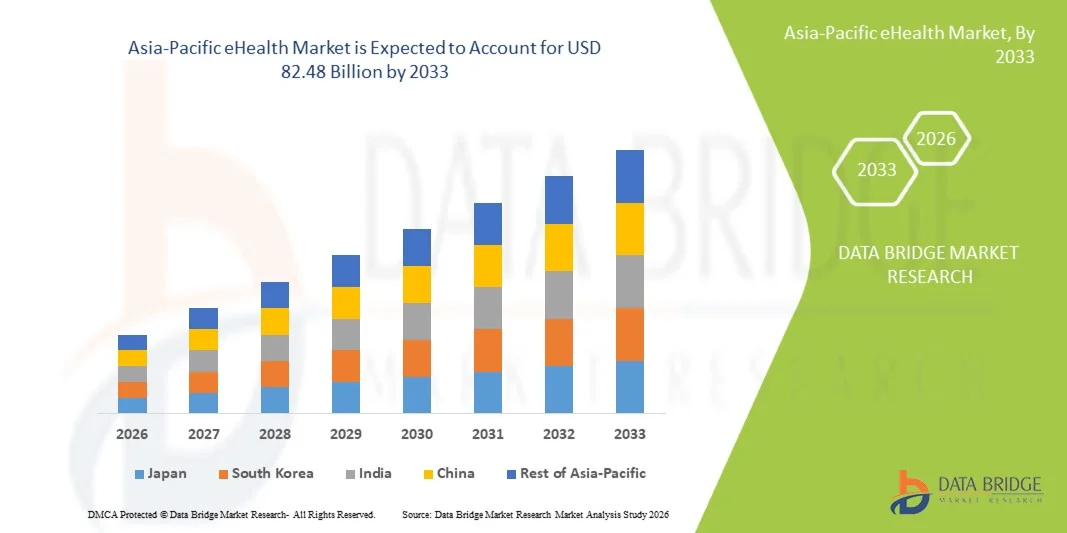

- The Asia-Pacific eHealth market size was valued at USD 12.50 billion in 2025 and is expected to reach USD 82.48 billion by 2033, at a CAGR of 26.6% during the forecast period

- The market growth is largely fueled by the rapid adoption of digital healthcare solutions, increasing penetration of smartphones and internet connectivity, and the expansion of telemedicine, electronic health records, and mobile health applications across the region

- Furthermore, rising healthcare expenditure, supportive government initiatives for healthcare digitization, and growing demand for accessible, efficient, and patient-centric care are driving the adoption of eHealth platforms, thereby significantly accelerating the market growth in the Asia-Pacific region

Asia-Pacific eHealth Market Analysis

- eHealth solutions in countries across the Asia-Pacific region, including China, India, Japan, South Korea, and Australia, encompassing digital healthcare platforms such as telemedicine systems, electronic health records, mobile health applications, and health analytics tools, are increasingly vital components of modern healthcare delivery systems in both public and private settings due to their ability to enhance accessibility, improve clinical efficiency, and enable data-driven, patient-centric care

- The escalating demand for eHealth is primarily fueled by the rapid digital transformation of healthcare infrastructure, increasing penetration of smartphones and internet connectivity, growing prevalence of chronic diseases, aging populations in countries such as Japan and South Korea, and a rising preference for remote consultations and continuous patient monitoring solutions

- China dominated the Asia-Pacific eHealth market with the largest revenue share of 35.6% in 2025, driven by large-scale government-led digital health initiatives, widespread hospital digitization, strong investments in AI-enabled healthcare technologies, and extensive adoption of cloud-based health platforms across urban healthcare systems

- India is expected to be the fastest growing country in the Asia-Pacific eHealth market during the forecast period due to increasing government support for digital health programs, rapid expansion of telemedicine services, improving digital infrastructure, and rising demand for affordable and accessible healthcare solutions across both urban and rural populations

- Cloud segment dominated the eHealth market with a market share of 62.4% in 2025, driven by its scalability, cost-effectiveness, and ease of integration with existing healthcare systems, particularly among healthcare providers and enterprises seeking flexible, interoperable, and secure digital health infrastructure

