Asia Pacific Sternal Closure Systems Market

Размер рынка в млрд долларов США

CAGR :

%

USD

421.97 Million

USD

719.61 Million

2025

2033

USD

421.97 Million

USD

719.61 Million

2025

2033

| 2026 –2033 | |

| USD 421.97 Million | |

| USD 719.61 Million | |

| % | |

|

Asia-Pacific Sternal Closure Systems Market Segmentation, By Product (Closure Devices and Bone Cement), Procedure (Median Sternotomy, Hemisternotomy, and Bilateral Thoracosternotomy), Fixation Techniques (Wiring Fixation Techniques, Plate-Screw Systems, Interlocking Systems, Cementing, and Vacuum Assisted Closure), Material (Stainless Steel, PEEK, Titanium, and Others), End Users (Hospitals, and Specialized Surgical Centres)- Industry Trends and Forecast to 2033

Asia-Pacific Sternal Closure Systems Market Size

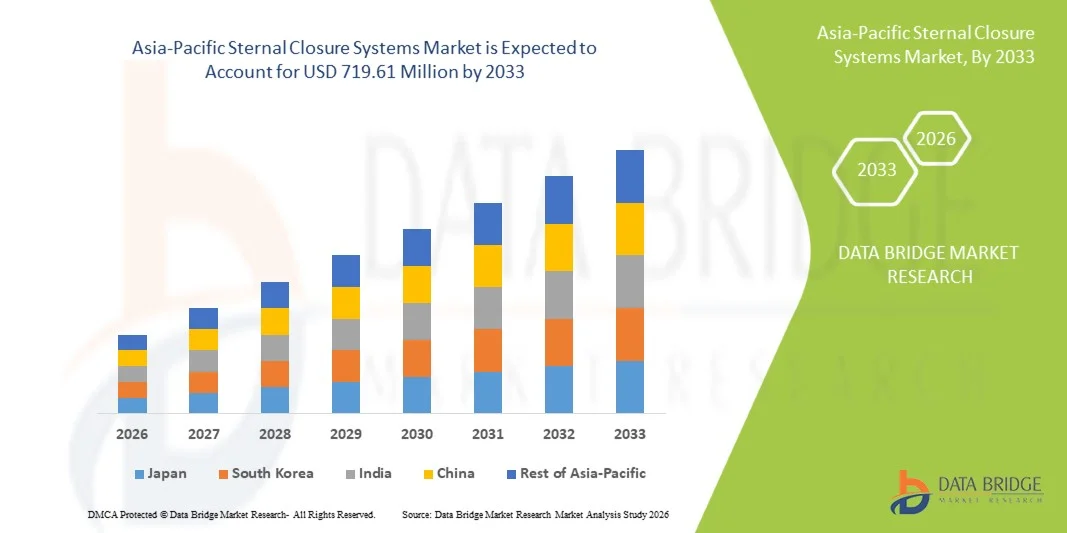

- The Asia-Pacific sternal closure systems market size was valued at USD 421.97 million in 2025 and is expected to reach USD 719.61 million by 2033, at a CAGR of 6.9% during the forecast period

- The market growth is largely driven by the rising number of cardiac surgeries, increasing prevalence of cardiovascular diseases, and expanding healthcare infrastructure across countries such as China, India, and Japan, fueling demand for advanced sternal fixation solutions

- Furthermore, growing awareness among surgeons about minimally invasive procedures, coupled with the adoption of innovative sternal closure devices that enhance patient recovery and reduce postoperative complications, is positioning these systems as the preferred choice in modern cardiac surgery. These converging factors are accelerating market adoption, thereby significantly boosting the industry's growth

Asia-Pacific Sternal Closure Systems Market Analysis

- Sternal closure systems, offering advanced fixation solutions for median sternotomy procedures, are increasingly vital components of modern cardiac surgery in both hospitals and specialty clinics due to their enhanced stability, reduced postoperative complications, and improved patient recovery outcomes

