Europe Ambulatory Infusion Pumps Market

Размер рынка в млрд долларов США

CAGR :

%

USD

2.27 Billion

USD

4.69 Billion

2025

2033

USD

2.27 Billion

USD

4.69 Billion

2025

2033

| 2026 –2033 | |

| USD 2.27 Billion | |

| USD 4.69 Billion | |

| % | |

|

Europe Ambulatory Infusion Pumps Market Segmentation, By Product Type (Devices, and Accessories and Consumables), Usage (Disposable and Reusable), Route of Administration (Subcutaneous, Intravenous and Epidural), Application (Emergency Medicine, General Anaesthesia, Pain Management, Oncology, Diabetes, Gastroenterology, Neonatology, and Others), End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Home Care Settings and Others), Distribution Channel (Direct Tender and Retail Sales)- Industry Trends and Forecast to 2033

Европейский рынок амбулаторных инфузионных насосов

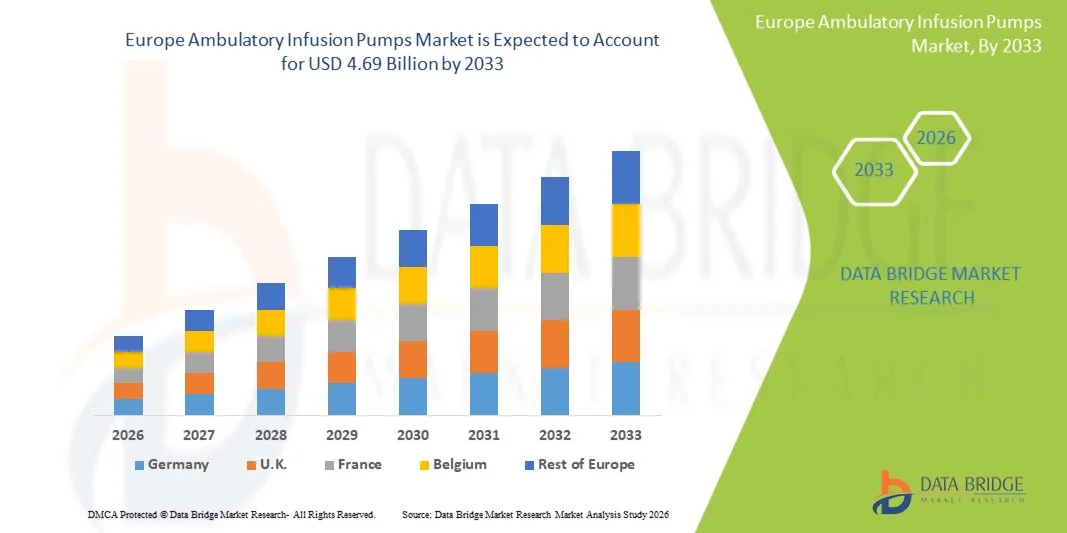

- Согласно анализу рынка Data Bridge Market Research, размер рынка амбулаторных инфузионных насосов в Европе был оценен как2,27 млрд долларов в 2025 годуОжидается, что он достигнет4,69 млрд долларов к 2033 году, вCAGR 9,5%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен растущим внедрением передовых систем доставки лекарств, ростом распространенности хронических заболеваний, требующих длительной инфузионной терапии, и расширением использования амбулаторных учреждений по всей Европе.

- Кроме того, растущий спрос на ориентированные на пациента, портативные и домашние инфузионные решения, наряду с технологическими достижениями в интеллектуальных и носимых инфузионных устройствах, стимулирует внедрение амбулаторных инфузионных насосов в больницах и амбулаторных учреждениях, тем самым значительно поддерживая расширение рынка.