Report Scope and Asia-Pacific eHealth Market Segmentation

|

Attributes |

Asia-Pacific eHealth Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific eHealth Market Trends

“Expansion of AI-Driven Telehealth and Integrated Digital Health Platforms”

- A significant and accelerating trend in the Asia-Pacific eHealth market is the increasing integration of artificial intelligence (AI) and cloud-based digital health platforms such as telemedicine systems, electronic health records, and mobile health applications, enhancing accessibility, efficiency, and continuity of care across healthcare ecosystems

- For instance, AI-enabled telemedicine platforms and virtual care solutions are being widely deployed in countries such as India and China, allowing patients to consult physicians remotely while improving diagnostic accuracy and reducing in-person hospital visits

- AI integration in eHealth enables features such as predictive analytics for disease risk assessment, automated triaging of patients, and intelligent clinical decision support systems that assist healthcare providers in delivering personalized and data-driven treatments over time

- The seamless integration of eHealth platforms with wearable devices and IoT-enabled health monitoring tools facilitates real-time tracking of patient vitals, enabling centralized management of health data across hospitals, clinics, and homecare settings through unified dashboards

- This trend toward more intelligent, interoperable, and patient-centric digital healthcare ecosystems is reshaping expectations for healthcare delivery, with companies and providers increasingly focusing on AI-enabled automation, remote monitoring, and voice-assisted health services across both urban and rural populations

- Furthermore, the growing use of mobile health applications and patient engagement platforms is empowering individuals to actively manage their health through access to digital prescriptions, appointment scheduling, and personalized wellness insights

Asia-Pacific eHealth Market Dynamics

Driver

“Growing Need Due to Rising Healthcare Demand and Digital Transformation Initiatives”

- The increasing burden of chronic diseases, coupled with rapid digital transformation of healthcare systems and government-led initiatives promoting digital health adoption, is a significant driver for the heightened demand for eHealth solutions across Asia-Pacific countries

- For instance, national digital health missions and telemedicine programs launched in countries such as India are advancing interoperable health records and expanding access to remote consultations, strengthening the adoption of eHealth platforms across the region

- As healthcare providers and patients seek improved accessibility and efficiency, eHealth solutions offer features such as remote consultations, electronic health records, and real-time health monitoring, providing a compelling alternative to traditional healthcare delivery models

- Furthermore, the growing penetration of smartphones, internet connectivity, and cloud infrastructure is enabling seamless access to digital health services, making eHealth an integral component of modern healthcare ecosystems across both developed and emerging economies

- The convenience of virtual care, reduced healthcare costs, and improved patient engagement through mobile applications and connected devices are key factors propelling the adoption of eHealth solutions in both public and private healthcare sectors, further supported by increasing investments in health IT infrastructure

- Additionally, rising investments from private healthcare providers and technology companies in digital health startups and platforms are accelerating innovation and expanding the availability of advanced eHealth solutions across the region

- The increasing focus on preventive healthcare and population health management is also encouraging healthcare systems to adopt eHealth tools for early diagnosis, continuous monitoring, and efficient management of long-term patient outcomes

Restraint/Challenge

“Data Privacy Concerns and Regulatory Compliance Complexity”

- Concerns surrounding data privacy, cybersecurity risks, and the secure handling of sensitive patient information pose a significant challenge to broader adoption of eHealth solutions across Asia-Pacific markets

- For instance, reports of data breaches and vulnerabilities in digital healthcare systems have raised concerns among healthcare providers and patients regarding the safety of cloud-based platforms and interconnected health networks

- Addressing these challenges through robust encryption standards, secure authentication mechanisms, and compliance with regional data protection regulations is critical for building trust and ensuring safe deployment of eHealth technologies

- While governments are introducing stricter regulatory frameworks for digital health data, compliance requirements across different countries can be complex and vary significantly, creating operational and integration challenges for healthcare providers and technology vendors

- Overcoming these challenges through strengthened cybersecurity infrastructure, standardized data governance policies, and increased awareness among stakeholders will be essential for sustaining long-term growth and widespread adoption of eHealth solutions across the region

- Another key challenge is the lack of standardized interoperability between different healthcare systems and platforms, which can hinder seamless data exchange and limit the effectiveness of integrated eHealth ecosystems

- Furthermore, limited digital literacy among patients and healthcare professionals in certain developing countries can slow down adoption and reduce the overall efficiency of eHealth implementation across diverse healthcare settings

Asia-Pacific eHealth Market Scope

The market is segmented on the basis of offering, deployment, enterprise size, functionality, technology, and end user.