- The escalating demand for sternal closure systems is primarily fueled by the rising prevalence of cardiovascular diseases, increasing number of cardiac surgeries, and growing adoption of technologically advanced fixation devices that enhance surgical efficiency and patient safety

- Japan dominated the Asia-Pacific sternal closure systems market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, high cardiac surgery volumes, and a strong presence of key medical device companies, with hospitals witnessing substantial adoption of innovative sternal fixation solutions including rigid plate systems and minimally invasive devices

- China is expected to be the fastest growing country in the Asia-Pacific sternal closure systems market during the forecast period due to expanding healthcare infrastructure, increasing number of cardiac centers, and rising awareness among surgeons about improved fixation technologies that reduce postoperative complications

- Wiring Fixation Techniques segment dominated the sternal closure systems market with a market share of 45.4% in 2025, driven by its long-standing clinical reliability, cost-effectiveness, and ease of use in conventional cardiac procedures

Report Scope and Asia-Pacific Sternal Closure Systems Market Segmentation

|

Attributes |

Asia-Pacific Sternal Closure Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Sternal Closure Systems Market Trends

“Advancements Through Minimally Invasive and Rigid Plate Technologies”

- A significant and accelerating trend in the Asia-Pacific sternal closure systems market is the increasing adoption of minimally invasive surgical techniques combined with rigid plate fixation systems, enhancing postoperative recovery and reducing complication rates

- For instance, rigid plate systems allow precise sternal alignment and stabilization, improving outcomes in high-risk cardiac patients compared to traditional wire-based closure methods

- Surgeons are increasingly using innovative fixation solutions that incorporate bioresorbable materials and customizable plate designs, allowing patient-specific optimization and enhanced biomechanical stability

- These advanced systems facilitate faster recovery, reduce the risk of sternal dehiscence, and minimize hospital stays, aligning with the growing emphasis on value-based healthcare in the region

- This trend towards more sophisticated, patient-centric, and durable sternal closure solutions is driving product development among leading companies, with firms such as Biosorb and SternaTech developing next-generation plates and hybrid fixation devices

- The demand for advanced sternal closure systems is rising rapidly across hospitals and cardiac specialty centers, as healthcare providers prioritize improved surgical outcomes and patient safety

- Adoption of digital surgical planning and 3D modeling for sternal fixation procedures is emerging as a key trend, enabling surgeons to customize closure strategies and improve precision

Asia-Pacific Sternal Closure Systems Market Dynamics

Driver

“Increasing Cardiac Surgeries and Expanding Healthcare Infrastructure”

- The rising prevalence of cardiovascular diseases and the growing number of cardiac surgeries in Asia-Pacific countries is a significant driver for heightened demand for sternal closure systems

- For instance, in March 2025, Terumo Corporation reported increased adoption of its sternal fixation devices in Japan and India, aligning with expanding cardiac care facilities and advanced surgical programs

- Hospitals and cardiac centers are increasingly seeking technologically advanced sternal closure solutions that reduce complications, improve patient recovery, and support minimally invasive approaches

- Furthermore, government initiatives to improve healthcare infrastructure, particularly in China, India, and South Korea, are increasing access to advanced surgical tools and devices

- The need for efficient, reliable, and safe fixation systems, coupled with rising awareness among surgeons, is driving the adoption of both wire-based and rigid plate systems across public and private hospitals in the region

- Rising investments by private healthcare providers in cardiac surgery programs are expanding the adoption of advanced sternal closure devices

- Training programs and workshops for surgeons on minimally invasive sternal fixation techniques are increasing, boosting confidence and adoption rates in advanced closure systems.