Размер рынка и прогноз

- Глобальная рыночная стоимость (2025):2,27 млрд долларов в 2025 году

- Ожидаемая рыночная стоимость (2033):4,69 млрд долларов к 2033 году

- Прогноз CAGR (2026–2033):9.5%

Европейский анализ рынка амбулаторных инфузионных насосов

- Амбулаторные инфузионные насосы, предназначенные для доставки контролируемых и непрерывных лекарств вне больничных учреждений, становятся все более важными в системе здравоохранения Европы из-за их роли в обеспечении долгосрочных методов лечения, улучшении мобильности пациентов и поддержке перехода к домашним и амбулаторным моделям лечения.

- Растущий спрос на амбулаторные инфузионные насосы в первую очередь обусловлен растущей распространенностью хронических заболеваний, таких как рак, диабет и аутоиммунные расстройства, а также растущим предпочтением минимально инвазивных и портативных решений для доставки лекарств в больницах и учреждениях по уходу на дому.

- Германия доминировала на рынке амбулаторных инфузионных насосов с самой большой долей дохода 27,8% в 2025 году, поддерживаемой передовой инфраструктурой здравоохранения, сильным внедрением инфузионных технологий и широким использованием в онкологии, лечении боли и лечении диабета.

- Ожидается, что Великобритания станет самой быстрорастущей страной на рынке амбулаторных инфузионных насосов в течение прогнозируемого периода из-за растущего расширения настроек домашнего ухода, растущего спроса на модели амбулаторного лечения и растущего использования портативных инфузионных систем при лечении хронических заболеваний.

- Сегмент применения онкологии доминировал на рынке в 2025 году с долей 32,4%, что обусловлено высокой распространенностью рака и растущим использованием амбулаторных инфузионных насосов для доставки химиотерапии.

Сфера охвата и сегментация рынка амбулаторных инфузионных насосов Европы

|

Атрибуты |

Европа амбулаторные инфузионные насосы ключевые рыночные идеи |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Европа

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают углубленный экспертный анализ, эпидемиологию пациентов, анализ трубопроводов, анализ цен и нормативную базу. |

Европейские тенденции рынка амбулаторных инфузионных насосов

«Растущий сдвиг в сторону портативных, интеллектуальных и систем доставки лекарств для пациентов»

- Значительной и ускоряющейся тенденцией на европейском рынке амбулаторных инфузионных насосов является растущее внедрение портативных и носимых инфузионных систем, интегрированных с цифровыми функциями мониторинга, повышение мобильности пациентов и непрерывности лечения в домашних условиях и клинических условиях.

- Например, современные эластомерные и электронные амбулаторные насосы широко используются в Европе для химиотерапии и лечения боли, что позволяет пациентам получать терапию за пределами больниц, сохраняя точность и безопасность дозирования.

- Интеграция инфузионных насосов с поддержкой подключенияудаленный мониторингиЭлектронные медицинские записиУлучшает отслеживание терапии, позволяя клиницистам контролировать соблюдение дозировки и реакцию пациентов в режиме реального времени в сетях здравоохранения.

- Бесшовный переход инфузионной терапии из больниц в стационары облегчает децентрализованные модели лечения, позволяя поставщикам медицинских услуг снизить больничную нагрузку, одновременно повышая комфорт пациентов и эффективность долгосрочного ухода.

- Расширение внедрения одноразовых и одноразовых амбулаторных инфузионных насосов снижает риски заражения и упрощает администрирование терапии, особенно в амбулаторных и послеоперационных условиях по всей Европе.

- Эта тенденция к более интеллектуальным, легким и домашним инфузионным системам коренным образом меняет ожидания в отношении доставки лечения в Европе, поскольку компании все чаще разрабатывают удобные, программируемые и безопасные амбулаторные устройства.

- Спрос на передовые амбулаторные инфузионные насосы быстро растет в приложениях для онкологии, диабета и лечения боли, поскольку системы здравоохранения все чаще отдают приоритет амбулаторной помощи и экономически эффективной доставке лечения.