- By Offering

On the basis of offering, the eHealth market is segmented into solutions and services. The solutions segment dominated the market with the largest market revenue share of 64.5% in 2025, driven by the widespread adoption of electronic health records (EHR), telemedicine platforms, mobile health applications, and clinical decision support systems across hospitals and healthcare institutions. Healthcare providers increasingly prefer integrated digital solutions that streamline operations, improve patient outcomes, and enable centralized data management. The demand is further supported by government-led digitization initiatives and the need for interoperable healthcare systems. The availability of advanced analytics, AI-enabled diagnostics, and cloud-based health platforms also strengthens the dominance of the solutions segment in both public and private healthcare settings.

The services segment is anticipated to witness the fastest growth rate of 22.8% from 2026 to 2033, fueled by increasing demand for implementation, integration, consulting, maintenance, and support services associated with eHealth systems. As healthcare organizations adopt complex digital infrastructures, the need for specialized services to ensure seamless deployment and optimization is rising. Managed services, in particular, are gaining traction among small and medium healthcare providers that lack in-house IT expertise. Additionally, continuous system upgrades, cybersecurity support, and data management services are contributing to the rapid expansion of this segment across emerging economies in Asia-Pacific.

- By Deployment

On the basis of deployment, the eHealth market is segmented into cloud and on-premises. The cloud segment dominated the market with the largest market revenue share of 62.4% in 2025, driven by its scalability, cost efficiency, and ease of access across multiple healthcare facilities. Cloud-based eHealth solutions enable real-time data sharing, remote access to patient records, and seamless collaboration among healthcare professionals, making them highly suitable for large hospital networks and integrated care systems. The growing adoption of SaaS-based healthcare platforms and increasing investments in cloud infrastructure further support this dominance. Cloud deployment also reduces the burden of IT maintenance and infrastructure costs, making it highly attractive for both large enterprises and smaller healthcare providers.

The on-premises segment is expected to witness the fastest growth rate of 18.5% from 2026 to 2033, driven by increasing concerns over data privacy, regulatory compliance, and data sovereignty, particularly in countries with strict healthcare data regulations. Some healthcare institutions prefer on-premises deployment for greater control over sensitive patient data and customized system configurations. Additionally, large hospitals and government healthcare organizations with established IT infrastructure continue to invest in on-premises solutions for mission-critical applications where security and control are prioritized.

- By Enterprise Size

On the basis of enterprise size, the eHealth market is segmented into large enterprises and small and medium enterprises (SMEs). The large enterprises segment dominated the market with the largest market revenue share of 58.7% in 2025, driven by their strong financial capabilities, advanced IT infrastructure, and early adoption of digital healthcare technologies. Large hospitals, healthcare networks, and multinational healthcare organizations are increasingly implementing comprehensive eHealth systems such as EHRs, telehealth platforms, and integrated analytics solutions to enhance operational efficiency and patient care. Their ability to invest in sophisticated technologies and manage large-scale digital transformation projects contributes significantly to segment dominance.

The SMEs segment is expected to witness the fastest growth rate of 23.6% from 2026 to 2033, fueled by increasing affordability of cloud-based eHealth solutions and growing awareness of digital healthcare benefits among smaller providers. SMEs are rapidly adopting scalable and subscription-based models that require lower upfront investments while offering essential functionalities such as teleconsultation, patient management, and billing systems. Government support programs and digital health initiatives targeting smaller healthcare providers are further accelerating adoption across developing countries in Asia-Pacific.