Restraint/Challenge

“High Device Cost and Regulatory Compliance Hurdles”

- The relatively high cost of advanced sternal closure systems compared to traditional wire-based methods poses a significant challenge to broader market penetration, especially in price-sensitive markets within Asia-Pacific

- For instance, premium rigid plate systems can be financially restrictive for smaller hospitals or clinics in developing countries, limiting adoption despite clinical benefits

- Regulatory approval requirements across different countries in the region, such as Japan, India, and China, can delay product launches and add to compliance costs, posing a challenge for manufacturers

- Hospitals may be hesitant to adopt newer technologies until sufficient clinical evidence and cost-effectiveness data are available, slowing market growth in certain areas

- Overcoming these challenges through strategic pricing, localized manufacturing, and faster regulatory approvals will be vital for sustained adoption and expansion of sternal closure systems in Asia-Pacific

- Lack of awareness among surgeons in smaller cities and rural hospitals regarding advanced closure technologies can limit market penetration

- Supply chain disruptions and limited availability of raw materials for advanced fixation devices can temporarily affect production and distribution in the region

Asia-Pacific Sternal Closure Systems Market Scope

The market is segmented on the basis of product, procedure, fixation technique, material, and end users.

- By Product

On the basis of product, the Asia-Pacific sternal closure systems market is segmented into closure devices and bone cement. The closure devices segment dominated the market in 2025 with the largest revenue share of 62%, driven by their widespread adoption in cardiac surgeries across hospitals and specialized surgical centers. These devices, including wires and rigid plates, are preferred for their proven reliability, ease of use, and compatibility with standard median sternotomy procedures. Surgeons favor closure devices because they minimize operative time and reduce the risk of sternal instability post-surgery. The segment also benefits from continuous technological advancements, such as pre-shaped plates and bioresorbable materials, enhancing fixation outcomes. In addition, closure devices are integral to both traditional and minimally invasive procedures, making them versatile and highly demanded across the region.

The bone cement segment is expected to witness the fastest growth, with a projected CAGR of 10.2% from 2026 to 2033. Bone cement is increasingly used to augment sternal fixation in high-risk patients, such as the elderly or osteoporotic individuals, providing additional stability and reducing complications such as sternal dehiscence. Its growing adoption is fueled by surgeon awareness of improved postoperative outcomes and integration with hybrid fixation techniques. Bone cement is also gaining traction in emerging markets due to its cost-effectiveness compared to advanced plate systems.

- By Procedure

On the basis of procedure, the market is segmented into median sternotomy, hemisternotomy, and bilateral thoracosternotomy. The median sternotomy segment dominated in 2025, accounting for the largest share of 68%, as it remains the standard approach for open-heart surgeries across Asia-Pacific. Its dominance is driven by the high volume of cardiac procedures, including coronary artery bypass grafting and valve replacements. The procedure’s compatibility with both wire-based and plate fixation systems ensures wide usage of sternal closure devices. In addition, median sternotomy allows for straightforward postoperative monitoring and intervention, reinforcing its preference among surgeons. The segment benefits from growing investments in cardiac surgery infrastructure in countries such as Japan, China, and India. Hospitals increasingly prioritize proven, reliable closure solutions that complement this conventional procedure.

The hemisternotomy segment is expected to grow at the fastest CAGR of 9.6% during 2026–2033. Minimally invasive hemisternotomy is gaining adoption due to reduced surgical trauma, shorter hospital stays, and quicker patient recovery. It is particularly preferred in specialized cardiac centers where patient outcomes and cosmetic results are critical. The segment’s growth is also driven by increasing surgeon expertise and availability of dedicated fixation devices designed for partial sternotomy approaches.

- By Fixation Technique

On the basis of fixation technique, the market is segmented into wiring fixation techniques, plate-screw systems, interlocking systems, cementing, and vacuum-assisted closure. The wiring fixation techniques segment dominated in 2025 with a market share of 45.4%, owing to its long-standing clinical reliability, cost-effectiveness, and ease of implementation in conventional cardiac surgeries. Wires provide sufficient mechanical stability for the majority of patients undergoing median sternotomy and are preferred for routine procedures in both public and private hospitals. Their dominance is reinforced by surgeon familiarity and widespread availability across Asia-Pacific. The segment also benefits from incremental innovations, such as reinforced wires and pre-twisted configurations, improving postoperative outcomes.