Динамика рынка амбулаторных инфузионных насосов Европы

водитель

«Растущее бремя хронических заболеваний и расширение медицинских услуг на дому»

- Растущая распространенность хронических заболеваний, таких как рак, диабет и желудочно-кишечные расстройства, в сочетании с растущим спросом на долгосрочную инфузионную терапию, является основным фактором, ускоряющим внедрение амбулаторных инфузионных насосов по всей Европе.

- Например, поставщики медицинских услуг по всей Европе все чаще используют амбулаторные насосы для химиотерапии и доставки инсулина в амбулаторных условиях и на дому, чтобы улучшить удобство пациентов и сократить продолжительность пребывания в больнице.

- По мере того, как системы здравоохранения переходят на модели ухода, основанные на стоимости, амбулаторные инфузионные насосы все чаще предпочитают за их способность обеспечивать непрерывное и контролируемое введение лекарств за пределами традиционных больничных сред.

- Кроме того, растущий акцент на снижении нагрузки на инфраструктуру здравоохранения и улучшении качества жизни пациентов стимулирует внедрение портативных инфузионных технологий в больницах, специализированных клиниках и учреждениях по уходу на дому.

- Удобство программируемого контроля дозировки, улучшенная мобильность пациентов и снижение риска внутрибольничных инфекций являются ключевыми факторами, способствующими широкому использованию амбулаторных инфузионных насосов в Европе.

- Увеличение инвестиций в услуги здравоохранения на дому и политика вспомогательного возмещения еще больше укрепляют проникновение на рынок основных европейских систем здравоохранения.

- Растущее внедрение специализированных методов лечения, таких как онкология и целевая доставка лекарств, еще больше повышает спрос на системы точной амбулаторной инфузии в больницах и амбулаторных центрах.

- Расширение использования подкожных инфузионных методов лечения диабета и лечения боли ускоряет переход к форматам амбулаторных родов по всей Европе.

Сдержанность/вызов

«Высокая стоимость оборудования и опасения по поводу эксплуатационной сложности и рисков безопасности»

- Опасения, связанные с высокой стоимостью передовых систем амбулаторных инфузионных насосов, наряду с расходами на техническое обслуживание и расходные материалы, представляют собой серьезную проблему для более широкого проникновения на рынок в чувствительных к цене сегментах здравоохранения в Европе.

- Например, современные носимые и электронные инфузионные насосы с программируемыми функциями часто значительно дороже, чем обычные инфузионные системы, что ограничивает внедрение в небольших медицинских учреждениях и учреждениях по уходу на дому.

- Операционная сложность и потребность в квалифицированных медицинских работниках для управления программированием дозировки и калибровкой устройства могут увеличить риск ошибок при приеме лекарств, создавая колебания среди некоторых конечных пользователей.

- Кроме того, риски, связанные с неправильной доставкой дозы, неисправностью устройства или ошибками обращения с пользователем, остаются проблемой, особенно в домашних условиях, где прямой клинический надзор ограничен.

- Нормативно-правовые требования к соблюдению стандартов безопасности инфузионных устройств в европейских странах добавляют дополнительное время утверждения и бремя затрат для производителей, замедляя коммерциализацию продукта.

- Проблемы конфиденциальности данных и кибербезопасности, связанные с подключенными инфузионными системами, становятся все более распространенными в больничных сетях.

- В то время как производители внедряют упрощенные интерфейсы и конструкции, повышающие безопасность, воспринимаемая сложность передовых инфузионных систем по-прежнему служит барьером для широкого внедрения в определенных условиях ухода.

- Решение этих проблем путем оптимизации затрат, улучшения обучения пользователей, более строгого регулирования и улучшения функций безопасности устройств будет иметь решающее значение для устойчивого роста рынка амбулаторных инфузионных насосов в Европе.

Европейский рынок амбулаторных инфузионных насосов

Рынок сегментируется на основе типа продукта, использования, маршрута администрирования, приложения, конечного пользователя и канала распространения.