- By Functionality

On the basis of functionality, the eHealth market is segmented into content management systems, group messaging, dashboards, video sessions, social support, and others. The video sessions segment dominated the market with the largest market revenue share of 28.9% in 2025, driven by the rapid adoption of telemedicine and virtual consultations across healthcare systems. Video-based consultations provide real-time interaction between patients and healthcare providers, improving accessibility and reducing the need for physical visits. The COVID-19 pandemic significantly accelerated the adoption of video consultation platforms, and this trend continues as patients and providers increasingly prefer remote care options. Integration of video sessions with EHRs and scheduling systems further enhances usability and efficiency.

The AI-enabled dashboard and analytics segment is expected to witness the fastest growth rate of 24.1% from 2026 to 2033, driven by the increasing need for real-time data visualization, performance tracking, and clinical decision support. Dashboards integrated with AI and big data analytics enable healthcare providers to monitor patient outcomes, identify trends, and make informed decisions quickly. The growing emphasis on data-driven healthcare and population health management is accelerating the adoption of advanced dashboard functionalities across hospitals and healthcare organizations.

- By Technology

On the basis of technology, the eHealth market is segmented into Internet of Things (IoT), chatbots, artificial intelligence, blockchain, big data, and others. The artificial intelligence segment dominated the market with the largest market revenue share of 31.4% in 2025, driven by its wide-ranging applications in diagnostics, predictive analytics, personalized treatment, and clinical decision support systems. AI-powered tools are increasingly being integrated into telehealth platforms, imaging systems, and patient monitoring solutions, enhancing accuracy and efficiency in healthcare delivery. The growing availability of healthcare data and advancements in machine learning algorithms are further supporting the dominance of AI in the eHealth ecosystem.

The Internet of Things (IoT) segment is expected to witness the fastest growth rate of 25.3% from 2026 to 2033, driven by the increasing adoption of connected medical devices and wearable health monitoring technologies. IoT enables continuous real-time monitoring of patient vitals, remote patient management, and seamless data transmission between devices and healthcare platforms. The rising demand for home healthcare solutions, coupled with advancements in sensor technologies and connectivity infrastructure, is accelerating the adoption of IoT-based eHealth solutions across the region.

- By End User

On the basis of end user, the eHealth market is segmented into healthcare providers, payers, healthcare consumers, pharmacies, and others. The healthcare providers segment dominated the market with the largest market revenue share of 49.2% in 2025, driven by the extensive adoption of eHealth solutions by hospitals, clinics, and diagnostic centers to improve operational efficiency, patient care, and data management. Providers are the primary users of electronic health records, telemedicine platforms, and clinical management systems, making them the largest contributors to market revenue. The increasing need for integrated healthcare systems and interoperability between departments further strengthens this segment’s dominance.

The healthcare consumers segment is expected to witness the fastest growth rate of 26.0% from 2026 to 2033, driven by rising awareness of digital health tools, increasing use of mobile health applications, and growing preference for self-care and remote consultations. Patients are increasingly engaging with wearable devices, health tracking apps, and teleconsultation services to monitor their health and access care conveniently. The shift toward patient-centric healthcare and increased digital literacy across Asia-Pacific populations are key factors driving rapid growth in this segment.

Asia-Pacific eHealth Market Regional Analysis

- China dominated the Asia-Pacific eHealth market with the largest revenue share of 35.6% in 2025, driven by large-scale government-led digital health initiatives, widespread hospital digitization, strong investments in AI-enabled healthcare technologies, and extensive adoption of cloud-based health platforms across urban healthcare systems

- Healthcare providers and consumers in China increasingly value the accessibility, efficiency, and scalability offered by eHealth solutions, including cloud-based platforms, mobile health applications, and integrated hospital information systems that enhance patient care and operational efficiency

- This widespread adoption is further supported by rapid urbanization, a large patient population, expanding healthcare infrastructure, and strong participation from both public and private sectors in advancing digital healthcare ecosystems, establishing China as a key contributor to the growth of the Asia-Pacific eHealth market

The China eHealth Market Insight

China dominated the Asia-Pacific eHealth market with the largest revenue share of 35.6% in 2025, driven by strong government support for digital healthcare transformation, widespread adoption of telemedicine platforms, and large-scale deployment of electronic health records across hospitals and healthcare institutions. The country’s healthcare providers are increasingly prioritizing integrated digital solutions to improve efficiency, patient outcomes, and data management. Growing investments in AI-enabled diagnostics, cloud-based healthcare platforms, and big data analytics are further accelerating market growth. Additionally, China’s large population base and expanding healthcare infrastructure continue to create significant demand for scalable and advanced eHealth solutions.