The plate-screw systems segment is expected to witness the fastest growth at a CAGR of 11.5% during the forecast period. Rigid plate fixation provides superior stability, particularly in high-risk patients or redo cardiac surgeries. Growing adoption is driven by improved patient outcomes, lower rates of sternal non-union, and compatibility with minimally invasive surgical approaches. Surgeons increasingly prefer plate systems for complex cases where traditional wiring may not provide adequate mechanical support.

- By Material

On the basis of material, the market is segmented into stainless steel, PEEK, titanium, and others. The stainless steel segment dominated in 2025 with a market share of 60%, owing to its high strength, cost-effectiveness, and long-standing clinical use in sternal fixation. Stainless steel is widely available and compatible with both wire and plate fixation systems, making it the first choice for conventional cardiac procedures. Hospitals across Asia-Pacific rely on stainless steel due to its reliability, ease of handling during surgery, and proven postoperative performance. Surgeons are well-acquainted with its properties, ensuring predictable surgical outcomes. Incremental innovations, such as corrosion-resistant coatings, have further strengthened its market position.

The titanium segment is expected to register the fastest growth with a CAGR of 10.8% from 2026 to 2033. Titanium is favored for its superior biocompatibility, lightweight nature, and corrosion resistance, especially in rigid plate systems. Its adoption is increasing in premium cardiac centers and specialized surgical hospitals focused on minimally invasive approaches and enhanced patient outcomes. Surgeons prefer titanium plates for their mechanical strength and reduced risk of long-term complications.

- By End Users

On the basis of end users, the market is segmented into hospitals and specialized surgical centers. The hospitals segment dominated the market in 2025 with a revenue share of 70%, driven by the high volume of cardiac surgeries conducted in tertiary care and multi-specialty hospitals. Hospitals prefer standardized sternal closure devices and wiring techniques due to ease of procurement, cost-effectiveness, and compatibility with various surgical procedures. Large hospitals also invest in advanced plate-screw systems for high-risk or complex cases. The segment benefits from increasing cardiac surgery infrastructure, government support, and expanding hospital networks across Asia-Pacific.

The specialized surgical centers segment is expected to witness the fastest growth with a CAGR of 12% from 2026 to 2033. These centers focus on minimally invasive surgeries, complex cardiac cases, and elective procedures, driving the adoption of advanced sternal closure solutions, including rigid plate systems and hybrid fixation devices. Surgeons in specialized centers prioritize cutting-edge technologies that enhance patient recovery and reduce postoperative complications. The segment growth is also supported by increasing private investments and specialized cardiac care programs in countries such as China, Japan, and India.

Asia-Pacific Sternal Closure Systems Market Regional Analysis

- Japan dominated the Asia-Pacific sternal closure systems market with the largest revenue share of 28.5% in 2025, characterized by advanced healthcare infrastructure, high cardiac surgery volumes, and a strong presence of key medical device companies

- Hospitals and cardiac centers in Japan prioritize technologically advanced closure systems, including rigid plate and hybrid fixation solutions, due to their proven reliability, improved patient outcomes, and reduced postoperative complications

- This widespread adoption is further supported by increasing investments in cardiac care programs, availability of trained cardiac surgeons, and rising awareness about minimally invasive and rigid plate fixation techniques, establishing Japan as the leading country for sternal closure systems in the region

The Japan Sternal Closure Systems Market Insight

The Japan sternal closure systems market is gaining momentum due to the country’s advanced healthcare infrastructure, high cardiac surgery volumes, and emphasis on technological innovation. Hospitals and cardiac centers prioritize rigid plate systems and hybrid fixation solutions for better postoperative outcomes and reduced complications. In addition, Japan’s aging population and increasing demand for minimally invasive procedures are driving the adoption of sophisticated sternal closure devices in both public and private hospitals. Integration of next-generation fixation technologies and bioresorbable materials further supports market growth.