- Тип продукта

Исходя из типа продукта, европейский рынок амбулаторных инфузионных насосов сегментирован на устройства, аксессуары и расходные материалы. Сегмент устройств доминировал на рынке с самой большой долей выручки в 62,8% в 2025 году, что обусловлено высоким внедрением электронных и эластомерных инфузионных насосов в больницах и домашних условиях. Эти устройства составляют основу доставки терапии, предлагая программируемые скорости инфузии, переносимость и улучшенное соответствие пациентов в долгосрочных методах лечения. Расширение использования передовых инфузионных технологий в онкологии и лечении боли еще больше усиливает спрос на устройства по всей Европе. Кроме того, постоянные инновации в легких и носимых конструкциях насосов усиливают клиническое внедрение в амбулаторное лечение. Сильное предпочтение многоразовых и интеллектуальных инфузионных систем также вносит значительный вклад в доминирование этого сегмента.

Ожидается, что в сегменте аксессуаров и расходных материалов будет наблюдаться самый быстрый рост на 8,9% с 2026 по 2033 год, чему способствует постоянный спрос на инфузионные наборы, трубки, картриджи и одноразовые компоненты. Растущее использование одноразовых расходных материалов для снижения риска заражения в домашних условиях и больницах является ключевым фактором роста. Увеличение числа длительных методов лечения, особенно в онкологии и диабете, способствует повторным покупкам расходных материалов. Кроме того, расширение домашних медицинских услуг увеличивает зависимость от простых в использовании одноразовых аксессуаров. Растущий акцент на стандартах безопасности и гигиены пациентов в Европе также ускоряет спрос. Непрерывные инновации в экономически эффективных и стерильных расходных материалах способствуют дальнейшему расширению сегмента.

- Используя

На основе использования рынок сегментирован на одноразовые и многоразовые инфузионные насосы. Сегмент многоразового использования доминировал на рынке с долей выручки 58,3% в 2025 году, что обусловлено его экономической эффективностью для долгосрочного использования в больницах и совместимостью с несколькими циклами терапии. Многоразовые насосы широко используются в больницах и специализированных клиниках для контролируемой доставки лекарств в онкологии, управлении болью и приложениях критической помощи. Их способность поддерживать нескольких пациентов в течение долгого времени делает их высокоэффективными в институциональных условиях. Наличие известных производителей медицинских изделий, предлагающих долговечные и программируемые системы, еще больше укрепляет этот сегмент. Кроме того, расширенные функции безопасности и возможности точного дозирования увеличивают их предпочтение в клинических условиях.

Ожидается, что в сегменте одноразовой терапии будет наблюдаться самый быстрый рост на 10,2% с 2026 по 2033 год, что обусловлено растущим спросом на инфекционный контроль и упрощенные решения для терапии на дому. Одноразовые насосы все чаще используются в послеоперационном и амбулаторном лечении из-за их простоты использования и устранения рисков перекрестного загрязнения. Рост услуг по домашнему здравоохранению в Европе значительно способствует внедрению одноразовых устройств. Кроме того, увеличение предпочтения пациента безболезненной инфузионной терапии без обслуживания устройства ускоряет спрос. Повышение осведомленности о приобретенных в больницах инфекциях еще больше расширяет использование. Постоянные достижения в области недорогих одноразовых насосных технологий также способствуют быстрому росту рынка.

- По маршруту администрации

На основе пути введения рынок сегментирован на подкожный, внутривенный и эпидуральный. Внутривенный сегмент доминировал на рынке с долей дохода 49,6% в 2025 году, что обусловлено его широким использованием в химиотерапии, антибиотикотерапии и инфузионном лечении. Внутривенное введение обеспечивает быструю и контролируемую доставку лекарств, что делает его предпочтительным методом в больницах и специализированных клиниках. Широкое распространение онкологии в Европе значительно поддерживает доминирование этого сегмента. Увеличение использования программируемых инфузионных насосов для IV терапии повышает точность дозирования и безопасность пациента. Кроме того, установленные клинические протоколы для доставки лекарств внутривенно способствуют его высокому уровню использования.