Japan eHealth Market Insight

The Japan eHealth market is experiencing steady growth due to its aging population, advanced healthcare infrastructure, and strong emphasis on technological innovation. The country’s healthcare providers are increasingly adopting electronic health records, remote patient monitoring systems, and telemedicine services to improve care delivery and manage chronic conditions efficiently. Integration of AI, robotics, and IoT-enabled devices is also enhancing healthcare automation and diagnostics. Furthermore, Japan’s focus on precision medicine and digital health initiatives is supporting the adoption of sophisticated eHealth platforms across hospitals and clinics.

India eHealth Market Insight

The India eHealth market accounted for a significant market share in Asia-Pacific in 2025, attributed to rapid digital transformation in healthcare, increasing smartphone and internet penetration, and strong government initiatives such as national digital health missions. India is witnessing growing adoption of telemedicine, mobile health applications, and cloud-based electronic health record systems across urban and rural healthcare settings. The expanding middle-class population, rising healthcare awareness, and increasing demand for affordable and accessible healthcare services are key factors driving market growth. Additionally, the presence of a large patient base and growing investments from both public and private sectors are further supporting eHealth adoption in the country.

Australia eHealth Market Insight

The Australia eHealth market is witnessing steady expansion driven by well-established healthcare infrastructure, strong regulatory frameworks, and high adoption of digital health technologies. Healthcare providers in the country are increasingly leveraging electronic health records, telehealth platforms, and integrated healthcare systems to enhance patient care and operational efficiency. Government-led initiatives supporting digital health interoperability and data sharing are further accelerating adoption. Moreover, increasing demand for remote healthcare services, particularly in rural and remote areas, is contributing to the growing use of eHealth solutions across the country.

Asia-Pacific eHealth Market Share

The Asia-Pacific eHealth industry is primarily led by well-established companies, including:

- Tencent Holdings Limited (China)

- Alibaba Health Information Technology Limited (China)

- WeDoctor Holdings Limited (China)

- JD Health International Inc (China)

- Practo Technologies Pvt. Ltd (India)

- HealthifyMe (India)

- mFine (India)

- Halodoc (Indonesia)

- MyDoc Pte. Ltd (Singapore)

- Samsung Electronics Co. Ltd (South Korea)

- Koninklijke Philips N.V. (Netherlands)

- Cisco Systems, Inc. (U.S.)

- IBM Corporation (U.S.)

- Epic Systems Corporation (U.S.)

- Allscripts Healthcare, LLC (U.S.)

- McKesson Corporation (U.S.)

- AT&T Inc. (U.S.)

- QSI Management, LLC (U.S.)

- Vodafone Group Plc (U.K.)

What are the Recent Developments in Asia-Pacific eHealth Market?

- In January 2026, Asia-Pacific digital health funding rose 14% year-on-year to USD 2.4 billion, with Australia emerging as the top-funded market ahead of China and India, signaling a shift in investment leadership and concentrated capital deployment into tech-driven healthcare solutions in the region

- In December 2025, Transform Health and the Asia eHealth Information Network (AeHIN) participated in the launch of the Roadmap to 2030: Health for All in the Digital Age, outlining a five-year action agenda to strengthen the enabling environment for digital health, interoperability, and universal health coverage across Asia-Pacific countries

- In September 2025, at a high-level APEC health meeting, regional leaders emphasized the importance of harnessing digital innovation and technologies such as eHealth to strengthen healthcare systems and address demographic challenges such as aging populations and chronic disease burdens

- In June 2025, MEDITECH Asia Pacific showcased future-ready health technology at the Digital Health Festival 2025, where healthcare organizations demonstrated advanced digital solutions aimed at driving safer and smarter medication practices and integrated clinical workflows across the region

- In May 2024, a Bain & Company industry insight reported that telemedicine adoption in Asia-Pacific had nearly doubled during the COVID-19 period and continued to maintain high penetration post-pandemic, indicating lasting integration of virtual care into healthcare systems

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.