China Sternal Closure Systems Market Insight

The China sternal closure systems market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, increasing number of cardiac surgeries, and rising awareness of advanced sternal fixation techniques. Government initiatives to expand healthcare infrastructure and improve cardiac care facilities are promoting the adoption of both wire-based and rigid plate systems. The market is also benefiting from growing domestic production of sternal closure devices, making high-quality products more accessible and cost-effective. Increasing investments in specialized cardiac centers further boost demand.

India Sternal Closure Systems Market Insight

The India sternal closure systems market is expected to grow at a substantial CAGR during the forecast period, fueled by rising cardiovascular disease prevalence, expanding hospital infrastructure, and increasing awareness among surgeons regarding advanced fixation technologies. The country’s growing private healthcare sector and push towards specialized cardiac care are supporting the adoption of both conventional wire systems and rigid plate fixation solutions. In addition, government initiatives promoting cardiac surgery programs, along with increasing affordability and availability of modern devices, are driving the market.

South Korea Sternal Closure Systems Market Insight

The South Korea sternal closure systems market is witnessing steady growth due to high-quality healthcare infrastructure, advanced surgical practices, and increasing investments in cardiac care programs. Hospitals and cardiac centers in South Korea are adopting rigid plate and hybrid fixation systems to improve patient outcomes and minimize postoperative complications. The rising demand for minimally invasive procedures and the adoption of next-generation sternal closure technologies are further fueling market expansion.

Asia-Pacific Sternal Closure Systems Market Share

The Asia-Pacific Sternal Closure Systems industry is primarily led by well-established companies, including:

- Zimmer Biomet. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- B. Braun SE (Germany)

- KLS Martin Group (Germany)

- Acumed LLC (U.S.)

- Kinamed Incorporated (U.S.)

- Stryker (U.S.)

- Teleflex Incorporated (U.S.)

- JEIL Medical Corporation (South Korea)

- Arthrex, Inc. (U.S.)

- A&E Medical Corporation (U.S.)

- Jace Medical, LLC (U.S.)

- Able Medical Devices (U.S.)

- Praesidia SRL (Italy)

- Dispomedica GmbH (Germany)

- Medicon eG (Germany)

- Orthofix Medical Inc. (U.S.)

- Abyrx, Inc. (U.S.)

- Idear SRL (Italy)

- Acute Innovations LLC (U.S.)

What are the Recent Developments in Asia-Pacific Sternal Closure Systems Market?

- In December 2025, a case report in Journal of Orthopaedic Case Reports detailed the successful use of a titanium locking plate for thoracoscopy‑assisted minimally invasive sternal osteosynthesis, demonstrating application of advanced rigid plate fixation in sternal body fracture repair with less invasive approaches

- In April 2025, Journal of Clinical Medicine published a study comparing polyethylene suture tapes vs. steel wires for sternal closure in cardiac patients, showing that suture tape systems significantly reduced infection and dehiscence rates, shortened closure time, and improved postoperative comfort highlighting innovation in closure materials and techniques

- In August 2024, DePuy Synthes Launches MatrixSTERNUM™ Fixation System, a next‑generation plate‑and‑screw sternal fixation system providing stronger locking strength, faster fixation workflow, and thinner plates to enhance chest stability after open‑heart surgery, representing a significant product introduction in closure hardware

- In October 2023, a retrospective study published in the Journal of Cardiothoracic Surgery reported that use of a three‑piece bioresorbable mesh plate technique for sternal closure reduced postoperative hemorrhage and improved chest stability following congenital and coronary surgery, indicating clinical benefits of mesh‑based fixation approaches

- In June 2021, researchers in Heart, Lung and Circulation described a novel sternal closure technique using an absorbable mesh (Super‑FIXSORB‑MX®40) combined with PDS cord for osteoporotic patients undergoing sternotomy, offering an alternative to traditional wire cerclage for enhanced stability in high‑risk bone conditions

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.