Ожидается, что в подкожном сегменте будет наблюдаться самый быстрый рост на 9,8% с 2026 по 2033 год, что обусловлено растущим внедрением методов лечения диабета и долгосрочной терапии боли. Подкожная инфузия облегчает лечение на дому, уменьшая зависимость от посещений больницы. Растущее предпочтение малоинвазивных методов доставки лекарств значительно способствует их принятию. Расширение технологий носимых инфузионных насосов еще больше повышает возможность подкожного введения. Растущее бремя хронических заболеваний в Европе также поддерживает рост сегмента. Кроме того, улучшение комфорта и удобства пациентов по сравнению с внутривенными методами ускоряет их принятие.

- С помощью приложения

На основе применения рынок сегментирован в экстренную медицину, общую анестезию, обезболивание, онкологию, диабет, гастроэнтерологию, неонатологию и другие. Сегмент онкологии доминировал на рынке с долей выручки 32,4% в 2025 году, что обусловлено высокой распространенностью рака и увеличением использования амбулаторных инфузионных насосов для химиотерапии. Амбулаторные насосы обеспечивают непрерывную и контролируемую доставку лекарств, улучшая результаты лечения и уменьшая пребывание в больнице. Широкое внедрение целевых методов лечения рака, требующих точного дозирования, еще больше поддерживает этот сегмент. Растущий сдвиг в сторону амбулаторной онкологической помощи в Европе также повышает спрос. Кроме того, технологические достижения в портативных инфузионных системах повышают эффективность лечения при лечении рака.

Ожидается, что в сегменте диабета будет наблюдаться самый быстрый темп роста в 10,5% с 2026 по 2033 год, что обусловлено ростом распространенности диабета в Европе и увеличением спроса на инфузионную терапию инсулином. Амбулаторные инфузионные насосы обеспечивают лучший гликемический контроль по сравнению с традиционными методами доставки инсулина. Растущее внедрение носимых и портативных устройств позволяет пациентам более независимо управлять диабетом. Повышение осведомленности о преимуществах непрерывной инфузии инсулина еще больше способствует расширению сегмента. Расширение настроек домашнего ухода также ускоряет принятие. Кроме того, интеграция интеллектуальных функций мониторинга улучшает приверженность лечению и стимулирует рост.

- Конечный пользователь

На базе конечного пользователя рынок сегментирован на больницы, специализированные клиники, амбулаторные хирургические центры, настройки домашнего ухода и другие. Сегмент больниц доминировал на рынке с долей дохода 45,1% в 2025 году, что обусловлено высоким притоком пациентов, требующих инфузионной терапии в онкологии, неотложной помощи и хирургических процедурах. Больницы являются основными центрами внедрения передовых инфузионных насосов из-за наличия квалифицированных медицинских работников. Сильные закупки высококачественных устройств через институциональные закупки еще больше поддерживают доминирование. Увеличение использования инфузионных насосов в реанимации и послеоперационном управлении также способствует спросу. Кроме того, налаженная инфраструктура для комплексного введения лекарственных средств расширяет использование больниц.

Ожидается, что в сегменте услуг по уходу на дому будет наблюдаться самый быстрый рост на 11,3% с 2026 по 2033 год, что обусловлено быстрым переходом к децентрализованной доставке медицинских услуг в Европе. Растущее предпочтение лечения хронических заболеваний на дому значительно стимулирует усыновление. Амбулаторные инфузионные насосы позволяют пациентам поддерживать подвижность при длительной терапии. Растущее давление на расходы на здравоохранение поощряет усыновление на дому. Увеличение доступности удобных носимых устройств еще больше поддерживает эту тенденцию. Кроме того, поддержка политики возмещения расходов на услуги здравоохранения на дому ускоряет рост сегмента.

- Дистрибьюторский канал

На основе канала дистрибуции рынок сегментируется на прямые тендерные и розничные продажи. Сегмент прямых тендеров доминировал на рынке с долей выручки 67,9% в 2025 году, чему способствовали крупномасштабные закупки больниц и государственных систем здравоохранения по всей Европе. Прямые торги обеспечивают массовую закупку инфузионных насосов по согласованным ценам, что делает их экономически эффективными для институциональных покупателей. Существенное присутствие инфраструктуры общественного здравоохранения в Европе значительно поддерживает этот сегмент. Увеличение спроса со стороны больниц на стандартизированные и высококачественные устройства еще больше стимулирует закупки через тендеры. Кроме того, долгосрочные контракты с производителями повышают стабильность рынка.

Ожидается, что в сегменте розничных продаж будет наблюдаться самый быстрый рост на 9,6% с 2026 по 2033 год, что обусловлено растущим внедрением инфузионной терапии на дому и повышением осведомленности потребителей. Пациенты все чаще приобретают амбулаторные инфузионные насосы через медицинские розничные каналы для личного использования. Рост распространения медицинских устройств в электронной коммерции еще больше ускоряет доступность. Растущее предпочтение самостоятельного лечения хронических заболеваний также способствует расширению розничной торговли. Кроме того, доступность упрощенных и портативных устройств способствует прямому внедрению в жизнь потребителей. Расширение экосистемы домашнего здравоохранения в Европе способствует быстрому росту сегмента.

Европейский рынок амбулаторных инфузионных насосов Региональный анализ

- Германия доминировала на рынке амбулаторных инфузионных насосов с самой большой долей дохода 27,8% в 2025 году, поддерживаемой передовой инфраструктурой здравоохранения, сильным внедрением инфузионных технологий и широким использованием в онкологии, лечении боли и лечении диабета.

- Поставщики медицинских услуг в стране высоко ценят точность, переносимость и улучшенные результаты лечения пациентов, предлагаемые амбулаторными инфузионными насосами, особенно в онкологических, диабетических и болеутоляющих приложениях в больницах и специализированных учреждениях.

- Это широкое внедрение также поддерживается сильной политикой возмещения, высокими расходами на здравоохранение и растущим акцентом на децентрализованные модели ухода, устанавливая амбулаторные инфузионные насосы в качестве ключевого компонента современной инфраструктуры лечения Германии.

Немецкий рынок амбулаторных инфузионных насосов

Рынок амбулаторных инфузионных насосов в Германии занял самую большую долю дохода в 27,8% в Европе в 2025 году, чему способствовала высокоразвитая система здравоохранения, широкое внедрение медицинских технологий и растущий спрос на домашние и амбулаторные инфузионные методы лечения. Немецкие поставщики медицинских услуг придают большое значение точной доставке лекарств, безопасности пациентов и эффективности лечения в области онкологии, диабета и лечения боли. Растущий акцент на сокращение пребывания в больницах и улучшение управления хроническими заболеваниями еще больше ускоряет принятие. Кроме того, прочная система возмещения расходов и хорошо налаженная инфраструктура больниц в значительной степени способствуют проникновению на рынок.

Британский рынок амбулаторных инфузионных насосов

Ожидается, что рынок амбулаторных инфузионных насосов в Великобритании в течение прогнозируемого периода будет расти с заметным CAGR, что обусловлено растущим переходом к домашнему здравоохранению, растущим бременем хронических заболеваний и растущим спросом на экономически эффективные решения для амбулаторного лечения. Поставщики медицинских услуг все чаще используют портативные инфузионные системы для повышения комфорта пациентов и снижения зависимости от больницы. Сильная экосистема цифрового здравоохранения в стране и сосредоточение внимания на уходе на уровне общин еще больше способствуют принятию. Кроме того, растущие инвестиции в программы ухода на дому под руководством NHS ускоряют расширение рынка в нескольких терапевтических областях.

Рынок амбулаторных инфузионных насосов Франции

Ожидается, что в течение прогнозируемого периода рынок амбулаторных инфузионных насосов во Франции будет расширяться при значительном CAGR, чему будет способствовать растущая осведомленность о передовых системах доставки лекарств и растущее внедрение моделей ухода на дому. Система здравоохранения страны все больше фокусируется на сокращении заторов в больницах и повышении эффективности лечения хронических заболеваний. Растущий спрос на амбулаторную химиотерапию и лечение боли еще больше стимулирует рост рынка. Кроме того, политика возмещения расходов и расширение инфраструктуры амбулаторной помощи способствуют внедрению в больницах и специализированных клиниках.

Итальянский рынок амбулаторных инфузионных насосов

Рынок амбулаторных инфузионных насосов в Италии демонстрирует устойчивый рост, обусловленный увеличением распространенности хронических заболеваний и растущим спросом на долгосрочную инфузионную терапию как в больницах, так и на дому. Медицинские работники все чаще переходят на портативные инфузионные системы для повышения мобильности пациентов и снижения расходов на госпитализацию. Расширение пожилого населения, нуждающегося в постоянном введении наркотиков, также поддерживает спрос на рынке. Кроме того, постепенная модернизация инфраструктуры здравоохранения и растущее внедрение амбулаторных услуг способствуют расширению рынка.

Доля рынка амбулаторных инфузионных насосов Европы

Индустрия амбулаторных инфузионных насосов в Европе в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- B. Braun SE (Германия)

- Fresenius Kabi AG (Германия)

- Бакстер (США)

- ICU Medical, Inc. (США)

- BD (США)

- Smiths Group PLC (Великобритания)

- Terumo Corporation (Япония)

- Medtronic (Ирландия)

- NIPRO Corporation (Япония)

- Vygon SA (Франция)

- Micrel Medical Devices S.A. (Греция)

- Caesarea Medical Electronics Ltd. (Израиль)

- Eitan Medical Ltd. (Израиль)

- Moog Inc. (США)

- Zyno Medical LLC (США)

- Arcomed AG (Швейцария)

- Fresenius Kabi Deutschland GmbH (Германия)

- Tricumed Medizintechnik GmbH (Германия)

- Компания Mindray Medical International Limited (Китай)

Каковы последние события на европейском рынке амбулаторных инфузионных насосов

- В феврале 2025 года Baxter International объявила об обновлениях, связанных с работой инфузионных насосов, включая продолжающиеся проблемы регулирования и цепочки поставок, влияющие на портфель инфузионных систем, используемых в больницах и амбулаторных учреждениях в Европе.

- В октябре 2024 года компания B. Braun Medical расширила производственные мощности по производству инфузионной терапии, увеличив выпуск систем IV, трубок и сопутствующих расходных материалов, используемых с амбулаторными инфузионными насосами на мировых рынках, включая Европу.

- В июне 2024 года европейские больницы все чаще внедряют интеллектуальные системы инфузионных насосов следующего поколения с программным обеспечением для снижения дозовых ошибок и функциями беспроводной связи. Эти системы были интегрированы в ИТ-инфраструктуру больницы, чтобы повысить безопасность лекарств, уменьшить инфузионные ошибки и обеспечить мониторинг в режиме реального времени в приложениях критической помощи и онкологии.

- В марте 2024 года Fresenius Kabi укрепила свой портфель инфузионной терапии в Европе, расширив доступность передовых электронных инфузионных систем и сопутствующих расходных материалов, используемых в больницах и амбулаторных учреждениях.

- В сентябре 2023 года программы домашнего здравоохранения по всей Европе расширили использование амбулаторных инфузионных насосов для амбулаторного лечения рака, инфекций и лечения боли. Поставщики медицинских услуг все чаще переводят пациентов из больниц на домашние модели ухода с использованием портативных инфузионных систем для повышения комфорта и снижения нагрузки на систему здравоохранения.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.